You opened the report or the insurer's estimate, looked at the number, and felt your stomach drop. It doesn't match the actual cost to repair the damage. Your contractor says one thing. The carrier's paperwork says another. Now you're stuck wondering whether contesting an appraisal is worth the stress, the cost, and the time.

It usually is, if you're fighting the right battle.

I'm going to be blunt. A low valuation isn't automatically fraud, and it isn't automatically final either. In Oregon and Washington, policyholders lose ground when they assume the insurer's first number is the number. It isn't. If the disagreement is about the amount of loss, your policy may already contain the mechanism to force a real valuation process instead of endless back-and-forth.

The Appraisal Came In Low Now What

You open the insurer's estimate, compare it to what your contractor says the work will cost, and the gap is big enough to stop you cold. That is the point where people make expensive mistakes. They argue by phone, fire off emotional emails, or accept a number that will not finish the repairs.

Slow down and get precise.

Low doesn't mean correct

A low appraisal or estimate usually comes from one of four problems. The scope is incomplete. The measurements are wrong. The pricing is detached from your local market. Or the loss was classified in a way that strips out real cost.

That last point matters more than policyholders realize. In Oregon and Washington, I regularly see losses discounted because the carrier treats code-required work, access issues, matching, or market conditions like optional add-ons instead of actual claim cost. On property valuation disputes outside insurance, the same pattern shows up through missed factors such as external obsolescence, poor comparable selection, or condition errors. The label changes. The result is the same. The number comes in low because the inputs were bad.

If the insurer accepts coverage and the primary dispute is price, quantity, quality, or scope, you are in amount-of-loss territory. That is the zone where appraisal can matter.

Stop treating the first number like a verdict

The insurer's first estimate is usually a working position built from software choices, labor assumptions, depreciation decisions, and line-item judgments made by someone who may never have priced your repair with local contractors. It is paper. It is not proof.

Your job is to identify the exact reason the number is low.

Put the carrier estimate beside the contractor bid and mark every difference. Look for missing trades, low unit costs, omitted demolition, detached overhead and profit, code upgrades, finish mismatches, drying or contamination work, and access issues. If you need help reading what the carrier wrote, this guide to insurance claim estimates will help you spot where the shortfall starts.

What deserves your attention right now

Do not waste energy arguing that the number feels unfair. Pin down the errors.

Focus on evidence that moves value:

- Scope gaps: rooms, assemblies, finishes, detach-reset items, debris removal, permits, and supervision that were left out

- Pricing errors: labor, material, and subcontractor rates that do not reflect your area

- Condition and quality errors: the estimate prices builder-grade materials where the damaged property was clearly better than that

- Market-based factors: delays, access constraints, and outside economic conditions that increase actual repair cost

- Support documents: photos, contractor notes, invoices, prior remodel records, plans, and expert opinions

A weak dispute says the carrier is cheap. A strong dispute shows exactly where the estimate fails and what proof fixes it.

The practical rule

Contest the low number when the difference is tied to identifiable mistakes and the dollars justify the effort. Do not contest it just because you are angry.

That sounds blunt because it is. A formal fight costs time, attention, and often money. But if the estimate is short because the insurer ignored real scope or real market pricing, letting it slide usually costs more than challenging it.

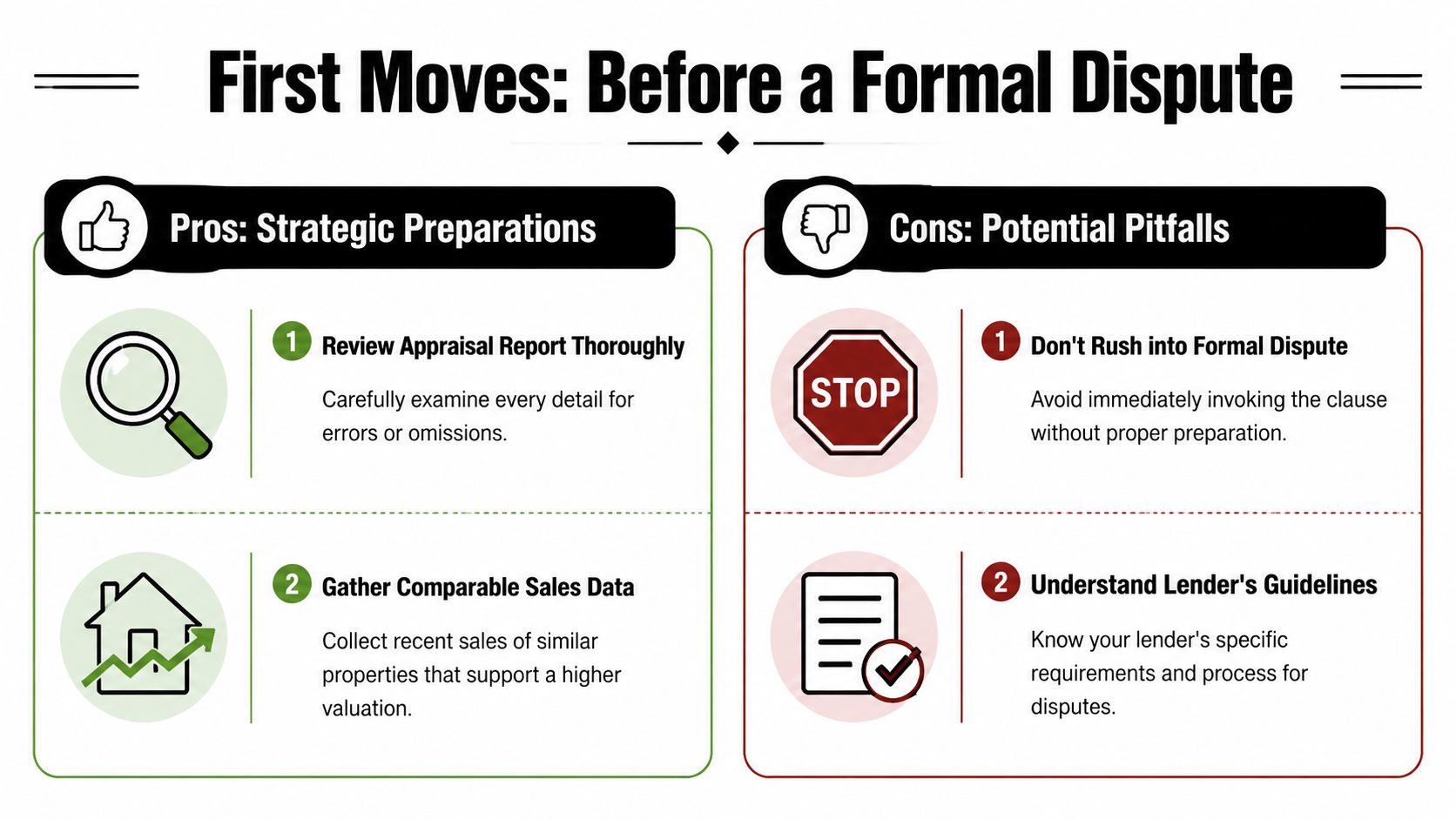

Your First Moves Before Declaring a Formal Dispute

You open the report, see a number that will not cover the actual loss, and feel the urge to fire off an angry email that night. Don't. Your first moves should be boring, disciplined, and strategic. That is how you keep a low appraisal from turning into a worse problem.

The job here is simple. Decide whether you have a correctable error, a real valuation dispute, or just a result you do not like. Those are not the same thing, and Oregon and Washington policyholders lose time when they treat them like they are.

When a reconsideration is worth the effort

A reconsideration works when you can point to something concrete and prove it fast.

Bank of America's overview of disputing a low home appraisal makes the right basic point. Challenges tend to work better when they fix objective errors, not when they argue over opinion. That applies far beyond mortgage deals. In insurance disputes, the same rule holds. Facts move numbers. Frustration does not.

Use reconsideration first if the report or estimate includes:

- wrong square footage or measurements

- missed rooms, features, or structures

- permitted improvements that were ignored

- bad comparable sales

- incorrect condition or quality ratings

- site issues, access limits, or outside influences that affect value, including external obsolescence when it is misapplied or overstated

If your argument boils down to “they should have valued it higher,” stop there. That is not a strategy.

Run your dispute through a hard filter

Before you declare a formal dispute, sort the problem into the right bucket.

- Clear factual error: wrong dimensions, wrong room count, wrong materials, wrong sale data, wrong property features

- Supportable omission: stronger comps existed, relevant damage was missed, or local cost conditions were left out

- Technical valuation issue: the appraiser used a weak adjustment, overstated depreciation, or mishandled external obsolescence

- Pure judgment fight: they saw the same facts and reached a different opinion

- Pressure from the transaction or claim: you need a higher number, but the file does not support it yet

The first three justify real work. The last two usually do not.

Challenges often fail for the same reason: they are built on frustration, not proof.

Audit the report before you escalate

Read the whole thing line by line. Mark every place where the conclusion depends on a bad input.

For homeowners dealing with insurance estimates, it helps to understand how carriers build pricing and scope inside estimating platforms. This Xactimate training resource gives useful context if you need to see how line items, quantities, and assumptions shape the number.

Pay close attention to these pressure points:

- Measurements and quantities: living area, roof, siding, flooring, fencing, detached structures, and waste factors

- Condition and quality calls: water intrusion, smoke residue, hidden damage, code items, finish grade, and prior upgrades

- Market inputs: local labor rates, material pricing, access difficulty, permit requirements, and delays

- Valuation adjustments: depreciation, condition adjustments, location adjustments, and claims of external obsolescence

- Comparables or support data: whether the chosen comps or benchmark properties match your property and market

A good review does more than spot mistakes. It shows you whether the gap comes from one fixable issue or from a pattern of low assumptions.

Do the math before you pick a fight

Formal appraisal is not free. You may need your own appraiser, and in some cases an umpire gets involved too. That expense is one reason you should measure the likely upside before you escalate. If the gap is modest, a focused correction request may be smarter than a full appraisal fight. If the shortfall is large, tied to real evidence, and affecting major scope or valuation issues, contest it.

That is the practical framework. Size of the gap. Quality of the proof. Cost of the process. Probability of a better result.

If you want a plain-English primer on how appraisal logic and inspections shape value, this guide to property appraisals gives a useful baseline. Then come back to your own file and apply that standard with discipline.

One more point matters here. Mortgage appraisal disputes, tax valuation disputes, and insurance appraisal disputes use different procedures and different rules. In Oregon and Washington, that distinction matters early. Use the process that matches the document in front of you, not the one a random online article happened to describe.

Building an Ironclad Case for a Higher Value

You don't win by saying the appraisal is unfair. You win by making the other side look incomplete.

That means your file has to be clean, specific, and easy for another professional to follow. Not a chaotic email chain. Not a folder full of random photos. A real evidence package.

Build the file like a professional

Start with the basics and stack upward.

Core evidence that carries weight

- Photos and video: Organize them by room, elevation, or damaged area. Label them in plain English.

- Repair estimates: Get detailed contractor bids, not vague totals. Line-item detail matters.

- Receipts and invoices: Prior upgrades, mitigation work, emergency repairs, and specialty materials all help establish what's present.

- Property-specific notes: Roof age, custom finishes, outbuildings, drainage issues, access problems, or specialty systems.

If you're dealing with line-item pricing fights in an insurance claim, it helps to understand how carriers often build estimates inside Xactimate. A practical place to get familiar with that environment is this Xactimate resource.

The advanced points most people miss

Many challenges often fail. They focus only on “better comps” and never address the technical adjustments driving value down.

A better strategy is to identify compensating factors and challenge claims of external obsolescence when they're weak or overstated. As explained in this discussion of appraisal dispute strategy, successful disputes often hinge on showing that the appraiser missed positive location factors or deducted too much for outside influences.

Compensating factors

A compensating factor is a feature that offsets a weakness in a comparison.

Examples:

- Your property sits in the stronger part of a neighborhood.

- Your lot has better utility, privacy, or access.

- The comp backed to a busier corridor, mixed-use parcel, or nuisance use, and yours doesn't.

- The comp had inferior curb appeal or layout.

External obsolescence

This refers to value loss caused by outside conditions, not the house itself.

Common examples include:

- Proximity to commercial use

- Traffic noise

- Flood-related stigma

- Nearby adverse land use

- Functional impact from surrounding development

If an appraiser or evaluator applies an external obsolescence deduction, ask one direct question: What specific outside condition, on this property, justifies that adjustment? If the answer is fuzzy, the deduction may be vulnerable.

Field advice: Don't just say a comp is bad. Explain why its outside influences differ from your property and how that changes value.

Present it in the right order

Your evidence package should read like a short case, not a dump of paperwork.

- State the disputed conclusion

- Identify the factual errors or omissions

- Attach photos, bids, receipts, and comparison notes

- Explain technical points like compensating factors

- Ask for a specific correction or revised number

If you want a broader non-insurance reference for how appraisal logic works, this guide to property appraisals is useful because it helps property owners understand the vocabulary professionals use. That matters. Once you use the right language, your challenge gets taken more seriously.

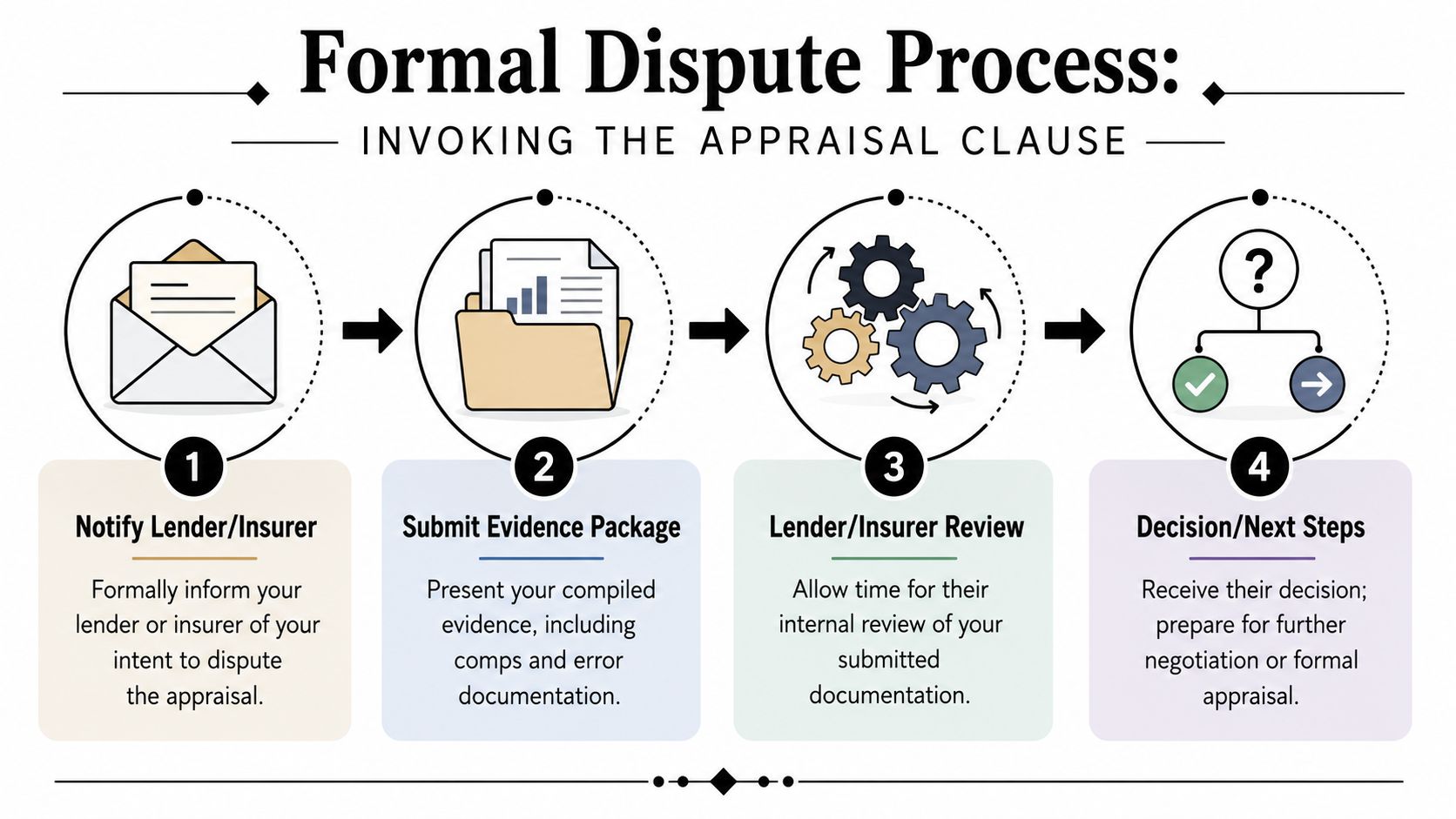

Invoking the Appraisal Clause and The Formal Process

Your carrier says the number is final. It is not. If the fight is about price, scope pricing, or the amount of covered damage, you stop arguing in circles and trigger the appraisal clause the right way.

Done correctly, appraisal forces the dispute into a defined process. Done sloppily, it gives the insurer room to stall, blur coverage with valuation, or attack your appraiser choice.

What the demand needs to say

Your demand letter should read like a formal trigger under the policy, not a complaint email.

Include these points:

- a clear statement that there is a dispute over the amount of loss

- the policy number, claim number, date of loss, and the policy language that gives either side the right to demand appraisal

- a short, specific description of what values are disputed

- the name and full contact information for your chosen appraiser

- a request that the carrier identify its appraiser by the deadline in the policy

- any proposed ground rules or appraisal agreement, if you want the scope and procedures pinned down early

Keep it tight. Keep it specific. If you bury the dispute in pages of argument, you make the opening move weaker than it needs to be.

If you have not submitted the documents the policy requires before appraisal, fix that first. In many claims, that means getting the proof of loss and your appraiser designation handled before the carrier can claim your demand is premature.

Define the dispute before the panel does it for you

Policyholders in Oregon and Washington lose control of the process at this point. They demand appraisal without pinning down what the panel is supposed to value.

Do not hand the panel a vague mess. State the disputed categories in writing. Roofing. Interior finishes. Drying. Framing. Code-related work. Overhead and profit. Exterior components. Spell it out.

Then separate valuation from coverage. If the insurer says, "we agree on price, but that item is excluded," that is a coverage dispute. Appraisal usually decides the amount of loss, not whether the policy covers a category at all. If you mix those issues together, the carrier gets a built-in argument later about whether the award means anything.

This matters even more in water claims, where hidden moisture, demolition, microbial growth, and code upgrades often get folded into one blurry disagreement. The Eagle Restoration water damage guide gives a useful overview of the repair issues that often sit underneath these valuation fights.

The formal process, step by step

Most policies follow the same sequence. The exact deadline can vary by policy form, so read yours and use the stated timing, not what an adjuster says on the phone.

| Stage | What happens | Why it matters |

|---|---|---|

| Demand | One side sends a written demand for appraisal under the policy | This starts the contractual process and frames the dispute |

| Appraiser selection | Each side names its appraiser within the policy deadline, often 20 days from the demand | A weak or conflicted appraiser puts you behind immediately |

| Umpire selection | The two appraisers try to agree on an umpire if they cannot resolve the amount themselves | The umpire can decide the outcome if the appraisers split |

| Award | Any two of the three sign the written award | That signed award usually fixes the amount of loss |

The common 20-day appointment window shows up in many appraisal clauses, but do not assume. Verify the exact wording in your policy and quote it in your demand. That cuts off a lot of nonsense early.

A practical recommendation

Ask for a written appraisal protocol if the claim is large, technical, or already contentious. That document can address the scope submitted to the panel, exchange deadlines, inspection access, whether line-item estimates will be shared, and how the umpire gets involved. Clear procedure lowers the odds of a side fight over process.

If you want a policyholder-focused explanation of how insurer-side appraisal works before you send the demand, review this home insurance appraisal overview. It lays out the mechanics in plain language, which helps you make a cleaner first move.

Once you invoke appraisal, act like the file may end up in front of an umpire. Because it might.

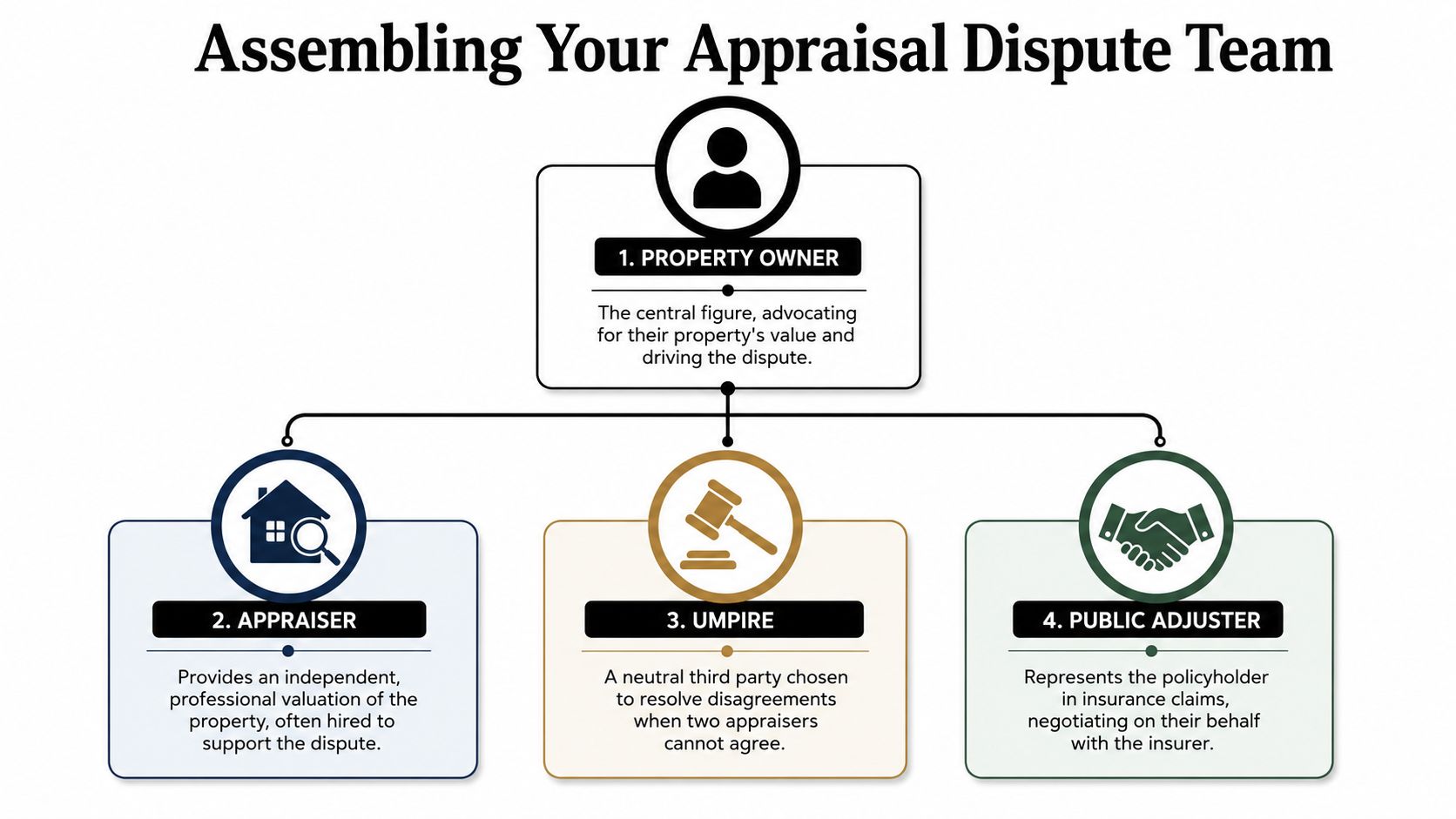

Assembling Your Team Appraisers Umpires and Public Adjusters

You don't need a crowd. You need the right people in the right roles.

At this stage, stressed policyholders often make expensive mistakes. They hire someone because the title sounds impressive, then learn too late that the person can't do what the claim needs.

The role confusion that hurts claims

An appraiser values the disputed loss. An umpire breaks a deadlock. A lawyer handles legal and coverage disputes. A public adjuster manages and advances the claim for the policyholder.

Those are not interchangeable jobs.

If your problem is that the insurer underpriced demolition, drying, structural repair, finish work, and code-related items, a lawyer may not be the first person you need. If the carrier denied coverage outright, an appraiser won't solve that. If the claim is sprawling and document-heavy, trying to manage everything alone often leads to a weaker presentation.

Who does what in an appraisal dispute

| Role | Primary Function | Best For |

|---|---|---|

| Appraiser | Evaluates the amount of loss and argues valuation within the appraisal process | Scope and pricing disputes |

| Umpire | Acts as neutral tiebreaker if appraisers can't agree | Deadlocked valuation issues |

| Lawyer | Addresses legal rights, coverage disputes, bad-faith issues, and litigation strategy | Coverage denial or legal escalation |

| Public adjuster | Represents the policyholder, documents damage, organizes evidence, negotiates with the insurer, and helps manage appraisal strategy | Complex claims and overwhelmed policyholders |

What to look for in an appraiser

Don't hire based on personality alone. Hire based on claim fit.

Look for:

- Relevant property experience: Fire loss, water loss, storm damage, commercial build-outs, or large residential repairs.

- Actual estimating fluency: They should be able to explain line-item differences, not just give opinions.

- Disinterested status: The policy language usually requires this. That standard matters.

- Communication discipline: A strong appraiser writes clearly and doesn't create unnecessary noise.

Why a public adjuster changes the outcome

A public adjuster isn't just another voice on the claim. A good one coordinates the entire record. They make sure the estimate, the photos, the scope, the contractor input, and the policy position all point in the same direction.

That's especially important in Oregon and Washington, where policyholders often juggle weather-related damage, contractor shortages, and insurer delay tactics at the same time. A public adjuster can keep the claim organized, push back on low scope, and keep valuation disputes from sliding into procedural confusion.

If you want a clear picture of what policyholder representation involves, review how an insurance claim public adjuster works before you decide who should lead your side.

The wrong hire makes the claim louder. The right hire makes it stronger.

Oregon and Washington Rules and Final Takeaways

In Oregon and Washington, insurers still owe policyholders fair dealing. That doesn't mean they'll volunteer their best number. It means you should expect resistance wrapped in procedure.

Your advantage is preparation.

If you're contesting an appraisal in the Pacific Northwest, keep your focus narrow and sharp. Separate coverage disputes from amount-of-loss disputes. Document damage early. Build a file that another professional can follow without guessing. If you're arguing market value in a real-estate context, don't rely on emotion. If you're invoking an insurance appraisal clause, define the disputed scope in writing and do it cleanly.

For Oregon property owners, local property records can help verify key facts when you're checking characteristics tied to valuation arguments. A practical place to start is the Portland assessors database.

The main takeaway is simple. A low appraisal is not the end of the story. It's the start of a decision. Sometimes the right move is a narrow reconsideration based on obvious errors. Sometimes the right move is formal appraisal. Sometimes the smartest choice is to stop arguing weak points and press the few facts that materially change value.

Be calm. Be specific. Don't let the insurer or lender define the claim for you.

If you're dealing with a low insurance valuation in Oregon or Washington and need someone to take control of the process, NW Claims Management can help. Their licensed public adjusters represent policyholders, not insurers, and they handle the documentation, valuation, and negotiation work that most owners should not be forced to manage alone after a major loss.