A windstorm rolls through Oregon or Washington overnight. In the morning, your fence is down, branches are everywhere, and your car has fresh damage that wasn't there the day before. Then the insurance process starts. The carrier's estimate feels thin. The photos they relied on don't tell the whole story. The adjuster focuses on what can be seen from a quick walkaround, while you know something underneath may also be wrong.

That gap is where auto inspection jobs matter to your wallet.

A vehicle inspector is often thought of as someone who signs off on safety checks or works at a dealership. In claims, the right inspector does something more valuable. They document damage in a way that turns suspicion into evidence. That matters after collisions, hail, fallen limbs, flood exposure, vandalism, and debris strikes. A proper inspection can separate cosmetic damage from structural damage, identify repair issues the first estimate skipped, and support a more accurate valuation when the insurer is deciding whether to repair the vehicle or treat it as a total loss.

Policyholders in the Pacific Northwest often understand the value of a public adjuster for a building claim. The same logic applies to vehicles. A qualified inspector can become the technical voice that backs up your side of the file.

Your Guide to Auto Inspection Jobs and Winning Your Claim

A common claims problem starts the same way. The insurer writes an estimate from photos, an app, or a short field visit. The number comes back lower than expected. The vehicle owner looks at cracked trim, bent panels, possible suspension issues, warning lights, or water exposure and realizes the estimate only captured part of the loss.

That's when the job title matters less than the function.

An auto inspector is often the person who turns a vague complaint into a defensible record. In the United States, there are over 3,632 vehicle inspectors employed across the country, and that workforce exists in part because 37 U.S. states and the District of Columbia require mandatory inspection laws according to Zippia's vehicle inspector demographics. For a policyholder, that means you're not dealing with a fringe specialty. You're dealing with an established profession built around documenting vehicle condition.

Why this matters after a low offer

When an insurance company controls the first inspection, it controls the first version of the story. That doesn't always mean bad faith. It often means speed, limited access, or an estimate written before hidden damage appears. A strong independent inspection changes the discussion from "I think they missed something" to "here is the documented condition of the vehicle."

Practical rule: The more technical the dispute, the less useful a general complaint becomes. You need findings, photos, measurements, and repair logic.

That is especially important when a vehicle claim overlaps with a larger property loss. Homeowners dealing with storm damage already have enough on their plate. If you're also weighing whether broader claim help makes sense, this guide on when to hire a public adjuster gives useful context for the building side of the file.

The inspector's role in plain English

The best inspectors don't argue emotionally. They document methodically. They note impact points, secondary damage, alignment concerns, mechanical symptoms, electronic faults, corrosion risk, and whether prior wear is separate from new loss.

That kind of report can help you push back when:

- The estimate is too narrow: It covers visible panels but skips likely mechanical follow-up.

- The insurer treats damage as pre-existing: A detailed condition report can help separate old wear from fresh loss.

- The repair plan seems incomplete: Inspectors can identify items that should be checked before a repair is finalized.

If your claim involves meaningful vehicle damage, understanding auto inspection jobs isn't career trivia. It's part of protecting the value of your claim.

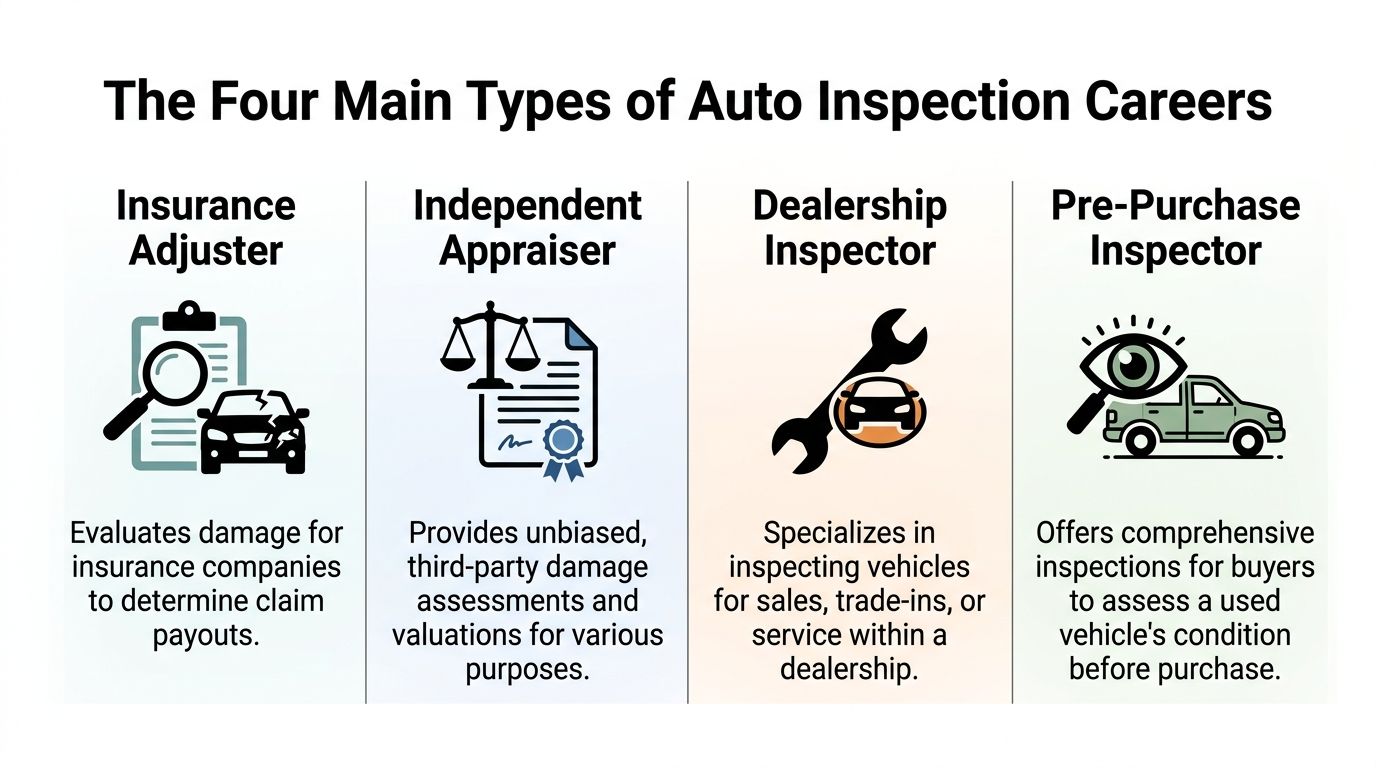

The Four Main Types of Auto Inspection Careers

Most policyholders hear "inspector" and assume every inspector does the same work. They don't. In claims, that distinction matters because different inspectors answer to different priorities.

The easiest way to understand auto inspection jobs is to sort them by who they serve and what question they're trying to answer.

State and compliance inspectors

These inspectors focus on whether a vehicle meets legal or regulatory requirements. Their lens is compliance. They care about safety items, emissions-related issues where required, documentation standards, and whether the vehicle can pass the rules that apply in that setting.

For a claim, this type of inspection can matter when the damage affects roadworthiness. If suspension parts are compromised, lights no longer function correctly, or emissions-related components were hit, compliance becomes part of the loss picture.

What works with this type of inspector is using them when a legal pass-or-fail issue exists. What doesn't work is expecting them to provide a full claim valuation narrative. Their job is usually narrower.

Dealership and service-lane inspectors

These are the people who inspect trade-ins, certify used inventory, evaluate service needs, and identify repair items before a sale or after intake. They often know the specific make, model, and recurring failure points well.

That can be useful if your damaged vehicle has manufacturer-specific systems, trim packages, or known weak points. A dealership inspector may spot issues a general observer misses. The trade-off is that their report may be built around service recommendations rather than claim presentation.

A dealership inspection tends to help most when the dispute is technical, such as:

- ADAS concerns: Cameras, sensors, and related calibration issues after an impact.

- Brand-specific components: Hybrid systems, proprietary electronics, and model-specific repair procedures.

- Repair verification: Whether a prior repair returned the vehicle to pre-loss condition.

Insurance company field inspectors

These professionals are often competent and experienced. But their assignment is not the same as yours. They are usually asked to evaluate damage for the carrier, confirm causation, and help control the claim's repair scope and payout.

That doesn't make them your enemy. It does mean their report is not independent.

If you're trying to sort out the difference between insurer-side and policyholder-side claim roles, this breakdown of public adjuster vs insurance adjuster helps clarify who works for whom.

The right question isn't whether the insurer's inspector is qualified. It's whether their assignment aligns with your financial interest.

Many policyholders encounter a common pitfall. They assume one inspection equals a final answer. In practice, one inspection is often just one version of the file.

Independent appraisers and third-party vehicle experts

For a disputed claim, this is often the most valuable category. An independent appraiser or vehicle damage expert isn't there to sell the car, certify inventory, or manage the insurer's cost exposure. Their role is to evaluate condition and damage with a defensible record.

They usually become important when there is disagreement about repair cost, hidden damage, diminished value concerns, pre-existing condition arguments, or total-loss valuation.

Here's a simple comparison:

| Inspector type | Primary loyalty | Best use in a claim | Main limitation |

|---|---|---|---|

| State/compliance inspector | Regulation and safety rules | Roadworthiness and compliance issues | Narrower valuation role |

| Dealership inspector | Service department or dealer operations | Brand-specific damage review | May focus more on repair intake than claim strategy |

| Insurance field inspector | Insurance carrier assignment | Initial claim scope and causation review | Not independent from the payout decision |

| Independent appraiser | Objective third-party assessment | Disputed damage and valuation support | Usually most useful when there is already a dispute |

Which one protects your interests best

If your claim is straightforward and the insurer's estimate is complete, you may not need much beyond the standard process. But when the estimate feels rushed, the repair plan looks incomplete, or the damage could affect value beyond a dented panel, independent expertise becomes more important.

Use this simple filter:

- Need legal pass/fail confirmation: look to compliance-focused inspection.

- Need model-specific technical insight: dealership or specialist service inspection may help.

- Need a carrier estimate reviewed: compare it against a third-party assessment.

- Need objective support in a dispute: independent appraisal is usually the strongest fit.

The mistake I see most often is hiring the wrong kind of expert for the wrong problem. A pre-sale inspection mindset won't carry a contested insurance claim very far. A claim dispute needs documentation built for scrutiny.

An Inspector's Core Duties and Daily Tasks

A good vehicle inspector works like a detective. Not the dramatic kind. The useful kind. They start with what can be observed, then test whether those clues point to something larger.

The daily work is less about one big discovery and more about disciplined verification. Transportation vehicle inspectors perform core tasks including damage assessment, regulatory compliance verification, and repair validation, with those duties rated highly for importance by O*NET's transportation vehicle inspector profile. In claim disputes, that matters because a detailed inspection creates objective benchmarks that are harder to wave away.

The walkaround is only the start

The first pass usually begins outside the vehicle. The inspector looks at body lines, panel gaps, glass, lights, trim, wheel position, and obvious impact areas. A trained eye also watches for subtle clues. Uneven spacing, fresh abrasion near hidden fasteners, rippling in adjacent panels, and mismatch between visible damage and claimed impact direction.

Then comes the question that separates a real inspection from a casual opinion. If this part took the hit, what else may have moved with it?

A proper inspection often follows the chain of force through connected systems. A curb strike might not stop at the wheel. It can point toward suspension, steering, alignment, tire damage, or underbody contact. Water intrusion isn't just wet carpet. It raises concerns about wiring, connectors, corrosion, sensors, and future intermittent failures.

What inspectors actually document

A serious report doesn't just say "front-end damage" or "storm damage present." It breaks findings into categories that can be evaluated and priced.

Typical documentation includes:

- Visible exterior damage: Cracks, dents, paint transfer, shattered glass, broken lamps, torn trim.

- Structural or mounting concerns: Bent supports, attachment point issues, deformation around impact zones.

- Mechanical symptoms: Pulling, noise, vibration, warning lights, fluid leaks, limited operation.

- Electronic issues: Sensor faults, camera problems, battery concerns, intermittent warnings.

- Condition evidence: Photos, notes, scan findings where applicable, and repair-related recommendations.

For policyholders, this level of detail matters because insurers tend to respond better to organized findings than general frustration.

A thin estimate often reflects a thin inspection. If the inspection gets deeper, the claim discussion usually gets better.

Repair validation is its own job

Inspection doesn't stop once the vehicle enters a shop. One of the most underrated parts of auto inspection jobs is confirming whether repairs were completed properly.

That can include checking whether damaged parts were replaced or repaired as planned, whether calibrations were addressed, whether warning lights remain, and whether the final condition matches the pre-loss objective. This matters when a shop supplements the repair plan or when the insurer questions added work.

A solid post-repair review can uncover problems such as:

| Issue | Why it matters to the claim |

|---|---|

| Incomplete repair steps | The insurer may need to reconsider unpaid items |

| Persistent fault indicators | The vehicle may not be fully restored |

| Cosmetic shortcuts | Final value and appearance may still be impaired |

| Missed hidden damage | The original scope may have been too narrow |

The tools are ordinary. The judgment isn't.

Flashlights, mirrors, scan tools, tablets, measuring references, and photo documentation are common. What separates a strong inspector is judgment. They know when a scratch is just a scratch and when it indicates deeper movement. They know the difference between old wear and fresh event-related damage. They know what has to be checked before anyone can call a vehicle fully repaired.

That rigor is why an inspector's report can carry real weight in a negotiation. You aren't paying for someone to notice a dent. You're paying for someone to understand what the dent may mean.

If you're dealing with broader loss documentation, this overview of property damage assessment is useful because the same principle applies across claims. Detailed facts beat assumptions.

Essential Skills and Certifications for Inspectors

Not every person who has worked around cars can produce a claim-ready inspection. That's the first distinction policyholders need to make. Familiarity with vehicles matters, but credibility comes from deeper skill, repeatable process, and the ability to explain findings under scrutiny.

Industry standards often require at least three years of hands-on automotive technician experience to qualify for inspection roles, according to DARCARS guidance for auto inspectors. That makes sense. A vehicle is a linked system. One failed component can trigger symptoms somewhere else, and a weak inspector often misses the connection.

What separates a credible inspector from a casual evaluator

The strongest inspectors usually combine mechanical experience with disciplined documentation. They don't just know what they're looking at. They know how to record it so another party can follow the logic.

Look for these traits.

- System thinking: A credible inspector understands how brakes, suspension, steering, structural points, electronics, and emissions-related components interact.

- Damage discrimination: They can separate new loss from prior wear, deferred maintenance, and unrelated defects.

- Report discipline: They write clearly, use organized photos, and explain why a finding matters.

- Comfort with technology: Modern claims often involve warning systems, onboard diagnostics, sensors, and software-related complaints.

- Credibility under pushback: They can defend their findings when a shop, insurer, or opposing expert asks hard questions.

A weak evaluator often sounds confident in person and vague on paper. That's a bad combination in a claim.

Certifications help, but they aren't magic

People often ask whether ASE certification is enough. It's valuable, but no single credential replaces judgment. A certificate can show baseline competence or commitment to the trade. It doesn't automatically mean the person is strong at claim documentation, valuation disputes, or post-loss causation issues.

The better approach is to treat certifications as one part of a bigger vetting process.

Ask practical questions such as:

- What kind of inspections do you perform most often? A person who mainly handles pre-sale checks may not be the best fit for a disputed storm loss.

- How do you document hidden-damage concerns? Listen for a method, not just confidence.

- Can you explain your report to an insurer or attorney if needed? Communication matters.

- What vehicle systems are you most comfortable diagnosing? This becomes critical with electrical or sensor-heavy damage.

- How do you distinguish fresh event damage from prior condition? That's a central issue in many claims.

Field test: If the inspector can't explain their process in simple language, don't expect their report to persuade a skeptical carrier.

Mechanical experience still matters more than buzzwords

Modern cars have cameras, modules, sensors, and software dependencies. That doesn't reduce the importance of core mechanical skill. It increases it. Good inspectors still need to understand impact patterns, suspension geometry, corrosion risk, fluid intrusion, restraint-system concerns, and the way minor visible damage can mask larger structural or operational problems.

This is also why career changers can succeed if they bring the right transferable skills. Claims professionals, for example, often already know how to document damage, compare condition against a standard, write defensible notes, and handle disagreement without losing focus. Those skills don't replace technical automotive knowledge, but they do shorten the learning curve in inspection-heavy roles.

How policyholders should vet an inspector

You don't need to interview an inspector like you're hiring a shop foreman. But you do need enough information to know whether their opinion will hold up.

A practical screening table helps:

| What to ask | Strong sign | Weak sign |

|---|---|---|

| Background | Direct technician or inspection experience across multiple vehicle systems | Only general automotive familiarity |

| Documentation style | Sample reports with organized photos and clear explanations | Mostly verbal opinions |

| Claim familiarity | Understands supplements, disputes, causation issues, and repair validation | Focuses only on service recommendations |

| Technology comfort | Familiar with scans, electronics, and sensor-related concerns | Avoids anything beyond visible damage |

Ongoing learning matters more now

Vehicles don't stay still as a trade. Inspectors need current knowledge because older habits don't always fit newer systems. Sensor calibration, electronic faults after moisture exposure, and hidden issues after seemingly minor impacts can change the scope of a claim fast.

For policyholders, the takeaway is simple. Don't just ask whether someone "knows cars." Ask whether they know how to inspect a damaged car in a way that stands up in a dispute.

And if the insurer resists a well-supported outside opinion, that's often the point where strong representation and strategy around negotiating with the insurance company become more important than one more phone call.

Salary and Job Outlook in the Pacific Northwest

Auto inspection jobs aren't side gigs. The compensation and outlook show that this is a real trade with staying power, and that's relevant to policyholders because serious professions produce better experts.

Employment in automotive service fields, including inspection-related work, is projected to grow 4% from 2024 to 2034, and the median annual wage is $49,670, according to the Bureau of Labor Statistics automotive service technicians and mechanics outlook. For Oregon and Washington claimants, the practical implication is straightforward. There is a stable labor pool of people whose work includes diagnosing, documenting, and evaluating vehicle condition.

What the numbers mean in real life

A stable occupation tends to produce two things policyholders care about. First, more experienced people stay in the field long enough to build judgment. Second, there is usually a broader network of technicians, inspectors, and specialists available when a claim turns technical.

That matters in the Pacific Northwest because vehicle losses here are rarely one-note. Storms can combine impact damage and moisture exposure. A crash can be followed by disputes over electronics, alignment, or hidden underbody issues. Commercial owners may also have pressure to return vehicles to service quickly, which makes the quality of the inspection more important.

Why regional context matters

Washington and Oregon aren't identical claim environments, but they share a common problem. Vehicle damage often arrives in the middle of larger property disruption. When a homeowner or business owner is already dealing with roofing, water, debris, or operational downtime, a vehicle claim can get under-documented because no one has time to chase every technical issue.

That's one reason independent expertise carries value beyond the inspection fee. You're not only paying for technical knowledge. You're paying for someone to slow the process down enough to get the facts right.

Here's a practical way to think about the profession's value:

- For policyholders: A recognized, paid specialist is more persuasive than a vehicle owner's unsupported opinion.

- For career changers: The field offers stable demand and multiple entry points.

- For businesses: Inspection capacity helps reduce delay when damage must be documented and repaired correctly.

The job outlook also supports claim strategy

When a field has steady demand, you can usually find specialists with different strengths. Some are better with commercial equipment. Some are better with dealership-grade diagnostics. Others are stronger in independent appraisal and dispute work.

That gives policyholders an advantage. You aren't limited to the first opinion on the file.

And if your vehicle loss sits inside a larger insurance matter, understanding the broader property damage claim process helps you coordinate the vehicle side with the rest of the claim instead of letting it get treated as an afterthought.

How to Get Hired in Auto Inspection

The most practical route into auto inspection jobs isn't always the obvious one. Many people assume the only path runs through a dealership service bay. That's a common route, but it isn't the only one.

There's a meaningful opportunity for people with insurance adjusting backgrounds to move into this work because many postings value damage assessment and policy interpretation experience, and some offer training. Verified job-market guidance also notes national pay ranges of $17 to $60 per hour for these roles in certain listings, as reflected in Indeed's auto inspector job listings context.

The straight-line path

The traditional route usually looks like this: gain hands-on technician experience, become the person others trust to diagnose difficult issues, learn documentation discipline, then move into inspection-heavy roles.

That path works well because it builds real technical credibility. If you're already in a shop, the smartest move is to get experience with intake inspections, post-repair verification, safety-related findings, and customer-facing explanations. Those are the parts of the job that transfer most directly into claim-related work.

A strong early-career candidate usually shows:

- Hands-on repair background: Not just parts swapping, but actual diagnostic thinking.

- Clear written communication: Inspection jobs produce paper trails.

- Photo discipline: Good visuals often carry as much weight as the narrative.

- Calm under disagreement: People challenge claim findings all the time.

The less obvious path from claims into inspection

This is the gap many articles miss. Claims professionals often have more relevant overlap than they realize.

If you've worked as an adjuster, estimator, or field damage documenter, you may already know how to inspect for scope, organize evidence, compare observed damage to a reported event, and write in a way that supports a decision. The missing piece is usually deeper automotive technical knowledge, not the inspection mindset itself.

That means a transition can work when the person intentionally closes the technical gap.

A useful pivot plan looks like this:

Audit your overlap

List the tasks you already do well. Damage documentation, file organization, policy reading, negotiation, and causation analysis all transfer.Add vehicle-specific competence

Spend time in environments where you can observe repair logic, scan tool usage, and common mechanical relationships. You need enough depth to avoid superficial reports.Build proof, not just interest

Employers want to see sample documentation, mechanical fluency, and evidence that you understand vehicle systems.Target the right roles first

Start with positions that value field inspections, damage review, condition reporting, or claim support rather than jumping straight into highly specialized technical roles.

A hiring manager can teach a disciplined claims professional more technical detail. It's harder to teach an experienced technician how to document like a claims professional under dispute pressure.

Resume and interview advice that actually helps

Most resumes for this field fail because they read like generic service histories. They list duties instead of proving judgment. If you want a useful primer on structure and presentation, this guide to writing a resume that gets you hired is worth reviewing before you apply.

Your resume should emphasize evidence-producing work. That includes inspection, diagnostics, repair verification, damage review, file documentation, customer explanation, and any role where your observations affected a financial or repair decision.

Interview preparation should be practical. Expect questions such as:

| Question | What the employer is testing |

|---|---|

| How do you handle hidden damage concerns? | Whether you think beyond visible loss |

| How do you document a disputed condition issue? | Writing discipline and objectivity |

| What do you do when the reported event doesn't match the vehicle evidence? | Causation judgment |

| How comfortable are you with scans and modern electronics? | Technical range |

Where candidates go wrong

The most common mistakes are predictable.

- Overstating expertise: If you don't know suspension, electronics, or structural indicators well, don't bluff.

- Underplaying documentation: Many applicants talk only about repairs and ignore report writing.

- Applying too broadly: A pre-purchase role, dealership role, insurer field role, and independent appraisal role don't ask for the same strengths.

- Ignoring claim logic: In many inspection jobs, especially disputed ones, the issue isn't just what is damaged. It's whether you can explain why it matters.

For people entering the field from the Pacific Northwest claims world, that last point is often where they stand out. The industry needs people who can connect damage facts to real financial consequences.

Why Expert Inspection Is Your Best Tool in a Claim

When a vehicle claim gets expensive, technical, or contested, opinions stop mattering and documentation takes over. That's the thread running through all auto inspection jobs. The useful inspectors are the ones who can convert visible damage, hidden concerns, and repair questions into a record another party has to deal with seriously.

Policyholders usually lose their advantage when they rely on general statements. "The car doesn't feel right." "I think they missed something." "The payout seems low." Those are understandable reactions. They just don't move a file very far.

An expert inspection does.

The right inspection clarifies which type of professional you need, what a proper review should include, and why qualifications matter. It also helps you avoid a common mistake. Many people assume the insurer's first estimate is the full reality of the damage. Sometimes it is. Often it isn't. Vehicles are complex, and losses involving storms, impact, moisture, or electronics can look smaller at first glance than they really are.

What actually protects your settlement

The strongest claim support usually includes a few consistent elements:

- Independent judgment: The report isn't shaped by the insurer's payout goal.

- Technical depth: Findings go beyond surface damage.

- Clear documentation: Photos, notes, and repair logic line up.

- Credible qualifications: The person behind the report can explain and defend it.

If a claim turns into a technical argument, the side with the better inspection usually has the better chance.

For Oregon and Washington policyholders, this matters even more because vehicle losses often happen during broader property events. When you're juggling contractors, temporary repairs, cleanup, and insurer communication, it's easy for the vehicle portion to get treated as secondary. That can cost real money.

A strong inspector helps fix that by narrowing the dispute to evidence instead of frustration. That's good for homeowners, business owners, nonprofits, and anyone trying to recover fully after a disruptive loss.

If your insurer's number doesn't reflect what happened to your vehicle or your property, NW Claims Management can help you document the loss, interpret the policy, and push for the full settlement your claim supports.