The fire trucks are gone. The fans are still running. Your kitchen smells like smoke, your roof tarp is flapping in the rain, or your basement is full of warped flooring and soaked drywall. Then the insurance claim starts, and suddenly the damage itself isn't the only problem.

Now you're expected to answer technical questions, keep track of every conversation, photograph everything, list every damaged item, understand policy language, review repair scopes, and respond to an adjuster who does this every day while you're trying to keep your life from falling apart.

That's the moment most property owners in Oregon and Washington realize something important. This isn't just paperwork. It's a negotiation, and one side is already staffed with professionals.

After Disaster Strikes Your Expert Advocate

A homeowner in the Portland area calls after a tree comes through the roof during a windstorm. The family has already spent days moving furniture, finding temporary housing, and trying to keep water from spreading through the ceiling. They think the hardest part is over.

It usually isn't.

The claim starts with forms, inspections, estimates, recorded conversations, and a growing sense that every answer matters more than it should. A business owner in Washington faces the same thing after a pipe break. A nonprofit director deals with it after vandalism damages a community facility. Different losses, same pressure. The insurer begins building its file immediately, and if you're not doing the same, you're already behind.

That's where a licensed public adjuster changes the entire experience. A public adjuster works for the policyholder, not the insurance company. The job is simple to describe and hard to do well. Read the policy carefully, inspect the loss thoroughly, document everything, value the damage correctly, and push the claim until the insurer pays what the policy allows.

You don't need another person telling you to “be patient.” You need an expert advocate who knows how claims really move in the Pacific Northwest. Oregon and Washington losses often involve moisture migration, smoke contamination, hidden structural issues, code-related repair questions, and weather conditions that make delays more expensive.

When the insurance company has experts on its side, you need one on yours too.

If you're trying to understand what that support looks like in practice, review how home and business public adjusters help policyholders before you go any deeper into the claim alone.

Who Represents Who in an Insurance Claim

Most property owners get tripped up on one basic issue. They assume every adjuster involved is there to help them. That's not how claims work.

If you were in a legal dispute, you wouldn't ask the other side's lawyer to protect your interests. Insurance claims work the same way. The title “adjuster” sounds neutral, but the loyalty behind that title matters.

The three players you need to understand

A company adjuster works directly for the insurance carrier. That person may be polite, responsive, and knowledgeable. None of that changes who signs the paycheck.

An independent adjuster isn't independent from the insurer in the way most homeowners assume. This person is typically a contractor hired by the insurance company to inspect and handle claims on the insurer's behalf.

A licensed public adjuster works for you. That's the only adjuster in the process whose job is tied to the policyholder's financial recovery.

Here's the cleanest way to look at it:

| Insurance Claim Adjuster Comparison | Works For | Represents the Interests Of |

|---|---|---|

| Company Adjuster | Insurance company | Insurance company |

| Independent Adjuster | Insurance company that hired them | Insurance company |

| Licensed Public Adjuster | Policyholder | Policyholder |

Why this distinction changes everything

The insurer's adjusters are focused on evaluating the claim through the insurer's process, software, guidelines, and interpretation of the policy. Sometimes that leads to a fair result. Sometimes it doesn't. But either way, they aren't your advocate.

That matters most when the claim gets technical. Hidden water damage. Partial smoke cleaning versus full replacement. Matching issues. Debris removal. Code upgrade questions. Business interruption support. These aren't small details. They often decide whether you get a workable settlement or an underfunded mess.

Practical rule: Never confuse a courteous insurance representative with your representative.

What a policyholder should do next

Before you rely on the carrier's inspection alone, make sure you understand the difference between a public adjuster and an insurance adjuster. That distinction is the foundation for every decision that follows.

Use this checklist when you speak with anyone on the claim:

- Ask who they work for: Don't assume. Get a direct answer.

- Ask what authority they have: Some people inspect. Others decide. Those aren't the same role.

- Ask whether their estimate is final: Early numbers often change, and sometimes they should.

- Keep your own records: Save emails, inspection dates, photos, and repair proposals.

If you remember only one thing from this section, remember this. The insurance company already has representation. If you don't, you're the only unrepresented party in a professional claims process.

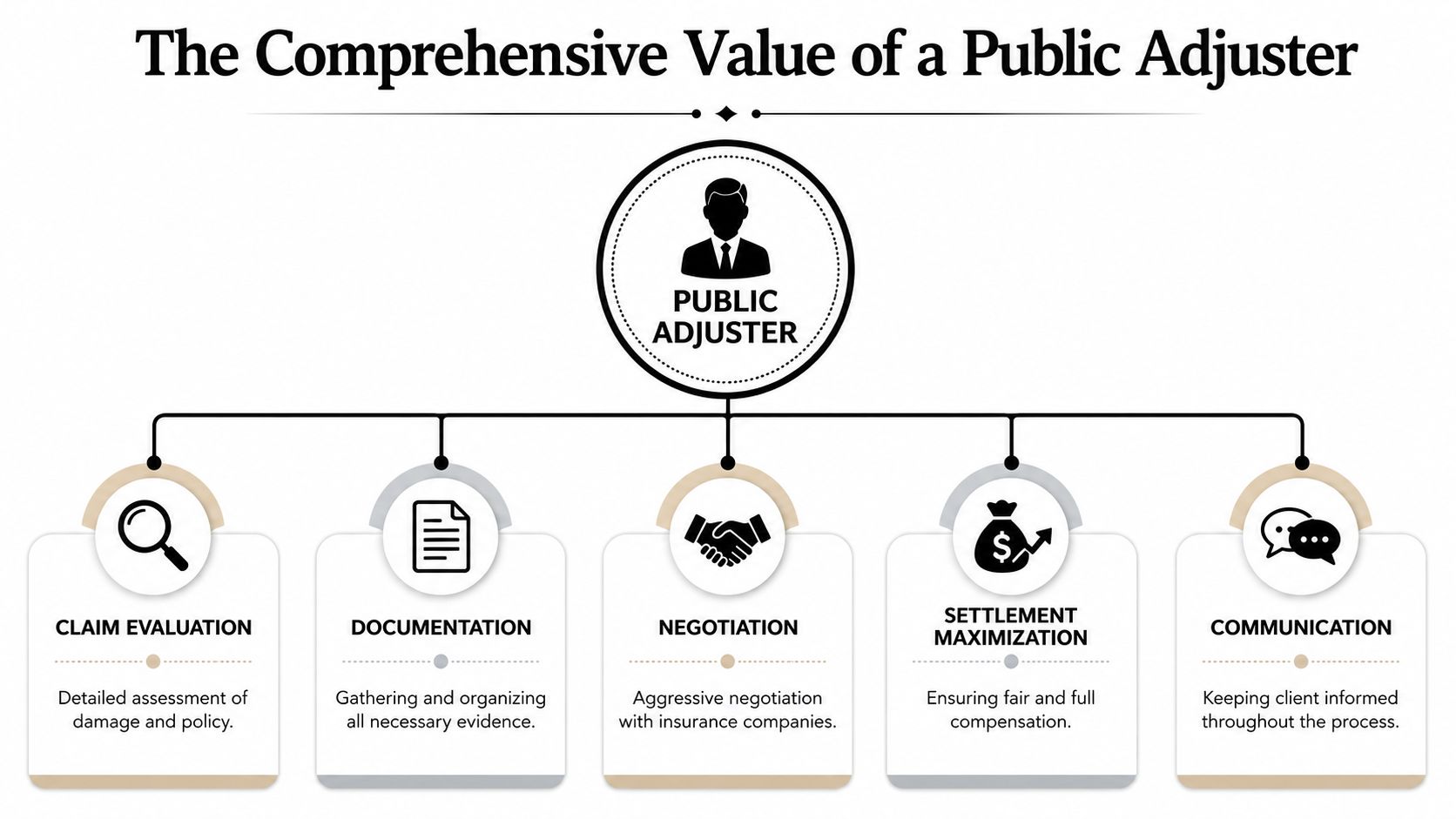

The Services and Value of a Public Adjuster

It's often thought that a public adjuster fills out forms and argues over numbers. That's far too narrow. A good licensed public adjuster builds the claim from the ground up and manages it from first inspection to final payment.

That starts with the policy. Not the summary. The policy itself. Coverage language, exclusions, duties after loss, additional benefits, endorsements, and limitations all need to be read together. Miss one provision and you can leave money on the table without even knowing it.

What the work actually includes

A public adjuster typically handles the parts of the claim that overwhelm policyholders fastest:

- Policy review: Identifying what the contract may cover, including issues many owners overlook until it's too late.

- Damage documentation: Inspecting the property, photographing conditions, organizing evidence, and building a record that supports payment.

- Independent estimating: Preparing a detailed scope and valuation instead of accepting the insurer's first version as gospel.

- Contents and inventory support: Listing damaged personal property, equipment, furnishings, and materials in a way the carrier can evaluate.

- Negotiation and communication: Dealing with the insurer's adjusters, requests, follow-ups, and disputes so you don't carry that burden alone.

This visual sums up the core job:

How that value shows up in real claims

For a homeowner, the difference often shows up in overlooked line items. Smoke damage isn't just black marks on the wall. It can affect insulation, HVAC systems, attic spaces, soft goods, cabinets, and electronics. Water losses often extend behind baseboards, under flooring, and into wall cavities. A public adjuster documents what the eye doesn't catch in a quick walk-through.

For a commercial property owner, the challenge is broader. The building loss is one part. The interruption to operations is another. Lost use of space, damage to tenant improvements, specialized equipment issues, and pressure to reopen fast can all complicate the claim. The faster the claim is organized correctly, the faster the owner can make informed recovery decisions.

For a nonprofit or community organization, the damage can interrupt services people rely on. A claim isn't just about walls and flooring. It's about restoring the building so the organization can continue its mission. That requires careful documentation and persistent communication, especially when the facility serves multiple functions.

Why hiring early matters

The strongest claims are usually built early, before the insurer's first estimate hardens into the default version of the loss. That's one reason public adjusters can have such a major impact. Independent studies have shown that policyholders who hire a public adjuster from the start of their claim receive, on average, settlements that are over 500% larger than those who handle the claim themselves or rely solely on the company adjuster, according to the Florida Office of Program Policy Analysis and Government Accountability report.

That doesn't mean every claim turns into a fight. It means the financial stakes are too high to treat claim preparation casually.

A weak claim file invites a weak payment. A documented claim gives you leverage.

If you want a practical look at the benefits of hiring a public adjuster, focus on one question. Who is doing the work required to prove what your loss is worth?

Licensing and Regulation in Oregon and Washington

“Licensed” isn't marketing language. It's the line between a regulated professional and someone who just says they know claims.

In Oregon and Washington, that distinction matters. After a major loss, out-of-state solicitors and self-described consultants often appear fast. Some know what they're doing. Some don't. If a person wants to represent you in a claim as a public adjuster, licensing and compliance should be the first thing you verify.

What licensing is supposed to tell you

A licensed public adjuster is operating under state rules, not personal promises. That means the adjuster has to meet formal requirements, maintain credentials, and work within legal and ethical standards set by state regulators.

For property owners, that creates accountability. If someone mishandles your claim, misrepresents their authority, or operates outside the rules, there's a regulatory framework behind the license. Without that framework, you're relying on trust alone, and that's a bad gamble when your property and finances are on the line.

What Oregon and Washington owners should ask

You don't need to become a licensing expert. You do need to ask direct questions:

- Are you licensed in my state? If your property is in Oregon or Washington, the adjuster should be properly authorized there.

- Are you bonded if the state requires it? That's part of professional accountability.

- Do you complete ongoing education? Good adjusters stay current on insurance law, ethics, policy interpretation, and claim handling practices.

- Will your contract clearly explain fees and services? If the answer is fuzzy, walk away.

Why local compliance matters in the Pacific Northwest

Oregon and Washington claims carry local issues that outsiders often underestimate. Moisture intrusion, mold risk, smoke spread, steep-roof storm damage, regional contractor availability, and local repair standards can all affect claim presentation. A licensed professional working in these states should understand the regulatory environment and the practical realities of repairing property here.

That's also why a random “catastrophe team” that knocked on your door yesterday may not be the right fit for your claim.

Licensing doesn't guarantee skill. But skipping licensing checks is asking for trouble.

If you want a broader overview of the profession and the credentialing path, this guide on how to become a public insurance adjuster is useful background. As a policyholder, the point is simple. Verify the license first. Ask questions second. Sign nothing until both check out.

Navigating Your Claim with an Expert Advocate

The best time to hire a licensed public adjuster is early. Not after months of frustration. Not after you've given a recorded statement you regret. Not after you've accepted a scope that misses half the damage.

Early involvement changes the file before the claim narrative gets locked in.

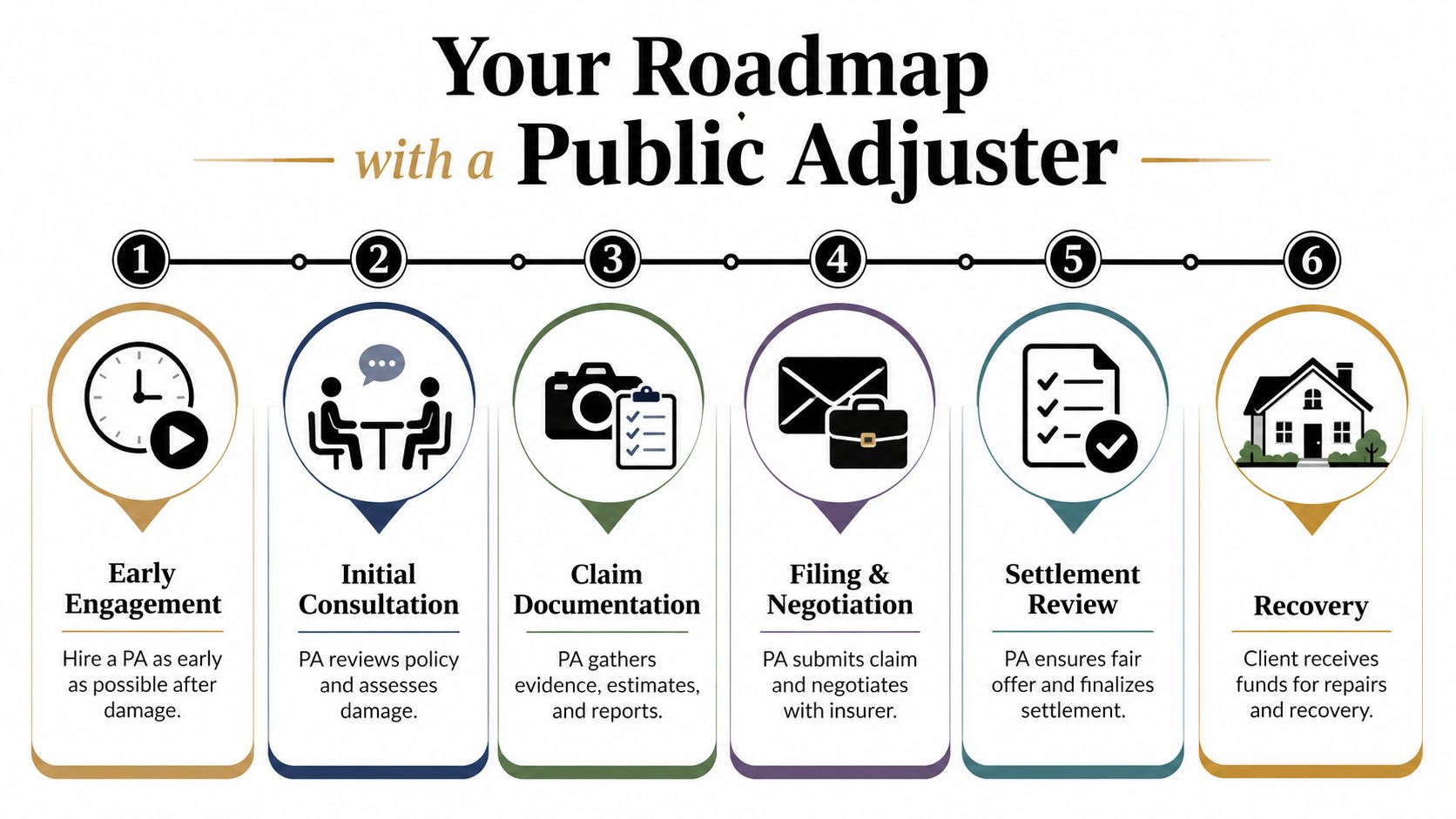

What the claim process looks like

A public adjuster should bring order to a process that usually feels scattered and reactive. The workflow is straightforward when it's handled properly.

In practice, it often looks like this:

Initial review of the loss

The adjuster inspects the property, listens to your timeline, and identifies immediate issues that need documentation.Policy analysis

The policy is reviewed against the facts of the loss so the claim is framed correctly from the beginning.Detailed documentation

Photos, measurements, inventories, contractor input, and supporting records are assembled into a coherent claim package.Claim submission and insurer coordination

The adjuster communicates with the carrier, responds to requests, attends inspections, and keeps the process moving.Negotiation

If the insurer undervalues or omits damage, the public adjuster challenges that position with evidence.Settlement review

Before you accept payment, the numbers and scope are checked against the actual loss.

Common insurer tactics and how to respond

Most policyholders aren't prepared for the pressure points in a claim. They should be.

Recorded statements

Insurers may ask for recorded statements early. Sometimes that request is legitimate. Sometimes it's used to pin you to incomplete facts before the damage is fully understood. A stressed owner can easily miss details, guess at timelines, or speak too broadly.

A public adjuster helps you slow down, prepare properly, and avoid careless statements that can later be used against your claim.

Early low offers

An insurer may present an estimate that feels official and final. It often isn't. It may be incomplete, based on limited inspection, or missing categories of damage that only become clear after deeper review.

That's why you don't judge a claim by the first number you receive.

Delay and attrition

Some claims wear people down. Calls aren't returned promptly. New document requests appear in waves. The file changes hands. You're asked to resend items you already provided. Property owners with jobs, families, or business operations often give in because they're exhausted.

A public adjuster acts as both shield and pressure source. The shield protects you from constant demands and confusing back-and-forth. The pressure source keeps the file active, documented, and harder to ignore.

The insurer works claims all day. You're living through one of the hardest weeks of your life. That imbalance is real.

How fees usually work

Most public adjusters work on a contingency fee. That means the fee is tied to the recovery, not a large upfront payment. The structure matters because it aligns the adjuster's incentive with the result. If there's no recovery, the fee model should reflect that agreement as written in the contract.

One Oregon-based option is NW Claims Management, which handles residential, commercial, and nonprofit property claims in Oregon and Washington on a contingency basis. That model is common because it gives property owners access to representation without paying substantial fees before the claim work begins.

How to Choose the Right Public Adjuster

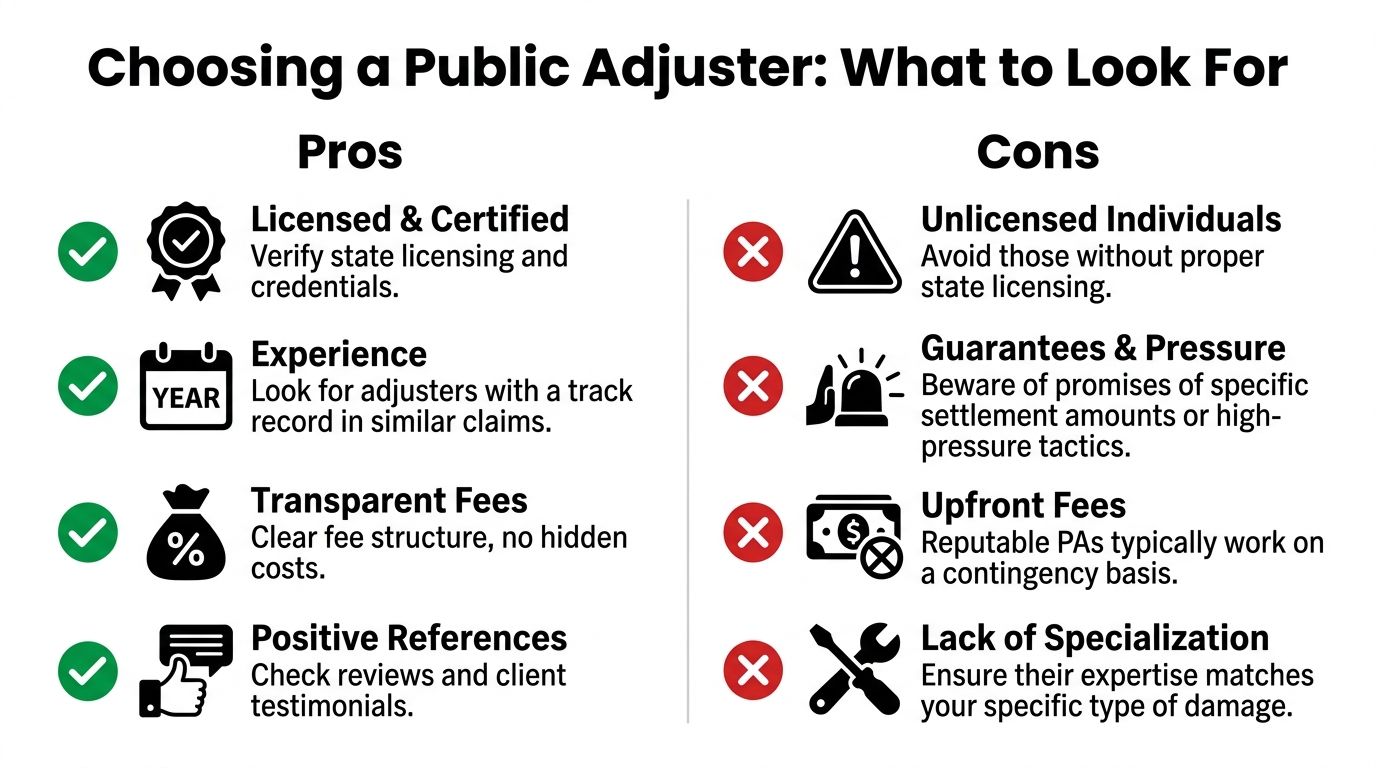

After a major loss, bad actors move fast. They know you're tired, distracted, and worried about money. That's exactly why you need a screening process before you hire anyone.

A polished pitch means nothing. A truck wrap means nothing. A business card means nothing. What matters is licensing, clarity, conduct, and whether the person can explain your claim without resorting to pressure.

Green flags and red flags

This comparison is a good starting point:

Red flags to treat seriously

- Unsolicited pressure: Someone shows up uninvited and pushes you to sign immediately.

- Settlement guarantees: No honest adjuster can promise a specific payout before a full review.

- Large upfront fee demands: Be careful if the payment structure feels front-loaded and aggressive.

- Inflation talk: If they encourage you to exaggerate or “pad” the claim, end the conversation.

- Vague answers about licensing: That should disqualify them on the spot.

Green flags that actually matter

- State licensing and compliance: They can clearly confirm they're authorized to work in Oregon or Washington.

- Relevant claim experience: They understand the type of damage you're dealing with, not just claims in general.

- Clear contract terms: Fees, scope of work, and responsibilities are spelled out in writing.

- Willingness to educate: They answer questions without rushing you.

- Local familiarity: They understand regional construction issues, climate-related damage patterns, and how claims play out here.

Questions worth asking before you sign

Use direct questions. Good professionals won't be offended.

- Who will handle my file?

- How do you document structural damage and contents loss?

- What happens if the insurer disputes your estimate?

- How often will I hear from you?

- Can I review the contract before making a decision?

If someone pushes you to sign before you understand the agreement, they're telling you exactly how they'll handle your claim.

If you're still deciding whether now is the right moment, this guide on when to hire a public adjuster can help you judge timing without guesswork.

Your Local Advocate for Oregon and Washington Claims

When your property is damaged, the claim becomes part financial negotiation, part documentation project, and part endurance test. You don't need to master policy language overnight. You need qualified representation that knows how to carry the load.

That matters even more in Oregon and Washington, where local weather, repair conditions, code questions, and insurer handling patterns can shape the outcome of a claim. A local licensed public adjuster should understand those realities and know how to present damage in a way that holds up under scrutiny.

Here's a look at the firm behind this guidance:

NW Claims Management is based in Portland and serves property owners across Oregon and Washington. The firm handles residential, commercial, and nonprofit claims, and its work centers on policy review, damage documentation, estimate preparation, insurer communication, and settlement negotiation. The local focus matters because property claims in the Pacific Northwest aren't generic.

If you're overwhelmed, that reaction makes sense. You likely only learn how insurance claims really work when you're forced into one. The right advocate helps you regain control, protect your rights, and stop reacting to the insurer's timeline alone.

You don't have to carry the entire claim yourself, and you shouldn't.

If you need calm, experienced help with a property loss in Oregon or Washington, contact NW Claims Management for a free, no-obligation claim evaluation.