You've already been through the hard part. The storm hit, the pipe burst, the fire spread, or the vandalism happened. You reported the loss, answered the carrier's questions, let their adjuster inspect the property, and waited for the estimate.

Then the offer arrived, and it didn't come close.

That moment rattles people for a reason. You've paid premiums for years, and now the numbers on paper don't reflect what local contractors are telling you it will take to put your home back together. For many Oregon and Washington homeowners, that's when the claim fight begins. Not because the damage isn't real, but because the insurer and the policyholder are no longer speaking the same language about value, scope, and what proper repair really looks like.

Your Insurance Offer Is Too Low Now What

A common scenario looks like this. A homeowner gets a carrier estimate after a wind or water loss, calls a contractor, and hears something very different. The carrier may allow for patching. The contractor says the damaged area has to be removed farther back to reach sound material, match finishes, or rebuild correctly. The insurer prices generic materials. The homeowner has upgraded finishes, custom trim, or older construction that takes more labor.

That gap creates panic fast. You still need to protect the property. You may be paying out of pocket for temporary fixes. You may also feel like if you push back too hard, the claim will stall.

The first problem is usually scope, not attitude

Most low settlement disputes don't start with dramatic bad faith behavior. They start with an estimate that's too narrow, too rushed, or built on incomplete information. The adjuster may have missed part of the damage. The estimate may leave out trades. The pricing may not reflect what qualified contractors will bid. If you haven't compared the carrier's numbers carefully against independent insurance claim estimates, it's hard to know whether the offer is merely incomplete or strategically low.

That distinction matters because your response should match the problem.

If the insurer lacks documents, you may solve it with a supplement package. If the insurer agrees the loss is covered but keeps undervaluing the repair, appraisal may become the right move. If the insurer is denying coverage outright, appraisal usually isn't the tool that fixes that.

Practical rule: Don't treat every disagreement like the same fight. First identify whether you're arguing about price, scope, or coverage.

Appraisal is often the homeowner's strongest pressure point

Many policyholders don't realize their own policy may contain a built-in process for resolving a dispute over value. That process is the appraisal clause. It can move the valuation issue out of endless back-and-forth with the desk adjuster and into a formal dispute process focused on the amount of loss.

That matters when you're stuck in the familiar loop:

- The carrier says your contractor is too high.

- Your contractor says the insurer's estimate won't complete the work.

- You say you just want enough to repair the property correctly.

A well-timed appraisal demand changes the conversation. Instead of debating in circles, each side appoints an appraiser, and if needed, a neutral umpire helps decide the amount of loss. It doesn't guarantee every issue disappears. It does give the homeowner a contractual mechanism to force a serious valuation process.

For worried homeowners in Oregon and Washington, that shift is often the point where the claim stops feeling one-sided.

Decoding Home Insurance Appraisal and the Appraisal Clause

A home insurance appraisal is not a real estate appraisal. It does not tell you what your house would sell for. It does not care what the land is worth. It is a replacement-cost exercise focused on what it would cost to rebuild or repair the insured structure as of the valuation date.

According to Reserve Advisors' explanation of insurance appraisals, the process centers on rebuilding cost, excludes land and other non-insurable site improvements, and relies on details like on-site measurements, photos, construction characteristics, HVAC and finish information, and a worksheet that separates replacement new, exclusions, and insurable value. That's the core distinction many homeowners miss when they assume “appraisal” means a market-value opinion.

Think rebuild cost, not resale price

If your home could sell for a certain amount tomorrow, that still doesn't answer the insurance question. Insurance wants to know what it would cost to repair or replace covered damage using current labor, materials, and construction details.

That's why details matter so much in a home insurance appraisal:

- Measurements matter because small errors in dimensions can distort quantities and pricing.

- Finish level matters because builder-grade materials and custom finishes price very differently.

- Exclusions matter because not every item on the property is part of the insurable building value.

- Documentation matters because appraisers need facts, not assumptions.

A homeowner who walks into appraisal with only a rough contractor total often feels frustrated by how technical the process becomes. The homeowner who brings a detailed estimate, photos, invoices, and accurate property information usually has a stronger position.

A related issue that confuses people is the difference between actual cash value vs replacement cost. If you don't know which valuation basis your policy is applying at a given stage, it's easy to misread what the insurer is doing.

The process itself works in a fairly structured way.

What the appraisal clause actually does

In many property policies, the appraisal clause is a binding dispute-resolution process for the amount of loss, not coverage. As explained in Keating Wagner's discussion of property insurance appraisal, once appraisal is invoked, each side appoints a competent appraiser, the appraisers select a neutral umpire, and a majority decision becomes binding.

Three terms in that clause usually deserve translation.

| Term | What it means in practice |

|---|---|

| Competent appraiser | Someone who understands property damage valuation, construction pricing, and claim documentation. |

| Neutral umpire | The third decision-maker who steps in when the two appraisers disagree. |

| Binding award | A signed decision on the amount of loss that the policy treats as controlling. |

Appraisal is not a loophole. It's part of the contract your insurer wrote and sold to you.

That's why timing and issue selection are strategic. If the insurer agrees the loss is covered but the estimate is too low, the appraisal clause can be a powerful tool. If the carrier says the policy doesn't cover the damage at all, the clause may not solve your real problem.

For homeowners, the key takeaway is simple. Appraisal is not just a definition buried in the policy booklet. It's one of the few mechanisms in the claim process that can force movement when valuation talks have stalled.

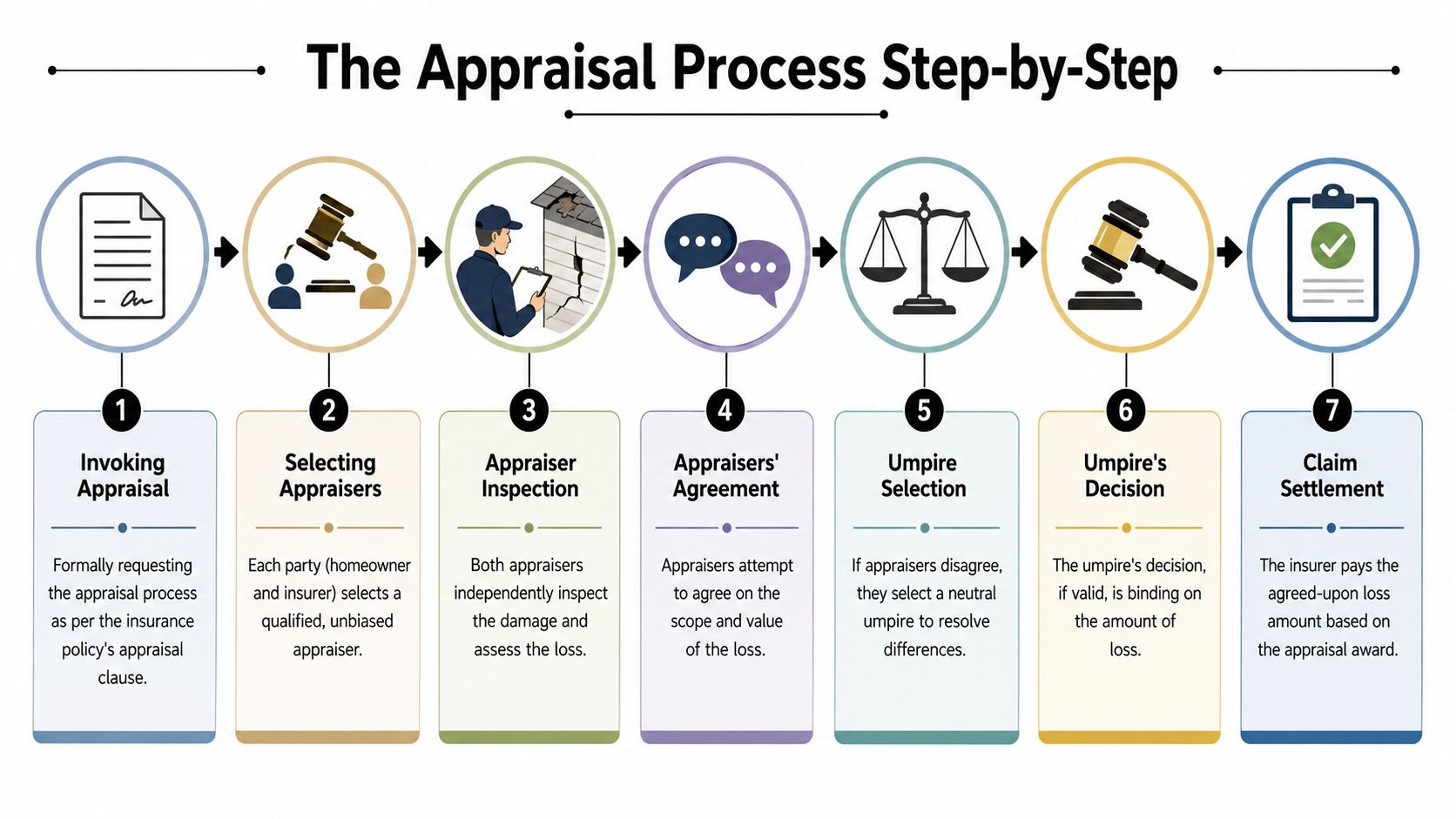

The Appraisal Process Step by Step

Most homeowners calm down once they see the process in order. Appraisal feels intimidating when it's abstract. It feels manageable when you know who does what, what documents matter, and where disputes usually stall.

The comparison below helps place appraisal alongside other routes people consider when a claim goes sideways.

Step one starts with a written demand

The process usually begins when one side sends written notice invoking the appraisal clause. That letter should be short, clear, and tied to the policy. You don't need dramatic language. You need precision.

A straightforward demand generally does three things:

- Identifies the claim and property.

- States there is a disagreement over the amount of loss.

- Invokes the appraisal clause and names your selected appraiser, if you're ready to do so.

If you invoke appraisal too early, you may lose the chance to resolve the dispute with a strong supplement package. If you invoke too late, you may spend months repeating the same failed conversation. In Oregon and Washington claims, the best timing is often after the insurer has had a fair chance to review supporting documents and has still held to a low number.

Picking the appraiser is the real fork in the road

Homeowners sometimes assume any contractor, friend in real estate, or retired adjuster can fill this role. That's a mistake. The appraiser needs to understand estimating, building assemblies, repair logic, line-item pricing, and how to support a position under scrutiny.

Look for someone who can do the following well:

- Read the estimate line by line. They should catch omitted trades, inadequate quantities, and repair methods that don't restore the property properly.

- Defend the scope. A strong appraiser can explain why a repair extends beyond the visibly damaged area.

- Document pre-loss condition. Prior photos, remodel records, and maintenance history often matter more than homeowners expect.

- Stay credible. Extreme or inflated positions can hurt the whole presentation.

The insurer will appoint its own appraiser. Some are thoughtful and practical. Others approach the role as an extension of claim containment. You can't control who they appoint, but you can control whether your side comes in prepared.

The appraisal process rewards specificity. Vague objections rarely move numbers.

The umpire and the evidence phase

If the two appraisers can't agree, they select an umpire. The umpire doesn't replace the appraisers. The umpire resolves the remaining disputes between them.

At that point, evidence quality becomes decisive. Useful materials often include contractor bids, photographs, repair invoices, engineering input where needed, product information, and proof of upgrades or specialty finishes. Detailed measurements and clear room-by-room support usually carry more weight than broad complaints about unfairness.

Some appraisal files stay largely on paper. Others involve site meetings and re-inspection. The more complex the loss, the more likely it is that the appraisers and umpire will need a careful walk-through and a disciplined estimate comparison.

The award is binding on value

When any two of the three sign the award, the amount of loss is set under the policy. That does not mean every dispute in the claim disappears. It means the valuation issue has been decided through the contract mechanism.

A good homeowner mindset during appraisal is steady and organized:

- Answer questions quickly

- Keep every invoice and communication

- Don't start freelancing new theories

- Stay focused on documented damage and repair cost

The process works best when the homeowner treats it like a formal valuation proceeding, not a venting session.

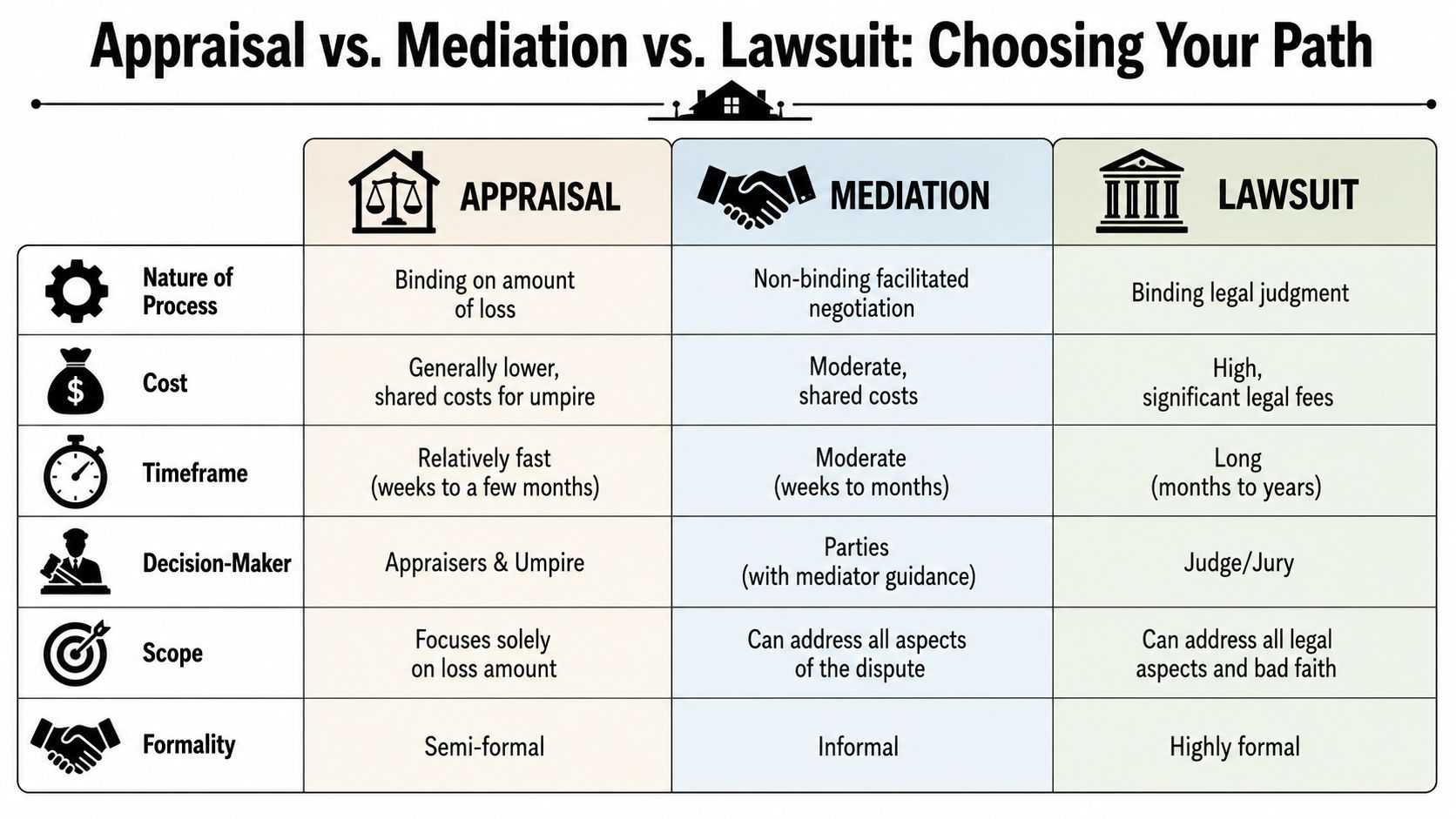

Appraisal vs Mediation vs Lawsuit Choosing Your Path

The hardest decision usually isn't whether appraisal exists. It's whether appraisal is the right move right now.

Homeowners often hear three options in the same week. A contractor says to push harder. A lawyer mentions litigation. Someone else suggests mediation. Each path has a place, but they solve different problems.

The evidence checklist below shows the kind of file strength that matters before you choose any path.

When appraisal is the sharper tool

Appraisal is usually strongest when the insurer has accepted that there is covered damage, but the parties disagree on the amount of loss. That can include disputes over repair cost, omitted items, or whether the estimate reflects what proper restoration requires.

According to Arizona Insurance Law's explanation of appraisal limits, appraisal is generally limited to the amount of loss and does not decide whether damage is covered or whether the insurer is liable at all. That limitation is the strategic key. If your real fight is over coverage, appraisal may give you a valuation answer without giving you payment.

A simple way to think about it:

| Your dispute | Better first option |

|---|---|

| The insurer agrees damage is covered, but the estimate is too low | Appraisal |

| The parties may still negotiate and need a neutral facilitator | Mediation |

| The insurer denies coverage, alleges exclusions, or the dispute turns legal | Lawsuit or coverage counsel |

Where mediation fits

Mediation works when both sides still have room to negotiate. It can help when personalities are getting in the way, or when the dispute includes several issues at once and no one wants the cost or rigidity of litigation. It's often useful where the homeowner wants a global resolution and the insurer is willing to make business decisions.

But mediation is not a forced valuation mechanism in the same way appraisal can be. If the insurer's strategy is delay, vague promises to “re-review,” or soft resistance without changing the estimate, mediation may produce a conversation without producing enough money.

When litigation is the necessary path

Lawsuits belong in a different category. They address legal disputes. If the carrier says the policy excludes the damage, claims late notice, or disputes liability itself, a lawsuit may be the path that can resolve those issues. The trade-off is obvious. Lawsuits are more formal, broader in scope, and often heavier for the homeowner.

A second strategic issue is timing. The same Arizona analysis notes that in at least one jurisdiction-specific context, appraisal may be waived if not requested within one year of loss. Oregon and Washington homeowners should not assume deadlines are generous or uniform. Waiting too long can weaken your bargaining power even when your valuation position is strong.

If the carrier is saying “we don't owe this,” appraisal may not fix it. If the carrier is saying “we owe something, just not that much,” appraisal becomes far more useful.

The right choice depends on the dispute you have, not the one you wish you had.

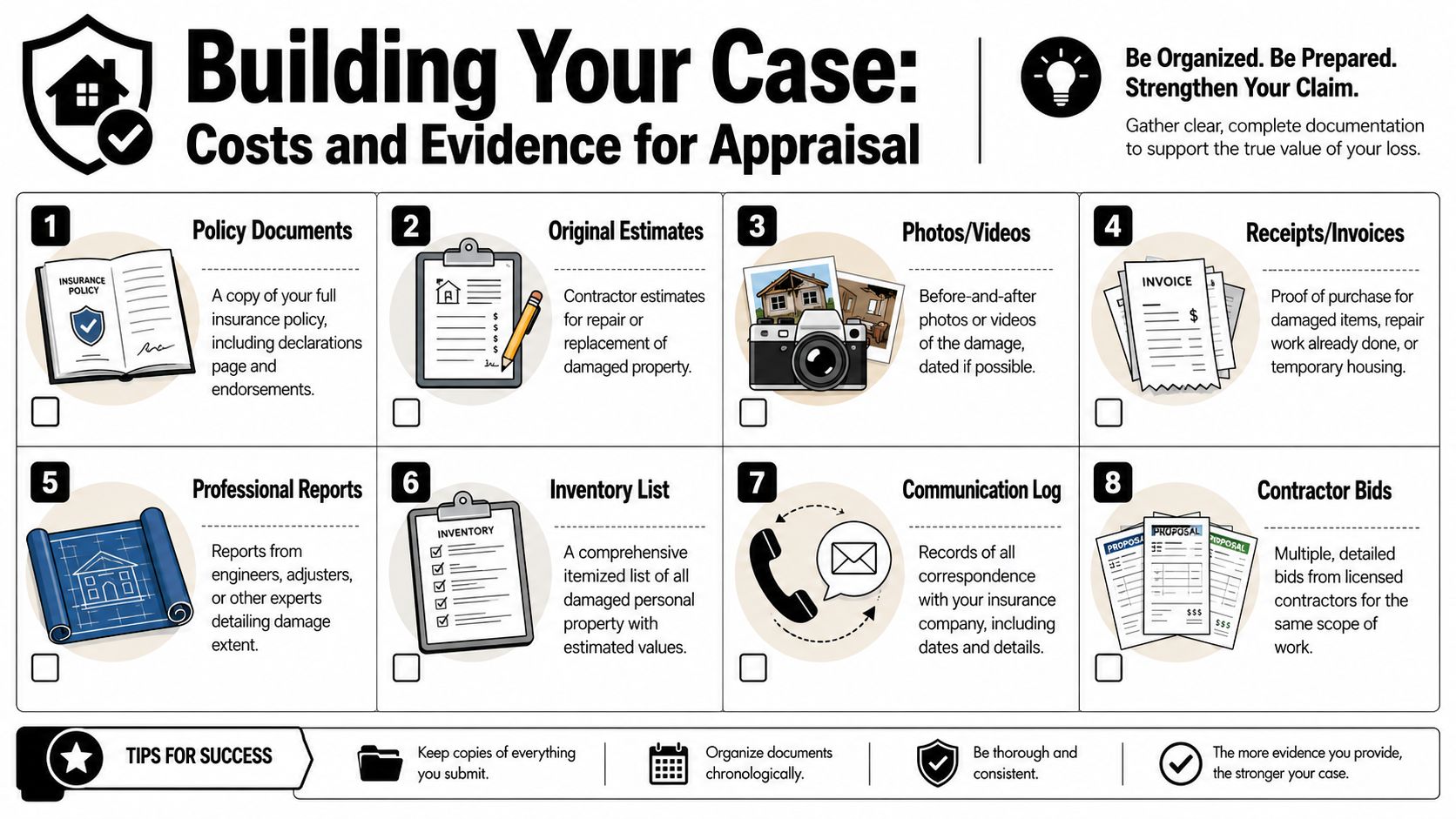

Building Your Case Costs and Evidence for Appraisal

An appraisal win usually starts long before the appraisers disagree. It starts with the file. Homeowners who gather clean, specific evidence put themselves in a much better position than homeowners who rely on memory and a single rough bid.

This checklist is a good working model for what to assemble.

What belongs in a strong appraisal file

Start with the documents that tell the story of the property before and after the loss.

- Your full policy package including declarations, forms, and endorsements.

- The carrier estimate with every line item visible.

- Independent contractor bids that explain scope, not just total price.

- Photos and video from before the loss if you have them, and from immediately after.

- Invoices and receipts for emergency mitigation, temporary repairs, and prior improvements.

- Room-by-room notes listing what was damaged and what repair method is being proposed.

If the dispute involves specialty materials, match issues, or partial replacement questions, get specific. Product names, dimensions, finish descriptions, and install details matter. For flooring claims, for example, homeowners often need outside pricing context to understand whether a line item is realistic. A practical resource on hardwood floor replacement costs can help you compare the insurer's assumptions against the kind of repair work the claim may require.

Budgeting for the appraisal itself

There is also the direct cost of obtaining valuation help. According to industry data cited by Wawanesa's home insurance appraisal guide, independent appraisals typically range between $300 and $600 depending on location and property size. That number won't tell you what every claim professional will charge for every role in every dispute, but it gives homeowners a realistic budgeting anchor when they decide whether to bring in outside valuation support.

The important question isn't “Do I have to spend anything?” It's “Will spending on competent evidence materially improve my position?”

In many claims, the answer is yes.

Evidence that helps and evidence that doesn't

Helpful evidence is detailed, dated, and tied to the actual repair problem. Weak evidence is broad, emotional, or unsupported.

| Strong evidence | Weak evidence |

|---|---|

| Detailed contractor estimate | One-page total with no scope |

| Dated photos | Undated images with no context |

| Product and finish documentation | “Like kind and quality” with no backup |

| Communication log | Verbal recollection only |

For homeowners and representatives working inside Xactimate-driven claim disputes, estimate literacy matters. Training resources such as Verisk Xactimate training can help you understand why line items, quantities, and repair logic often decide whether an appraisal position looks credible.

A worried homeowner often wants a silver bullet. There usually isn't one. There is, however, a repeatable formula: document the property accurately, prove the scope, support the pricing, and keep the file organized enough that another professional can step in and defend it.

Why a Public Adjuster Is Your Essential Ally in Appraisal

A homeowner can go through appraisal alone. The question is whether that's wise when the insurer handles claim valuation disputes every day.

In Oregon and Washington, this process often turns on details that look small until they cost real money. Repair sequence. Waste factors. Trade overlap. Access issues. Matching concerns. Finish quality. Temporary protections. The insurer's estimate may flatten those details into a cheaper number. The homeowner then has to prove why that number doesn't restore the property correctly.

Rising costs have made precision more important

Historical data from the period between 2018 and 2022 showed that average homeowners insurance premiums rose 8.7% faster than inflation, according to Guardian Service's homeowners insurance statistics. That trend matters because it reflects a broader reality homeowners have felt directly. Construction and insurance costs don't sit still. Static assumptions about rebuild cost age badly.

In practical claim work, that means old valuations, generic estimating, and shallow inspections can leave policyholders short at the worst possible moment. It also means the person reviewing your file needs more than a general sense that the offer “seems low.” They need a disciplined position built from scope, pricing, and policy language.

What a public adjuster actually does in appraisal

A good public adjuster doesn't just complain louder than the homeowner. The job is more technical than that.

A public adjuster may help by:

- Reviewing the policy to identify whether appraisal is available and whether the dispute is about amount of loss.

- Testing the estimate against contractor reality, building conditions, and omitted repair items.

- Organizing the evidence so photos, invoices, bids, and prior improvements support a coherent scope.

- Helping select the right professionals for the valuation fight, including an appraiser when the matter proceeds that way.

- Managing communication so the carrier gets a clear, documented position instead of fragmented emails and phone calls.

For policyholders who want a better sense of what that broader representation looks like, this overview of the benefits of hiring a public adjuster is a useful starting point.

Homeowners live through a claim once in a while. Insurers and claim professionals work inside these disputes every week. That experience gap is real.

Why this matters specifically in Oregon and Washington

Regional claims have their own practical pressures. Contractor availability can affect bid timing. Weather exposure can complicate temporary repairs. Older housing stock in parts of Portland, Seattle, and surrounding communities can hide layers of prior work, custom materials, or code-related complications that a quick carrier estimate doesn't fully capture.

For homeowners who want representation, NW Claims Management is one Oregon-based public adjusting firm that works with policyholders in Oregon and Washington on residential and other property claims. The practical value of any public adjuster is not the title itself. It's whether they can convert a scattered file into a defensible claim position and help the homeowner choose the right moment to push, supplement, appraise, or escalate.

The strongest strategic move is rarely emotional. It's informed.

Your Next Move to Secure a Fair Settlement

A home insurance appraisal can be one of the most useful tools in a property claim, but only when you use it for the right problem and at the right time. If the insurer agrees there's covered damage and the primary dispute is what it costs to repair, appraisal can shift the fight into a formal valuation process. If the problem is coverage, liability, or a legal denial, another route may be more effective.

That's why preparation matters as much as the clause itself. A clean estimate comparison, strong photos, contractor support, receipts, policy review, and a clear theory of repair give appraisal a real chance to work. Without that foundation, homeowners often enter the process hoping the panel will somehow fill in missing facts for them.

If you're in Oregon or Washington and you're staring at an offer that doesn't reflect the actual cost of restoring your property, don't assume the insurer's first number is the final word. Review the scope carefully. Identify whether the dispute is over value or coverage. Then decide whether negotiation, appraisal, or a more formal escalation is the smart next move.

For policyholders trying to protect their payout, this guide on how to maximize insurance claim payout is a practical next read before you respond to the carrier.

If you want a second set of experienced eyes on a low offer, appraisal decision, or disputed scope of damage, contact NW Claims Management. They provide claim reviews for Oregon and Washington policyholders and can help you determine whether your dispute is best handled through additional documentation, appraisal, or another claims strategy.