Claims adjuster training is your first step into a career where you become part financial detective, part crisis manager. At its heart, the job is about walking onto a property after a disaster—a house fire, a flooded storefront—and figuring out what it will take to make things right.

You're the one who has to assess the damage, dig deep into the insurance policy, and determine the fair and correct payout.

What a Claims Adjuster Actually Does

Picture this: you've just arrived at a home that’s been hit hard by a storm. There's obvious damage, of course, but your job goes much deeper. You need to uncover the full story, piece together the facts of the loss, and then translate all of that into a dollar amount based on the fine print of an insurance policy.

You are the crucial connection between a family or business owner who has just suffered a major loss and the financial protection they’ve been paying for. It's a role with real responsibility, and the demand for skilled adjusters is growing fast.

The claims adjusting sector is projected to hit $14.6 billion in 2025, which reflects a strong 9.6% annual growth rate over the last few years. If you're curious about the numbers, you can read the full market research report on Kentley Insights to see just how much opportunity is out there.

The Two Sides of the Claim

One of the first things you'll learn in any claims adjuster training is who you work for. This single distinction defines your entire career path, from your daily tasks to your ultimate loyalties. There are two main types of adjusters, and they operate on opposite sides of the table.

An adjuster’s allegiance is the most important factor in a claim. It determines their primary objective—whether it's to protect the insurance company’s bottom line or to advocate for the policyholder's maximum recovery.

Let's break down this crucial difference.

Staff Adjuster vs Public Adjuster At a Glance

The table below gives you a quick snapshot of the core differences between these two roles.

| Attribute | Staff Adjuster | Public Adjuster |

|---|---|---|

| Who They Work For | A specific insurance company (they are a direct employee). | The policyholder (the home or business owner who hired them). |

| Primary Objective | To investigate and settle the claim on behalf of the insurer, managing costs. | To advocate for the policyholder and maximize their financial recovery. |

| Compensation | Salary and benefits paid by the insurance company. | Typically a small percentage of the final claim settlement. |

As you can see, while the title "adjuster" is the same, the mission is completely different.

Here’s a closer look at what that means in practice:

- Staff Adjusters: These are the adjusters who work directly for an insurance company. When you file a claim, they are the ones sent out to investigate on their employer's behalf. Their job is to evaluate the damage and determine a settlement based on the company's interpretation of the policy.

- Public Adjusters: By contrast, public adjusters are independent professionals hired directly by the policyholder—the person or business that suffered the loss. They serve as the policyholder’s expert advocate, managing the claim from start to finish. Their sole focus is to ensure their client gets the full and fair settlement they're entitled to.

You can dive deeper into this topic in our guide on the differences between a public adjuster vs an insurance adjuster.

Deciding which path to take is one of the first big choices you'll make. Both roles demand sharp analytical skills and a solid grasp of insurance policy, but their day-to-day work and ultimate goals couldn't be more different.

Getting Your Adjuster License in Oregon and Washington

Before you ever set foot on a client's property to assess damage, you need a license. This isn't just a piece of paper; it's your official key to the profession. Think of it as a passport—without it, you simply can’t work as a claims adjuster. It’s the first, most critical step in your career.

And what a career to be stepping into. The insurance claims industry is growing at a staggering pace, with projections showing a $155.1 billion expansion between 2024 and 2029. North America is the largest market, which means the demand for sharp, licensed adjusters right here in Oregon and Washington is only going to climb. You can get a closer look at the numbers in Technavio's market analysis.

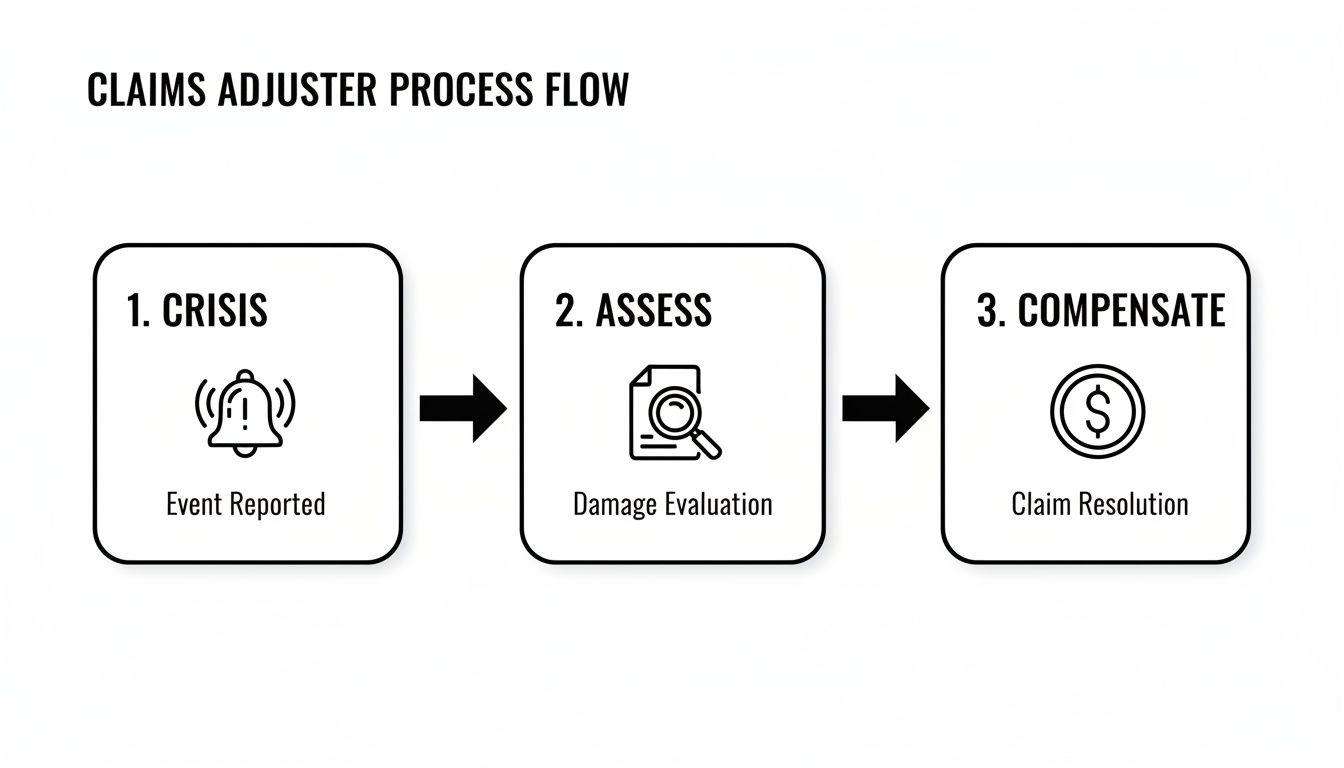

This process boils down to three core functions: responding to a crisis, assessing the situation, and getting the policyholder compensated.

Your license is what gives you the legal authority to perform every single one of those steps. It’s what empowers you to investigate, evaluate, and ultimately, help people get back on their feet.

Your Licensing Roadmap in Oregon

For anyone looking to become an adjuster in Oregon, the Division of Financial Regulation (DFR) has laid out a clear path. You’ll need to follow these steps in order.

- Complete Pre-Licensing Education: First, you have to enroll in and complete a state-approved 20-hour pre-licensing course. This is your essential claims adjuster training, covering the fundamentals of insurance and professional ethics.

- Pass the State Exam: Once you’ve completed your coursework, you’ll sit for the Oregon adjuster licensing exam. It’s designed to test your understanding of state regulations, policies, and best practices for handling claims.

- Submit Your Application: After you pass the exam, you’ll submit your official license application through the National Insurance Producer Registry (NIPR), which is the standard online portal for the industry.

- Fingerprinting and Background Check: The final step is a criminal background check, which includes getting your fingerprints taken. This ensures every licensed adjuster meets the state's ethical requirements.

All in, you can expect the costs for the course, exam, and fees to be somewhere between $400 and $600. You can find all the necessary forms and detailed instructions over at the Oregon Division of Financial Regulation website.

Navigating the Licensing Process in Washington

Washington’s process, which is managed by the Office of the Insurance Commissioner (OIC), is similar to Oregon's but with a few key differences.

- No Pre-Licensing Mandate: Here’s the big one—Washington doesn't have a mandatory pre-licensing hour requirement. That said, walking into the state exam cold is a terrible idea. I strongly recommend taking a quality exam prep course to make sure you’re ready.

- State Exam: You must pass the Washington state adjuster exam. It focuses heavily on property and casualty insurance knowledge.

- Application and Background Check: Just like in Oregon, your application goes through the NIPR portal, and you’ll need to clear a background check.

The cost to get licensed in Washington is very similar to Oregon, usually running between $350 and $550, mostly depending on which exam prep materials you choose. For all the official details and application links, head to the Washington State Office of the Insurance Commissioner's licensing page.

A Note on Reciprocity: Once you have your license in your home state (what's known as a "designated home state" or DHS license), you can often get licensed in other states through reciprocity. This is a huge advantage, as it lets you work claims across state lines without having to take another exam, opening up a world of opportunity.

Why Compliance Is Non-Negotiable

Trying to work as an adjuster without a license isn't just a bad idea—it's illegal and comes with serious fines and penalties. Beyond that, holding a license is a promise. It tells clients, employers, and the public that you have met a high standard of competence and are committed to ethical conduct.

That standard includes having a solid command of the insurance policy, which is the rulebook for every claim you'll ever handle. If you want to get a head start on that, take a look at our guide on how to understand insurance policy limits. Your license is the proof that you’re qualified to interpret these complex documents and help deliver a fair outcome.

Choosing Your Claims Adjuster Training Path

There’s no single "right way" to become a claims adjuster. Think of it less like a straight highway and more like a trail system with a few different routes leading to the same great view. The best path for you really comes down to how you learn, what your background looks like, and where you want to take your career.

Fundamentally, you're choosing between two main approaches: a formal, structured course or a hands-on apprenticeship. It’s a bit like learning a skilled trade. You can go to a technical college to learn all the theory and principles first, or you can start working alongside a master craftsman and learn on the job. Both can make you a pro; they just get you there differently.

The Structured Course Path

For most people just starting out, the journey begins with claims adjuster training in a more formal setting, like a pre-licensing or exam prep course. These programs are laser-focused on one thing: giving you the core knowledge you need to pass your state’s licensing exam. That means diving deep into insurance principles, the fine print of policy language, and all the relevant state regulations.

This is the fast track to getting licensed. As you look at different providers, it's helpful to understand the various templates for training programs to see which one aligns with your learning style.

- Online Training: This route offers incredible flexibility. You can study at your own pace from just about anywhere, which is a huge advantage if you’re trying to fit this around a current job or family life.

- In-Person Training: Nothing beats a real classroom for some people. You get direct interaction with instructors and can build connections with other aspiring adjusters. The live discussion is perfect for those who learn best by talking things through.

The main goal of a structured course is to give you the "book smarts" to ace the exam. It provides the essential vocabulary and rules of the game. The real-world application, however, usually comes next.

The Apprenticeship and On-the-Job Path

The other major route is learning by doing. This usually means starting as a trainee or an apprentice at an independent adjusting firm or a large insurance carrier. This path is all about practical, in-the-field education rather than classroom lectures. You'll learn by shadowing a seasoned adjuster, helping out on actual claims, and slowly being given more responsibility.

This is true trade-style learning. You won't just read a manual on how to inspect a fire-damaged home; you’ll be there with a mentor, smelling the smoke and seeing firsthand what to look for. It might take a bit longer to absorb all the theoretical knowledge needed for the exam, but the skills you build are instantly practical and deeply ingrained.

Specialized and Software Certifications

Getting your license is just the beginning. To really build a successful and rewarding career, you’ll want to add some specialized training to your resume. Think of your license as a general driver's license, and these certifications as endorsements for driving a big rig or a bus.

Key Certifications to Consider:

- Xactimate Training: This is non-negotiable. Xactimate is the industry-standard software for estimating repair costs, and knowing it inside and out is often a job requirement. Learning it isn't just about software; it’s about learning the logic of how to scope and price a loss.

- Property Damage Certifications: Courses in specific niches like residential construction, commercial property, or water mitigation (IICRC WRT, for example) make you a much more valuable expert. Our team’s deep knowledge in property damage assessment is what allows us to handle complex claims with confidence.

- Earthquake or Flood Certifications: If you work in the Pacific Northwest, being certified for specific perils like earthquakes or floods isn't just a bonus—it makes you an indispensable resource for carriers and policyholders.

In the end, the most successful adjusters I know have done a bit of everything. They often start with a formal course to get licensed quickly, then find a great mentor to gain on-the-job experience, all while continuing to earn certifications that make them true specialists in their field.

Your First Two Years: A Career and Learning Timeline

Becoming a claims adjuster isn’t just about passing an exam; it’s a commitment to constant learning. The journey from a newly licensed trainee to a seasoned pro who can confidently manage a complex claim is marked by distinct phases. Here’s a realistic look at what you can expect as you build your skills from the ground up.

Think of your first couple of years like a medical residency. You’ve got the textbook knowledge, but now it’s time to apply it in the real world, where things get messy and unpredictable. Your initial claims adjuster training is just the beginning of this intense, hands-on development.

The First Six Months: Licensing and Laying the Groundwork

This initial stage is an all-out sprint to get licensed and absorb the absolute fundamentals. This is where the bedrock of your entire career is formed.

- Months 1-3 (The Sprint to Get Licensed): Your one and only mission is to complete your pre-licensing course and pass that state exam. This period is a deep dive into insurance policies, state-specific regulations, and the core principles of handling a claim. Passing the exam is the key that opens every other door.

- Months 4-6 (First Steps in the Field): With your new license, you'll almost certainly start as a trainee under the wing of a senior adjuster. You’ll be a sponge—riding along on property inspections, listening in on difficult phone calls, and learning the company’s specific software and procedures. Your job is to watch, listen, and soak up the "why" behind every decision.

This is where the theory you learned crashes into the messy, human reality of property loss. You’ll quickly see the huge difference between reading about a claim in a textbook and standing in a water-damaged living room with a distressed homeowner.

Months Seven to Eighteen: Earning Your Independence

Once you’ve got the basics down, you’ll start taking on your own claims, but with a strong safety net. You’ll begin with a small, manageable caseload of less complicated files, which allows you to build confidence and hone your process without feeling overwhelmed.

This is a massive growth spurt. You'll be writing your first real estimates, communicating directly with policyholders, and learning the delicate art of negotiation. You will make mistakes—everyone does. A good manager or mentor will use these moments as powerful teaching opportunities. For those drawn to public adjusting, this is when you truly start to understand what it means to be the policyholder’s fiercest advocate. If you're weighing that career path, you can learn more about what a public adjuster does in our detailed guide.

The End of Year Two: Becoming a Pro

By the time you hit the two-year mark, you should be handling a full caseload of moderately complex claims with confidence and minimal supervision. You’ll have your own rhythm and workflow for managing a file from the first call to the final payment.

This is the point where you truly start to feel like an adjuster. You'll know how to dissect a policy, scope a loss accurately, write a clean estimate, and negotiate a fair settlement. This is also when you might look into specialized certifications to deepen your expertise, increase your earning potential, and become even more valuable in an industry where skilled professionals are always in demand. In fact, claims adjusters and related roles make up a substantial 16% of the insurance workforce.

Below is a table that breaks down what these milestones look like during your first year.

First-Year Milestones for a New Claims Adjuster

This table outlines the key learning objectives and professional goals that will shape your first year in the field, turning you from a trainee into a capable adjuster.

| Timeframe | Key Milestone | Primary Skills Gained |

|---|---|---|

| Months 1–3 | Pass the State Licensing Exam | Foundational knowledge of insurance principles, policy types, and state-specific laws and ethics. |

| Months 4–6 | Complete Initial Shadowing/Trainee Program | Understanding company procedures, claims software, initial damage assessment, and professional communication. |

| Months 7–9 | Handle First Solo Claims (Low Complexity) | Basic scoping and estimating, client interaction, file documentation, and time management. |

| Months 10–12 | Manage a Small, Independent Caseload | Increased autonomy, proficiency in estimation software, basic negotiation skills, and closing out simple claims. |

By the end of that first year, you'll have moved from pure theory to practical application, setting a strong foundation for a long and successful career.

What Does It Cost to Become an Adjuster? A Look at the Investment and Return

Thinking about a career as a claims adjuster isn't just a career change—it's an investment in your future. And like any good investment, you have to consider the upfront costs against the potential payoff. So, let's talk dollars and cents.

Think of your claims adjuster training as the seed money for a new venture. It’s what you need to put in to get the doors open and start earning.

Breaking Down the Upfront Costs

The total bill to get licensed and ready for the field can fluctuate, but here’s a realistic breakdown for anyone starting out in Oregon or Washington.

- Pre-Licensing Courses: This is usually the biggest single expense, running anywhere from $200 to $500. The price difference often comes down to a basic online course versus a more complete package with practice exams and instructor support.

- State Exam and Licensing Fees: Set aside about $100 to $150. This covers the fee to sit for the state exam, the actual license application, and any processing charges.

- Fingerprinting and Background Check: States mandate this to protect consumers. It’s a standard step that typically costs between $50 and $75.

- Essential Software Training: You simply have to know how to use Xactimate, the industry-standard software for writing estimates. A solid foundational course will likely cost between $300 and $600.

Realistically, you should budget between $650 and $1,325 to get fully licensed and trained on the core software. This initial investment is your ticket to a career with serious earning potential.

Calculating Your Potential Return on Investment

Now for the exciting part: the return. A career in claims adjusting, especially on the public adjuster side, offers a clear path to a solid income that grows as your skills sharpen.

Most new staff or independent adjusters can expect a starting salary in the $50,000 to $65,000 range. But that's just the starting line. Once you have a few years of experience and build a reputation for thorough, accurate work, salaries can easily jump to $75,000 to $90,000 and beyond.

Public adjusters, on the other hand, work on a different model. Their pay is typically a contingency fee—a small, agreed-upon percentage of the final claim settlement they secure for a policyholder. This creates a powerful win-win situation; the better the outcome for their client, the better they do. While income can vary from month to month, successful public adjusters who consistently deliver great results often earn well into the six figures. You can get a much deeper explanation by reading about how the cost of a public adjuster works in our detailed guide.

When you look at the numbers, the investment in your training pays for itself incredibly fast. By your first anniversary in the field, you will have almost certainly earned back your initial costs many times over, making it one of the smartest financial decisions you can make for your career.

Growing Beyond Your Initial License

Think of your claims adjuster license not as the finish line, but as the ticket that gets you into the game. The real work, and the real career-building, starts now. The insurance world is constantly shifting—policies get updated, new technologies change how we work, and even building codes evolve. The adjusters who not only survive but thrive are the ones who never stop learning.

Your initial claims adjuster training got you through the exam. Your ongoing education is what will make you a pro.

This commitment to growth starts with something every licensed adjuster knows well: Continuing Education, or CE. Both Oregon and Washington mandate that adjusters complete a certain number of CE hours to keep their licenses active. It’s the industry’s way of making sure we all stay sharp and up-to-date.

Meeting Your CE Requirements

The specific rules can shift over time, but the fundamental requirement doesn't. You have to complete state-approved courses to renew your license every couple of years. It's non-negotiable.

- For Oregon Adjusters: You’ll need to complete 24 hours of continuing education for every two-year renewal period. At least three of those hours have to be in professional ethics.

- For Washington Adjusters: The requirement is identical—24 CE hours per renewal cycle, which must also include three hours of ethics training.

You can knock out these hours through all sorts of approved courses, webinars, and workshops. The topics range from advanced policy interpretation to specialized skills for things like flood or earthquake claims. A word of caution: don't let this slide. If you miss your deadline, your license goes inactive, and your career grinds to a halt until you get it sorted out.

Moving Beyond the Minimums to True Expertise

Checking the box on your CE requirements keeps you employed. But if you want to become a top-tier adjuster—the kind that gets the complex claims and earns a top-tier income—you have to go beyond the basics. This is where you start pursuing advanced designations and real expertise.

“Working hard for something we don’t care about is called stress. Working hard for something we love is called passion.” —Simon Sinek

For adjusters who are genuinely passionate about this work, advanced training isn’t a chore. It’s an opportunity to master the craft and make a bigger difference. This is where you move from just following the rules to understanding the why behind them.

One of the most respected paths is earning the Chartered Property Casualty Underwriter (CPCU) designation. Think of the CPCU as the master’s degree of the insurance world. It’s a serious commitment, but it signals to everyone—employers, attorneys, and policyholders—that you possess a deep and comprehensive understanding of risk, policy, and insurance operations.

But the CPCU isn't the only way to level up. Other incredibly valuable areas for advanced training include:

- Negotiation and Communication: We might call them "soft skills," but they are arguably an adjuster's most powerful tools. Taking advanced workshops on managing difficult conversations and de-escalating conflict will directly translate to better outcomes on your claims.

- Specialized Certifications: Do you want to be the go-to expert for a certain type of claim? Get certified. Designations in commercial property, agricultural claims, or advanced Xactimate proficiency can make you indispensable.

- Appraisal and Umpire Training: Many seasoned adjusters eventually find a new calling in dispute resolution. As an appraiser or umpire, your expertise is used to settle disagreements over value, a critical role that requires years of accumulated knowledge.

At the end of the day, the best adjusters I know all share one trait: they understand their license was just permission to start learning. The real rewards come from a relentless drive to know more and do better.

Your Top Questions About Claims Adjuster Training, Answered

As you get closer to starting a new career, the questions tend to pile up. It's completely normal. Let's tackle some of the most common ones we hear from people just like you, so you can move forward with a clear head.

How Long Does It Take to Get Licensed?

This is usually the first thing people ask. While everyone moves at their own pace, a focused person can realistically get through the required pre-licensing material and pass the state exam in about two to four months.

Once you pass the exam, you're not quite done. You have to submit your application and wait for the state to process it, which can add another four to eight weeks. So, all in, you should plan for a total of three to six months from the day you start studying to the day you have that official license in your hands.

Can I Become an Adjuster Without a College Degree?

Yes, absolutely. To become a licensed claims adjuster in Oregon or Washington, you don't need a four-year degree. A high school diploma or a GED is the only educational requirement to take the exam and get your license.

That said, your background can give you a huge leg up. If you have experience in fields like construction, finance, or even law enforcement, you'll find those skills are incredibly useful. What employers really want are people with sharp problem-solving skills, the ability to communicate clearly, and a knack for negotiation—things you learn in the real world, not just a classroom.

What Is the Hardest Part of Claims Adjuster Training?

For most newcomers, the biggest challenge is getting fluent in "insurance policy." These documents are packed with dense, technical language. Learning to read them correctly—to truly understand what every exclusion, condition, and endorsement means—is like learning a new language. It takes serious focus.

The second major hurdle is bridging the gap between theory and practice. It’s one thing to read about a complex loss, but it's another to write a perfect damage estimate, document the scene accurately, and confidently negotiate with an experienced company adjuster. Those are skills you only sharpen through hands-on practice and good mentorship.

What Is the Difference Between an Independent and Public Adjuster?

Understanding this is fundamental because it defines who you work for. The entire job changes based on your answer. The key difference comes down to one thing: who they represent.

- An independent adjuster works for the insurance company. They're typically contractors brought in by an insurer to handle a surge of claims, often after a major storm. Their loyalty and professional duty are to the insurance carrier that hired them.

- A public adjuster works for the policyholder. They are hired directly by the home or business owner who has suffered the damage. Their only job is to advocate for their client and manage the entire claim to ensure their client’s interests are protected.

Choosing a path means deciding whether you want to work on behalf of the insurance company or on behalf of the public.

If you've suffered property damage and feel overwhelmed by the insurance process, you don't have to face it alone. The licensed public adjusters at NW Claims Management are here to advocate for you. We manage every detail of your claim to ensure you receive the full and fair settlement you deserve. Contact us today for a free claim evaluation.