You're probably here because you're at a professional fork in the road. Maybe you want a career that's more stable than sales, more analytical than general customer service, and more meaningful than moving tickets from one queue to another. Or maybe you've already touched insurance from the edge, in restoration, roofing, construction, legal support, medical billing, or property operations, and you want to know whether claims management jobs are a real career path or just another broad job-board label.

They're a real path. A large one.

The insurance industry supported some 3.0 million U.S. jobs in 2025, including about 389,000 claims adjusters, appraisers, examiners, and investigators, according to the Insurance Information Institute's employment overview. That matters because it tells you claims work isn't a side function tucked behind underwriting. It's a core operating discipline.

What most guides miss is that “claims management jobs” can point in two very different directions. One path puts you inside a carrier, managing claim files on behalf of the insurer. The other puts you on the policyholder side as a public adjuster, where your job is to document damage, interpret coverage, and negotiate for the insured. If you're in Oregon or Washington and you're drawn to property losses, that second path deserves more attention than it usually gets.

Is a Career in Claims Management Right for You

Claims work fits people who can stay calm when someone else's day has gone sideways. A claim usually starts when a person, family, business, or nonprofit has already taken a hit. Water got in. A vehicle was damaged. A worker was hurt. A roof failed after a storm. The file may be procedural on paper, but to the person living through it, it's personal.

That's why the wrong people burn out fast. If you need constant novelty without process, or if you hate documenting your decisions, claims will frustrate you. If you like gathering facts, comparing versions of events, reading policy language, and making a file stand up under scrutiny, you'll have a much better shot.

The work has scale and staying power

Claims management jobs sit inside a massive industry, not a tiny specialty. The broader workforce context matters because it supports multiple entry points, from administrative support roles to field investigation to complex resolution work. If you're trying to break in, it helps to understand that claims departments need intake, documentation, coverage review, inspection, negotiation, and follow-up.

For people exploring related paths, workers' compensation adjuster roles are one example of how specialized claims tracks can become long-term careers.

Practical rule: If you want a claims career that lasts, don't choose it because you “like helping people” alone. Choose it because you can help people while handling conflict, deadlines, documentation, and imperfect facts.

Carrier work and public adjusting are not the same job

A lot of job seekers lump all adjuster roles together. That's a mistake.

Carrier-side claims professionals work for the insurer. Their duty is to investigate, apply policy terms, evaluate exposure, and resolve the file within internal standards and state requirements.

Public adjusters work for the policyholder. In property claims, that usually means building the loss presentation, documenting damage, reviewing scope, valuing what was affected, and negotiating from the insured's side of the table.

Neither role is “easy.” They demand different instincts. Carrier work tends to train discipline, reserve thinking, and file structure. Public adjusting demands deep policyholder advocacy, damage documentation, and settlement strategy. If you care about property losses and want to represent insureds directly, public adjusting is one of the most overlooked answers to the question of where claims management jobs can lead.

Mapping Your Path in Claims Management Roles

Think of a claims operation like an emergency response team. Not everyone does the same job, and that's the point. One person triages the incoming problem. Another goes into the field. Another supervises strategy and exposure. A public adjuster often acts more like the policyholder's specialist, building the case from the outside rather than managing it inside the carrier.

Four common role types

The easiest way to choose your path is to ask where you do your best work.

- Claims examiner: Best for people who like file review, written analysis, policy application, and steady process control.

- Field adjuster: Best for people who don't want to sit behind a screen all day and can inspect, interview, and make judgment calls on site.

- Claims manager: Best for professionals who can coach others, enforce standards, and make tougher calls on complex files.

- Public adjuster: Best for people who know property damage, can build evidence, and want to advocate for insureds instead of carriers.

If you're still early in the process, insurance trainee positions are often the cleanest way to see which environment fits your temperament.

Comparison of Key Claims Management Roles

| Role | Primary Focus | Work Environment | Median Salary Range (2026 est.) | Best For |

|---|---|---|---|---|

| Claims Examiner | Coverage review, documentation, payment decisions, file handling | Mostly desk-based or hybrid | Varies by employer, line, and licensing | Detail-heavy analysts who like consistency |

| Field Adjuster | Inspection, interviews, on-site investigation, scope review | Travel, property visits, field meetings | Varies by territory, catastrophe work, and experience | People who prefer movement and direct observation |

| Claims Manager | Oversight, escalation handling, staffing, compliance, quality control | Office or hybrid leadership setting | Varies by organization size and claim complexity | Experienced adjusters ready to lead teams |

| Public Adjuster | Policyholder advocacy, damage documentation, valuation, negotiation | Fieldwork plus client meetings and file strategy | Varies by state rules, case mix, and fee structure | Property-focused professionals who want to represent insureds |

How to choose without wasting a year

Don't choose based on title alone. Choose based on daily friction.

If you hate ambiguity in the field, a field role can wear you down. If you hate repetitive documentation, examiner work will feel endless. If you don't want conflict, public adjusting and complex claims negotiation may not fit.

The people who last in claims aren't always the loudest or most polished. They're usually the ones who can separate facts from assumptions and keep moving the file.

A practical self-test helps:

- Read a messy situation carefully. Do you naturally start organizing facts?

- Write your conclusion down. Can you explain it clearly enough that another reviewer would follow your reasoning?

- Handle disagreement. Can you stay professional when the other side doesn't like the answer?

- Track details over time. Claims rarely resolve in one clean step.

Public adjusting deserves special mention here because it combines technical file work with advocacy. In Oregon and Washington, that matters. Property claims often turn on documentation quality, policy interpretation, timing, and how well the loss is presented. If you're the kind of person who wants your work to affect a real household, business, school, or nonprofit trying to recover after property damage, that path has weight.

A Day in the Life of a Claims Professional

Most new hires imagine claims work as a lot of phone calls and data entry. There is some of that. But once you move beyond the most basic files, the job becomes a sequence of judgment calls.

The file moves through four real tasks

A claims professional's day usually rotates through the same core functions, but the facts change every time.

First, there's investigation. In advanced roles, the work includes end-to-end investigation and liability analysis, and the professional must apply facts from research to decide claim validity, control exposure, and develop resolution strategy on complex matters, as outlined in Missouri's risk and claims management job family description. In property work, that can mean reviewing photos, comparing scope documents, checking cause of loss, talking with contractors, and figuring out what happened versus what is being assumed.

Then comes documentation. Many otherwise smart people fail at this stage. If it isn't documented clearly, it may as well not have happened. Good file notes explain what was received, what was verified, what remains open, and why the next action makes sense.

What that looks like on a property loss

Take a water-damage claim in a commercial building. The professional handling it might start the morning by reviewing the first notice of loss, prior communications, photos from the site, and any emergency mitigation invoices. Next comes outreach to confirm timeline, affected areas, and who has inspection access.

By afternoon, the file may shift into evaluation. Does the reported damage line up with the observed conditions? Is there enough support for the scope being claimed? Are business interruption concerns starting to surface? At this stage, broad labels like “claims management jobs” cease to be helpful, and the true profession emerges.

For people drawn to catastrophe and property response, disaster claims adjuster jobs show just how fast file complexity can rise when losses are widespread and timelines tighten.

A strong adjuster doesn't chase every theory. They identify the missing facts that actually change the outcome, then they go get those facts.

Negotiation is not the final step. It's threaded through the file

New people often think negotiation starts when everyone already agrees on the facts. Usually, it starts much earlier.

A contractor may have one view of scope. An insured may be focused on urgency. A carrier may need more support before moving position. A public adjuster may be assembling documentation to close those gaps. The daily work is partly technical and partly relational. You're moving people toward a supportable outcome while keeping the record clean enough that another reviewer, manager, regulator, or attorney could understand the path you took.

That's why the best claims professionals blend empathy with discipline. Too much softness and the file drifts. Too much rigidity and you miss the human reality of the loss.

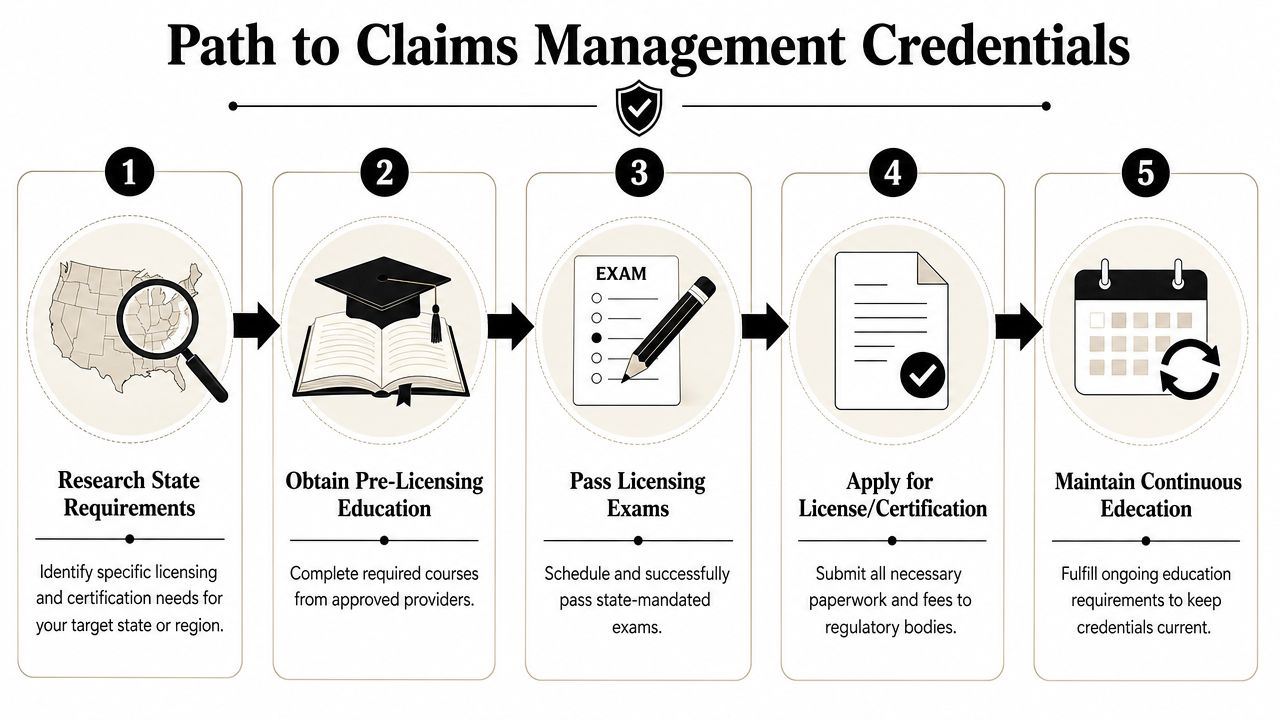

Getting Licensed and Certified for Success

Licensing is where many people realize claims isn't one national system with one universal checklist. It's fragmented. State rules matter. Residency can matter. Role type matters. Property work has its own complications. Public adjusting adds another layer because you're representing policyholders directly, not just handling claims within a carrier framework.

Why state-specific licensing matters

Licensing complexity is a real barrier to entry, especially in property claims. Job listings and hiring practices often reflect local requirements, and state-specific regulations, deadlines, and consumer protections differ enough that jurisdictional knowledge in markets like Oregon and Washington becomes valuable, as reflected in this Molina role highlighting state-specific requirements.

That's not bureaucracy for its own sake. It changes how you work a file. Deadlines, communication requirements, contract rules, and consumer protections can affect what documentation is needed, how quickly it must be handled, and what conduct is permitted.

If you're new to the field, a practical starting point is formal claims adjuster training that helps you understand terminology, file structure, and the difference between adjuster role types before you spend money on the wrong path.

Know which credential path you're actually pursuing

People often say “I want to be an adjuster” when they mean one of several different things:

Staff or company adjuster

Usually employed by an insurer. You handle claims on the carrier side.Independent adjuster

Often works on behalf of insurers or third-party administrators, commonly on assignment-based or field-heavy work.Public adjuster

Represents the policyholder in property claims. This is the path that matters most if you want to advocate for insureds in Oregon or Washington.

Field note: The license you need depends on who you represent. That's the first question to answer before you sign up for any course or exam.

A practical roadmap for Oregon and Washington public adjuster candidates

Because regulations change, candidates should verify current requirements directly with the appropriate state regulator before applying. But the process generally follows a clear sequence.

Oregon

For a public adjuster track in Oregon, candidates should expect to:

- Confirm eligibility and regulator requirements: Check the current state rules for public adjuster licensing, application forms, and any required disclosures.

- Complete any required pre-licensing steps: If education or approved coursework is required, finish that first.

- Prepare for the state exam if applicable: Don't study only broad insurance concepts. Focus on policy structure, ethics, state rules, and practical claim handling.

- Address bonding and application items: Public adjuster licensing commonly requires supporting application materials beyond just an exam result.

- Set up a compliance system: Even before your first file, know how you'll handle contracts, communications, deadlines, and recordkeeping.

Washington

Washington candidates should take the same disciplined approach:

- Start with the current public adjuster licensing requirements in Washington.

- Confirm whether examination, bonding, fingerprinting, or other application steps apply.

- Learn the rules that govern solicitation, contracts, fee disclosures, and claim representation.

- Build a clean documentation process from day one. Public adjusting falls apart fast when records are scattered.

Certifications help, but they don't replace judgment

Certifications can strengthen your resume, especially in property claims, but they won't rescue poor file handling. Employers and clients still care most about whether you can read damage, organize proof, interpret policy language, and negotiate without losing control of the facts.

In the Pacific Northwest, that's where public adjusting becomes a real career differentiator. Oregon and Washington property claims can involve moisture intrusion, smoke, fire, storm loss, and complicated rebuilding questions. The professionals who stand out aren't just licensed. They're reliable under pressure, accurate in documentation, and careful with state-specific obligations.

Building Your Resume and Nailing the Interview

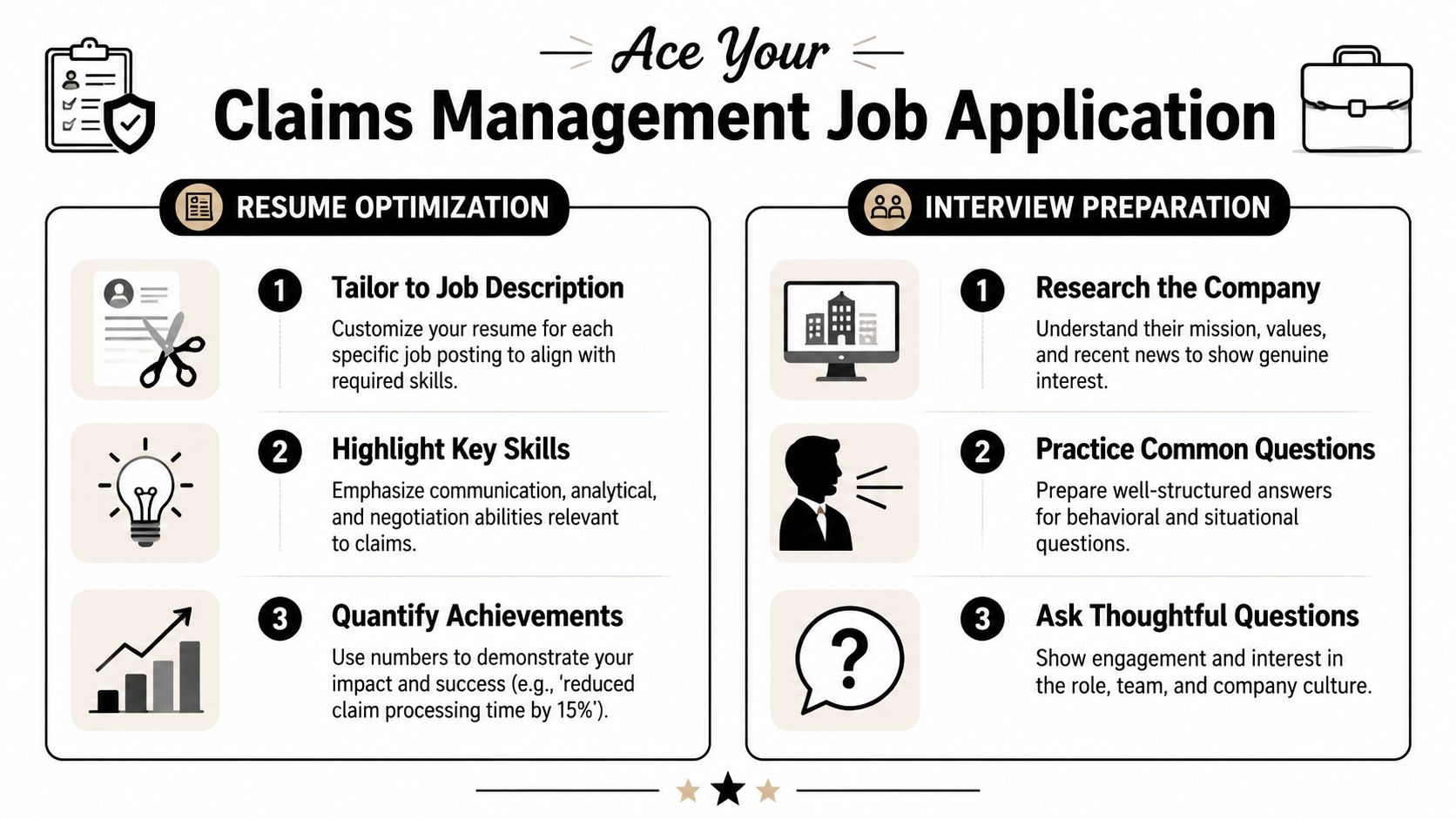

Most resumes for claims management jobs fail for one simple reason. They describe duties, not decisions.

A hiring manager already knows an adjuster “handled files” or “communicated with customers.” What they need to see is whether you can think, document, and move a file toward resolution. If you're coming from another industry, that still applies. Customer service, restoration, construction coordination, legal intake, project management, and medical claims work can all translate if you frame them correctly.

What to put on the resume

Use language that matches how claims teams evaluate candidates. Good keywords include policy interpretation, coverage review, damage assessment, liability analysis, investigation, subrogation awareness, fraud identification, negotiation, file documentation, record review, and regulatory compliance.

If you have tool-specific experience, name it. For property roles, software literacy matters when it's real. Don't stuff your resume with product names you can't discuss in an interview.

For job seekers who need help showing impact credibly, this guide on using metrics in your resume is useful. The key in claims is to keep metrics honest and specific to your actual work. If you don't have verified numbers, describe outcomes qualitatively instead of inventing precision.

A related niche worth exploring is auto inspection jobs if your background is more visual, field-based, or tied to estimating rather than desk adjudication.

Interview answers that actually land

Claims interviews usually test four things:

- Judgment: Can you make a supportable decision with incomplete facts?

- Documentation discipline: Will your file notes hold up?

- Communication: Can you explain difficult outcomes calmly?

- Composure: What do you do when the claimant, insured, contractor, or attorney pushes back?

Try preparing around questions like these:

| Common interview question | What the manager is really testing |

|---|---|

| How do you handle a difficult claimant? | Emotional control, empathy, boundary setting |

| Describe a time you caught an important detail others missed | Investigative focus and file accuracy |

| How do you prioritize multiple urgent claims? | Triage and operational discipline |

| Tell me about a disagreement with a customer or partner | Professionalism under pressure |

Don't give polished corporate answers. Give file-based answers. Explain what happened, what information you gathered, what decision you made, and how you documented it.

If you're aiming for public adjuster work, expect more scrutiny on ethics, communication, and property-loss understanding. You may be asked how you'd handle scope disputes, missing documentation, or an insured whose expectations are out of line with what the file supports. A strong answer shows advocacy without sloppiness.

Where to Find Top Claims Management Jobs

The broad job boards still matter. LinkedIn, Indeed, and major insurer career pages can surface staff adjuster, examiner, and claims leadership openings. But if you stop there, you'll miss a lot of the market. Claims hiring is fragmented. Some employers recruit through corporate portals, some through niche insurance boards, and some through regional relationships.

Search by role type, not just by keyword

Don't only search “claims management jobs.” Search combinations like public adjuster, field adjuster, claims examiner, catastrophe claims, property claims, workers' compensation adjuster, and denials management if you're crossing over from health claims.

It also helps to keep a second list of operational terms. Some jobs are titled around functions rather than “claims” itself, especially in support or review-heavy roles.

Use broad boards and niche boards together

A practical search stack looks like this:

- Large job platforms for volume and alerts

- Carrier career pages for direct employer pipelines

- Regional insurance networks for local opportunities

- Niche hiring platforms to catch roles that don't get broad visibility

If you want another source of active listings outside the major boards, you can browse open positions through Shorepod and compare how claims-adjacent roles are titled across employers.

For policyholder-side property work in the Pacific Northwest, local focus matters more than people think. Oregon and Washington roles may be shaped by licensing, storm response needs, and state-specific claim handling rules. That's also where NW Claims Management fits as one factual example of a public-adjusting firm in the region. It handles property claims for policyholders in Oregon and Washington, which makes it relevant for candidates interested in the public adjuster path rather than insurer-side file handling.

Frequently Asked Questions About Claims Careers

Will AI replace claims management jobs

It'll replace some routine tasks, not the profession. Claims operations are already shifting toward automation for workflow, document extraction, triage, and exception handling. The work that remains most human is the work that's hardest to standardize: complex coverage analysis, fraud-sensitive review, negotiation, customer-facing escalation, and difficult judgment calls.

That's why the safer career move is to become the person who can manage exceptions, not just repeat steps.

Is claims still a stable career

Yes, but not because every role is growing. According to the U.S. Bureau of Labor Statistics outlook for claims adjusters, appraisers, examiners, and investigators, employment is projected to decline 5% from 2024 to 2034, yet the field is still expected to produce about 21,600 openings per year on average over that period, mostly from replacement needs. The same BLS page lists a median annual wage of $76,790 in May 2024.

That tells you the market is changing, not disappearing.

Can career changers break into claims

Yes, especially if they bring transferable discipline. Restoration, construction estimating, legal case support, medical records work, customer escalation handling, and project coordination all map well if you can show documentation habits and sound judgment. Career changers usually struggle most with policy language and file structure, not with professionalism.

What's the biggest difference between insurer-side claims work and public adjusting

The side you represent changes the entire job. Insurer-side professionals investigate and resolve claims for the carrier. Public adjusters represent the policyholder in property losses. The skills overlap, but the posture is different. One role manages the file from inside the insurer's process. The other builds and supports the policyholder's claim presentation from the outside.

If you're interested in property damage, documentation, and advocacy in Oregon or Washington, public adjusting is one of the clearest specialized paths inside the broader world of claims management jobs.

If you're exploring the public adjuster path or want to understand how property claims work in Oregon and Washington, NW Claims Management is a practical place to start. The firm works on behalf of policyholders, not insurers, and its site can help you understand the practical demands of property claim documentation, negotiation, and state-specific compliance.