The call usually comes after the worst part has already happened. A tenant says the kitchen ceiling collapsed after a pipe burst. The fire department has red-tagged the unit after a small electrical fire filled the building with smoke. A windstorm tore roofing off a duplex and rain got inside before anyone could tarp it.

Your tenant leaves with a few bags. You're left with a damaged property, a stack of bills, and a policy that suddenly matters more than it ever did before.

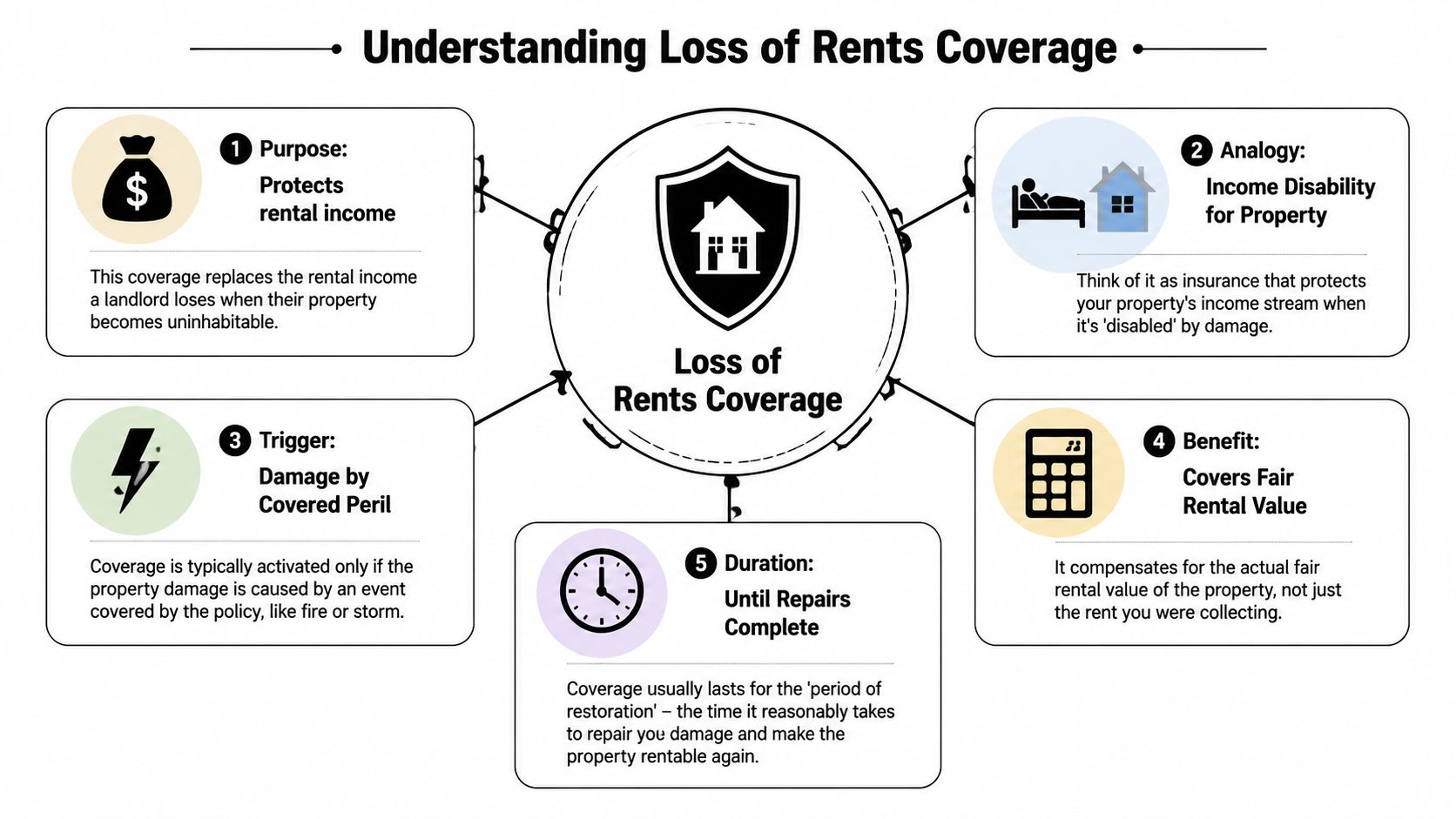

Loss of rents coverage moves beyond insurance jargon to become practical cash flow. If the damage makes the unit uninhabitable and the cause of loss is covered, this part of the policy is supposed to replace the rent you can't collect while repairs are underway. When it works, it keeps a bad situation from becoming a financial spiral. When owners mishandle it, or assume coverage applies when it doesn't, the claim gets smaller fast.

Your Rental Is Uninhabitable Now What

The first problem isn't the drywall, flooring, or cabinetry. It's the gap between what just happened and what still has to be paid.

A landlord in Oregon or Washington can lose rent overnight after a burst pipe, fire, or major storm loss. The tenant can't stay. The contractor hasn't even written an estimate yet. Meanwhile, the mortgage servicer still expects payment, and nobody pauses taxes or insurance premiums because the unit is vacant due to damage.

In real claims, the first few days decide a lot. Owners who move quickly usually preserve more claim value. Owners who wait, clean up too much, or assume the carrier will automatically calculate lost rent correctly often create problems they have to fight later.

What to do in the first day

Start with safety and control.

- Protect people first: If the unit isn't safe, get the tenant out and keep records of when occupancy stopped.

- Report the damage right away: Open the property claim with the carrier as soon as you know the unit may be uninhabitable.

- Document before repairs begin: Take photos and video of every affected room, exterior damage, and any contents or building components that show the scope of loss.

- Prevent additional damage: Tarp, board up, dry out, or shut off water if needed. Keep every receipt.

If water is involved, practical repair information matters. Owners dealing with visible wall damage often need guidance on addressing water stains on drywall because cosmetic signs can point to a much larger moisture problem behind the surface.

The rent loss claim starts the day the property becomes unusable, not the day you finally get a contractor on site.

If your tenant needs help finding a place to land while the property is being evaluated, a temporary housing directory for displaced occupants can save hours of frantic searching.

Defining Loss of Rents Coverage

Think of loss of rents coverage as income disability insurance for the property. The building has been damaged badly enough that it can't perform its job, which is to produce rental income. This coverage is designed to replace that lost income while the property is being repaired after a covered event.

That definition matters because owners often mix it up with other forms of insurance that sound similar but solve different problems.

What it is

In California guidance that closely matches how many landlord policies are discussed nationally, loss of rents coverage, often called Fair Rental Value, is frequently included in standard landlord insurance policies but isn't universally guaranteed, so owners need to verify it directly in the policy. Coverage applies only when a covered peril such as fire, mold, or major water damage renders the unit physically uninhabitable and forces the tenant to vacate. The same guidance notes that insurers typically require lease agreements, rental payment history, damage photos, contractor estimates, and inspection reports to support the claim and calculate payment based on rental value and policy limits, as explained in this overview of Fair Rental Value and loss of rent insurance.

What it is not

It's not protection against every rent problem.

- Tenant non-payment: If the tenant can still live there but stops paying, that's not a loss of rents claim.

- Normal vacancy: If the unit is empty between tenants without property damage, this coverage doesn't step in.

- A homeowner's loss of use benefit: That coverage addresses the insured's own living arrangements, not rental income from an investment property.

- A tenant's business interruption policy: Commercial tenants buy that to protect their own business income. It isn't the landlord's rent protection.

That distinction trips people up, especially with mixed-use buildings or small commercial spaces. If you want a broader look at interruption-related insurance concepts from the business side, this guide offers expert advice for business continuity in a useful plain-English format.

The cleanest way to test the coverage

Ask two questions.

- Was there direct physical damage?

- Did that damage make the unit uninhabitable so rent stopped?

If the answer to either question is no, you may have a property problem, but you probably don't have a loss of rents claim.

What Your Policy Covers and Excludes

After a fire or major water loss, owners usually focus on debris, contractors, and where the tenant will go. The insurance carrier is asking a different question first. What caused the damage, and is that cause covered under the policy? That answer often decides the rent claim before anyone discusses the missing income.

Covered property damage has to trigger the claim

Loss of rents coverage usually does not stand on its own. It follows the building claim. NREIG explains that point clearly in its overview of protecting income with Loss of Rents coverage. If the carrier denies the underlying property damage because the cause of loss is excluded, the rent portion usually goes with it.

That is why the first dispute is often over cause, not math.

A burst supply line may lead to a valid building claim and a valid rent-loss claim if the policy covers sudden and accidental water damage. A river overflow or surface water intrusion can leave the unit just as unlivable, but without separate flood coverage, many landlords find out too late that the rent loss is not insured. I see that problem after winter storms in Oregon and Washington, especially where owners assume all water claims are treated the same.

Losses that are often covered

The details depend on the form, endorsements, and the facts on site, but these are the situations that commonly support a rent-loss claim:

- Fire and smoke damage: The unit cannot be occupied while cleanup, deodorization, and repairs are underway.

- Wind-driven damage: Roof failure, broken windows, and interior water damage can force the tenant out.

- Burst pipes or appliance line failures: Drying equipment, demolition, and reconstruction can make normal occupancy impossible.

- Vandalism with physical damage: Broken doors, damaged walls, or unsafe conditions may suspend rent while the unit is restored.

Owners who are still sorting out the broader policy structure often benefit from understanding landlord insurance before arguing over a specific rent claim.

Exclusions and limitations that catch owners off guard

The hard part is not the obvious denial. It is the partial denial. The carrier may accept some building damage but still limit or reject the rent claim because it says the unit was still livable, the delay was unrelated to repairs, or part of the loss came from an excluded cause.

| Situation | Usually covered under loss of rents coverage | Why |

|---|---|---|

| Tenant stops paying but stays in unit | No | No covered physical damage caused the income loss |

| Vacancy between tenants | No | No insured property loss interrupted rent |

| Flood loss under a policy without flood coverage | No | The cause of loss is excluded |

| Mold, wear and tear, or deferred maintenance issues | Often no | Many policies exclude long-term or maintenance-related conditions |

| Delays caused by owner indecision or slow contractor selection | Often disputed | The carrier may argue the extra time was not part of necessary restoration |

Document habitability early.

For residential rentals in Oregon and Washington, that can mean photos, contractor notes, remediation reports, municipal notices, and written statements from the property manager showing why the tenant could not safely remain. If the dispute turns on repair scope or timing, a repair estimate built on accepted pricing software can help support the restoration position. This is one reason owners and contractors look for Verisk Xactimate training for property damage estimating.

Time limits and policy caps still control

Even with a covered loss, the policy sets boundaries. Payment is usually limited by the restoration period described in the policy and by the coverage limit shown on the declarations page. If repairs stretch out because of permit delays, utility coordination, or code issues, the carrier may question whether all of that time counts.

That matters a lot in the Pacific Northwest. In parts of Oregon and Washington, permit and contractor delays can be real, but the insurer may still push for a shorter repair timeline unless the file shows why the delay was necessary and tied to the covered work.

How to Calculate Your Loss of Rents Claim

After a fire or major water loss, owners usually focus on the repair bill first. The rent claim gets shorted because the math looks simple when it is not. A strong loss of rents calculation has two moving parts: the income the unit would have produced, and the covered time the unit could not be rented.

Start with the income stream you can prove.

If a signed lease was in place, use that rent amount. If the tenant paid for storage, parking, or other charges that are treated as rental income under your policy language, include those items only if the policy supports them. Then subtract any rent received during the same period, including partial payments or occupancy in part of the unit.

Do not estimate from memory. Build the claim from documents the carrier can verify:

- Lease agreement

- Rent ledger or payment history

- Bank statements showing deposits

- Property management statements

- Notice to vacate or other record showing when occupancy ended

The second part is the restoration period. During this period, I often see owners leave money on the table.

A carrier may plug in a short repair timeline based on a limited scope. The actual job may require emergency mitigation, tear-out, drying, mold work, inspections, permits, rebuilding, and a final clearance before a tenant can return. If the timeline is understated, the rent loss is understated too.

The repair schedule needs to match the damage, the local permit process, and the labor market. In Oregon and Washington, permit review, specialty trades, and weather-related delays can affect the return-to-rent date. The carrier may not count every delay, so tie each stretch of time back to covered repair work and keep written support. Owners who want to understand how estimating software influences duration assumptions can review Verisk Xactimate training for repair estimating workflows.

A simple example

Use a worksheet, not a guess.

| Item | Example |

|---|---|

| Monthly rent under lease | $2,500 |

| Months property is uninhabitable during covered repairs | Based on documented repair schedule |

| Rent received during that time | Subtract any amount collected |

| Claimed loss of rents | Monthly rent x covered restoration period, less any rent received, subject to policy limit |

That framework is a starting point, not a universal formula. Some claims involve partial occupancy, phased repairs, tenant early move-outs, or disputes about the date the unit was fit to rent again.

Documents that make the math hold up

A rent loss submission is stronger when the numbers and the timeline support each other.

- Financial proof: Lease, ledger, deposit history, and management records showing the expected rent stream.

- Damage support: Photos, mitigation invoices, contractor estimates, and inspection records showing why the unit could not be occupied.

- Timeline support: Contractor schedules, permit records, material lead times, and communications that explain why repairs took the time they took.

Rent claims usually break down on the timeline, not the monthly rent figure.

Navigating the Claims Process Step by Step

When the property is damaged, stressed owners usually try to solve everything at once. That creates gaps. The cleaner approach is to move in order and document every handoff.

Step 1 and Step 2

Start with notice and evidence.

Report the loss immediately

Many policies require prompt notice. Open the property claim as soon as the damage makes the rental unit unsafe or unusable.Document the condition before changes are made

Take wide shots, room-by-room photos, close-ups of damaged materials, exterior images, and video that captures the full scope. Save files in dated folders.

Step 3 and Step 4

Once the file exists, focus on access and mitigation.

Meet the adjuster with records in hand

Have the lease, payment history, contractor contact information, and a written timeline ready. The field inspection is not the moment to start looking for documents.Mitigate without destroying evidence

Dry-out, emergency board-up, tarping, and water extraction often need to happen quickly. Photograph everything before and after.

A good overview of the broader home insurance claim process after property damage can help owners understand how the rent component fits into the larger building claim.

Step 5 and Step 6

Then build the income portion deliberately.

Submit a separate, organized rent package

Don't assume the carrier will pull the rent loss together from the building file. Send the lease, rent history, vacancy date, habitability support, and projected repair duration in one package.Track ongoing delays and updates

Repair delays, permit issues, supplemental damage, and inspection hold-ups can affect the covered period. Update the carrier in writing when the timeline changes.

What the insurer usually asks for

Expect requests for the following:

- Proof of tenancy: Signed lease or rental agreement.

- Proof of income: Ledger, deposit records, or management statements.

- Proof of uninhabitability: Photos, contractor opinions, inspection results, or municipal notices.

- Proof of repair duration: Estimates, schedules, invoices, and status updates.

Keep one claim diary. Date every call, email, inspection, promise, and payment. Owners who keep a clean chronology are harder to push around.

Common Pitfalls and Advanced Scenarios

The biggest mistakes in loss of rents claims usually come from assumptions. Owners assume the carrier's timeline is reasonable. They assume vacancy kills coverage in every case. They assume code issues or permitting delays are automatically reflected in the payment. Often, none of that is true.

The vacant unit problem

One of the most misunderstood issues involves units that are empty when the loss occurs. Consumer articles often frame loss of rents coverage as simple rent replacement after a tenant is displaced. That's not always the whole story.

A legal analysis of commercial property policies notes that lost-rents provisions may depend on physical damage to covered structures and can apply even when there is no tenant in place, a nuance that is often missed in consumer discussions of the topic, as explained in this analysis of loss of rents coverage under commercial property insurance.

That doesn't mean every vacant residential unit is covered. It means you cannot stop your analysis at “there was no tenant.” Commercial forms, mixed-use property forms, and manuscript language can be more nuanced than landlords expect.

Where owners leave money behind

Three issues show up repeatedly.

- Repair time is underestimated: The carrier may price the repair correctly but compress the schedule. That cuts the rent claim.

- Code and permit realities are ignored: Older buildings in Oregon and Washington often trigger added steps once walls are opened, especially after fire and water losses.

- Partial usability gets overstated: A carrier may argue the property was rentable sooner than it was because one area looked finished while key systems were still offline.

If you've never seen how claim handlers frame these arguments, reviewing common insurance adjuster tricks used to limit settlements helps owners spot the pattern early.

Practical warning signs

Watch for these red flags in your file:

- The rent claim is discussed only verbally: Get the insurer's position in writing.

- The restoration timeline never gets revised: If supplemental damage was found, the timeline should move too.

- The adjuster focuses only on visible finishes: Habitability depends on more than paint and flooring. Plumbing, electrical, drying, inspections, and safety all matter.

When a property can't legally or safely be rented, the dispute often turns on documentation, not common sense.

The Public Adjuster's Role and Oregon Washington Notes

A public adjuster represents the policyholder, not the insurance company. In a loss of rents claim, that matters because the income portion often gets treated like a side issue when it should be documented and negotiated with the same care as the building damage.

The work usually comes down to four pressure points. Reading the policy for hidden limits and conditions. Proving when habitability ended and resumed. Building a realistic repair timeline. Packaging the financial records so the carrier has less room to minimize the claim.

For Oregon and Washington owners, the local details matter. Pacific Northwest claims often involve roof leaks, wind-driven rain, burst pipes during cold snaps, and moisture-related complexity after the initial event. Those losses rarely move in a straight line. Drying, mold concerns, contractor availability, and permit timing can all affect when a unit becomes rentable again. Older housing stock can add code complications that stretch restoration beyond the first estimate.

That's one reason owners here benefit from a representative who knows the local claim environment and state-specific public adjusting rules. If you need Oregon-specific guidance on representation, licensing, and what a policyholder advocate does, this page on working with a public adjuster in Oregon is a useful starting point.

If there's one practical takeaway, it's this. Don't treat loss of rents coverage as automatic, and don't treat it as secondary. It's often the part of the claim that keeps the property financially stable while everything else is being rebuilt.

If you're dealing with a fire, water, storm, or vandalism loss and need help sorting out the rent portion of the claim, NW Claims Management works with Oregon and Washington policyholders to evaluate coverage, document damages, and pursue a fair insurance settlement.