You walk outside after a storm and see shingles in the yard, granules in the gutter, and maybe a brown water stain spreading across the ceiling. Your first thought is simple. Will insurance cover a new roof?

Sometimes yes. Often no. More often than homeowners expect, the answer turns on details that were decided long before the storm hit.

That's why roof claims go sideways so often. Approximately 75% of residential homes in the United States are covered with asphalt shingle roofs, yet insurance companies pay for only about 30% of roof replacement claims involving these materials according to the data summarized from the Insurance Information Institute in this roofing discussion. That gap tells you something important. A damaged roof and a paid roof claim are not the same thing.

If you're stressed, start here. Don't guess. Don't let a roofer, neighbor, or call center rep tell you “insurance always covers storm damage.” It doesn't. But if the loss is covered and you document it correctly from day one, you give yourself a real shot.

Your Roof Is Damaged Now What

The first few hours matter more than most homeowners realize. People panic, call the first roofer who answers, and then assume the claim will sort itself out. That's a mistake.

When homeowners ask me whether insurance will cover a new roof, I tell them to stop thinking about replacement first and start thinking about proof. Insurance companies don't pay because your roof looks bad. They pay when the evidence shows a covered event caused sudden damage that the policy covers.

Start with triage, not assumptions

Do these things first:

Protect the house

If water is getting in, get a tarp or temporary dry-in from a qualified professional. Keep the invoice and photos.Photograph before cleanup

Take wide shots of the roofline, the yard, downspouts, gutters, attic stains, and anything blown off or broken.Check your policy documents

Pull your declarations page and endorsement pages. You need to know what form of coverage you bought.Create one claim folder

Put every photo, receipt, inspection note, email, and voicemail summary in one place. A simple digital folder works.

A practical starting point is using a structured property inspection checklist so you don't miss easy evidence while you're rattled.

Why the stakes are so high

Most roofs on homes are asphalt shingles. Most roof claims don't end in a full paid replacement. That's not because every insurer is acting in bad faith. It's because claims get denied for the same reasons over and over: the roof was old, the damage wasn't clearly tied to a covered event, the homeowner waited too long, or the file didn't separate storm damage from pre-existing wear.

Practical rule: Your claim gets stronger when your evidence answers the insurer's next objection before they raise it.

If you handle the first day badly, you hand the carrier an opening. If you handle it well, you force the conversation onto the facts.

Is the Damage from a Covered Peril

The first real test is simple. What caused the damage? Not when you noticed it. Not how expensive it is. Cause comes first.

Insurance coverage for a new roof is strictly contingent on the damage originating from a covered peril, such as wind, hail, fire, or falling debris, rather than wear and tear or neglected maintenance, as explained in Progressive's overview of roof damage coverage.

Covered peril versus excluded condition

Think about car insurance. If someone crashes into your parked car, that's a sudden event. If your car body rusts out over time, that isn't a collision claim. Roof insurance works the same way.

A storm ripping shingles loose can be covered. Old shingles curling, drying out, or failing at the end of their life usually aren't.

Common covered perils often include:

- Wind damage when gusts crease, tear, or remove shingles

- Hail impact when strikes bruise or fracture roofing material

- Fire damage from direct flame or resulting destruction

- Falling objects like tree limbs or debris

Common reasons carriers push back:

- Wear and tear from age and sun exposure

- Neglected maintenance like long-term leaks left unrepaired

- Rot or deterioration that developed gradually

- Installation defects from prior roofing work

The argument usually isn't about the leak

Most disputes aren't about whether water came in. They're about why.

A homeowner says, “The storm caused the problem.” The insurer says, “The roof was already failing, and the storm only revealed it.” That's where many claims die.

This is also why generic online advice falls short. If you want a contractor-side perspective on what homeowners should watch for, this guide with expert roof replacement advice is useful, especially if you compare it against your actual policy language and your own claim facts.

One page in your policy matters more than you think

Your declarations page and endorsements can tell you where the traps are. Some policies narrow roof coverage long before a claim is filed. If you haven't reviewed those limitations, read up on common insurance coverage gaps before you assume you're fully protected.

If the cause is excluded, the claim usually fails even when the damage is obvious.

That sounds harsh, but it's how these claims are decided every day.

Replacement Cost vs Actual Cash Value Explained

A lot of homeowners think approval means the insurer will pay for a brand-new roof. That's where the next shock hits. Coverage can be approved and still leave you with a painful bill.

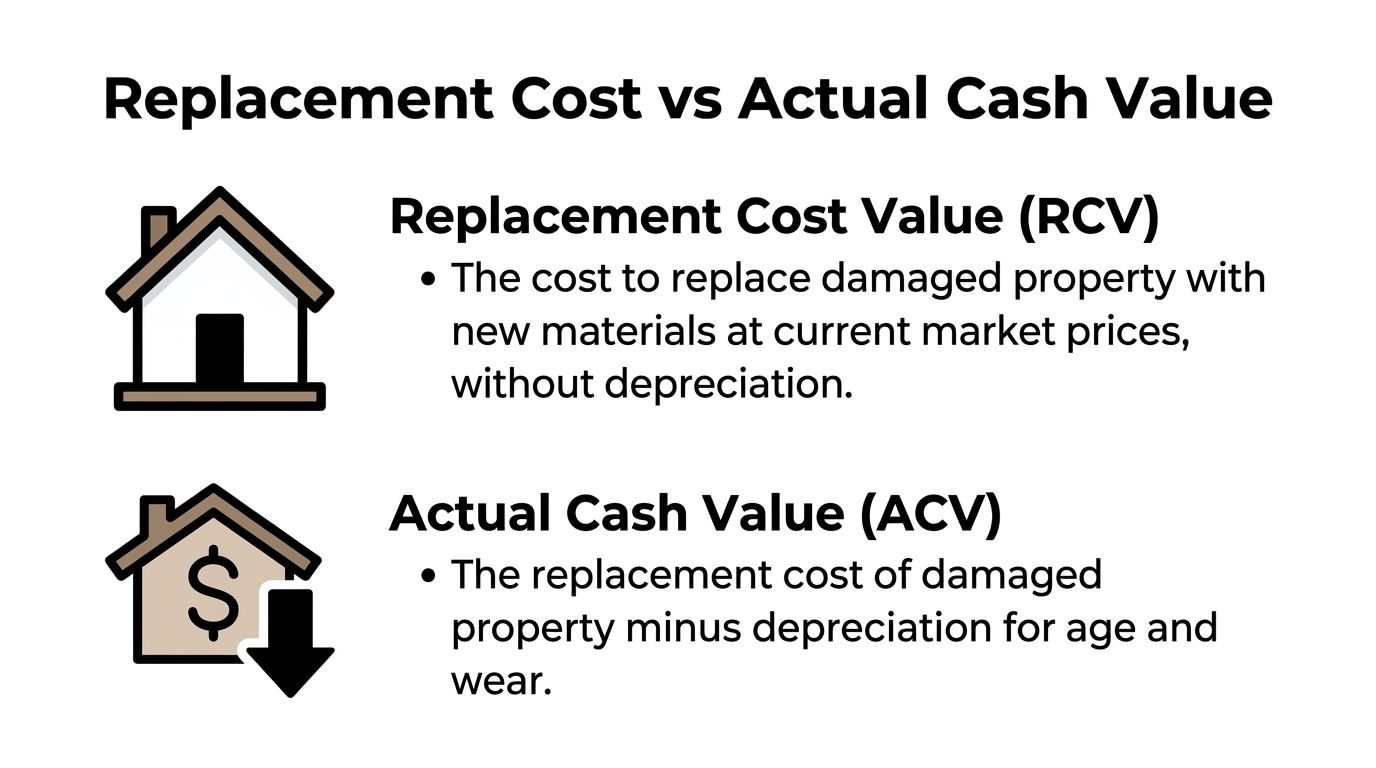

The reason is usually the difference between Replacement Cost Value and Actual Cash Value.

The laptop analogy

If your newer laptop gets destroyed in a covered loss, replacement cost is what it takes to buy a comparable new one today. Actual cash value is what that used laptop was worth right before it was damaged.

Roofs work the same way.

- Replacement Cost Value or RCV means the policy pays based on the cost to replace with new materials at current prices, subject to policy terms.

- Actual Cash Value or ACV means the insurer subtracts depreciation for age and wear.

That distinction can decide whether the claim feels manageable or financially brutal.

The age-depreciation trap

Many insurers now reduce roof payouts based on age. According to Texas Bay Credit Union's explanation of changing homeowner renewals, some policies cover only 40% of the replacement cost for roofs aged 16 to 20 years and only 20% for roofs over 21 years old under age-based tiers in certain cases, as shown in this summary of roof coverage changes on renewals.

Here's what that means in plain English. You can have real storm damage. You can have a covered peril. You can still get a settlement that feels nowhere near enough because the carrier values your older roof like a worn-out asset, not a new build.

What to look for in your policy

Don't skim. Look for these terms specifically:

| Policy term | What it usually means for you |

|---|---|

| Replacement Cost | Better settlement structure if the loss is covered |

| Actual Cash Value | Depreciation gets applied |

| Roof surfacing schedule | Separate limits for roofing materials |

| Loss settlement | Tells you how the carrier calculates payment |

| Endorsement | Can change standard coverage language |

A lot of estimate disputes also come down to software and pricing logic. If you're trying to understand how claim estimates are built, it helps to review tools tied to Xactimate pricing and estimating, because many carriers and adjusters rely on that format when valuing damage.

The question you should ask before arguing price

Don't start by arguing the contractor's estimate against the insurer's estimate. Ask this first:

Is the roof being valued under RCV or ACV?

If you miss that question, you can spend days fighting line items when the actual problem is the settlement method itself.

Watch this closely: A claim can be approved on cause and still underpay badly on valuation.

That's why homeowners often feel blindsided. They were focused on whether the claim would be accepted. They should've been focused on how the payment would be calculated.

Reading the Fine Print Deductibles and Code Upgrades

Even if you've cleared the cause issue and the valuation issue, your final payout can still shrink fast. Three policy details usually drive that surprise: deductibles, code upgrades, and cosmetic limits.

Deductibles can change the math fast

Most homeowners know they have a deductible. Fewer know whether it's a flat amount or a special wind or hail deductible tied to the type of loss. That matters because roof claims often involve storm events, and storm deductibles can hit harder than expected.

Read the declarations page carefully. Don't assume the deductible for a kitchen leak is the same deductible for a wind claim.

Code upgrades are real costs

Older roofs often trigger current building code requirements during replacement. That can involve underlayment, ventilation, flashing details, or other items that weren't part of the original roof system.

If your policy includes Ordinance or Law coverage, that may help with those added costs. If it doesn't, you may be paying the difference yourself even when the roof damage is otherwise covered.

Cosmetic exclusions can block leverage

Not every visible problem counts as payable damage. Some policies limit or exclude payment for cosmetic changes that don't impair function. That comes up often with metal roofing, but the principle can show up elsewhere too.

Use this quick scan before filing:

- Check the deductible line on the declarations page, especially for wind and hail.

- Look for Ordinance or Law wording if the roof may need code-related upgrades.

- Read endorsements for cosmetic damage language that narrows payment.

You don't need to become an insurance lawyer. You do need to know where the money can disappear.

Your Responsibilities After a Roof Is Damaged

An insurance policy isn't a one-way promise. It's a contract. Once damage happens, you have duties. Ignore them and you make the carrier's job easier.

Mitigate first

If rain is entering through the roof, stop the intrusion. Tarp the opening. Move belongings. Dry wet areas. Hire emergency mitigation if needed.

This isn't optional. If more water damage develops because no one took reasonable protective steps, the insurer may separate that later damage from the original event and refuse to pay for the avoidable portion.

Report promptly and keep your own record

Policies usually require prompt notice. They don't want a roof claim reported long after the weather event, when conditions have changed and the evidence is weaker.

When you call in the claim:

- Write down the claim number

- Record the date and time of every call

- Note the name of each adjuster or representative

- Summarize what they told you in a simple log

If the insurer asks for a formal statement of damages, learn what a proof of loss is before you sign or submit anything. That document can carry real consequences.

Don't create avoidable problems

Homeowners hurt their own claims in familiar ways:

- Waiting too long because they hope the leak will stop

- Throwing away damaged materials before documenting them

- Letting repairs start without clear records

- Relying on memory instead of written notes

The insured who keeps the best file usually stands on firmer ground than the insured who tells the best story.

That's not glamorous advice, but it's the truth. Claims are won with records.

How to Document Damage and File Your Claim

This is the part many individuals underdo. They take a few photos, file the claim, and expect the adjuster to figure out the rest. Then the carrier says the roof had pre-existing wear, the leak was long-term, or the storm didn't cause enough damage to justify replacement.

That isn't rare. As noted in this discussion of roof claim disputes, insurers often argue that the problem was pre-existing wear and tear rather than sudden storm damage, and many homeowners don't know how to document the difference effectively in roof replacement claim disputes.

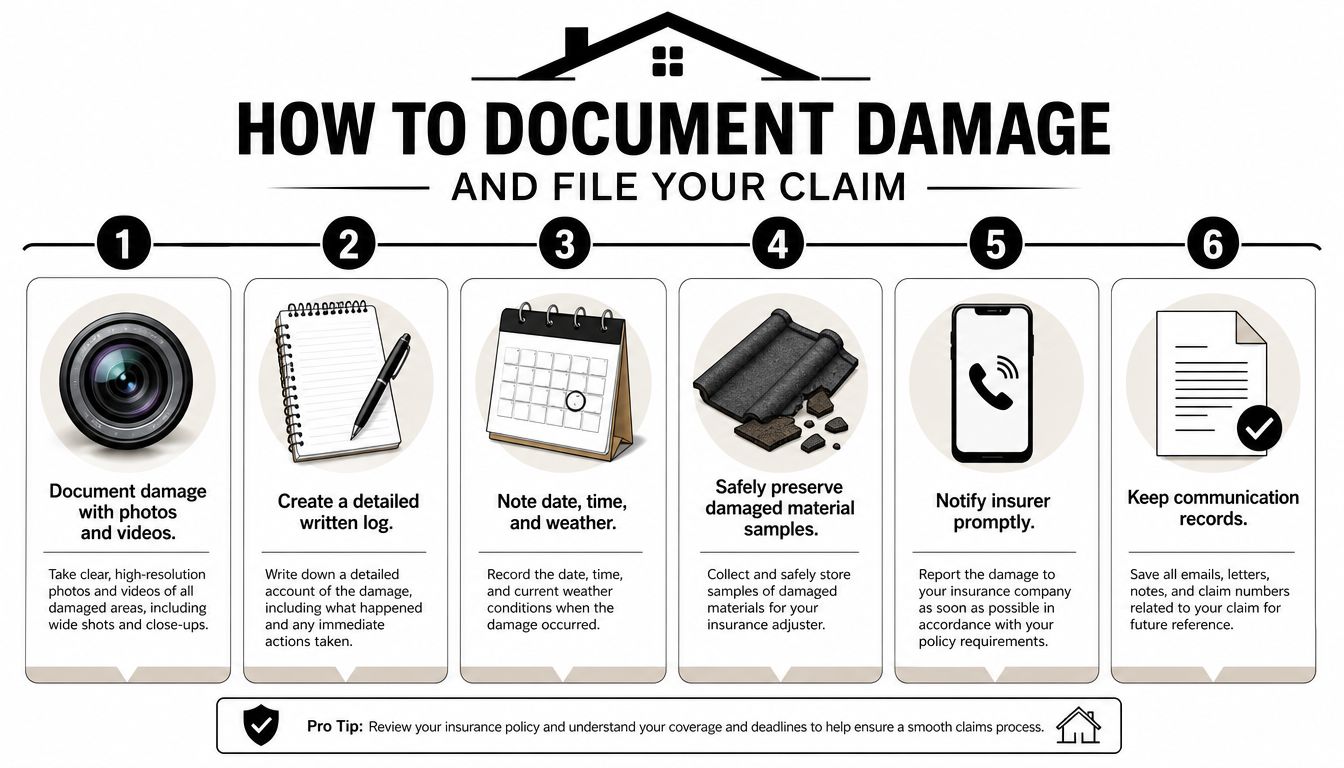

Build a sudden-loss record

Your job is to show a clean timeline. Not just damage, but new damage tied to a specific event.

Document these items immediately:

Wide exterior shots

Take photos of all slopes, ridges, valleys, gutters, downspouts, siding, screens, and soft metals. You want the full scene, not just close-ups.Ground evidence

Photograph shingles, tabs, granules, branches, and debris on the lawn or driveway before cleanup. Those details help anchor timing.Interior indicators

Capture ceiling stains, wet insulation, attic drips, and wall damage. Include wide shots and close detail.Weather timing

Write down the date and approximate time you discovered the issue and the storm event you believe caused it.

Don't just take photos. Take useful photos.

Bad claim photos are random and context-free. Good claim photos tell a story.

Use this sequence:

Start wide

Show the whole elevation or roofline.Move to medium range

Show the damaged area in relation to vents, chimneys, valleys, or gutters.Finish with close-ups

Capture creased shingles, lifted tabs, punctures, impact marks, or torn materials.Add scale

Place a ruler or common object nearby when safe and appropriate so the size of damage is clear.Take video

Walk the perimeter slowly and narrate what you're seeing, the date, and what happened after the storm.

Counter the pre-existing damage denial before it starts

The insurer's favorite argument is simple: “This wasn't new.”

So give them a harder file to dispute.

- Use before-and-after evidence if you have older home sale photos, maintenance records, inspection reports, or past contractor pictures.

- Separate old wear from fresh damage in your notes. Faded shingles are one thing. creased tabs or freshly torn seal strips are another.

- Preserve samples when safe if detached material is found on the ground and a professional says it can be retained.

- Ask roofing professionals for cause-focused observations instead of vague statements like “roof needs replacement.”

“Storm damage” is not enough. Tie the damage to what happened, when it happened, and where it happened.

File like you expect a disagreement

That mindset helps. Keep every communication in one log.

| What to keep | Why it matters |

|---|---|

| Claim number and adjuster names | Keeps the file organized and traceable |

| Emails and texts | Preserves exact wording |

| Inspection dates | Establishes timeline |

| Temporary repair receipts | Shows mitigation efforts |

| Contractor notes and photos | Supports scope and cause analysis |

When you file, be accurate and concise. Don't exaggerate. Don't speculate about things you haven't confirmed. Report the facts, attach your evidence, and keep control of your own copy of everything.

The homeowners who do this well don't leave the file empty and hope the insurer fills it in fairly. They present a claim package that already answers the obvious objections.

When to Hire a Public Adjuster Like NW Claims Management

Some roof claims are straightforward. Many aren't. If the insurer is dragging the file out, blaming age, under-scoping the damage, or paying far below what the loss appears to justify, you may need an advocate who works for you instead of the carrier.

A public adjuster represents the policyholder. Not the insurer. That distinction matters when the fight is about policy interpretation, damage scope, valuation, or the difference between old wear and sudden accidental loss.

When it makes sense to get help

Consider bringing in a public adjuster when:

The claim was denied

Especially if the denial leans on wear and tear, pre-existing damage, or lack of proof.The payment is too low

A small settlement doesn't mean the carrier is right. It may mean the file was under-documented or under-estimated.The damage is broad or complex

Multi-slope roofs, interior water intrusion, code issues, and mixed causes require tighter analysis.You're exhausted

That's a valid reason. Insurance claims are technical and time-consuming.

For a deeper read on the tipping points, review this guide on when to hire a public adjuster.

Why local experience matters in Oregon and Washington

Roof claims in Oregon and Washington often involve storm conditions, moisture issues, aging roof systems, and policy disputes over cause. Local experience matters because the details of damage presentation, contractor documentation, inspection standards, and claim handling expectations vary in practice.

A good public adjuster helps by:

- reviewing the policy language that controls payment

- documenting the loss in a way that addresses likely denial arguments

- organizing estimates, photos, reports, and communications

- negotiating directly with the insurer for a fairer result

You don't hire a public adjuster because you want a fight. You hire one because you want a professional record, a disciplined claim strategy, and somebody who knows what carriers look for when they limit or deny payment.

If you're still asking whether insurance will cover a new roof, the honest answer is this: it might, but only if the claim is built on the right facts, the right documentation, and the right reading of the policy.

If your roof claim in Oregon or Washington has been denied, delayed, or underpaid, NW Claims Management can review the loss, explain your policy in plain English, and help you decide the next move. A free claim evaluation gives you a clear read on whether the insurer's position is reasonable or whether it's time to push back.