The letter arrives after a fire, wind loss, plumbing break, or roof claim. You open it expecting help, and instead you get a denial, a partial denial, or a number that doesn't come close to what it will take to put the property back together. The language feels formal on purpose. The message underneath it is simple: accept this and move on.

That's the moment most policyholders lose ground.

Not because the insurer is always right, but because homeowners often answer the wrong way. They call in angry. They send a short email. They argue from frustration instead of from the policy, the facts, and the damage record. A strong rebuttal letter changes that dynamic. It puts your dispute into a format the carrier has to process, respond to, and defend.

A rebuttal letter template helps, but only if you use it as a framework and not as a script. The primary job is to build a record that makes it harder for the insurer to say no again without exposing gaps in its own position. In Oregon and Washington, that matters. Carriers know when a policyholder is venting, and they know when a policyholder is building a file that could later be reviewed by a supervisor, a regulator, an appraiser, or counsel.

You Received a Denial Now What?

The first thing to understand is that a denial letter isn't the end of the claim. It's the insurer's position at that moment, based on the information they chose to rely on or the way they chose to read the policy.

That distinction matters.

A homeowner in the Northwest often gets a letter that sounds more final than it really is. It may cite wear and tear after a windstorm, exclude water damage without explaining the cause analysis, or approve only part of the repair while ignoring what a contractor would need to do to return the property to pre-loss condition. The instinct is to argue every unfair thing at once. That usually weakens the response.

The better move is to treat the denial as the opening bid in a dispute. Your rebuttal letter is the first formal counter. If you're dealing with that situation now, this guide on how to fight an insurance claim denial gives useful background on the broader process.

The carrier wrote a conclusion. Your job is to answer it with a record.

A good rebuttal letter does three things at once. It identifies exactly what decision you dispute. It shows why that decision conflicts with the facts, the policy, or both. It signals that you're organized enough to keep escalating if the insurer keeps stalling.

That last part is psychological, and its importance is often underestimated. Claims departments see all kinds of responses. They see emotional messages, vague complaints, and unsupported demands every day. What gets attention is a letter that is calm, specific, and documented. Not dramatic. Not threatening. Just difficult to dismiss.

If your stomach dropped when you read the denial, that reaction is normal. But the next move needs to be controlled. You're no longer just reacting to bad news. You're building a rebuttal that puts the insurer on the defensive.

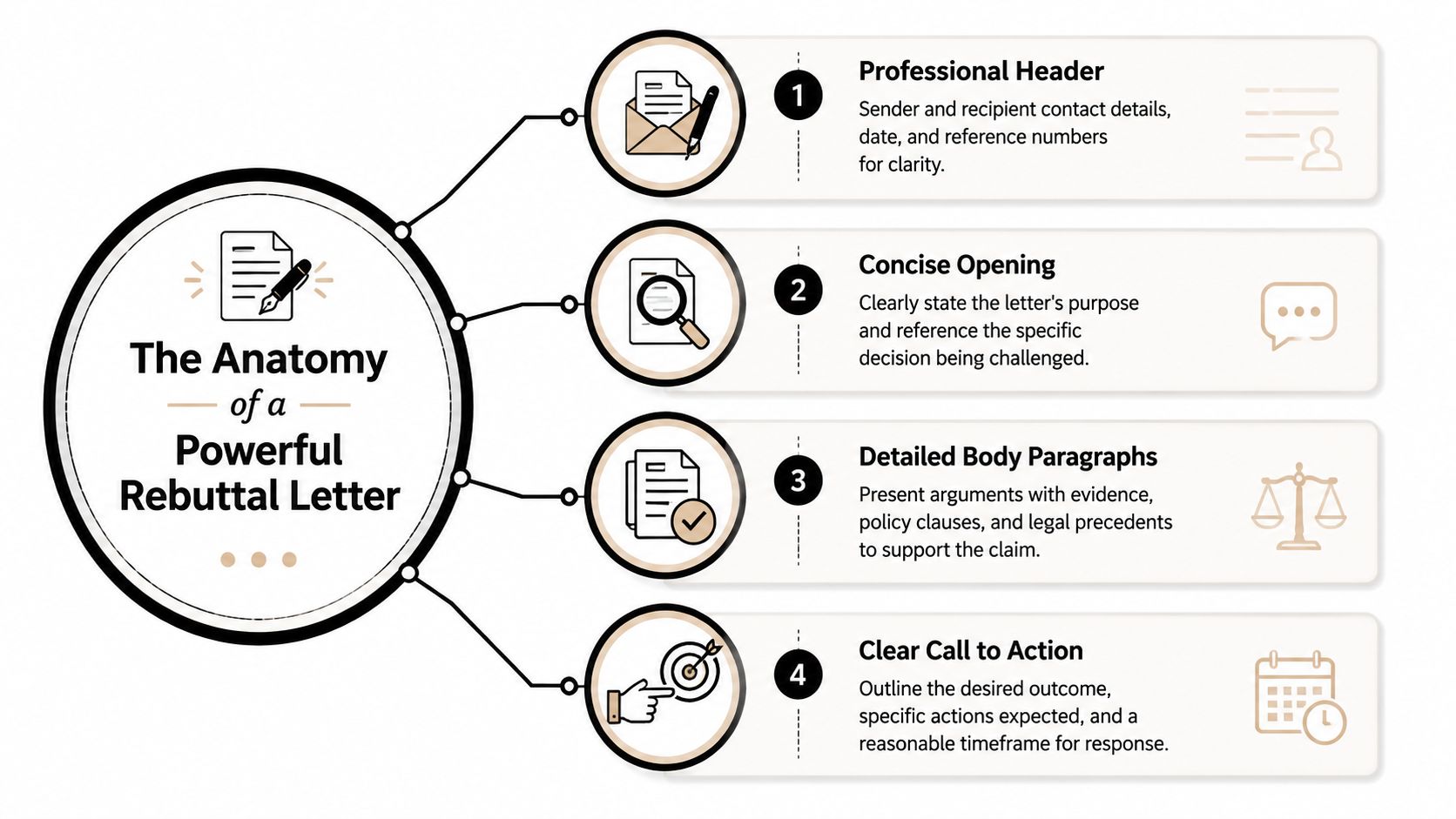

The Anatomy of a Powerful Rebuttal Letter

A rebuttal letter works best when it feels easy to review. That sounds almost too simple, but it's the difference between a claims examiner skimming past you and a supervisor seeing a real coverage or valuation problem.

Start with a clean header

Put your full name, property address, claim number, policy number, date of loss, and the name and address of the insurer or adjuster at the top. If you're sending it to more than one person, list them all.

This isn't busywork. It prevents the carrier from misrouting the letter or pretending it wasn't clear what claim you were addressing. In any property dispute, precision matters. That same principle comes up when people misunderstand what counts as compensable property damage under the legal definition of damage.

Open with a firm purpose statement

Your opening paragraph should do one job. It should state, plainly, that you dispute the denial, underpayment, or scope decision.

Use language like this:

I am writing to formally dispute your coverage decision dated [date] regarding claim number [number].

That sentence works because it's direct. It doesn't apologize. It doesn't ramble through the whole loss history. It tells the reader what this document is for.

If your writing tends to drift into legal-sounding clutter, it helps to review guidance on legal writing plain English. Insurance rebuttals are stronger when they're readable.

Build the body point by point

Most weak letters falter at this stage. Homeowners often write one long narrative. Insurers prefer that, because it lets them answer vaguely.

A stronger body mirrors the denial letter.

- Quote the insurer's reason: Pull the denial basis or valuation position directly from their letter.

- Answer that point only: Don't jump to three other complaints in the same paragraph.

- Tie your answer to proof: Contractor estimate, photos, moisture readings, engineer findings, invoices, code requirements, or policy language.

- Identify the missing step: Show what the insurer failed to inspect, failed to explain, or failed to include.

For example:

Your letter states that the interior water damage resulted from long-term seepage. The enclosed photographs, plumber findings, and mitigation records show a sudden plumbing failure on the reported date of loss.

That's stronger than saying the decision is unfair. “Unfair” is your opinion. “Your cause conclusion conflicts with the attached evidence” is an argument.

Close with a specific demand

The closing should tell the insurer what you want next.

Use one or more of these requests:

- Coverage reconsideration: Ask for a written reversal or revised coverage position.

- Reinspection: Request an additional site inspection with the appropriate expert.

- Revised estimate: Demand that omitted line items be evaluated and priced.

- Written explanation: If they maintain the denial, ask them to identify the exact policy language and factual basis supporting it.

Practical rule: Don't end your letter with “please help.” End it with a deadline-driven request for action.

A powerful rebuttal letter template isn't fancy. It's organized. It helps the insurer's reader see that every weak point in the denial has been matched with a factual response.

Rebuttal Letter Templates You Can Use Today

Templates are useful because they keep you from staring at a blank page. They're dangerous when people treat them like a fill-in-the-blank shortcut.

That's true in other dispute systems too. In credit card chargeback representments, rebuttal letters are expected to be concise and limited to no more than two pages, and the response has to be built around the actual dispute, not a stock form. Effective letters include core identifying details, the transaction facts, the argument against the stated reason, supporting evidence, and a formal request for reversal, while cookie-cutter letters are described as ineffective because each dispute requires its own factual case in Chargebacks911's chargeback rebuttal letter guidance.

The lesson carries over cleanly to property insurance. Start with a rebuttal letter template. Then customize it until it sounds like your claim, your loss, and your evidence.

Template for a policy exclusion denial

Use this when the insurer says the damage falls under wear and tear, repeated seepage, neglect, rot, faulty workmanship, or another exclusion.

[Your Name]

[Property Address]

[City, State, ZIP]

[Phone]

[Email][Date]

[Adjuster Name]

[Insurance Company]

[Address]Re: Formal Dispute of Denial

Claim Number: [Claim Number]

Policy Number: [Policy Number]

Date of Loss: [Date]Dear [Adjuster Name],

I am writing to formally dispute your denial of the above-referenced claim as stated in your letter dated [date]. Your decision appears to rely on the conclusion that the claimed damage falls within the policy exclusion for [stated exclusion].

I disagree with that conclusion because the facts of the loss do not match the exclusion cited. Specifically, [brief explanation of sudden event, damage progression, or cause].

The documents enclosed support this position, including [contractor report, plumber report, mitigation invoice, photographs, timeline, expert findings]. These materials show that [brief factual summary].

In addition, your denial letter does not fully address [specific missed issue, conflicting observation, or omitted damage area].

I request that you reopen and reconsider this claim, review the enclosed documentation, and provide a revised written coverage determination. If you maintain your denial, please identify the exact policy language and factual basis supporting that position as applied to the documented conditions at my property.

Sincerely,

[Your Name]

How a homeowner should fill it out

A weak version says, “This wasn't wear and tear because the roof was fine before.” That's too broad.

A stronger version says, “Your denial relies on a wear-and-tear exclusion, but the enclosed photos and contractor notes show lifted shingles and related interior staining after the reported wind event. The denial letter does not explain how those storm-related conditions were ruled out.”

That wording matters because it attacks the carrier's reasoning, not just the result.

Template for a lowball repair estimate

Use this when coverage is accepted, but the insurer's number won't restore the property.

[Your Name]

[Property Address]

[Contact Information][Date]

[Adjuster Name]

[Insurance Company]Re: Dispute of Claim Valuation

Claim Number: [Claim Number]Dear [Adjuster Name],

I am writing to dispute the current valuation of my property damage claim. Although coverage appears to have been accepted in part, the estimate provided does not reflect the full scope and reasonable cost of necessary repairs.

Your estimate omits or undervalues the following items: [list omitted rooms, line items, materials, code-related work, detach and reset work, matching issues, or labor components].

I have enclosed supporting documentation, including [independent contractor estimate, photographs, invoices, material specifications, code references, prior communications]. This documentation shows that the work required to restore the property involves more than the amount currently allowed.

I request that you review the enclosed estimate line by line, revise your scope and pricing accordingly, and issue supplemental payment for all covered repairs. If you disagree with any item, please provide a written explanation identifying each disputed line item and the basis for your position.

Sincerely,

[Your Name]

Annotated example

If the insurer only paid for painting one wall after a leak, don't write, “Your estimate is way too low.”

Write this instead:

- Name the omission: “Your estimate includes paint for the repaired wall only.”

- Tie it to actual repair conditions: “The attached contractor estimate includes prep, texture blending, primer, and paint to achieve a uniform finish across the continuous affected area.”

- Force a specific response: “If you contend those items are unnecessary, please state that position in writing and identify the basis for excluding them.”

That final sentence is strategic. It forces the insurer to either revise the estimate or commit to a narrow written position. Either outcome helps you.

For readers who want to compare how demand structures work in other legal disputes, these personal injury demand letter templates are useful as a contrast. Different claim type, same underlying lesson. Facts, causation, documentation, and a clear demand carry the argument.

Template for a scope of work dispute

This one is common in roof, siding, flooring, and water claims. The insurer agrees something was damaged but draws the repair line too tightly.

[Your Name]

[Property Address]

[Contact Information][Date]

[Adjuster Name]

[Insurance Company]Re: Dispute of Repair Scope

Claim Number: [Claim Number]Dear [Adjuster Name],

I am writing to dispute the current scope of repairs for my claim. Your estimate allows for [example: replacement of one roof slope, spot repair of flooring, partial cabinet work], but that scope does not reflect the actual work required to restore the property.

The enclosed documentation shows that the approved scope is incomplete for the following reasons:

- [Reason tied to matching, continuity, access, code, manufacturer requirements, or practical repair limitations]

- [Reason tied to damage spread or interconnected materials]

- [Reason tied to contractor or expert findings]

I request a revised scope of loss that addresses these conditions and provides for complete covered repair or replacement as supported by the enclosed materials. If you disagree, please provide a written explanation addressing each of the points above.

Sincerely,

[Your Name]

Where homeowners usually lose leverage

Scope disputes are where carriers often rely on fatigue. They know many policyholders will accept half a roof, partial flooring, or disconnected repairs because they don't know how to frame the problem.

Use these pressure points instead:

| Dispute issue | Better rebuttal angle |

|---|---|

| Partial roof replacement | Explain why the approved repair doesn't produce a functional, uniform repair based on contractor findings |

| Spot flooring repair | Show continuity problems, material availability issues, and affected adjoining areas |

| Limited drywall scope | Tie the repair to necessary texture, insulation access, drying cuts, and finish restoration |

| Cabinet or siding mismatch | Focus on restoration outcome, not preference |

A rebuttal letter template is a skeleton. The evidence and the wording are what make it walk.

If you don't want to draft from scratch, some policyholders use a template and then have a contractor, attorney, or public adjuster review the final version before it goes out. That's often a smart middle path. Firms such as NW Claims Management provide claim documentation and dispute support as part of the larger adjustment process, which can help when the issue isn't just writing the letter but proving the full loss.

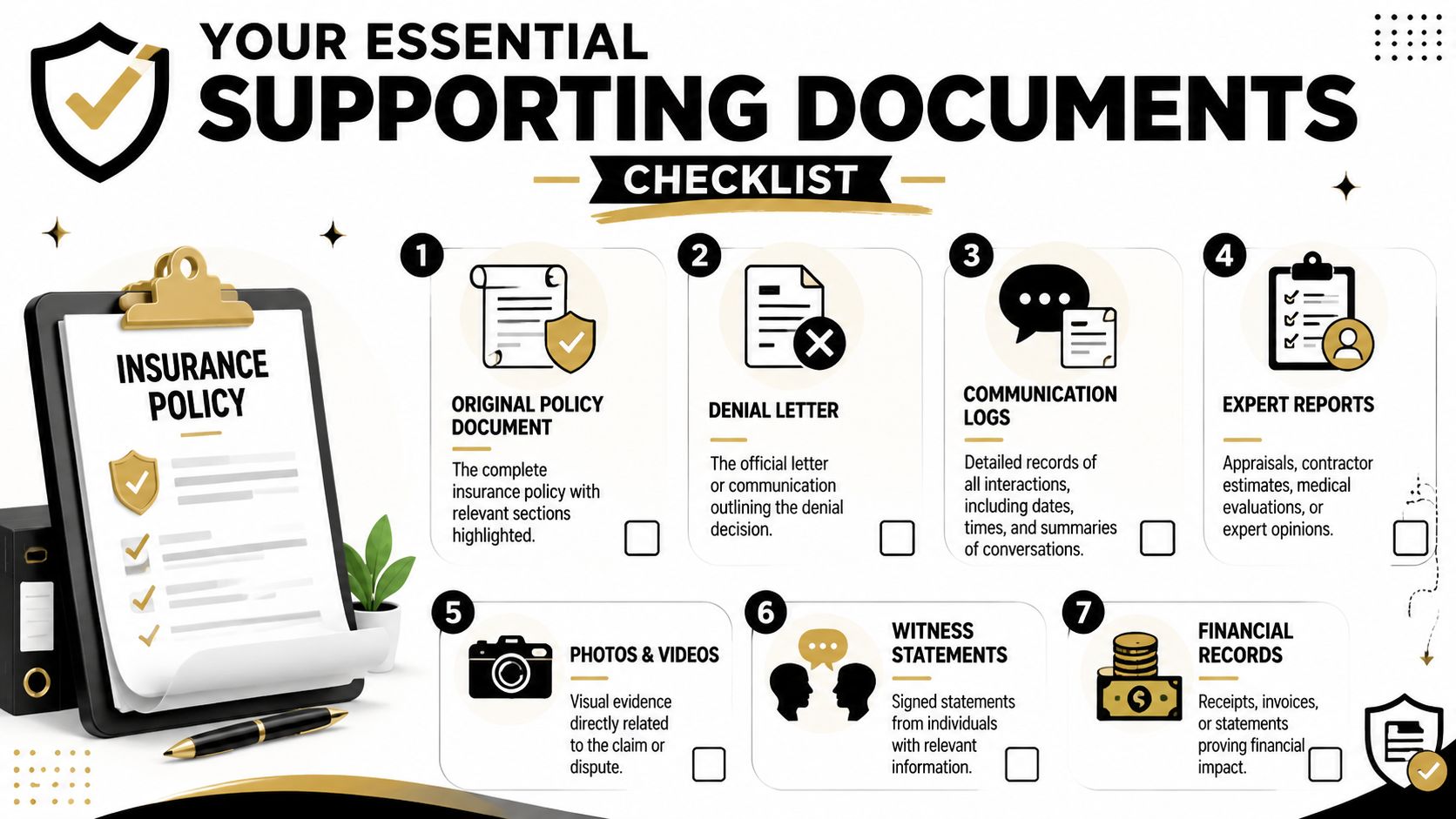

Your Essential Supporting Documents Checklist

A rebuttal letter without attachments is just a disagreement. A rebuttal letter with organized proof becomes a claim file the insurer has to answer.

The biggest mistake I see is homeowners mentioning evidence without packaging it well. If you refer to a contractor estimate, attach it and label it. If you mention photos, mark the date and what each image shows. Don't make the reviewer hunt.

What to gather before you send anything

In scholarly publishing, stronger rebuttals use a point-by-point structure that quotes each comment and identifies exactly where changes appear, and when new information is added it should be clearly referenced so the reviewer doesn't have to search for it. Guidance on major revisions also notes that serious rebuttal files are often several pages long and rely on exact references rather than vague statements in this discussion of rebuttal letter structure and evidence mapping.

The same logic applies here. If you add new evidence, call it out directly in the letter and identify where it appears in the attachment set.

Evidence checklist by dispute type

| Dispute type | Documents to attach | Why it matters |

|---|---|---|

| Coverage denial | Denial letter, full policy, photos, cause-of-loss report, mitigation records, timeline | Shows whether the insurer's stated exclusion actually fits the loss |

| Low estimate | Carrier estimate, independent estimate, room-by-room photos, invoices, material specs | Exposes omitted line items and underpriced repair components |

| Scope dispute | Contractor scope, diagrams, elevation photos, manufacturer information, code-related notes | Shows why partial repair isn't workable |

| Personal property issue | Inventory, photos, receipts, replacement links, prior ownership records | Supports valuation and existence of damaged contents |

If you're disputing damaged contents as part of the same loss, a personal property inventory template can help organize the list before you send it.

How to label the package

Use simple document names that match the letter:

- Exhibit A: Denial Letter dated [date]

- Exhibit B: Contractor Estimate from [company]

- Exhibit C: Interior Damage Photos

- Exhibit D: Plumbing Report

- Exhibit E: Policy Excerpts Highlighted

Don't attach fifty pages and hope the right pages speak for themselves. Name the document. Reference it in the letter. Tie it to a specific disputed point.

That method changes the tone of the dispute. You're no longer asking the insurer to “take another look.” You're directing them to a documented contradiction in their position.

Delivery Strategy and Key OR and WA Rules

How you send the rebuttal affects how seriously it gets treated. A strong letter can still lose force if it lands in the wrong inbox, gets buried in a claims portal, or never reaches anyone above the desk adjuster.

Send it like you may need to prove it later

Email is fine as one channel, but it shouldn't be the only one for a serious denial dispute. Send the rebuttal by certified mail and keep the mailing record, the full packet, and proof of delivery.

If you've never handled certified delivery before, Business Mail Boutique's mail service insights give a practical overview of how that process works and why businesses use it to document receipt.

Address the packet to more than one person when appropriate:

- The assigned adjuster

- The adjuster's supervisor

- The carrier's claims department or claims manager

- Any third-party administrator listed on the denial letter

That isn't overkill. It reduces the chance that your letter dies at the lowest level of review.

Keep a delivery file

Create one folder, digital and paper if possible, with:

- A signed copy of your rebuttal letter

- All exhibits exactly as mailed

- Mailing receipt and delivery confirmation

- A communication log with dates and names

- Any follow-up responses from the insurer

Disciplined policyholders distinguish themselves from frustrated ones. A complete delivery record shows the insurer that you're tracking the claim like a file, not like a one-time complaint.

Oregon and Washington pressure points

If your property is in Oregon, the Oregon Division of Financial Regulation is the state regulator that handles insurance consumer complaints. In Washington, that role belongs to the Office of the Insurance Commissioner. You don't need to threaten a complaint in every rebuttal letter, but you should know those agencies exist and that a formal complaint is an option if the carrier ignores documented issues.

You can also strengthen your position by using language that signals awareness of fair claim handling obligations without turning the letter into fake legal posturing.

For example:

I request a prompt written response that addresses the specific factual and policy issues raised in this letter.

That sentence does more work than a generic threat. It tells the carrier you expect a real answer.

For Oregon policyholders who need local representation, this overview of a public adjuster in Oregon explains how claim advocacy fits into the process.

Timing and tone matter

Send the rebuttal promptly after the denial or low estimate. Don't sit on it while repairs stall and the file goes cold.

At the same time, don't rush out a sloppy packet. A professional rebuttal is measured. It doesn't insult the adjuster. It doesn't accuse everyone of bad faith in the first letter. It builds a file that makes a later escalation more credible if you need one.

When Your Letter Gets Ignored Next Steps

Sometimes the insurer won't engage in a meaningful way. You send a solid rebuttal. They answer with a form paragraph. Or they don't answer at all. That doesn't mean the letter failed. It may mean you've learned exactly how the carrier intends to handle the claim.

That information has value.

When a rebuttal gets ignored, the next move depends on the dispute. If the issue is valuation, appraisal may be available under the policy. If the issue is claim handling, a complaint to the Oregon or Washington regulator may be appropriate. If the issue is broader, such as a flawed scope, misapplied exclusion, or chronic underpayment, it may be time to bring in a public adjuster or coverage counsel.

Signs it's time to escalate

- They repeat the same denial language: No response to your actual evidence.

- They refuse to answer line items: Common in low estimate disputes.

- They keep changing the rationale: The stated reason for denial keeps shifting.

- They stop communicating: Silence after receiving a documented rebuttal is a message in itself.

A lot of policyholders wait too long here. They assume one more phone call will fix it. Usually it won't. Once a carrier has seen your evidence and still won't engage, you need an advantage, not another voicemail.

When professional help changes the outcome

A public adjuster becomes useful when the dispute has moved past simple clarification. At that point, the issue isn't whether you can write a polite letter. It's whether you can document the loss, interpret the policy, challenge the insurer's scope or pricing, and negotiate from a position they take seriously.

If you're at that stage, this guide on when to hire a public adjuster will help you decide whether the claim has crossed that line.

The best rebuttal letter in the world can't fix a claim if nobody is forcing the insurer to confront the full loss.

That's the honest answer. DIY works up to a point. After that, the question becomes whether you want to keep arguing alone or put someone in the file whose job is to fight valuation and coverage issues for a living.

If your insurer denied, underpaid, or narrowed your property claim and you need help building a rebuttal that's grounded in the policy and the actual damage, NW Claims Management can review the claim, document the loss, and help you decide what the next step should be.