A Proof of Loss is a formal, sworn statement you must send to your insurance company detailing the amount of money you are claiming for your property damage. Under standard property policies, it's typically due within 60 days of the insurer's written request, and mistakes can delay or jeopardize the claim.

That letter from the carrier usually arrives when you're already stretched thin. The roof is torn open, the kitchen smells like smoke, the tenants are calling, or the mitigation crew is asking who's authorizing the next step. Then the insurer sends a document request that sounds routine but isn't routine at all.

Most homeowners first read “Proof of Loss” and assume it's just another claims form. It isn't. It's the point where your claim moves from “we had damage” to “this is the factual and financial position I am swearing to.” If you're trying to understand where this fits in the broader claims timeline, this overview of the home insurance claim process helps place it in context.

In Oregon and Washington, that distinction matters. A lot of claims don't break down because the damage isn't real. They break down because the paperwork is vague, rushed, unsupported, or submitted late. A strong Proof of Loss protects your advantage. A weak one gives the insurer room to challenge scope, value, ownership, timing, and compliance.

Your Insurer Demands a Proof of Loss Now What

The usual sequence goes like this. You report the loss. An adjuster inspects. You exchange emails, photos, maybe a contractor estimate. Then a formal letter arrives demanding a signed Proof of Loss. That's often the moment a policyholder realizes the claim has entered a more serious stage.

The first move is simple. Slow down and read the request carefully. Look for the deadline, the form the insurer wants used, whether notarization is required, and exactly what supporting documents they're asking for.

What to do in the first day

When that request lands, focus on control, not speed.

- Confirm the trigger date: The deadline usually runs from the insurer's written request, not from the date of loss.

- Create a claim file: Keep the request letter, envelope or email, policy, estimates, photos, and every communication in one place.

- Stop guessing on value: If you haven't fully assessed the damage, don't rush into numbers you can't support.

- Check for gaps: Many homeowners have building estimates but no contents inventory, or photos but no contractor scope.

A Proof of Loss is often the first document in the claim that can seriously hurt you if it's incomplete, inaccurate, or casually prepared.

Why this moment matters

Insurers ask for a Proof of Loss because they want your position in a sworn, reviewable form. That changes the tone of the claim. From here forward, your documentation quality matters as much as the damage itself.

If you treat the request like administrative cleanup, you can understate the loss before repairs are fully scoped. If you treat it like a legal and financial submission, you give yourself a stronger platform for the rest of the negotiation.

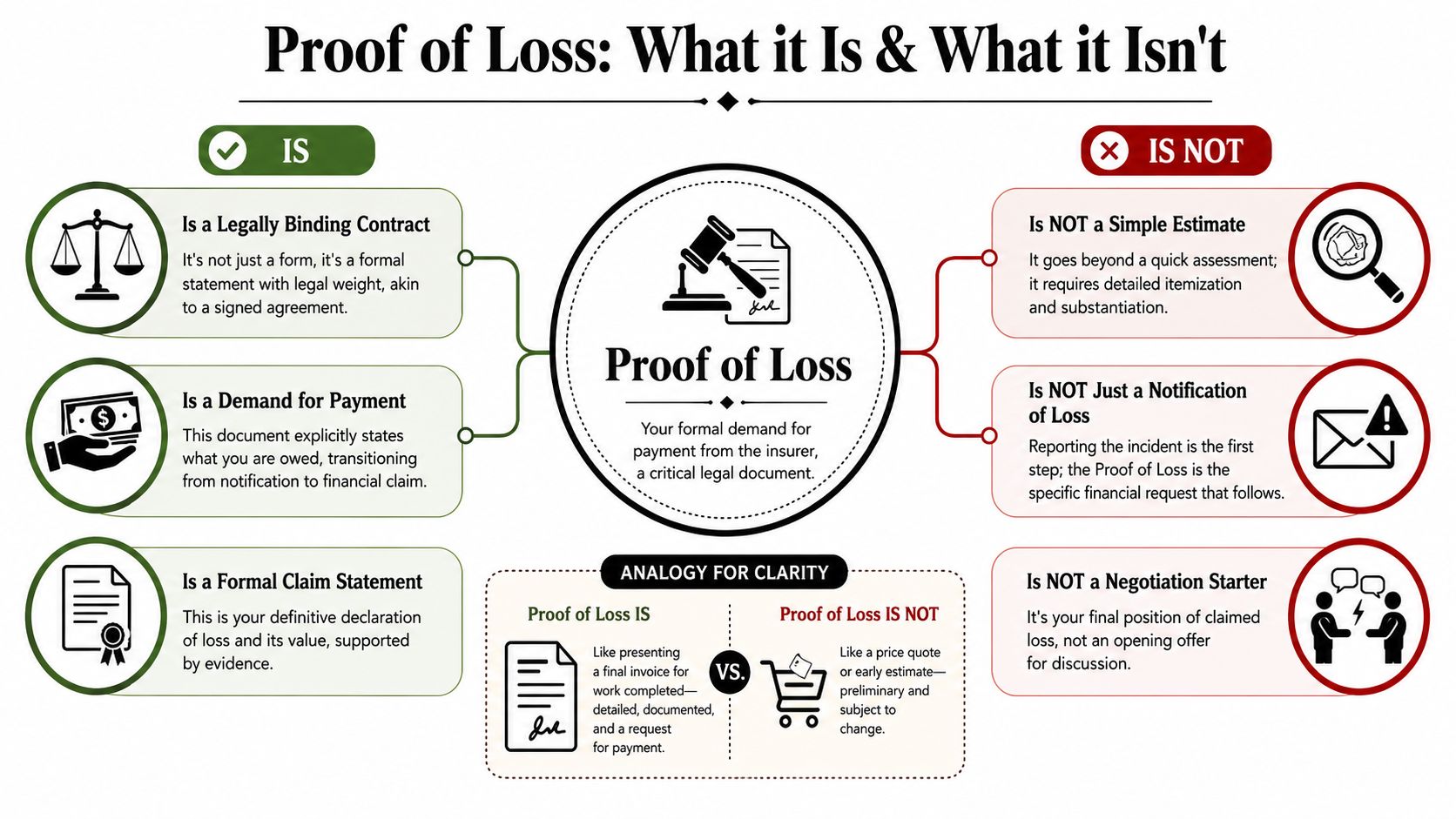

What a Proof of Loss Really Is and What It Is Not

A lot of confusion comes from the name. “Proof of Loss” sounds like you're merely proving that something bad happened. In practice, it does much more than that.

A Proof of Loss is a legally binding, sworn statement, typically requiring notarization, that standard property insurance policies use as a post-loss contractual obligation. It requires the policyholder to submit a signed, detailed account of damaged or destroyed property and the specific dollar amount claimed within 60 days of the insurer's written request. It is separate from the initial claim report and formally locks in the insured's position on the facts and value of the claim. The insurer then uses it to check the claim against policy coverage and begin its liability investigation. Failing to comply can delay or legally jeopardize the claim, and this requirement appears in nearly every homeowners policy contract, as explained in this breakdown of Proof of Loss requirements.

Think of it like a sworn declaration

The closest practical analogy is an affidavit attached to a financial demand. You're not just telling the insurer, “My home was damaged.” You're saying, under oath, “These are the facts, this is the property involved, and this is the amount I claim is owed.”

That's why casual language causes trouble. “About,” “around,” “roughly,” and “I think” have no place in a polished Proof of Loss unless the form or supporting narrative clearly explains an estimate and the basis for it.

A useful related concept is the legal meaning of damage in an insurance dispute. The carrier is not evaluating your frustration or inconvenience. It is evaluating documented, policy-covered damage and the amount tied to it.

What it is not

A Proof of Loss is not your first notice of claim. Reporting a fire, storm, or water event starts the file. The Proof of Loss states the formal amount you're seeking.

It's also not a rough estimate scribbled on a contractor bid. A contractor proposal may support your numbers, but the sworn statement itself is your submission, not the contractor's.

And it isn't a casual opening offer. Many policyholders assume they can throw out a number and “sort it out later.” That's risky. Once you sign a sworn claim statement, every inconsistency becomes something the insurer can examine.

| What it is | What it is not |

|---|---|

| A sworn claim statement | A simple notice that damage happened |

| A contractual obligation | Optional paperwork |

| A documented demand for payment | A guess at repair cost |

| A position backed by evidence | A placeholder until you get organized |

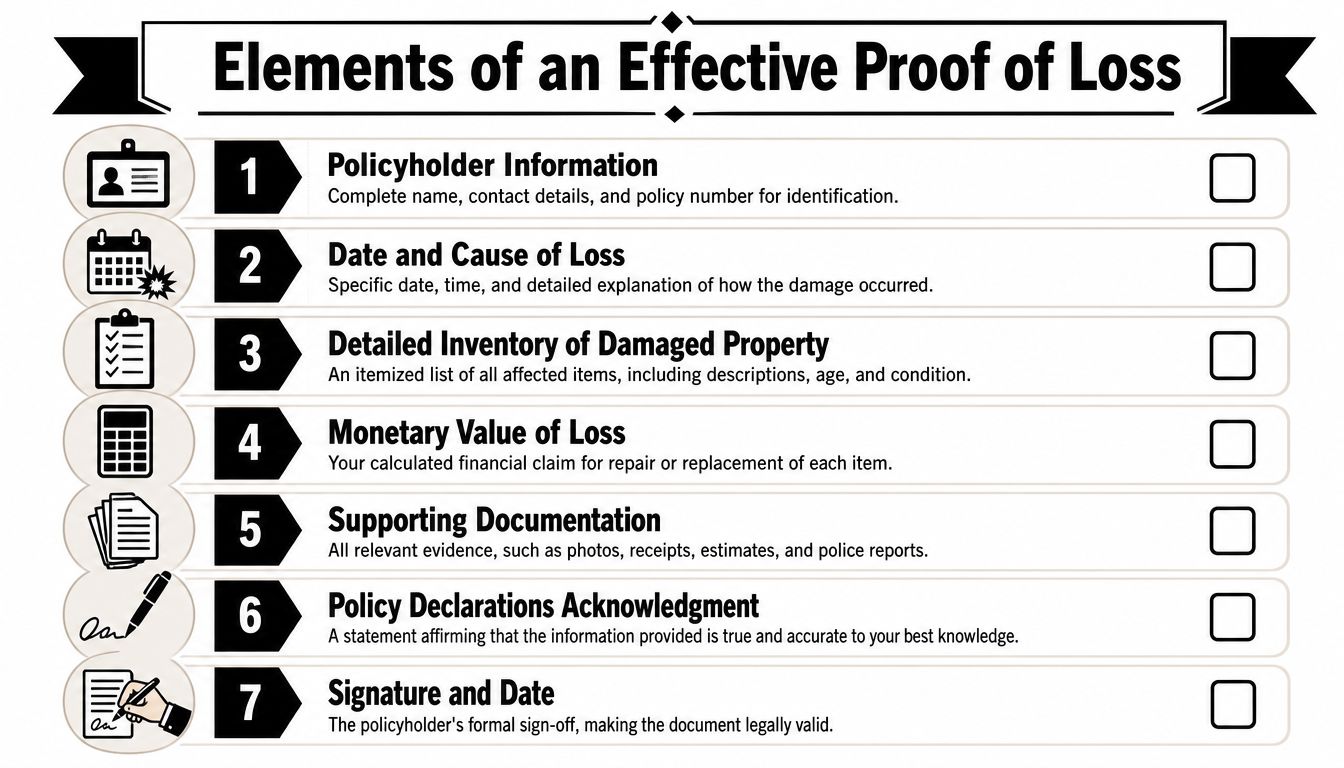

Anatomy of a Bulletproof Proof of Loss

A strong Proof of Loss is built like a case file. Every line should answer one question from the insurer before they have to ask it. If your form raises more questions than it answers, you've given away time and your advantage.

This visual checklist captures the core pieces.

The information that has to be there

Effective Proof of Loss documentation needs a granular evidentiary foundation. That includes the precise date and cause of loss, a detailed inventory of damaged property with specific locations, itemized estimates for repair or replacement costs valued as either Actual Cash Value (ACV) or Replacement Cost Value (RCV) depending on the policy, identification of the claimant, all parties with an interest in the property such as mortgagees or lienholders, disclosure of other applicable insurance, and a sworn certification signed under oath. Supporting evidence often includes photos, videos, receipts, and contractor estimates, as outlined in this explanation of what a Proof of Loss requires.

Here's how that translates in practice:

- Claimant details: Full legal name, property address, policy number, and contact information. If this is wrong, the file gets messy fast.

- Date and cause of loss: Be specific. “Water damage” is weak. “Water intrusion from a supply line failure under the upstairs bathroom sink” is useful.

- Damaged property by location: Room-by-room works better than broad summaries. Kitchen cabinets, hallway flooring, garage drywall, office contents.

- Dollar amount claimed: This is the heart of the document. It should come from actual estimating, invoices, inventory, and valuation work.

- Interested parties: Mortgage lenders, property managers, co-owners, or lienholders can't be omitted.

- Other insurance: If another policy may apply, disclose it. Hidden overlap creates credibility problems later.

- Sworn signature: If notarization is required, do it properly.

What separates a strong file from a weak one

The form itself is only part of the package. The supporting material is what makes the sworn number credible.

A solid submission often includes:

- Photographs and video: Wide shots show context. Close-ups show damage detail.

- Contractor estimates: Prefer detailed scopes over one-line bids.

- Mitigation invoices: Drying, board-up, pack-out, or emergency service charges should be organized and labeled.

- Personal property inventory: Brand, model, age, condition, location, and value basis. A personal property inventory template can help keep that list usable.

- Receipts and statements: Helpful when available, but not the only support.

- Repair history or pre-loss condition evidence: This can matter when the insurer questions age or wear.

Practical rule: If a stranger picked up your Proof of Loss package, they should be able to understand what was damaged, where it was damaged, why you value it that way, and what documents support each number.

ACV versus RCV changes strategy

Many insureds leave money on the table. If your policy pays on an ACV basis first and later releases replacement cost benefits after repairs, your Proof of Loss still needs a valuation framework that fits the policy. If you submit a single unsupported lump sum, you make both coverage review and later recoverable depreciation issues harder.

Use a simple structure:

| Category | Best support |

|---|---|

| Building damage | Line-item repair estimate with room or trade breakdown |

| Personal property | Itemized inventory with ownership support and value basis |

| Additional claimed amounts | Invoices, logs, or policy-based calculations where applicable |

The best Proofs of Loss aren't dramatic. They're organized, specific, and hard to pick apart.

Critical Deadlines and Rules for Oregon and Washington

For most policyholders, the deadline is the danger point. The insurer's request triggers the clock, and under standard property policy language the Proof of Loss is typically due within 60 days. Miss that date and you may spend the rest of the claim arguing about compliance instead of damage.

That doesn't mean panic helps. It means you should treat the deadline as a fixed project date from the first day the request arrives. Put it on your calendar. Put a reminder well before it. Build backward from the notarization and delivery step.

What Oregon and Washington policyholders should do first

In Oregon and Washington, the safest approach is strict compliance. Don't assume the insurer will excuse a technical defect because you've otherwise cooperated. Don't assume a field adjuster's casual comment changes the written requirement. And don't assume an email saying “we're still reviewing” extends your deadline.

If you need more time because the loss is complex, ask for an extension in writing before the deadline passes. Keep the request simple and professional. State why more time is needed, list what remains to be gathered, and ask the insurer to confirm the extension in writing.

Practical deadline handling

Use this sequence:

- Read the request letter the day it arrives

- Confirm the due date in writing if the letter is unclear

- Start gathering estimates and contents documentation immediately

- Request any extension before the deadline, not after

- Submit with proof of delivery

If the carrier wants a sworn statement, act like every date and signature will matter later, because they might.

For Oregon homeowners dealing with a large or technical loss, guidance from an Oregon-focused public adjuster resource can help you evaluate whether your timeline is realistic before the deadline closes in.

Common and Costly Proof of Loss Mistakes to Avoid

Most bad Proofs of Loss don't fail because someone lied. They fail because someone rushed, guessed, omitted, or misunderstood what the insurer was really testing.

The most expensive mistake is under-claiming. Homeowners often focus on what they can see on day one. They include the obvious drywall, flooring, and visible contents, but miss demolition, detached structures, code-related issues, specialty finishes, hidden moisture, or business property mixed into the residence. A low sworn number can box you into a weaker negotiating position.

Mistakes that cause trouble fast

- Incomplete form fields: Blank spaces invite follow-up and suspicion. If something doesn't apply, say so clearly rather than leaving it empty.

- Vague descriptions: “Various items damaged” is not a contents claim. “Samsung television from living room, water damaged during firefighting efforts” is better.

- No document trail: Numbers without support are easy to challenge.

- Late submission: A strong claim can still become a compliance fight if the deadline passes.

- Overstatement: Inflating damage can trigger fraud scrutiny. Don't do it.

- Relying on memory alone: Especially for contents, memory fades and broad estimates get picked apart.

Proof of Loss is not proof of ownership

This is the trap many homeowners never see coming. They think, “I swore to the loss amount, so I'm covered.” Not necessarily.

For personal property claims, there's a critical difference between proving the amount claimed and proving you owned the item in the first place. According to Allstate's explanation of proof of ownership for insurance claims, 38% of denied personal property claims stem from ownership disputes, not loss-value disputes. That's why receipts alone don't solve every problem, and why ownership support such as bank statements, photos, and serial numbers matters for higher-value items.

A sworn statement without ownership evidence is weak where contents are concerned.

What works better than receipts alone

Use layers of proof. One piece rarely carries the whole burden for expensive contents.

| Item type | Better ownership support |

|---|---|

| Electronics | Serial number photos, purchase statements, product registration |

| Jewelry or collectibles | Appraisals, photos of use, purchase records, storage records |

| Furniture | Delivery records, room photos, card statements |

| Tools or equipment | Photos, inventory lists, model numbers, maintenance records |

Homeowners lose legitimate contents claims when they can describe the item but can't prove they owned it.

Digital home inventories also help. A narrated video walkthrough of each room, showing item condition and identifying major purchases, can become powerful ownership evidence later. The best time to create one is before a loss, but after a loss you should still gather every pre-loss photo, social media image, move-in video, and phone backup that shows the item existed.

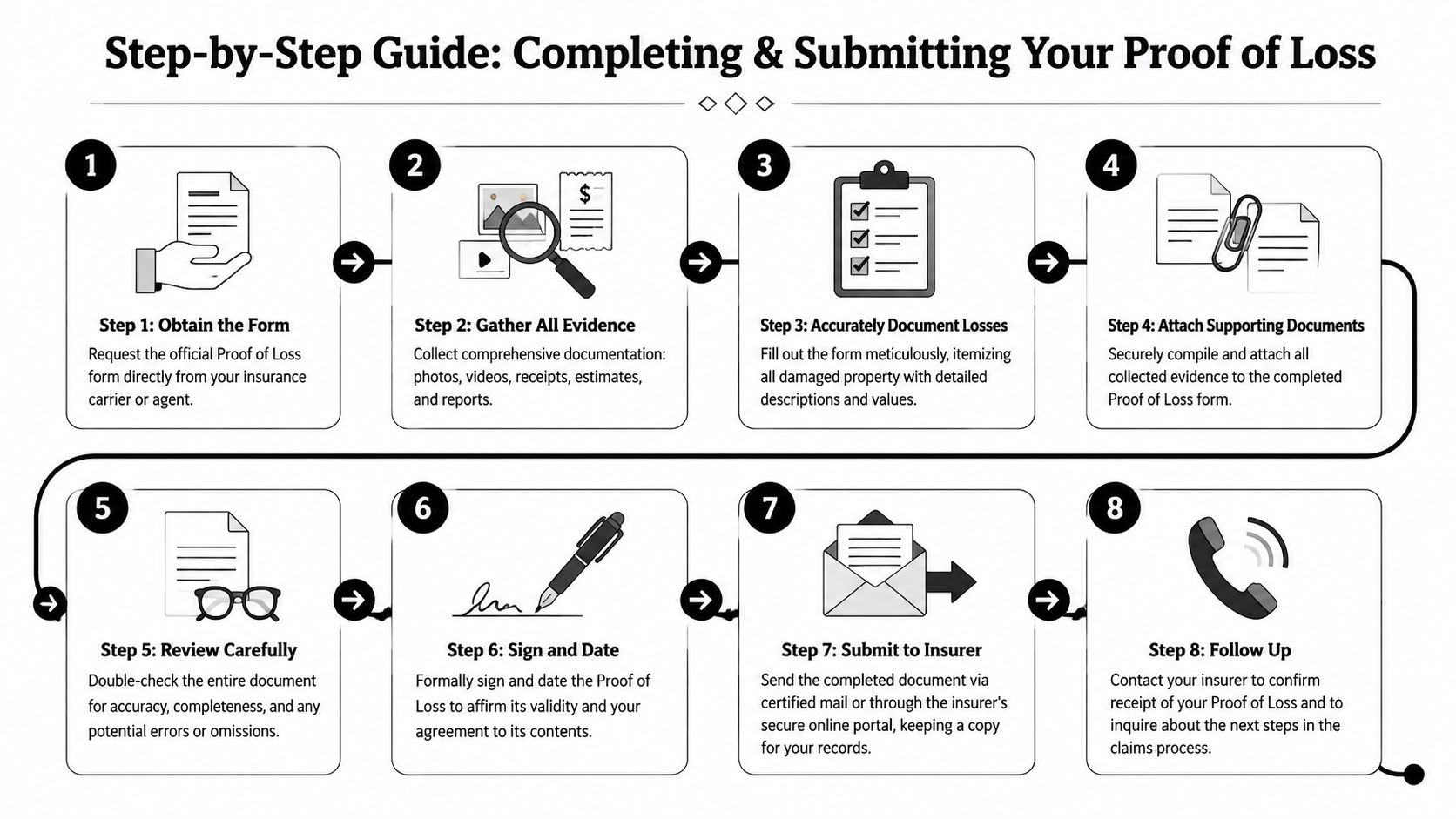

How to Complete and Submit Your Proof of Loss

Once you have the insurer's form and the supporting documents, the work becomes procedural. That's good news. Procedure can be controlled.

This process flow is the practical version most policyholders need.

A clean way to do it

Get the correct form from the insurer

Don't download a random template. Use the carrier's form if they've requested one.Read the entire form before writing anything

Identify what information is required, where attachments are referenced, and whether notarization is expected.Draft your numbers from evidence, not memory

Use contractor estimates, mitigation invoices, and organized inventory sheets.Write the cause of loss clearly

Keep it factual. For example:

“On or about [date], the property sustained damage caused by fire originating in the kitchen area.”

Or:

“On or about [date], the property sustained water damage resulting from a sudden plumbing failure.”Attach the supporting documents in a logical order

Label files. A reviewer should not have to guess what belongs to what.

Review before you sign

Before signing, compare the Proof of Loss to every major document in the claim file. The dates, property address, named insured, and totals should align. If your estimate says one thing and your sworn total says another, fix the discrepancy before submission.

Use a final review checklist:

- Names match the policy

- Loss date matches all estimates and reports

- Claimed amount matches the attached support

- Interested parties are listed

- Attachments are referenced and included

- Signature and notary sections are complete if required

Submission methods that create a record

Once signed, submit in a way that proves timing and content. Certified mail with return receipt requested is a common choice. If the insurer uses a secure claim portal, upload there too if appropriate, but keep screenshots or confirmation receipts.

Then keep a complete copy of everything you sent, exactly as sent.

Send the Proof of Loss like you may need to prove later when it was delivered and what was attached.

After submission, ask the insurer to confirm receipt and identify any claimed deficiencies in writing. Don't settle for “we got something.” You want a clear acknowledgment tied to the actual package.

When to Hire a Public Adjuster for Your Proof of Loss

Some claims are manageable without professional help. A small, well-documented loss with clear scope and limited contents can sometimes be handled directly by the policyholder. But many Proofs of Loss become difficult for reasons that have nothing to do with intelligence or effort. The homeowner is displaced, the building estimate keeps changing, the contents list is overwhelming, or the insurer is questioning causation, scope, or value.

That's when a public adjuster becomes a strategic decision, not a last resort.

Situations where help makes sense

You should strongly consider professional representation if:

- The loss is large or complex: Fire losses, major water events, storm losses, and mixed building-plus-contents claims get technical fast.

- The scope keeps growing: Hidden damage, code issues, and specialty materials often surface after the initial inspection.

- You're getting conflicting numbers: Contractor, carrier, and mitigation estimates don't always align.

- You don't have time to manage the file: Claims work is slow, repetitive, and detail-heavy.

- You're already in a dispute: Once the insurer questions your numbers or compliance, presentation matters even more.

What a good public adjuster actually does

A capable public adjuster doesn't just fill in blanks on a form. They build valuation support, organize evidence, identify missed damage, align the claim with policy language, and present the package in a way that can survive scrutiny.

That's especially useful when the Proof of Loss is the leverage point for the rest of the claim. If the sworn statement is solid, later negotiations start from a stronger factual record. If the sworn statement is weak, later arguments often become defensive.

If you're weighing that choice, this guide on when to hire a public adjuster is a practical place to start.

The right time to get help is before the deadline forces a rushed submission.

If you're facing a Proof of Loss in Oregon or Washington and don't want to risk under-claiming, missing required support, or handing the insurer a weak sworn statement, NW Claims Management can help evaluate your claim and guide the next step. Their team represents policyholders, not insurers, and can help you prepare a documented, defensible claim package that protects your rights.