You open the mail, or the email alert hits your phone, and there it is: a claim denial letter. You already dealt with the damage, the cleanup, the photos, the forms, the waiting, and now the insurer is telling you no. That feels personal, even when it isn't.

I want you to treat that letter differently. A denial letter is often the insurer's first hard position, not the final answer. If you read it carefully, answer it methodically, and back your response with proof, you can push the claim back into motion.

Don't Let a Denial Letter Be the Final Word

A denial letter is often perceived as a closed door. That's exactly why insurers rely on them. The language is formal, the reasoning sounds settled, and the tone is designed to make you think there's nothing left to argue.

That mindset costs policyholders money. Nearly one in five in-network claims are denied, yet less than 1% are appealed. When people do fight back, up to 80% of appeals succeed, and 44% of internal appeals overturn the denial, according to Counterforce Health's denial statistics summary.

That should change how you read your claim denial letter.

Practical rule: A denial letter is not a verdict. It's the insurer stating its position based on the file it has, the interpretation it prefers, and the gaps it wants you to accept.

I've seen policyholders freeze after a denial because they assume the carrier has already done a complete and fair review. Sometimes that's true. Often, it isn't. Sometimes the file is thin. Sometimes the carrier is leaning on an exclusion without applying the full policy. Sometimes the denial rests on missing documentation that could have been supplied with one phone call.

A good response starts with one decision. Don't argue emotionally. Don't rant. Don't toss the letter in a drawer. Read it like a business document and answer it like someone who expects the insurer to justify every line.

What a denial really means

A claim denial letter usually tells you one of three things:

- The insurer says the loss isn't covered

- The insurer says the proof is incomplete

- The insurer says the amount or scope doesn't support payment

Those are very different problems, and each one requires a different rebuttal. If you lump them together, your appeal gets sloppy.

What to do today

Before you do anything else:

- Save the letter. Print it and keep the envelope if you got it by mail.

- Mark the date received. Deadlines matter.

- Start a claim file. Put every estimate, photo, email, and note in one place.

- Stop assuming the insurer is finished. They've made a move. Now you make yours.

You do not need to like this process. You do need to control it.

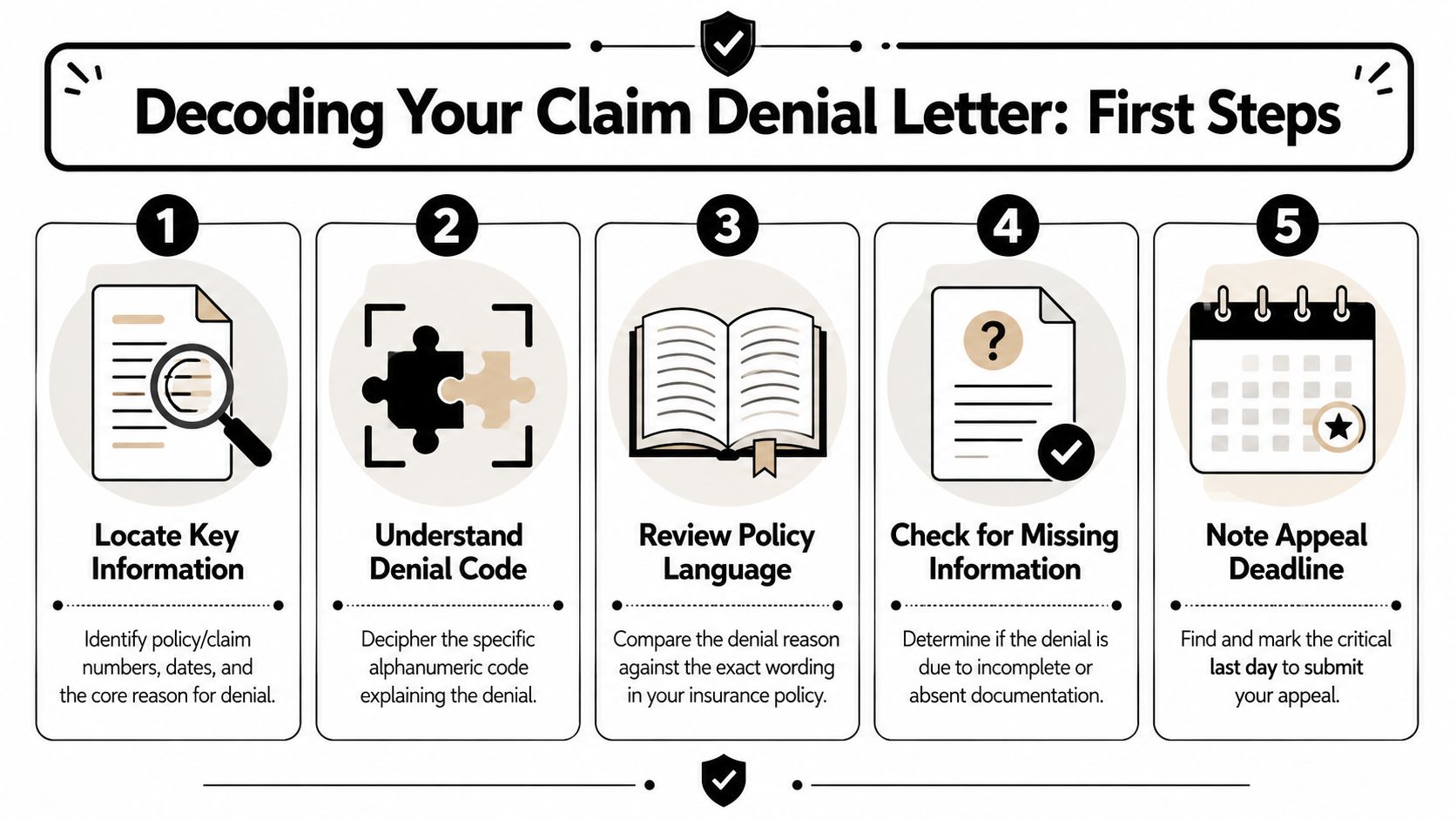

First Steps How to Decode Your Claim Denial Letter

Your claim denial letter is only useful if you strip it down to its parts. Right now, you're looking for facts, not tone. Find out exactly what the insurer said, what policy language it relied on, and what it claims is missing.

This visual gives you the quick version before you dig into the paperwork.

A legal analysis from Miller Friel puts it bluntly. Denial letters are often “written for the purpose of convincing corporate policyholders that they should not pursue a claim” and can be “fought and reversed” with a thorough analysis of facts and policy language, as explained in their discussion of insurance claim denial letters.

Pull out the core reason

Read the letter with a pen in your hand. Ignore the introductory fluff and find the sentence or paragraph that clearly states the basis for denial.

Look for language like:

- Not covered under the policy

- Excluded cause of loss

- Failure to provide requested documentation

- Damage predates the reported event

- Wear and tear, deterioration, neglect, or maintenance issue

- Late reporting or failure to protect the property

If you're dealing with fire-related losses, it helps to compare the denial language against common carrier arguments. This guide on reasons insurance companies deny fire claims is useful for spotting weak denial logic.

Match the denial to the policy

Once you identify the insurer's stated reason, go to the policy. Not the declarations page alone. The actual policy form, endorsements, exclusions, conditions, and definitions.

Create a simple comparison like this:

| Letter says | Policy says | Your next move |

|---|---|---|

| Damage is excluded | Check exact exclusion wording and exceptions | Test whether the insurer applied the exclusion too broadly |

| Proof is incomplete | Review duties after loss and document requests | Supply the missing items in organized form |

| Scope is overstated | Review valuation and covered damage terms | Support your scope with estimates, photos, and expert opinions |

This step matters because adjusters and claim examiners often summarize policy language in the denial letter. Your appeal should answer the actual policy wording, not their shorthand version.

Watch for a missing written denial

Some insurers slow things down by refusing to issue a clean written denial. That creates confusion on purpose. You can't rebut vague phone comments.

If you still don't have a proper denial document, take one of these steps in writing:

- Request the denial in writing and ask the insurer to identify the specific policy provisions relied upon.

- File a formal grievance or complaint through the insurer's process if they won't issue a letter.

- Ask for a benefit exclusion letter or equivalent written coverage position if they insist the issue is non-coverage.

- Submit a test claim or supplemental claim when appropriate to force a written adjudication.

Don't appeal a conversation. Appeal a document.

Your goal is simple. Turn an intimidating claim denial letter into a checklist. Once you know the reason, the policy basis, and the missing proof, the appeal becomes manageable.

How to Write a Powerful Appeal Letter

A strong appeal letter is not dramatic. It is organized, specific, and easy for a reviewer to approve. That's the standard.

Too many policyholders write angry letters full of conclusions and very few facts. That almost never works. Your job is to make the reviewer's path simple: identify the denial, quote the reason, answer it with evidence, and ask for a precise result.

A useful starting point is a structured rebuttal letter template that keeps your response focused on the denial language instead of your frustration.

Use a clean structure

The appeal packet should follow a disciplined format. AHIMA notes that a winning appeal packet mandates a one-page summary, labeled exhibits, and a letter of necessity. It also warns that failing to quote the insurer's specific reason for denial causes the appeal to lose focus. The letter should end with a clear request such as “I request reversal of the denial and approval of coverage,” as described in its step-by-step approach to resolving denials.

That structure works because it forces clarity.

Your appeal letter should include these parts:

Opening identification

State your name, policy number, claim number, property address, and date of loss.Statement of purpose

Say plainly that you are appealing the denial.Quoted denial basis

Quote or closely paraphrase the insurer's stated reason for denial.Point-by-point rebuttal

Answer the reason with facts, documents, and policy language.Exhibit references

Direct the reviewer to attached proof.Clear demand

Ask for reversal, coverage confirmation, payment, or reopening of the claim.

What to say in each part

Keep the opening tight. You're not writing a memoir.

Example opening:

I am writing to formally appeal the denial of Claim No. [number] under Policy No. [number] for the loss at [address] on [date of loss]. Your denial letter dated [date] states that the claim was denied because [insert exact reason].

That single paragraph does a lot of work. It identifies the file, pins down the insurer's position, and avoids vague argument.

Build your argument like a file review

The body of the letter should read like this:

- State the issue

- Cite the policy

- Present the evidence

- Explain why the denial fails

Here's a practical pattern:

| Step | What to include | Why it matters |

|---|---|---|

| Identify the denial point | Quote the exact denial reason | Keeps the appeal focused |

| Cite policy wording | Relevant section, condition, endorsement, or exception | Prevents the insurer from hiding behind summaries |

| Attach evidence | Photos, reports, invoices, timelines, expert opinions | Moves the dispute from opinion to proof |

| Request action | Reversal, payment, reconsideration, reinspection | Forces a decision, not a vague review |

If the carrier says the damage was pre-existing, answer with dated photos, contractor findings, repair history, and a timeline of the event. If the carrier says the loss falls under wear and tear, address the distinction between long-term deterioration and sudden covered damage. If the carrier says you failed to mitigate, show the emergency steps you took and the receipts that prove it.

Don't write like you're venting

The insurer doesn't need your outrage explained to them. They already know you're upset.

Use this tone instead:

- Firm, not hostile

- Detailed, not bloated

- Professional, not pleading

Avoid lines like “Your company is obviously trying to cheat me.” Even if that's what you believe, that sentence doesn't prove anything. Replace it with: “The denial does not account for the attached contractor findings and the policy language cited below.”

A good appeal letter sounds like someone who expects to be taken seriously, because they've done the work.

End with a specific request

Your closing should not say, “Please reconsider.” That's weak and invites delay.

Say what you want.

Examples:

- I request reversal of the denial and confirmation of coverage for this loss.

- I request that the claim be reopened and payment issued based on the enclosed estimate and supporting documentation.

- I request a written response addressing each point raised in this appeal and the exhibits attached.

Then add a deadline for response if appropriate under the claim process, and keep proof of delivery.

A powerful appeal letter does one thing well. It corners the denial into a smaller and smaller space until the insurer has to either pay, explain itself better, or expose the weakness in its own position.

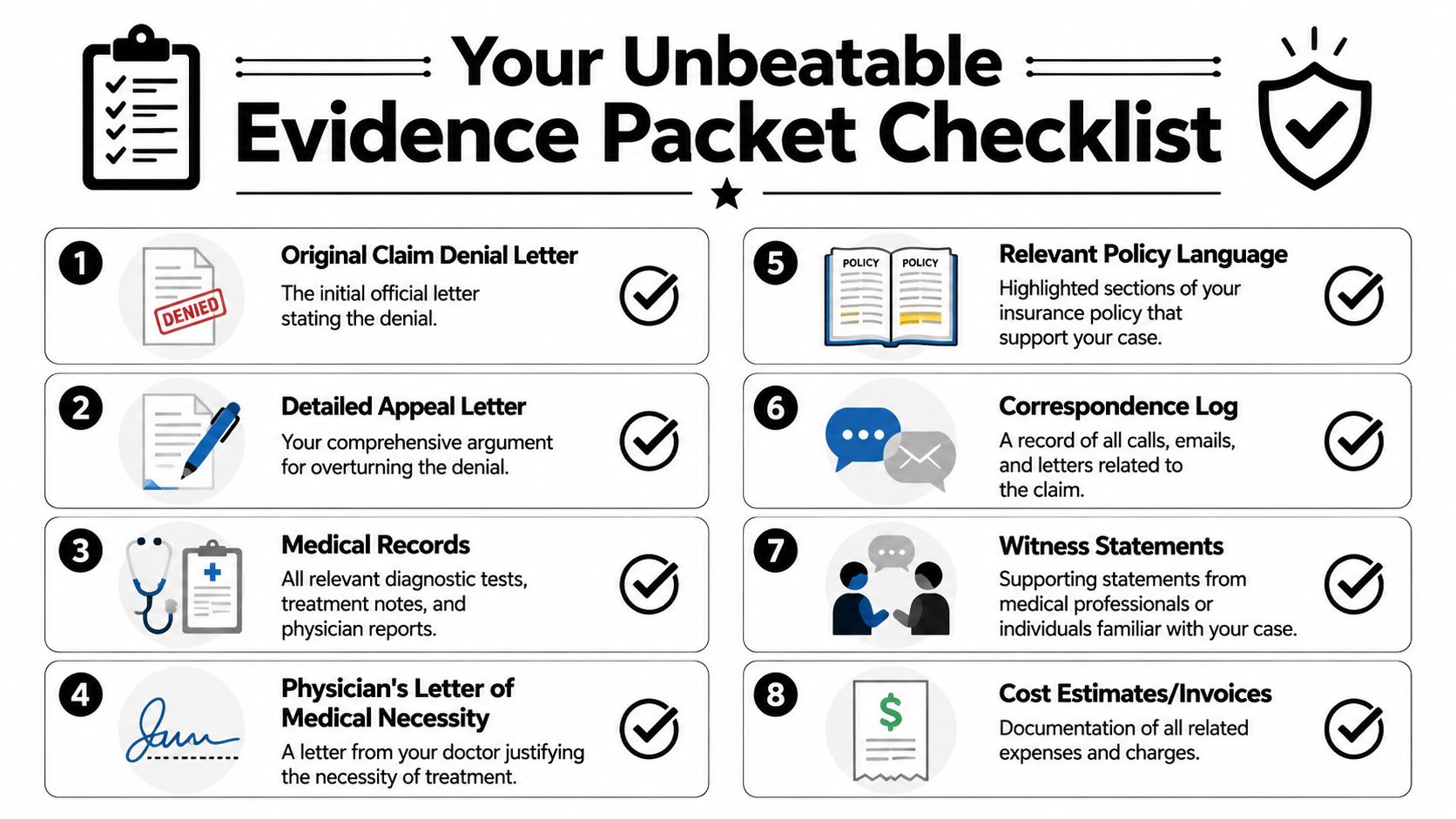

Building an Unbeatable Evidence Packet

Your appeal letter makes the case. Your evidence packet wins it.

If the file is thin, the insurer controls the narrative. If the file is organized and heavily documented, the insurer has to answer your proof point by point. That's where your influence comes from.

Medical billing guidance on appeals stresses that a successful appeal requires a thorough documentation packet including clinical records, physician notes, and authorization letters, and that the packet should be assembled within 48 hours of notification, with priority given to high-dollar claims, as outlined by Medical Billers and Coders. The same discipline applies to property claims. Fast, organized evidence beats scattered follow-up every time.

Use this checklist to build your file.

What belongs in the packet

- The original claim denial letter so the reviewer can see exactly what you're answering.

- Your appeal letter signed and dated.

- The relevant policy pages including exclusions, endorsements, definitions, and duties after loss.

- Photos and video showing the damage, the cause, and the condition before cleanup or temporary repair.

- Repair estimates and expert reports from contractors, engineers, roofers, mitigation companies, or other qualified professionals.

- Receipts and invoices for emergency services, temporary repairs, cleanup, lodging, or protective measures.

- A communication log listing calls, emails, inspections, and promises made by the insurer.

- Supporting inventories for damaged contents, which is where a solid personal property inventory template saves time and prevents missing items.

Make the packet easy to review

Don't send a stack of random documents. Label everything.

Use a sequence like:

- Exhibit A for the denial letter

- Exhibit B for the policy excerpts

- Exhibit C for photos

- Exhibit D for contractor estimate

- Exhibit E for receipts

- Exhibit F for timeline and communications log

That sounds basic, but it matters. Reviewers respond better when they can verify a point in seconds.

Include outside support when the damage is technical

Roof losses are a common flashpoint because carriers often reduce scope, blame wear, or separate covered storm damage from excluded conditions. If that's your issue, this guide on navigating roof damage claims is a practical companion for understanding what documentation and contractor input can strengthen the file.

The stronger your packet, the less room the insurer has to pretend the denial rests on uncertainty.

Build the file like someone else may have to review it later. That includes a supervisor, a regulator, an outside reviewer, or counsel.

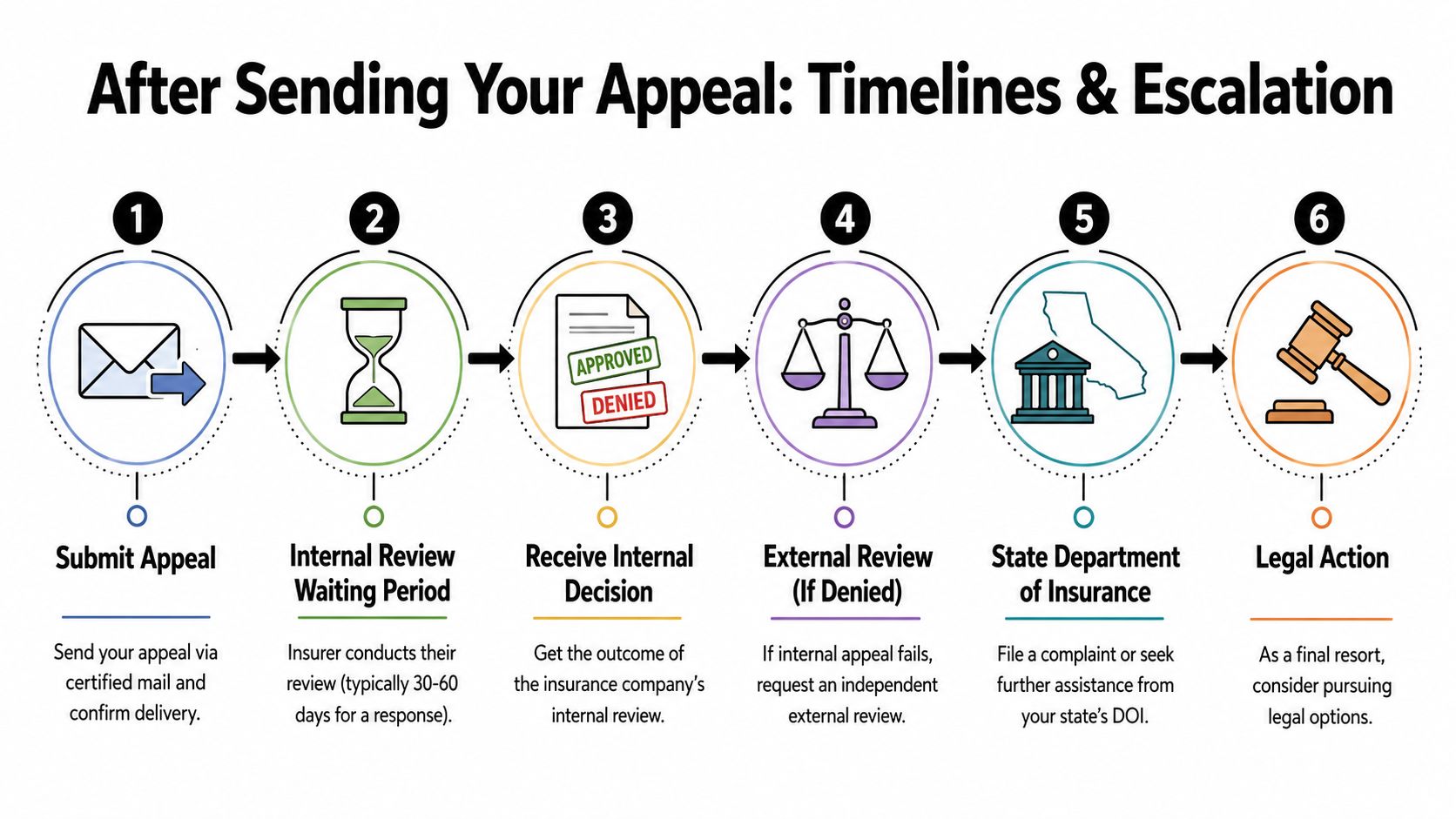

After You Hit Send Timelines and Escalation Paths

Once the appeal is out the door, most policyholders make one of two mistakes. They either sit and wait, or they start firing off scattered follow-ups with no tracking. Neither approach helps.

You need a controlled process. Track what was sent, how it was sent, who signed for it, and when the insurer responds. Persistence matters here. According to Etactics' summary of health insurance claim denial statistics, only 32.4% of denied claims are resubmitted by providers, and with an average denial rate of 17.3% in some plans, structured resubmission materially improves the chance of overturning the initial decision.

That principle carries over cleanly to property disputes. Organized follow-through beats passive waiting.

What to track after submission

Use a spreadsheet, claim diary, or a dedicated insurance claim management system to keep control of the file.

Track at least these items:

- Date appeal sent

- Delivery method

- Proof of receipt

- Reviewer or adjuster name

- Deadline for response

- Requests for more information

- Date of each follow-up

- Outcome of internal review

If you can't prove the insurer received your appeal, you've created a problem you didn't need.

Internal review and escalation

Most appeals start with an internal review. That means the insurer, or someone inside its review structure, looks again at the denial. Sometimes that leads to payment. Sometimes it leads to a revised denial with better wording.

If the denial stands, don't treat that as the end unless you've exhausted the next available path.

Here's the practical ladder:

| Stage | What happens | What you should do |

|---|---|---|

| Internal appeal | Insurer re-reviews its own decision | Demand a written response addressing your evidence |

| Supervisor review | A higher-level claims person reviews the file | Ask for reinspection if facts were missed |

| Complaint to regulator | You report claim handling concerns to the state | Submit organized documents, not general frustration |

| Legal or expert escalation | Public adjuster or counsel steps in | Use when the stakes or conduct justify it |

Stay disciplined when the carrier goes quiet

Silence is a tactic. So is repeated requests for documents you already sent.

When that happens:

- Resend the exact packet with a cover note identifying the prior submission date

- Ask the insurer to identify any remaining missing item in writing

- Pin every conversation to a date and name

- Request the current status and next decision point

If the insurer keeps moving the target, your records become part of the case.

Don't confuse delay with complexity. Sometimes a claim is complicated. Sometimes the file is just being slow-walked. Your notes will tell the difference.

When to Get Professional Help for Your Claim

Some denied claims can be fixed with a strong letter and a clean evidence packet. Others need outside help fast.

If the property loss is large, technical, or disruptive to your home or business, handling the appeal alone can become a second job. That's when policyholders start missing details, overlooking policy language, or accepting partial positions that shouldn't stand.

The red flags that tell me you need backup

Call in professional help if any of these are true:

- The loss is major. Fire, major water, storm, structural failure, or a business interruption claim is not the place to improvise.

- The denial cites multiple reasons. When the insurer mixes coverage arguments, scope disputes, and documentation complaints, the response needs strategy.

- The insurer keeps delaying. Repeated requests, vague status updates, or refusal to commit in writing are warning signs.

- Experts disagree. If your contractor says one thing and the carrier's field adjuster says another, someone needs to reconcile the evidence.

- You're exhausted. That matters more than people admit. A good claim response requires concentration and consistency.

What a public adjuster actually does

A licensed public adjuster works for the policyholder, not the insurance company. That means reviewing the policy, documenting the damage, organizing the loss, building the valuation, and negotiating directly against the carrier's position.

For denied or underpaid property claims, that work often includes:

- Reading the denial letter against the policy

- Identifying missing documentation or weak assumptions

- Coordinating estimates and expert support

- Preparing rebuttal materials

- Managing communication so the file stays on track

If you're trying to decide whether this is the point to bring one in, this guide on when to hire a public adjuster lays out the decision points clearly.

Don't wait for the file to get worse

In Oregon and Washington, property owners have another layer of pressure. The longer a dispute drags on, the harder it becomes to preserve clean evidence, tie damage to the original event, and keep repair costs from drifting upward.

You also have practical responsibilities. Homes need stabilization. Businesses need continuity. Nonprofits and public entities need documentation that can stand up to scrutiny from boards, auditors, and stakeholders.

That's why I'm direct about this. If the denial letter is tied to a substantial loss or the insurer is handling the file in a way that keeps you off balance, get experienced help sooner, not later. NW Claims Management is one option for Oregon and Washington policyholders who need someone to review the denial, document the loss, and manage the claim response from the policyholder side.

The right time to ask for help is when the denial still can be controlled, not after deadlines pass and the paper trail gets messy.

You don't need to hand over every claim. But you should stop handling it alone when the insurer has more time, more technical language, and a stronger grip on the process than you do.

If you're staring at a claim denial letter and you're not sure whether to appeal, escalate, or bring in help, talk to NW Claims Management. They work with Oregon and Washington policyholders to review denials, document losses, and respond with a fact-based strategy that fits the claim.