The email or envelope arrives, you open the insurer's estimate, and your stomach drops. The damage in your home is obvious. The disruption to your family is obvious. But the number on the page looks like it belongs to a different property.

That reaction is common, and it doesn't mean you're overreacting.

An insurance estimate is not just a payment figure. It's the working blueprint for how your property will be repaired, what gets left out, what gets depreciated, and how much of the burden gets pushed back onto you. If the estimate is thin, stale, or incomplete, your settlement usually follows the same pattern.

In Oregon and Washington, I see the same problem over and over. Owners focus on the total at the bottom. The actual fight is usually buried above it, inside the line items, the repair assumptions, and the scope decisions that shape that total. If you can read those choices clearly, you can challenge them clearly.

Your First Look at the Insurer's Estimate

You open the estimate after a kitchen leak or wind claim, scan to the bottom, and the amount looks too low to put your house back the way it was. That reaction is usually accurate. The first estimate often reflects the insurer's initial scope, not the full cost of a proper repair.

Read it like a repair plan under review.

The biggest mistake I see in Oregon and Washington is owners treating the first estimate as settled fact because it arrived on insurer letterhead and uses contractor-style pricing. It is still a human-made document. If the adjuster missed damage during a brief site visit, relied on remote photos, used the wrong material grade, skipped code-related work, or assumed partial repair where full replacement is required for matching, the estimate will carry those errors all the way to the final number.

What that first estimate really is

A property estimate is a scope of repair translated into estimating software. In many claims, that means Xactimate line items, labor categories, and regional price lists. The software does not make the estimate fair. The person building the scope does.

That distinction matters.

I have reviewed plenty of estimates that looked polished and still left out debris handling, detach and reset work, permit-related tasks, code triggers, paint blending, or materials that are no longer available in a reasonable match. Those are not minor details. They decide whether the settlement pays for a real repair or a paper repair.

If you want to understand how Xactimate entries are built and why line-item choices affect payment, these Xactimate training resources can help you read the document with a more critical eye.

What to check before you respond

Start by requesting the complete line-item estimate if you only received a summary. Then compare it to the actual condition of the property, room by room and elevation by elevation.

Look at these points first:

- Missing areas: Every damaged room, slope, wall section, outbuilding, or affected system should appear somewhere in the estimate.

- Incomplete repair steps: Repairs often require protection, tear-out, disposal, drying-related work, cleaning, detach and reset, masking, texture, primer, paint, and finish work. If those steps are absent, the total is usually understated.

- Wrong repair method: Insurers sometimes price a spot repair where matching, uniform appearance, or manufacturer limitations point to a larger replacement.

- Code and permit gaps: Older homes in Portland, Seattle, Eugene, Tacoma, and similar markets can trigger code upgrades that never appear in the first draft.

- Remote-adjusting errors: Desk estimates built from a few photos often miss steep roofs, layered roofing, hidden moisture damage, trim profiles, insulation, and access issues.

- Off-site property needs: If contents were moved out during mitigation or repair, related protection and storage costs may belong in the claim. For owners comparing private coverage options, affordable storage unit insurance is a separate issue from what the property claim itself should pay.

One more practical point. Do not argue only about the total. Mark the exact line items, quantities, and omissions that are wrong. That is how estimate disputes get traction. A general complaint about the payout being too low is easy to ignore. A documented challenge that shows missing scope, wrong measurements, and unsupported repair assumptions is much harder for an insurer to brush aside.

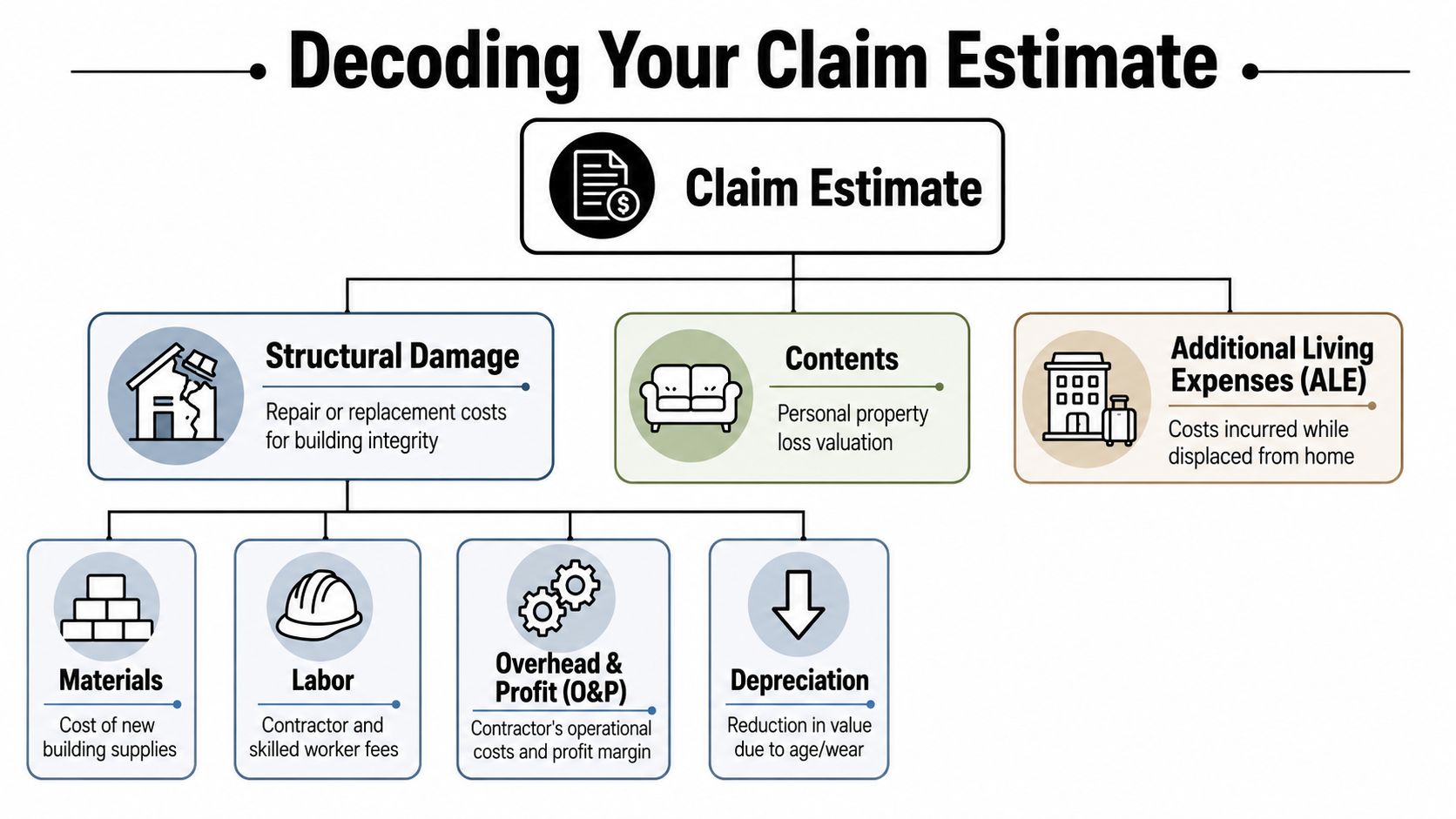

Decoding the Components of a Claim Estimate

A claim estimate should tell you exactly what is being repaired, how it is being repaired, and what the insurer is willing to pay for each step. If it does not do those three things clearly, it is not ready to trust.

Scope drives the entire estimate

The foundation is the scope of work. That is the room-by-room and trade-by-trade description of what was damaged and what proper repair requires. Xactimate or any other estimating platform can price line items fast, but software does not fix a bad scope. If the adjuster leaves out wet insulation behind a wall, detach and reset work around cabinetry, or code-triggered electrical updates, the estimate can look polished and still be wrong.

This is the part property owners in Oregon and Washington need to read slowly. Older housing stock, local permitting practices, and regional weather exposure create losses that do not fit neatly into a photo-only estimate. A short scope almost always produces a short payment.

The parts of the estimate that matter most

Several estimate components deserve close review because they affect value in different ways:

- Line items: Each task should be specific. "Replace drywall" is not enough if the job also requires insulation removal, vapor barrier work, texture, primer, and paint.

- Quantities and measurements: A correct unit price on the wrong square footage still underpays the loss. Check roof squares, linear feet of trim, flooring area, and paint surfaces.

- Material grade and type: Estimates often default to builder-grade materials. If your home had higher-grade finishes, custom profiles, or discontinued materials that create matching problems, the estimate should reflect that.

- Labor setup: Production rates and crew assumptions matter. Difficult access, steep roofs, occupied interiors, and protection of undamaged areas can increase labor time.

- Overhead and profit: On multi-trade losses, general contractor coordination is often part of the actual repair cost, not an optional add-on.

- Taxes, permits, and fees: These are easy to miss and expensive to absorb yourself.

- Depreciation and holdback: The insurer may issue an actual cash value payment first, then release recoverable depreciation later if the policy allows it and the repair is completed. This explanation of actual cash value versus replacement cost coverage helps if those numbers are causing confusion.

Owners often focus on the grand total first. I understand why. But estimate disputes are usually won much lower on the page, where the wrong quantity, missing trade, or cheap material assumption sits in plain view.

Where underpayment often hides

The problem is often not one dramatic error. It is a stack of smaller omissions.

One estimate may include drywall but omit insulation. Another may allow to replace a section of siding but ignore the fact that matching is impossible. Another may price interior painting for one wall even though the finish and sheen will force repainting a larger continuous area for a uniform result. In Oregon and Washington, code upgrade issues also show up often, especially in older homes and mixed-vintage additions.

Personal property logistics can also affect the claim. If contents must be packed out or stored off-site during mitigation or reconstruction, those handling and storage issues should be evaluated as part of the loss. Separately, some owners look into affordable storage unit insurance to protect belongings while the claim and repairs are still in motion.

A practical way to read the document

Read the estimate like a contractor who has to perform the job. Ask four direct questions:

- What exactly is being repaired or replaced?

- What steps are missing to complete that work properly?

- Are the measurements and material assumptions accurate?

- Does the estimate reflect local code, access, and matching realities?

If the answer to any of those questions is unclear, the estimate needs revision.

A sound estimate reads like an executable repair plan. A weak one reads like a rough draft with a price attached.

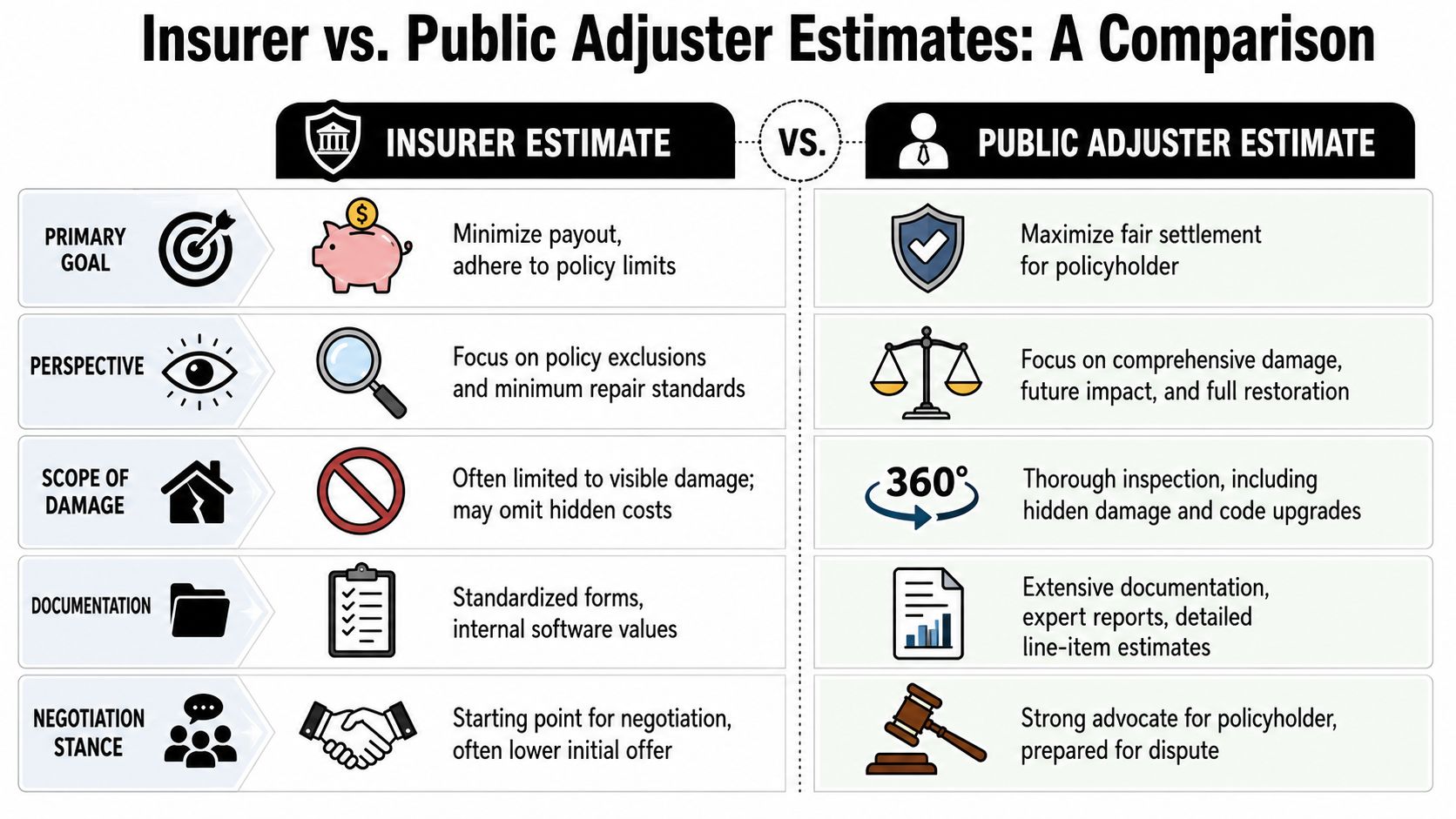

Why Insurer and Public Adjuster Estimates Differ

Two professionals can look at the same damage and produce very different estimates because they are doing different jobs for different clients. That's the heart of the issue.

Different mandates produce different estimates

The insurer's adjuster is there to evaluate the loss under the carrier's claim process and policy interpretation. In practice, that often leads to a narrower scope, a preference for visible damage, and conservative assumptions about what must be repaired or replaced.

A public adjuster works for the policyholder. The job is to document the full extent of damage, tie the damage to the policy, and defend a scope that reflects what proper restoration requires. If you want a straight comparison of those roles, this overview of a public adjuster vs. insurance adjuster lays out the distinction clearly.

The statistical problem behind severe losses

Insurers don't estimate losses by relying on simple averages alone. Claim data is often skewed and heavy-tailed, and one empirical study found that claim severity was best fit by a lognormal distribution while claim frequency was better modeled by negative binomial and geometric distributions. The practical takeaway is that severe, non-typical losses can distort expected-loss calculations, so baseline assumptions often struggle to capture major property damage accurately (empirical study on claim severity and frequency modeling).

That matters when your property loss isn't a tidy, average event.

A moderate kitchen leak is one thing. A fire with smoke migration, hidden heat damage, and code-triggered rebuild issues is something else entirely. The more your claim departs from a routine loss, the more documentation it usually takes to justify a fuller estimate.

Why contractor bids and public adjuster estimates aren't the same

Owners are often told to “get a contractor bid.” That can help, but it's not the same as a claim estimate prepared for negotiation under policy terms.

A contractor is usually pricing the work they expect to perform. A public adjuster is building and defending a claim presentation. That includes scope development, line-item review, policy application, and support for disputed items the carrier may resist.

A contractor answers, “What would I charge to do this job?”

A public adjuster answers, “What does this policy owe for this loss?”

Those are related questions, but they are not identical.

Common Insurer Tactics That Reduce Payouts

Most underpaid claims don't start with a dramatic denial. They start with a reasonable-looking estimate that causes an unstated narrowing of the job.

Methodology is where the money moves

Many estimate disputes aren't really about whether damage exists. They're about repair methodology. Public-facing industry commentary points out that insurers may price repairs without accounting for matching materials, local code-required upgrades, debris removal, or necessary contractor overhead, and that these omissions are a common hidden source of undervaluation, especially in older properties (discussion of estimate undervaluation methodology).

That's why a homeowner can stand in a clearly damaged room, look at a real estimate, and still be far short of what repairs will cost.

The line-item tactics I see most often

Some of the most common payout-reduction tactics include:

- Bundled repair entries: Instead of listing detach, prep, seal, texture, prime, and paint separately, the estimate collapses work into a simplified entry that doesn't reflect the actual sequence.

- Missing code-related work: The estimate pays for basic replacement but not the additional work local code requires once walls, roofing, wiring, or framing are opened up.

- No allowance for matching: The insurer prices a spot repair even when a partial replacement creates an obvious mismatch in adjoining materials.

- Outdated price assumptions: A stale price list or generic labor setup can understate current conditions, especially after regional storm losses.

- No overhead and profit where coordination is necessary: Multi-trade jobs often require management. Some estimates pretend they do not.

If you've dealt with a carrier estimate that felt polished but incomplete, this overview of common insurance adjuster tricks will sound familiar.

Remote adjusting creates a newer version of the same problem

Photo-based estimating and remote inspections can move claims faster, but speed has a cost. Hidden conditions don't show up well in app photos or quick video walk-throughs.

Watch for these gaps after a remote inspection:

- Moisture migration: Water moves behind walls, under flooring, and into insulation.

- Smoke and residue: Fire losses often require cleaning, sealing, and content handling beyond what visible charring suggests.

- Structural movement: Storm and impact claims can create alignment issues, roof decking concerns, and concealed openings.

- Roof detail losses: Flashing, underlayment, vents, and accessory items are easy to miss from ground photos.

If the inspection was remote, don't assume the estimate captures concealed damage. Remote tools are strongest on visible surfaces and weakest where the real repair cost often lives.

That's the pattern. The estimate sounds precise. The scope is narrow. The total follows the scope.

Your Action Plan to Verify and Dispute an Estimate

A low estimate doesn't fix itself. You need a disciplined paper trail. The good news is that organized policyholders often improve their position quickly because insurers increasingly use analytics, anomaly detection, and automated validation. Detailed, line-by-line support makes your dispute easier to process and harder to dismiss (insurance claims analytics and estimate validation overview).

Start with the full file, not the summary

Ask for the complete estimate in writing. You want every page, every line item, depreciation detail, and any supplemental revisions already created.

Then compare the estimate to the property itself, room by room. Don't review it in the abstract. Walk the house, building, or damaged area with the estimate in your hand.

Use this checklist as you review:

| Item / Area | Included in Insurer's Estimate? (Yes/No) | Is the Scope/Quantity Correct? | Notes (e.g., 'Missed drywall repair behind bookcase') |

|---|---|---|---|

| Kitchen | |||

| Living room | |||

| Primary bedroom | |||

| Hallway | |||

| Roof | |||

| Exterior siding | |||

| Flooring transitions | |||

| Insulation | |||

| Debris removal | |||

| Permit and code items |

Build a dispute file the adjuster can't ignore

Your dispute file should include:

Photos that match line items

Take overview photos and close-ups. Label them by room and issue.Measurements and counts

If a room size, roof area, cabinet count, or flooring quantity is off, note the difference clearly.Independent contractor scope

Don't ask for a one-page bid. Ask for a written scope with itemized work.Specific discrepancy notes

Write “missing detach and reset vanity” instead of “estimate too low.”Current supporting documents

Permits, prior renovation records, code comments, and specialist findings all help.

If you struggle to mark up documents clearly, even a general guide to efficient legal redlines can help you present estimate edits in a format that's easier for adjusters, contractors, and attorneys to follow.

Write the response like a business record

Your rebuttal letter should be calm and specific. Don't lead with anger. Lead with discrepancies.

A useful format looks like this:

- Opening: Identify claim number, property, and date of loss.

- Position statement: State that you dispute the estimate because scope and pricing are incomplete.

- Itemized corrections: List omitted or under-scoped items by area.

- Attachments: Identify photos, contractor scope, inspection notes, and supporting records.

- Request: Ask for reinspecton, estimate revision, or written explanation for refusal.

Field note: The strongest disputes don't say the insurer is dishonest. They show, line by line, why the estimate doesn't match the loss.

If the carrier still resists after you've documented the differences, that's when escalation starts to make sense. It may involve a reinspection, appraisal, legal review, or public adjuster representation. For owners who are already hitting a wall with the carrier, guidance on how to fight an insurance claim denial is also relevant because many underpayment disputes eventually turn into partial denials of scope.

One practical option at this stage is to have a public adjuster review the estimate and supporting documents. For example, NW Claims Management provides claim evaluation and estimate review for Oregon and Washington property losses, which can help identify whether the problem is pricing, scope, policy application, or all three.

When a Public Adjuster Becomes Your Strongest Ally

Some disputes are manageable on your own. Others aren't. The difference usually comes down to complexity, time pressure, and whether the insurer is engaging with your documentation in good faith.

The situations where self-management usually breaks down

A public adjuster becomes especially useful when:

- The loss is complex: Fire, major water damage, commercial losses, and multi-area storm claims produce layered scope disputes.

- Hidden damage is likely: Moisture intrusion, smoke residue, structural shifting, and concealed damage often require more than photos.

- The insurer keeps revising without resolving: Repeated small supplements can drag out the process while core scope issues remain untouched.

- You don't have time to manage the file: Claims become a second job fast.

- The dispute has stopped being about facts alone: Once the fight shifts to methodology and policy interpretation, many owners need professional help.

Industry and consumer reporting note that insurers are relying more on remote inspections and AI-assisted damage assessment, which can shorten claim cycles but also miss hidden damage. For conditions like moisture intrusion, smoke residue, or structural shifts, policyholders may need an independent inspection report to prove the full extent of the loss and counter a digitally derived, incomplete estimate (reporting on remote inspections and hidden damage issues).

Why this matters in Oregon and Washington

In Oregon and Washington, older housing stock, weather-driven losses, and local repair conditions often turn estimate disputes into scope disputes. The issue isn't always whether damage occurred. It's whether the insurer's chosen repair method will return the property to a proper condition under the policy.

Licensed public adjusters in both states operate under state rules and licensing requirements. That matters. You want someone who understands documentation standards, policy interpretation, and how to negotiate within the actual claim framework used by carriers here.

Fee structure and alignment

Most public adjusters work on a contingency basis. That means they're paid from the recovery rather than billing hourly while the claim is still uncertain.

For many owners, that alignment matters more than anything else. The adjuster has a direct incentive to document the loss thoroughly and pursue a higher fair settlement because the fee depends on the outcome.

If your claim is large, stalled, or technically disputed, bringing in a professional early can prevent months of avoidable under-scoping.

Frequently Asked Questions About Claim Estimates

Is the insurer's first estimate the final amount

No. It's often the starting point for review and negotiation. If the scope is incomplete, the amount can change through supplements, reinspection, appraisal, or formal dispute.

What should I ask the adjuster for first

Ask for the full line-item estimate, not just the summary. You also want depreciation detail and any revised versions already prepared.

Can I use my own contractor to challenge the estimate

Yes, but ask for a detailed written scope, not a lump-sum proposal. A contractor who only gives one bottom-line number won't help much in a line-item dispute.

What if the estimate includes the damaged area but still feels too low

That usually means the fight is over methodology. Look for missing prep, detach and reset work, matching issues, code items, waste, cleanup, or contractor overhead.

Should I accept payment while disputing the estimate

Often yes, but read the paperwork carefully. You don't want to sign anything that releases unresolved portions of the claim.

When should I stop handling it myself

Stop when the claim becomes too technical, too time-consuming, or too adversarial. Fire claims, large water losses, commercial losses, and hidden-damage disputes often cross that line quickly.

If you're in Oregon or Washington and the insurer's estimate doesn't match what your property needs, NW Claims Management can review the estimate, identify scope and pricing problems, and help you decide whether to dispute it yourself or bring in professional representation.