The phone rings a day or two after an injury report, a workplace accident, or some other loss connected to insurance. The person on the other end introduces themselves as an adjuster. If you've never dealt with a claim before, that call can make your stomach drop.

Many individuals have the same questions right away. Who is this person? Are they here to help me? What should I say? And if you're a property owner or business owner who already knows how stressful insurance can be, you may also wonder whether a work comp adjuster works anything like the adjuster handling a building, contents, or business interruption claim.

That confusion is normal. Insurance uses the same word, adjuster, across very different claim types. But the big principle stays the same. The adjuster plays a central role in the claim, and understanding who they work for changes how you should communicate, document your loss, and protect your interests.

The Adjuster's Call You Weren't Expecting

A lot of claims start in a blur. Someone gets hurt at work. A supervisor files an incident report. Medical treatment begins. Then comes the adjuster's call.

That first conversation matters because the adjuster often becomes the main person gathering facts, requesting records, and moving the file forward. To you, it may feel like a customer service call. To the insurance company, it's the opening stage of claim management.

If you're already under stress, it's easy to assume the adjuster is a neutral helper who will collect information and make things right. That's one of the most common misunderstandings in insurance. An adjuster may be polite, responsive, and professional, but that doesn't automatically make them your advocate.

The same lesson applies outside workers' compensation. Property owners often learn this after fire, storm, or water losses, when the insurer's representative starts asking detailed questions before the full damage picture is clear. If you're trying to understand the broader context, this overview of a local claims adjuster role and claim process helps show how adjusters fit into the insurance system more generally.

Your claim experience often depends less on what you meant to say and more on what got documented in the file.

That isn't meant to scare you. It's meant to steady you. Once you understand the adjuster's role, the process starts to make more sense.

A work comp adjuster isn't just a voice on the phone. They're part investigator, part administrator, and part decision-maker inside the insurer's process. When you know that from the start, you're much less likely to hand over information casually, miss a deadline, or assume silence means nothing is happening.

What a Work Comp Adjuster Actually Does

A work comp adjuster is best understood as a fact-finder and rule-applier for the insurance company. They gather information, compare it against the policy and the workers' compensation rules in that state, and make decisions about what gets paid and when.

According to this explanation of what a workers' compensation claims adjuster does, the adjuster is the insurance carrier's operational decision-maker for the claim. They investigate the injury, review incident reports, employer statements, wage information, and medical records, then determine eligibility for medical and income benefits and how much the insurer will pay. The same source makes an important point many people miss. The adjuster is not a neutral administrator.

Investigation comes first

At the beginning, the adjuster wants to answer basic questions.

- What happened: How did the injury occur, when did it happen, and who saw it?

- Who reported what: The adjuster compares the worker's account, the employer's report, and any witness statements.

- What records exist: They usually want medical notes, job details, wage information, and prior documentation tied to the event.

This is why the early stage can feel repetitive. The adjuster isn't just chatting. They're building the file.

Then comes evaluation

After gathering facts, the adjuster has to apply rules. That means asking whether the injury is compensable, what treatment should be authorized, and what wage-related benefits may apply.

If you're trying to understand how these legal frameworks vary by state, this guidance on workers' compensation law gives a helpful plain-English overview of the legal side. It isn't a substitute for advice in your own state, but it helps explain why adjusters focus so heavily on documentation, medical support, and timing.

Resolution is the end goal

Most adjusters are expected to keep the claim moving toward some form of resolution. That could mean approving treatment, issuing payments, disputing parts of the claim, arranging evaluations, or working toward settlement when appropriate.

A short way to think about it is this:

| Core function | What the adjuster does | Why it matters |

|---|---|---|

| Investigation | Collects facts and records | The file shapes later decisions |

| Evaluation | Applies policy and legal rules | Benefits can be approved, limited, or denied |

| Resolution | Moves the claim toward payment or closure | Delays and disputes often happen here |

If you want a broader breakdown of insurer-side responsibilities, this summary of claims adjuster duties is useful because it shows how much of the role depends on documentation, judgment, and file control.

How Adjusters Investigate and Value Claims

Claimants often don't see what happens after a claim file opens. They just notice the symptoms. More forms. More questions. Delays. Requests for records that seem unrelated.

Behind the scenes, the adjuster is trying to answer two connected questions. First, is the claim supported? Second, what is it worth under the applicable rules?

How the investigation usually unfolds

The process often starts with a recorded or documented statement. The adjuster may ask about the date of injury, job duties, body parts involved, prior symptoms, and what happened immediately after the incident. They may also request:

- Medical records: Office notes, restrictions, treatment plans, and work status updates

- Employment information: Wages, job description, attendance records, and date-of-injury details

- Incident materials: Supervisor reports, photos, witness statements, and internal reports

- Follow-up proof: Updated restrictions, referrals, and bills tied to treatment

Sometimes the questions feel narrow. Sometimes they feel broad. Both serve the same purpose. The adjuster is testing whether the facts line up cleanly enough to support payment.

Practical rule: If a fact matters to your claim, assume it should exist in writing somewhere outside a phone call.

How those facts turn into claim value

Workers' compensation doesn't value a claim the same way a property loss is valued, but the logic is familiar. The adjuster looks for supportable categories of loss, then matches those categories to what the law or policy allows.

In a work comp file, that often includes medical treatment, wage-related benefits, and other claim costs tied to the injury. The adjuster also watches for inconsistencies. If the medical records, employer report, and your own statement don't fit together, that can affect how the claim is reserved, paid, or disputed.

Good recordkeeping changes outcomes. A missing work note or vague doctor instruction can create a very different file than a detailed set of records showing diagnosis, restrictions, causation, and follow-up care.

Automation is changing the experience

Some delays or strange responses don't come from one overwhelmed person making every decision manually. Across major insurance markets, carriers have been expanding automation for intake, document triage, and fraud detection, as explained in this discussion of how algorithmic workflows affect workers' comp claims. That matters because part of your claim may be routed, flagged, or prioritized by systems before a human adjuster takes a closer look.

For claimants, that changes how to read the situation. A sudden document request, a generic denial letter, or silence after submission may reflect workflow design as much as individual judgment.

If your loss involves business records, income disruption, or complicated financial documentation on the property side, forensic accounting support for insurance claims shows how detailed records can make the value discussion far more concrete.

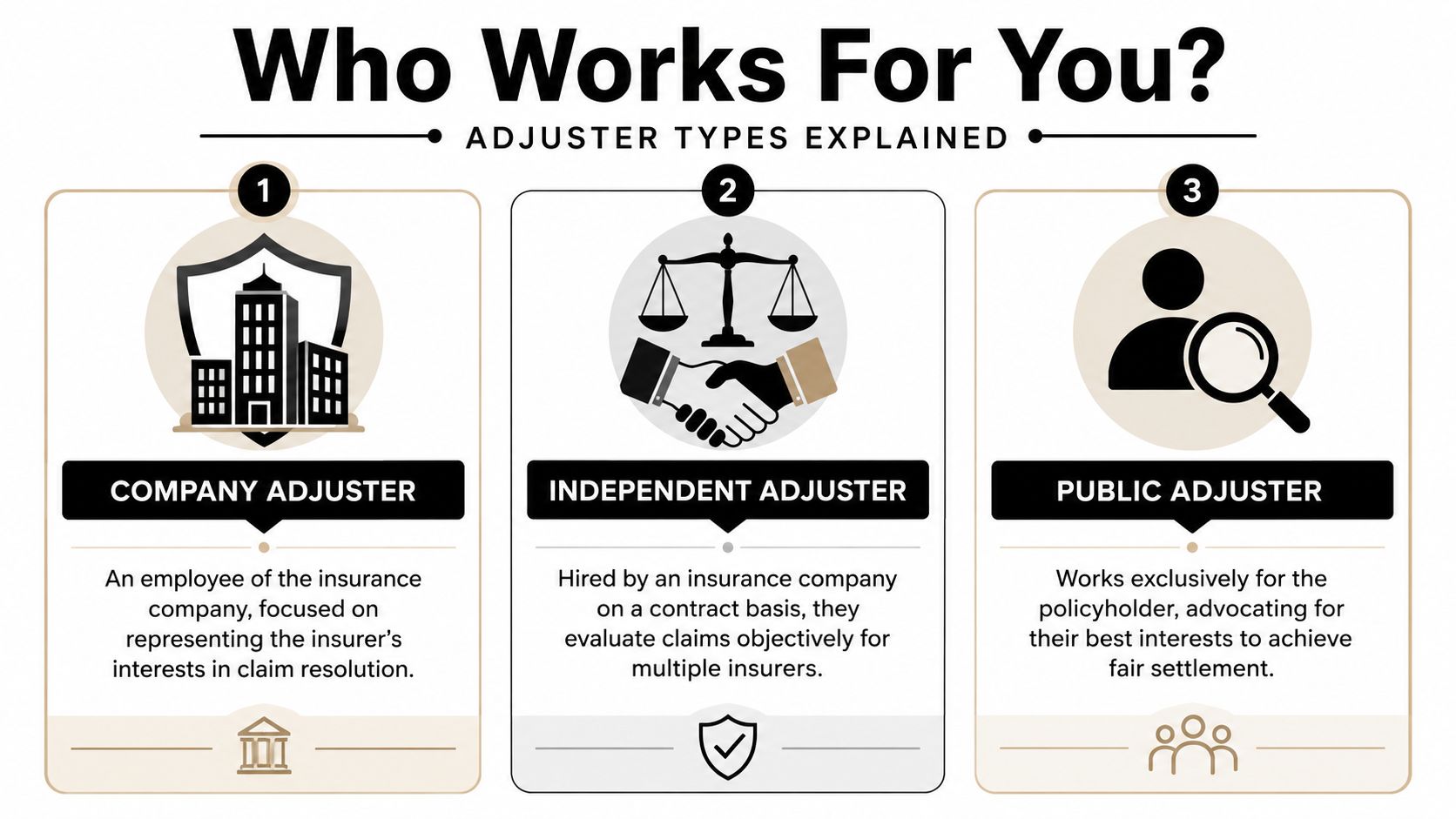

Company vs Independent vs Public Adjusters Who Works for You

The word adjuster causes trouble because it sounds singular. In practice, there are different kinds of adjusters, and the biggest difference isn't skill level. It's who they represent.

The three main adjuster types

Here's the simplest comparison:

| Adjuster type | Who hires them | Who they represent |

|---|---|---|

| Company adjuster | Insurance company | Insurance company |

| Independent adjuster | Insurance company on contract | Insurance company |

| Public adjuster | Policyholder | Policyholder |

A company adjuster is a direct employee of the insurer. They work inside that carrier's systems and follow that company's claim procedures.

An independent adjuster isn't independent from the insurer in the way many policyholders assume. They are usually contracted by insurance companies to handle claims on the insurer's behalf. They may work with multiple carriers, but in your claim, they still represent the carrier that hired them.

A public adjuster is different. A public adjuster is licensed to represent the policyholder in a property insurance claim, not the insurance company. That distinction matters when the dispute is about building damage, contents, scope of loss, estimates, business interruption, or policy interpretation after fire, water, storm, vandalism, or other property damage.

Why this distinction matters so much

People often hear "adjuster" and assume all adjusters occupy a neutral middle ground. They don't. The title describes a function. It doesn't tell you allegiance.

That matters even in a work comp context because the same confusion can shape expectations. If you're dealing with a work comp adjuster, you should understand you're dealing with the insurer's claim decision-maker. If you're dealing with a large property loss, the same basic lesson applies. The adjuster assigned by the carrier is there to adjust the claim for the carrier.

When people say, "I thought the adjuster was handling it for me," they're usually describing a misunderstanding about representation, not a problem with the title itself.

The expertise issue also matters. According to a BLS page covering claims adjusting careers and outlook, a 2017 benchmarking study found that 46% of claims leaders believed adjusters need four to six years of experience to become experts in workers' compensation claims. Complex claims take judgment. That applies whether someone is evaluating a workplace injury for an insurer or documenting a major property loss for a policyholder.

If you've ever wondered how insurer-retained field adjusters and contract adjusters fit together on the property side, this explanation of an independent adjusting company helps clarify the structure.

A practical way to remember it

Use this shortcut when the phone rings:

- If the insurer assigned the adjuster, that adjuster represents the insurer.

- If you hired the adjuster, that adjuster represents you.

- If you're not sure, ask directly and get the answer in writing.

That single question can save a lot of confusion later.

Your Rights and Key Claim Timelines

When you're under pressure, it's easy to act as if the adjuster controls everything. They don't. You still have rights, and deadlines work both ways.

First, you have the right to understand what the insurer is asking for and why. You also have the right to keep your own records, ask for copies of important communications, and challenge decisions you believe are wrong. In some situations, you may also have the right to representation by an attorney. On the property side, policyholders may also choose a public adjuster to help document and present the claim.

The timeline issue that catches people off guard

The biggest practical mistake I see is waiting too long because a claimant assumes the file is "still being reviewed." Claims often involve notice deadlines, treatment disputes, appeal windows, document requests, and filing periods that don't pause just because communication is slow.

A useful general reference is this workers compensation statute of limitations guide. It shows why you should confirm deadlines in your own state early, not after a denial arrives.

Oregon and Washington notes

If you're in Oregon, workers' compensation issues are generally governed through the state's workers' compensation system, and state-specific procedures matter. If you're in Washington, the Department of Labor & Industries plays a major role in claim administration and oversight. The exact process can differ depending on the claim path, the employer's coverage arrangement, and the issue being disputed.

That means two things.

- Check the governing agency early: Don't assume advice from another state applies to your file.

- Keep every deadline in one place: Use a calendar, not memory.

- Save every letter: Claim disputes often turn on what was sent, when it was sent, and whether you responded.

A missed deadline can damage a good claim more quickly than a bad phone call.

If your claim involves both injury issues and property damage to a business, treat them as separate tracks. They may arise from the same event, but they usually move under different rules, deadlines, and decision-makers.

Practical Tips for Communicating with Your Adjuster

Good communication doesn't mean saying more. It means saying the right things, clearly, and preserving a record.

Many claimants hurt their own position by trying to be overly helpful on the phone. They speculate, guess at dates, minimize symptoms, or use casual phrases that later look like admissions. A better approach is calm, factual, and documented communication.

What to do when the adjuster contacts you

Start with discipline, not emotion.

- Keep it factual: Stick to what you know, what happened, and what documents support it.

- Use writing when possible: Email creates a better record than memory.

- Confirm phone calls in follow-up messages: A short recap can prevent later disputes.

- Track requests: If the adjuster asks for records, note what was requested and when you sent it.

Claim files reward consistency. If your written timeline, medical records, and later statements all match, the file is easier to defend.

Why adjusters don't always call back

Silence feels personal when you're waiting on treatment or payment. In many cases, it isn't. Recent workers' compensation studies described in this article on work comp adjuster delays and workload show adjusters are carrying large caseloads, and that overload is linked to slower communication and delayed authorizations. That doesn't excuse poor handling, but it helps explain it.

Once you understand that, your strategy changes. Instead of repeated emotional voicemails, send concise written follow-ups that are easy to process and hard to ignore.

A useful format is simple:

- State the claim number.

- State the issue in one sentence.

- Attach or identify the supporting document.

- Ask for a response by a reasonable date.

- Save the message.

What not to do

Some mistakes create avoidable risk.

- Don't fill silence with extra talking: If you don't know, say you don't know.

- Don't assume a friendly tone means aligned interests: Professional does not mean representative.

- Don't ignore pressure tactics: If something feels rushed, document it and pause before responding.

If you want a plain-language outside perspective, this guide to workers' comp adjuster tricks to avoid is a helpful checklist of common pressure points. On the broader insurance side, this explanation of insurance adjuster tricks can also help you spot tactics that show up in different claim settings.

Short, written, documented communication usually beats passionate, improvised phone calls.

Taking Control of Your Insurance Claim

A work comp adjuster has real authority inside the claim, but that doesn't mean you're powerless. It means you need to understand the role clearly.

The insurance system is built around documentation, procedure, and decision-making by people who work for the carrier. The workers' compensation market was financially strong in 2023, with private carriers posting their 10th consecutive year of underwriting profitability, according to the NCCI State of the Line metrics report. That kind of system stability makes one thing even more important. A claim should be well documented and professionally managed if you want a fair result.

Knowledge changes the way you respond. You ask better questions. You keep better records. You stop assuming the insurer's process automatically protects your interests.

And when the outcome matters greatly, you remember that you can bring in your own advocate.

Frequently Asked Questions About Work Comp Adjusters

Can a work comp adjuster make me give a recorded statement

They can ask. Whether you should give one, and under what conditions, depends on the rules of your claim and your state's process. Before giving any recorded statement, understand why it's being requested and whether you want legal advice first.

Does the work comp adjuster choose my doctor

That depends on state rules and the structure of the claim. Some systems limit provider choice more than others. Don't rely on general internet advice. Verify what applies in your state and claim.

Is the adjuster the same as my lawyer

No. The adjuster handles the claim for the insurance side. Your lawyer, if you have one, represents you. On a property claim, a public adjuster also represents the policyholder rather than the insurer.

Why did I get a denial letter that feels generic

Some claim communications are generated through standardized workflows. A generic letter doesn't always mean no human reviewed the file. It may mean the file moved through a system process before someone took a closer look.

Should I talk to the adjuster by phone or email

Email is usually better for important issues because it creates a record. If you do speak by phone, send a follow-up email summarizing what was discussed.

Can I challenge the adjuster's decision

Yes. The exact method depends on the issue and your state. You may be able to request review, file an appeal, seek legal counsel, or use another formal dispute process.

If my issue involves property damage, should I still think about adjuster type

Absolutely. In property claims, who the adjuster works for can directly affect scope, valuation, and settlement negotiations.

If you're dealing with a confusing insurance claim in Oregon or Washington and need someone on the policyholder's side for a property loss, NW Claims Management helps homeowners, businesses, nonprofits, and public entities document damage, interpret policy language, and negotiate with insurers. When the claim is large, technical, or overwhelming, having a licensed public adjuster can give you a clearer process and a stronger position.