Most advice about insurance trainee positions starts in the wrong place. It assumes the only smart path is to join a carrier, learn the systems, and work your way up inside a large insurance organization.

That’s incomplete advice.

A better first question is this: Do you want to work for the insurer, or for the policyholder? Those are not the same job, even when the word “adjuster” appears in both titles. One path teaches you how companies evaluate risk, process claims, and protect their books. The other teaches you how to read policy language from the claimant’s side, document losses thoroughly, and push for a fair settlement when a property owner is overwhelmed.

If you're new to the field, that distinction matters more than job title, salary band, or whether the role sounds prestigious on LinkedIn.

The Untapped Opportunity in Insurance Careers

Insurance isn't a niche industry. It is one of the largest employment ecosystems in the country, and it's changing hands in real time. The U.S. insurance industry employs approximately 3 million workers, with over 400,000 professionals projected to retire in the coming years, and less than 25% of the workforce under 35, according to the Insurance Information Institute career and employment data.

That creates an opening most newcomers still underestimate.

The usual conversation focuses on stable jobs, benefits, and promotion ladders. Those matter. But the deeper opportunity is that an aging workforce leaves behind practical knowledge that firms urgently need to replace. Trainees who can learn policy language, communicate clearly, and handle tense conversations are entering at a moment when the industry has to build its next generation.

The overlooked fork in the road

Information often highlights insurer-side jobs, such as underwriting, claims handling, and agency sales. There is often insufficient information about public adjusting, where the adjuster represents the policyholder instead of the insurance company.

That difference changes the daily work. In a public-adjusting track, you're not trying to close a file efficiently for the carrier. You're trying to understand the loss, support the insured, and build the strongest defensible claim package possible. If you want to understand the homeowner experience before choosing your lane, review a plain-English breakdown of the home insurance claim process. It makes the pressure points obvious.

Insurance has room for analytical people, sales-minded people, and service-driven people. Public adjusting is one of the few paths that combines all three.

Why this path appeals to the right kind of trainee

Public adjusting isn't the easiest entry point. That's part of its appeal.

It asks more of you than memorizing product lines or following a call center script. You need patience, documentation habits, negotiation discipline, and the ability to explain a technical issue to someone who's tired, stressed, or angry. But if that fits your temperament, insurance trainee positions on the policyholder side can become very rewarding work.

A newcomer who understands this early avoids a common mistake. They don't just chase the first opening with “insurance” in the title. They choose the side of the table where they want to build a career.

Decoding the Different Types of Insurance Trainee Roles

Before you apply anywhere, sort the field into two broad camps. There are carrier-side roles, where you work for the insurer, and policyholder-side roles, where you advocate for the insured. Both can be good careers. They train different instincts.

The traditional carrier-side tracks

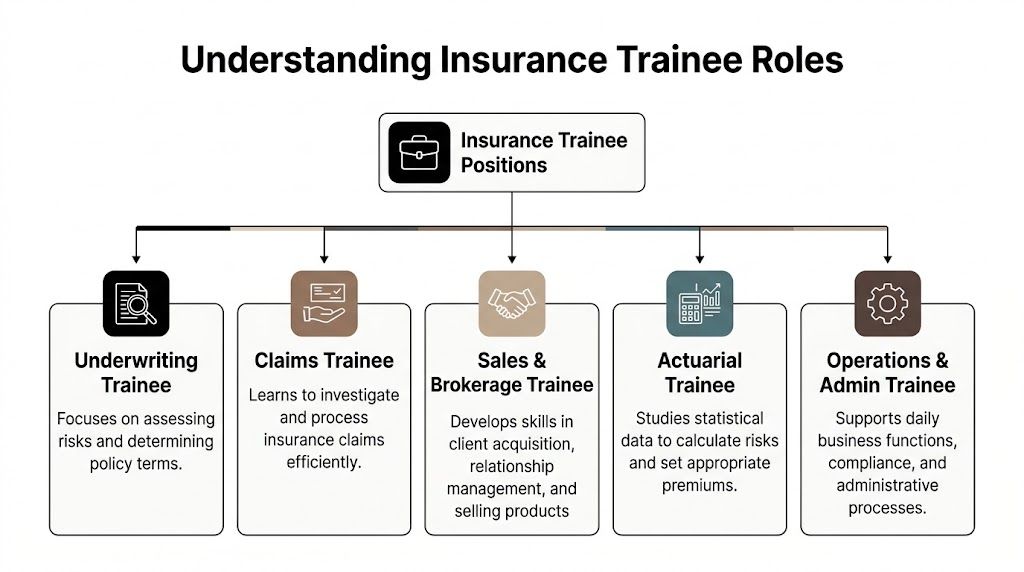

The most visible insurance trainee positions sit inside carriers, brokerages, and agencies.

Here’s the practical breakdown:

| Role | What you actually do | Best fit for | Training reality |

|---|---|---|---|

| Underwriting trainee | Review submissions, assess risk, interpret guidelines, support pricing and policy decisions | Analytical, detail-heavy thinkers | Classroom learning plus close file review |

| Claims trainee | Investigate losses, review documentation, communicate with insureds and vendors, apply policy terms | Calm communicators who can make decisions | Heavy process training and supervised claim handling |

| Sales or brokerage trainee | Prospect, build relationships, explain coverage, generate and retain business | Competitive people who don't mind rejection | Product training, sales scripts, and field coaching |

| Operations trainee | Support policy processing, compliance, service workflows, renewals, and documentation | Organized people who like structure | System training and accuracy-driven work |

| Actuarial trainee | Work with models, risk assumptions, and pricing data | Math-focused candidates | Formal technical training and exams |

The best-known compensation figures in entry-level discussions tend to come from the sales and underwriting side. Insurance sales agent trainees earn a median annual wage of $60,370, and underwriters earn $79,880, according to the Bureau of Labor Statistics occupational outlook for insurance sales agents. Those roles often begin with a high school diploma or bachelor's degree, followed by on-the-job training.

What those jobs teach you

Carrier-side training is useful because it builds discipline. You learn systems, file handling, policy interpretation, documentation standards, and how insurance organizations make decisions at scale.

If you want structured learning support, formal coursework can help you fill gaps before day one. A resource like Insurance Institute eLearning is useful for understanding how insurance education is delivered and how professional study fits into a broader career path.

But don't romanticize these roles. Underwriting can feel repetitive if you want more human interaction. Sales can be punishing if you dislike prospecting. Claims work can harden people if they never develop a strong service mindset.

The policyholder advocacy track

A public adjuster trainee learns the same insurance language from the opposite direction. Instead of protecting the insurer’s position, you help the insured present, document, and negotiate a claim.

That often includes:

- Loss documentation: Organizing photos, repair records, estimates, inventories, and scope details.

- Policy review: Reading coverage, exclusions, duties after loss, and valuation provisions carefully.

- Client communication: Translating technical claim language into plain English.

- Negotiation support: Assisting with the back-and-forth that shapes the final settlement.

If you're still fuzzy on how this differs from staff or independent adjusting, read this side-by-side explanation of a public adjuster vs insurance adjuster.

Practical rule: If you like process more than people, start on the carrier side. If you like process and people, and you don’t mind conflict when the facts support your position, public adjusting may suit you better.

How to choose your lane

Use personality, not prestige, as your filter.

Choose underwriting if you enjoy pattern recognition, careful review, and measured decision-making. Choose sales if you’re energized by outreach and can recover quickly from a “no.” Choose claims if you can stay composed while balancing empathy and policy language. Choose public adjusting if you want claim work with a clear advocacy mission.

That last path remains the least discussed, which is exactly why serious newcomers should pay attention.

Crafting Your Resume and Cover Letter to Get Noticed

Most insurance applications fail for a simple reason. The candidate sends the same resume to every role.

That doesn't work here because insurance trainee positions are not interchangeable. An underwriting trainee resume should sound different from a claims trainee resume. A public adjuster trainee application should sound different from both.

Match your language to the job

Hiring managers scan for fit fast. They want evidence that you understand the work, even if you haven't held the title before.

Use language like this based on the role:

- For underwriting trainee roles: risk analysis, policy review, data integrity, coverage evaluation, documentation accuracy, decision support

- For claims trainee roles: investigation support, loss review, file management, empathetic communication, fact gathering, resolution follow-through

- For sales or brokerage trainee roles: client acquisition, relationship management, needs analysis, pipeline discipline, renewal support

- For public adjuster trainee roles: client advocacy, loss documentation, negotiation support, property damage review, policy interpretation, stakeholder communication

If you're early in your career, structure matters just as much as wording. This guide on Crafting Your Resume for Recent Grad Success is helpful because it shows how to present transferable experience without sounding inflated.

Translate non-insurance experience properly

Retail, hospitality, banking, construction support, admin work, and customer service can all transfer into insurance. The key is translation.

Don't write:

- Helped customers with issues

- Managed paperwork

- Worked in a busy environment

Write:

- Resolved time-sensitive customer concerns while maintaining documentation accuracy

- Reviewed records for completeness and escalated discrepancies

- Communicated policy or service information clearly to stressed customers

- Coordinated across teams to move cases from intake to resolution

For a policyholder-side role, familiarity with how losses are documented is a plus. Reviewing examples of property damage assessment can help you understand the vocabulary employers expect around scope, evidence, and valuation.

A cover letter opening that works

Your opening paragraph shouldn't repeat your resume. It should explain why this side of insurance fits you.

I’m applying for this trainee role because I’m at my best when the work requires precision, calm communication, and follow-through for people dealing with stressful situations. In my prior customer-facing roles, I learned how to gather facts carefully, explain next steps clearly, and keep clients engaged through a process they didn’t fully understand. That combination is why insurance, and specifically claim-related work, stands out as the right career path for me.

What strong applications do differently

A useful application usually does three things well:

- It names the function clearly. The employer shouldn't have to guess whether you're applying for underwriting, claims, sales, or public adjusting.

- It mirrors the job language. Use their terminology when it fits your real experience.

- It shows judgment. Insurance is full of detail. Sloppy formatting, vague bullets, and generic enthusiasm hurt you fast.

A resume gets attention when it sounds like someone who already understands the work, even if they're still entering it.

Finding and Securing Your First Trainee Opportunity

If you rely only on major job boards, you'll see a distorted version of the market.

A search for entry-level insurance jobs in a major market like Denver yields 354 results, almost all for sales or insurer-side roles, with virtually no public-facing listings for public adjusting trainee positions, according to this Indeed search snapshot for entry-level insurance jobs. That's the key lesson, not the city. Public-adjusting opportunities often exist outside the normal posting channels.

Why the hidden market matters

Carrier roles are easy to find because large employers have formal recruiting pipelines. Public adjusting firms are often smaller, regional, and selective. They may hire when they find the right person, not only when a requisition goes live.

That means the strongest candidate doesn't just search. They identify firms, study their service area, and make a professional approach.

Most public-adjusting opportunities are found through direct outreach, local reputation, and timing. That's frustrating for passive applicants and useful for proactive ones.

A smarter search strategy

Use a layered approach instead of a single platform.

Start with these channels:

- Company websites: Look for firms that focus on property claims, business interruption, fire losses, storm damage, or large-loss advocacy.

- LinkedIn: Follow principals, senior adjusters, and operations leaders. Watch what kinds of claims they discuss.

- State directories and licensing resources: These help you verify who is operating legitimately in your state.

- Local networking: Restoration contractors, mitigation companies, policyholder attorneys, and insurance educators often know which firms train carefully.

Then do what most applicants won't do. Send a short, serious message introducing yourself, asking whether the firm ever brings on trainees, and showing that you understand their side of the business.

What to say when no opening is posted

A good outreach note is direct and restrained.

Try this structure:

- Who you are: Your current role or background

- Why this niche: A sentence on why public adjusting interests you specifically

- What you bring: Documentation skills, client communication, construction familiarity, claim curiosity, or negotiation temperament

- What you want: A conversation, not a demand for a job

Example:

I’m exploring a long-term career in property claims and I’m especially interested in policyholder advocacy work. My background includes client communication and detail-heavy documentation, and I’m looking for a firm where I can learn claim preparation the right way. If your team ever considers trainee or assistant-level hires, I’d value the chance to introduce myself.

Licensing and geography aren't side issues

For public adjusting, state rules matter. Oregon and Washington have their own licensing expectations, and a serious applicant should learn those early. Even before you're fully licensed, understanding the path signals maturity. It tells a firm you're not treating this like a casual sales job.

Don't wait until an interview to learn basic licensing vocabulary. Know the difference between trainee readiness, exam requirements, background checks, and continuing education expectations. In this niche, preparation itself is part of your credibility.

Mastering the Interview and Negotiating Your Offer

Insurance interviews reward candidates who can describe behavior, not just intentions. Saying you're organized or empathetic doesn't move the conversation. Giving a tight example does.

That’s why strong firms use STAR-method interviews to assess behavioral fit, and some agencies track outcomes against clear post-training benchmarks, including a 30% policy close uplift after training, as noted in this discussion of training and turnover reduction in insurance hiring. Even if you're not applying to a sales role, that tells you what hiring managers value. They want examples tied to results and coachability.

Use STAR without sounding rehearsed

STAR means Situation, Task, Action, Result. Keep each answer compact.

Here’s an example for a claims-oriented or public-adjusting trainee interview:

- Situation: A customer was upset because a service issue had delayed resolution.

- Task: I needed to calm the conversation, identify the missing information, and move the case forward.

- Action: I listened without interrupting, summarized the issue back to them, checked the record for gaps, and coordinated with the next team to confirm timing and ownership.

- Result: The customer understood the process, the case moved forward cleanly, and the issue didn't escalate further.

That answer works because it shows judgment under pressure. Insurance employers care about that.

Questions you should expect

Prepare for questions like these:

- Tell me about a time you handled a frustrated customer

- Describe a situation where accuracy mattered

- How do you learn technical material

- Why insurance, and why this role

- How would you balance empathy with policy or process requirements

For public-adjusting roles, expect a sharper version of the last two. Employers want to know whether you can advocate firmly without becoming reckless or emotional.

Questions that make you look serious

Ask questions that reveal you care about training quality and standards.

Good examples:

- What does success look like in the first 90 days for a trainee here?

- How are files reviewed before a new trainee handles work more independently?

- Who provides day-to-day coaching?

- How do you teach policy interpretation and loss documentation?

- When clients are under stress, what communication style works best on your team?

If the role involves claim negotiation, reading about the mechanics of negotiating with an insurance company helps you ask sharper questions about authority, documentation, and escalation.

Ask about the training process before you ask about flexibility. Early-career candidates earn trust faster when they signal that learning the work matters more than perks.

Negotiating the offer

You don't need to negotiate aggressively. You do need to negotiate professionally.

Focus on the full package:

| Area | What to ask |

|---|---|

| Compensation | How is base pay structured, and are there review points during the training period? |

| Licensing support | Does the company pay for exam prep, applications, or continuing education? |

| Mentorship | Who trains new hires, and how often are performance reviews held? |

| Progression | What milestones move a trainee into a more independent role? |

A respectful script works well:

I’m very interested in the role. Before I accept, I’d like to understand how compensation develops during training, what support is provided for licensing or professional education, and how you measure progress in the first several months.

That approach sounds like someone building a career, not just taking a job.

Your First 90 Days From Onboarding to Success

A lot of new people fail in insurance because they assume effort alone is enough. It isn't. The field rewards structured learning, disciplined habits, and the willingness to absorb correction without taking it personally.

That matters because new insurance agent failure rates are estimated at 70% to 80% within three years, and trainees who engage in effective onboarding, AI-enhanced coaching simulations, and ongoing mentorship achieve core competencies 40% faster, according to this analysis of insurance agent success rates and training methods. Even if your role isn't pure sales, the lesson carries. Good onboarding changes outcomes.

Days 1 through 30

The first month is for learning the language and the workflow.

A smart trainee spends this phase doing four things well:

- Build a vocabulary notebook: Policy terms, coverage triggers, exclusions, endorsements, valuation language, and common claim documents

- Learn the file path: Intake, review, documentation, escalation, follow-up, closeout

- Find your internal translator: Every team has one person who explains complex issues clearly. Learn from that person.

- Watch how experienced people write: Insurance is written work. Emails, notes, summaries, and file comments matter.

If you're entering the property-claim side, map the sequence of a property damage claim process so the moving parts don't feel abstract.

Days 31 through 60

At this point, many trainees get wobbly. They know enough to feel confident, but not enough to see their mistakes coming.

Use this month to move from observation into controlled execution.

Take on small tasks independently. Draft summaries. Organize supporting documents. Sit in on difficult calls and write down what the senior person did to keep the conversation productive. When you're corrected, fix the issue once and build a personal checklist so it doesn't recur.

The fastest learners aren't the people who ask the most questions. They're the people who ask a good question once, write down the answer, and apply it the next three times.

A public-adjusting trainee should be especially careful here. Early overconfidence can damage a file. Strong advocates don't improvise facts, stretch coverage language, or promise outcomes. They document carefully and strengthen their position with evidence.

Days 61 through 90

The last part of the first quarter is where you start showing value instead of just absorbing instruction.

That doesn't mean acting like a veteran. It means becoming reliable.

Look for opportunities like these:

- Spot a recurring bottleneck: Maybe photos are being mislabeled, estimates are arriving incomplete, or follow-ups are not being calendared consistently.

- Improve your own documentation: Clear file notes save everyone time.

- Own a narrow piece of work fully: Not everything. One thing.

- Demonstrate composure: Clients and counterparties remember the person who stays steady.

Here’s a simple way to think about the full 90 days:

| Phase | Main objective | What success looks like |

|---|---|---|

| First 30 days | Learn terminology, systems, and standards | Fewer basic mistakes, stronger note-taking, better questions |

| Next 30 days | Apply learning under supervision | Cleaner work product, more confidence, fewer repeated corrections |

| Final 30 days | Contribute consistently | Trusted with defined tasks, visible reliability, stronger judgment |

What works and what doesn't

What works:

- Showing up prepared

- Taking notes

- Studying policy language even when it feels slow

- Asking for examples of good work product

- Accepting that precision beats speed early on

What doesn't:

- Talking like you already know the field

- Treating claim files casually

- Confusing empathy with agreeing to everything

- Waiting for someone to organize your development

- Assuming all insurance trainee positions teach the same habits

The newcomers who last are not always the loudest or the smoothest. They are usually the most teachable. In insurance, that trait compounds quickly.

If you’re dealing with a property loss in Oregon or Washington and want experienced help from a firm that advocates for policyholders, NW Claims Management can guide you through documentation, policy interpretation, and settlement negotiations. Their team works exclusively for insureds, not carriers, and helps residential, commercial, and nonprofit clients pursue fair claim outcomes.