The fire trucks are gone. The water has stopped running. The tree is off the roof. Then the insurance estimate lands in your inbox, and suddenly the main fight starts.

You scan the document and see two terms that will decide how hard this loss hits your savings: ACV and RCV. Their meaning often goes unknown until a claim is already in progress. By then, the confusion is expensive.

If you've just suffered a property loss, this isn't an academic question. It's the difference between getting paid for what you owned as a used item or getting paid what it takes to replace it today. And if your policy uses a two-check system, the insurer may hold back part of the money until you finish the work, prove the cost, and satisfy the policy conditions. That catches a lot of people off guard.

Here's the short version: replacement cost is usually the better coverage, but it doesn't automatically mean you'll receive all that money up front. Actual cash value is cheaper coverage, but it often turns a property claim into a financing problem. That's especially brutal after a major home loss, and even worse for businesses and nonprofits that need to keep operating.

Your Insurance Settlement The Two Acronyms That Matter Most

A homeowner in the Pacific Northwest calls after a windstorm tears up part of the roof. The carrier sends an estimate. It lists replacement pricing for shingles, labor, and tear-off, which looks promising for about three seconds. Then the next line appears: depreciation. The first check is much smaller than expected.

That moment is where actual cash value vs replacement cost stops being insurance jargon and starts affecting whether repairs happen now or stall out.

The first mistake people make

Most policyholders assume a covered loss means the insurer writes a check for the full cost to fix the damage. Sometimes that happens. Often it doesn't.

What usually matters is the valuation method in the policy and the claim payment process tied to it. If the policy pays actual cash value, the insurer reduces the payment for age, wear, and condition. If the policy pays replacement cost, the insurer may still start by paying only the depreciated amount and release the rest later.

Practical rule: Don't judge your claim by the first check. Judge it by the policy language, the estimate line items, and what conditions control the second payment.

Why this matters right now

When you're dealing with smoke, water, storm, or vandalism damage, cash flow becomes urgent. Contractors want deposits. Emergency mitigation vendors want approval. Temporary housing, cleanup, storage, and business interruption pressures don't wait for the insurer's internal timeline.

If you understand ACV and RCV early, you can make better decisions immediately:

- Whether to push back on depreciation

- Whether the first payment is final or only partial

- Whether you need to document replacement costs aggressively

- Whether the claim creates a dangerous funding gap

That clarity matters more than any generic coverage summary.

What Are Actual Cash Value and Replacement Cost

Actual cash value and replacement cost answer one simple question differently: what is the insurer paying for?

Actual cash value means used value

Under actual cash value, the insurer pays the amount of the loss after subtracting depreciation for age and wear. The North Carolina Department of Insurance explains that ACV is the amount needed to fix a home minus the decrease in value from age or use, while RCV is the amount needed to repair a home at today's prices or replace belongings at today's cost, and it also notes that replacement-cost claims commonly involve an initial ACV payment followed by reimbursement of recoverable depreciation after repair or replacement is completed and receipts are submitted, as described in the North Carolina Department of Insurance guidance on ACV and RCV.

Consider a car. If someone totals a brand-new vehicle, nobody argues it has full value. If the same model is older and worn, the market treats it differently. Insurance does the same thing with roofs, flooring, furniture, appliances, and contents under ACV.

Replacement cost means current replacement pricing

Under replacement cost, the goal is to pay what it costs to repair or replace with property of similar kind and quality at today's prices, without deducting depreciation from the final covered amount. That's why replacement cost usually gives better claim protection.

For renters, this distinction is often hidden in the personal property section of the policy. If you're sorting through a contents loss, this breakdown of replacement cost renters insurance is worth reviewing because many tenants assume belongings are covered at new value when they're insured at depreciated value.

The plain-English difference

Use this rule of thumb:

| Coverage type | What it pays for | What hurts policyholders |

|---|---|---|

| Actual Cash Value | The damaged item's depreciated value | You often have to fund the gap yourself |

| Replacement Cost | The cost to replace with similar new property | You may have to wait for the held-back amount |

If your goal is to restore the property, replacement cost is stronger. If your policy pays actual cash value, expect the insurer to value your loss like used property, not new property.

How Insurers Calculate Your Payout A Real-World Example

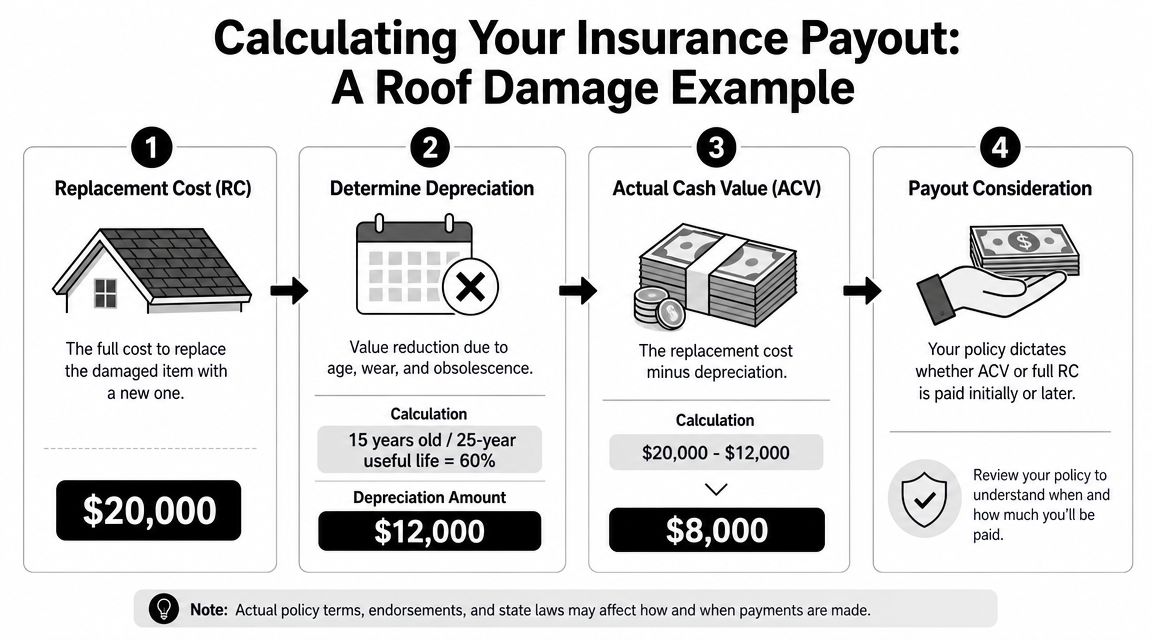

The easiest way to understand actual cash value vs replacement cost is to follow one damaged item through the claim.

Let's use a roof because that's where a lot of disputes start. Assume the roof is old enough that the insurer applies substantial depreciation, and the current replacement price is far higher than what the roof cost years ago.

The ACV version of the claim

Under an ACV policy, the math follows a familiar pattern: replacement cost minus depreciation. Progressive describes ACV that way and notes the practical result is a lower initial indemnity and a larger out-of-pocket gap, especially on older items such as electronics, appliances, and roofing, in its explanation of replacement cost vs actual cash value.

Here's what that means in practice on a roof claim:

| Step | Claim treatment under ACV |

|---|---|

| Estimate the replacement cost | What it costs today to replace the damaged roof |

| Apply depreciation | Reduce the value for age, wear, and condition |

| Issue payment | Pay the depreciated amount, subject to the policy terms |

That sounds straightforward until you're the one trying to hire a roofer with a reduced check in hand.

The RCV version and the two-check system

Replacement cost coverage is better, but policyholders frequently face an unexpected challenge. Insurers often don't send the full replacement amount immediately. Allstate notes that replacement cost is the more protective standard because it pays to repair or replace damaged property using materials of like kind and quality without deducting depreciation from the final covered amount, while actual cash value reduces the payout for age, wear and tear, and condition. It also explains the common claims milestone of recoverable depreciation, where the insurer may pay the ACV first and then the remaining difference after repairs are completed and documented, as outlined in Allstate's guide to actual cash value vs replacement cost.

So the payment sequence often looks like this:

- The insurer prepares an estimate using current pricing for the repair.

- The insurer withholds depreciation and issues an initial ACV payment.

- You complete the repair or replacement and keep the invoices, contracts, and proof of payment.

- You request the recoverable depreciation and submit the supporting documents.

- The insurer reviews the file and releases the held-back amount if the policy conditions are met.

Don't miss the significance of that process. A replacement cost claim can still feel like an ACV claim at the start because the first check may be based on depreciated value.

If the loss involves water, the repair timeline can get messy fast because mitigation, drying, demolition, and rebuild work overlap. Many policyholders don't understand that sequence until they read a practical breakdown of what is water damage restoration, and by then they've already approved work without lining up the claim documentation they'll need later.

Where disputes usually begin

The insurer's estimate isn't just a number. It's a position. It reflects pricing assumptions, scope choices, material selections, labor inputs, and depreciation decisions. If you've ever heard adjusters mention Xactimate, that's one of the main pricing systems behind those estimates. Understanding how those estimates are built helps you spot what was missed, which is why background on Verisk Xactimate training can be useful when you're reviewing a carrier worksheet.

The two-check system creates three practical risks:

- Liquidity risk because you may need contractor money before recoverable depreciation is released

- Documentation risk because missing invoices or incomplete submissions can delay the second payment

- Deadline risk because some policies require replacement within a specific time or under specific conditions

That's why I tell clients the first estimate is not the finish line. It's the opening position.

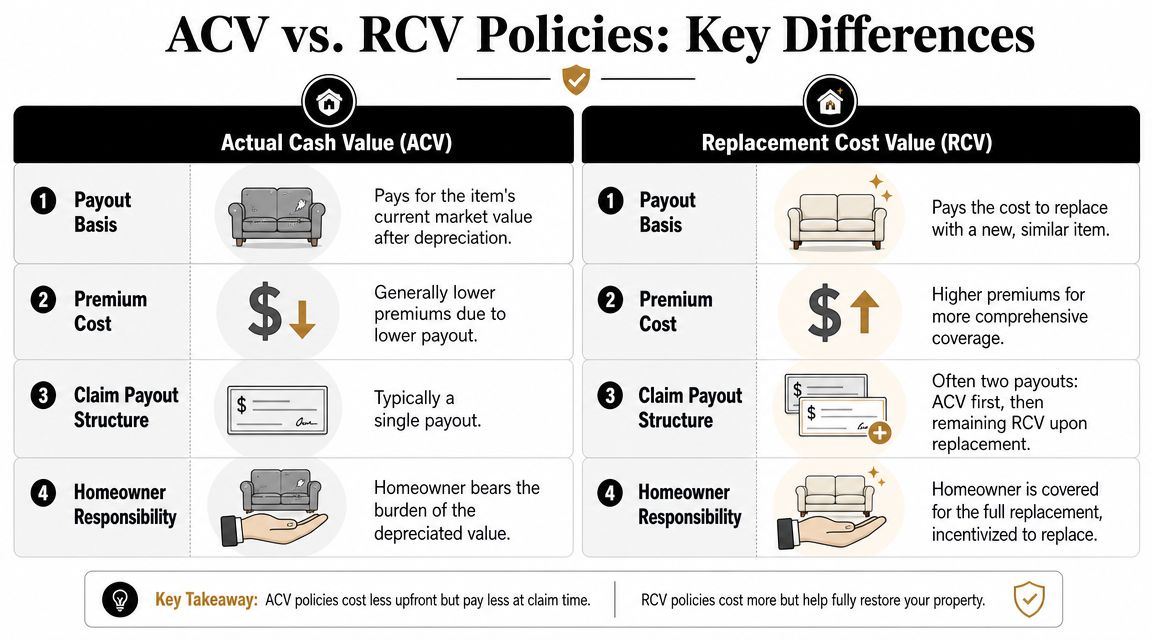

Key Differences Between ACV and RCV Policies

You don't need a dense policy analysis to understand the stakes. You need a side-by-side look at how each option behaves when a real claim lands.

| Issue | Actual Cash Value | Replacement Cost Value |

|---|---|---|

| Basis of payment | Depreciated value | Cost to replace with similar new property |

| Depreciation | Deducted | Not part of the final covered replacement payment |

| Typical premium impact | Usually lower | Usually higher |

| Upfront cash burden | Higher burden on the policyholder | Often lower overall burden, but not always lower at the start |

| Claim payment pattern | Often one depreciated payment | Often ACV first, then recoverable depreciation later |

| Best fit | People willing to absorb more loss themselves | People who want stronger restoration protection |

Premium savings versus claim adequacy

This is the trade-off in one sentence: ACV is cheaper before the loss and harsher after it.

That isn't a moral judgment. It's just how the risk is allocated. If the insurer only owes depreciated value, the carrier's exposure is lower. That's why ACV often costs less. But lower premium doesn't mean better value if a major loss leaves you unable to restore the property.

Why old property gets hit hardest

The older the item, the more painful ACV usually becomes. Roofs, siding, flooring, appliances, electronics, tenant improvements, and older contents can all produce a bigger gap between what the insurer pays and what replacement costs.

That gap matters less if you were planning to cash out and walk away. It matters a lot if you need the property functional again.

Claim reality: Replacement cost is usually the better benchmark when your goal is restoration, not liquidation.

Complexity versus finality

ACV has one advantage that people rarely mention. It's simpler. The claim often settles faster because the insurer pays the depreciated value and closes the issue. There's no second stage to chase.

RCV is stronger financially, but the process is more demanding. You have to manage contractors, invoices, replacements, deadlines, and requests for recoverable depreciation. If you don't complete those steps cleanly, you can leave money uncollected even though the policy appears more generous on paper.

My recommendation

For most homeowners, replacement cost is the right choice. For most businesses, nonprofits, schools, and municipalities, it's even more important. ACV might trim premium, but it often shifts too much restoration risk back onto the insured when the loss occurs.

If you already have an ACV claim, don't assume the carrier's depreciation is correct. Scrutinize it.

Special Notes for Oregon and Washington Property Owners

In Oregon and Washington, the coverage label alone doesn't tell you enough. You also need to know how the claim will work on the ground, especially if the loss involves roofing, siding, code issues, or partial damage that creates appearance and consistency disputes.

Matching and related scope issues

One of the most overlooked issues in property claims is matching. A policyholder may have damage to only one slope, one elevation, or one section of a building, but replacing only the damaged portion can leave the property visibly mismatched. That matters on homes, multifamily buildings, churches, schools, and commercial sites where appearance and uniformity affect usability and value.

Texas consumer guidance points out another part of this problem: significant financial pressure often comes from policy features beyond the ACV or RCV label, including matching, ordinance and law, debris removal, and code-upgrade components, all of which can narrow or widen the gap between a weak claim and an adequate one, as discussed in the Texas Department of Insurance article on replacement cost or actual cash value policies.

For Oregon and Washington owners, that means you shouldn't ask only, “Is this ACV or RCV?” Ask these too:

- Does the policy address matching?

- Is there ordinance-and-law coverage for code-triggered work?

- Are debris removal costs carved out or limited?

- Will code upgrades be funded separately or pushed back on?

Why ACV is dangerous for businesses and nonprofits

A homeowner can sometimes delay a project. A business often can't. A nonprofit often shouldn't.

If a commercial roof, kitchen, classroom, worship space, medical suite, or mission-critical equipment is damaged, an ACV payment can create a brutal cash-flow problem. The organization still has to reopen, serve clients, protect staff, satisfy tenants, or continue operations while paying emergency vendors and replacement contractors.

That's where the two-check dynamic becomes more than an annoyance. It becomes a funding obstacle.

A practical first step for Oregon owners is verifying property records and building details before arguing scope and valuation. The Portland property assessor database can help confirm baseline property information that sometimes becomes relevant when the insurer disputes size, use, or building characteristics.

Local advice that saves trouble

For Oregon and Washington claims, don't let the insurer frame the dispute as only a depreciation issue. It may be a scope issue, a matching issue, or a code issue wearing a depreciation label.

How to Maximize Your Insurance Settlement

In this scenario, policyholders either protect the claim or give money away.

The insurer's estimate is not sacred. Their depreciation table is not automatically right. Their first payment is not automatically the full amount owed. If you want the strongest outcome, you need to work the file like someone whose money is at stake, because it is.

Start with the paper trail

Homeowners often focus on cleanup first and paperwork second. That's understandable, but it's risky.

Do this before things disappear:

- Photograph every damaged area: Wide shots first, then close-ups, then room-by-room and item-by-item.

- Keep every estimate and invoice: Mitigation invoices, emergency service bills, contractor proposals, and materials quotes all matter.

- Save replacement evidence: Receipts, order confirmations, delivery records, and proof of payment support recoverable depreciation requests.

Attack depreciation, scope, and omissions

HomeFirst notes a critical point about replacement-cost claims: insurers often pay ACV first and reimburse recoverable depreciation only after repair or replacement is completed and documented, and if the insured doesn't satisfy those conditions, the claim can function like an ACV policy in practice, as explained in HomeFirst's article on replacement cost versus actual cash value.

That means three areas deserve immediate scrutiny:

Depreciation methodology

Ask how the insurer calculated depreciation on each major line item. Roof, flooring, cabinets, contents, and trim should not be treated as if they all age the same way.Scope of repair

If the estimate undercounts demolition, painting, detach and reset work, finish carpentry, code-related steps, or overhead and profit where appropriate, your claim gets squeezed before depreciation even enters the conversation.Held-back funds

Identify every dollar the insurer labeled as recoverable depreciation. Track what has to be submitted to trigger payment and when.

The policy may say replacement cost. Your file still has to earn the second check.

Use a practical claim checklist

- Read the loss settlement clause: Don't rely on the declarations page alone.

- Request the detailed estimate: You want line items, not a summary.

- Keep a communication log: Names, dates, promises, and follow-up deadlines matter.

- Compare contractor estimates to carrier scope: Differences reveal where the claim is underwritten too tightly.

- Push for supplements when needed: Additional damage often appears after demolition or drying.

- Review strategy help if the claim is stalling: This guide on how to maximize insurance claim payout gives a useful framework for evaluating next steps.

My direct advice is simple. If the loss is substantial, don't handle it casually. A serious property claim is a financial negotiation wrapped in policy language.

Frequently Asked Questions About Property Claims

Can I keep the insurance money and not do the repairs

Sometimes, but it depends on the policy, the property, and whether a lender has rights in the proceeds. If your claim involves replacement cost benefits, failing to repair or replace can stop you from collecting the held-back depreciation. In practice, that can turn a promising RCV claim into an ACV-level recovery.

Is ACV used for both the building and my personal property

It can be. Some policies insure the dwelling on a replacement-cost basis but value contents at actual cash value unless you bought an upgrade. Don't assume your structure and belongings are treated the same. Read each coverage part separately.

What if repair costs exceed my policy limit

Then the policy limit becomes a major issue, even if the loss is otherwise covered. Replacement cost coverage is not unlimited by default. If limits are too low, the policy can still underperform badly.

Can I upgrade during repairs and use insurance money for that

You can often choose better finishes or upgraded materials, but the insurer usually owes only what the policy covers for like kind and quality. If you upgrade, expect to pay the difference yourself unless a specific policy provision supports more.

Do I need to fight the insurer alone

No. You can get professional claim representation. If you're not sure who does what, this explanation of a public adjuster vs insurance adjuster helps clarify the difference.

What's the biggest mistake after an RCV loss

Treating the first check as the end of the claim. On a two-check file, the second payment often depends on receipts, deadlines, and strict compliance. Miss that process and you can leave real money behind.

If you're dealing with a property loss in Oregon or Washington and you need someone to review the policy language, challenge depreciation, document the full scope, and push for every dollar owed, talk to NW Claims Management. They represent policyholders, not insurers, and they handle residential, commercial, and nonprofit claims with a clear focus on maximizing the settlement.