The check cleared. The contractor opened the wall or lifted the roof covering. Then the underlying problem showed up.

That's where a lot of property owners in Oregon and Washington get blindsided. The insurer says the claim was already handled. The contractor says the approved scope won't cover what the job requires. You're stuck in the middle, trying to figure out whether this is normal, whether you missed your chance, and whether you're about to pay out of pocket for damage tied to the same loss.

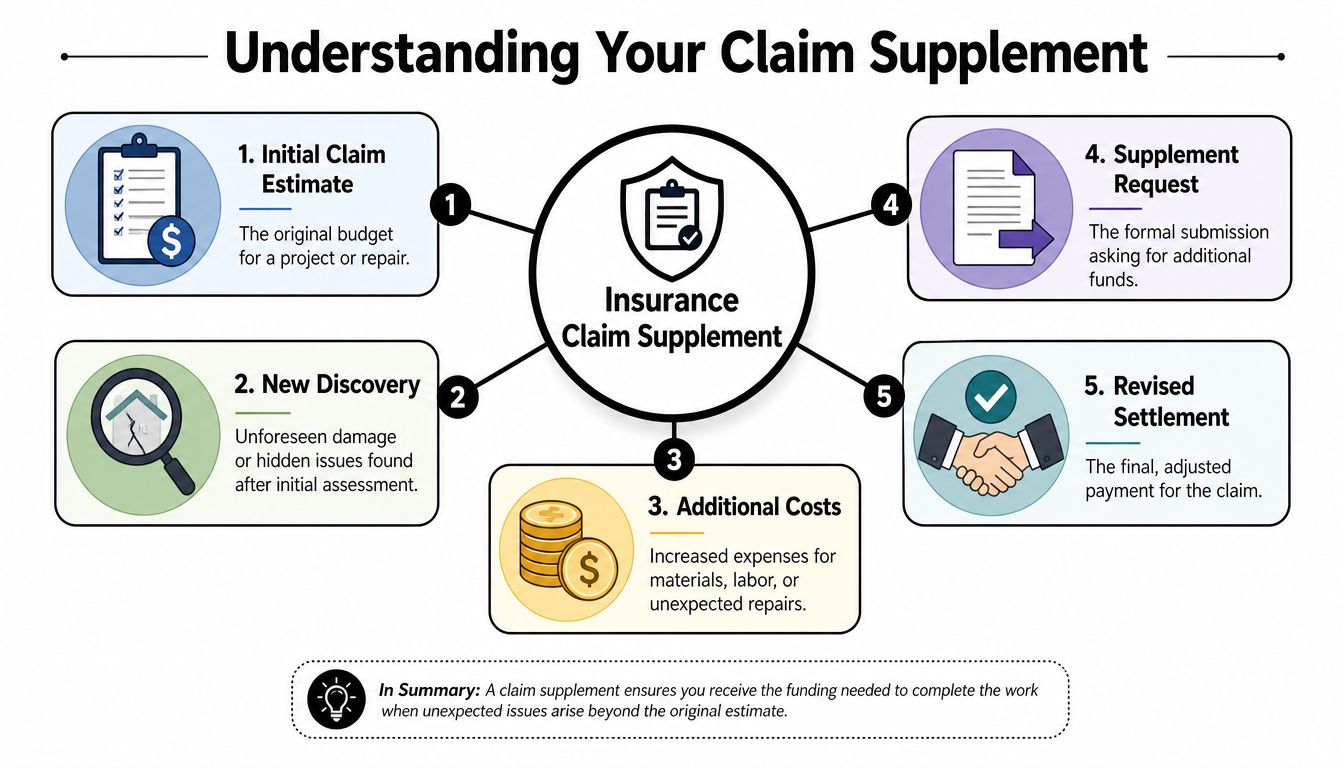

In many cases, the answer is straightforward. The claim may be paid, but it may not be complete. The tool used to correct that gap is an insurance claim supplement. It's a formal request to add covered items that were missed, unknown, or not yet visible when the original estimate was written.

Your Claim Is Settled But the Damage Is Not

A common version of this starts the same way. A wind or water loss hits the property. The carrier sends an adjuster, writes an estimate, and issues payment. At first, that feels like the hard part is over.

Then demolition starts.

The roofer finds damaged decking. The restoration contractor finds trapped moisture, damaged insulation, or electrical issues behind the wall. After a fire, cleanup reveals structural problems or contamination that nobody could confirm during the first inspection. Suddenly, the original settlement no longer matches the repair reality.

That isn't rare. It's built into the way many claims are first scoped. Initial inspections often focus on what is visible that day, under time pressure, before tear-out and before specialist trades weigh in. That's why undocumented hidden damage can change the financial outcome so sharply. The average property damage claim settlement is $13,804, and for fire and lightning losses it rises to $77,340, which is why missed supplemental damage can mean losing tens of thousands of dollars if it isn't properly claimed, according to 2026 insurance claim statistics summarized here.

The supplement is the fix

A supplement is the formal way to say: this loss is larger than the initial scope showed, and here is the proof.

It is not a favor request. It is not starting over. It is not asking the insurer to pay for upgrades unrelated to the covered event. It is a documented correction to the scope and price of repairs tied to the same date of loss.

Practical rule: If the contractor discovers new covered damage, stop treating the first estimate like the final word.

Homeowners get into trouble when they cash the first check and assume the file is closed for good. Claims can stay active for supplemental review if the added damage belongs to the same loss and you support it properly.

If you want to see why first estimates and actual repair scopes often diverge, this breakdown of insurance claim estimates helps explain where the shortfall usually starts.

What Exactly Is an Insurance Claim Supplement

Think of the original estimate as the first repair budget. The supplement is the formal change order.

It doesn't replace the claim. It amends it. The date of loss stays the same. The covered event stays the same. What changes is the scope of work and the amount required to return the property to pre-loss condition under the policy.

What a supplement is and what it is not

A proper insurance claim supplement adds items that were:

- Hidden at first inspection because they weren't visible until tear-out, moisture testing, or invasive inspection

- Required by code even though the carrier's original estimate omitted those items

- Incorrectly priced or mismatched when labor, materials, or product requirements were undervalued

It is not a second chance to add unrelated renovation work. It is not a way to slip in maintenance items. And it is not persuasive if the package says only that the contractor “needs more money.”

The three most common triggers

Hidden damage

This is the classic supplement issue. Roofing claims are a strong example. A roofing insurance supplement can recover an average of $7,000 to $8,000 per residential claim when line items, materials, or code-required components were missed in the original scope, according to this roofing supplement guide from licensed independent adjusters.

Once shingles come off, damaged decking, flashing issues, and other concealed conditions often become undeniable.

Code compliance

The insurer may estimate what was there. The contractor has to build what the local jurisdiction requires now. Those are not always the same thing.

If your city or county requires added underlayment, ventilation changes, electrical protection, or other code-driven work, the supplement must tie that requirement to the covered repair. In Oregon and Washington, local code adoption and amendment can matter a lot, especially on older housing stock.

Material mismatch and pricing gaps

Sometimes the issue isn't hidden damage. It's that the original estimate used the wrong material category, omitted necessary accessories, or priced the job in a way that won't support real restoration.

That's where itemized estimating matters. Broad complaints don't move claims. A line-by-line rebuttal does.

A supplement works best when it reads like a technical repair file, not an emotional appeal.

For a useful outside comparison of how a standard homeowners claim unfolds before supplement issues arise, see this guide to the Phoenix home damage claim process. And if a pricing dispute remains after supplement review, the home insurance appraisal process may become relevant depending on the policy language.

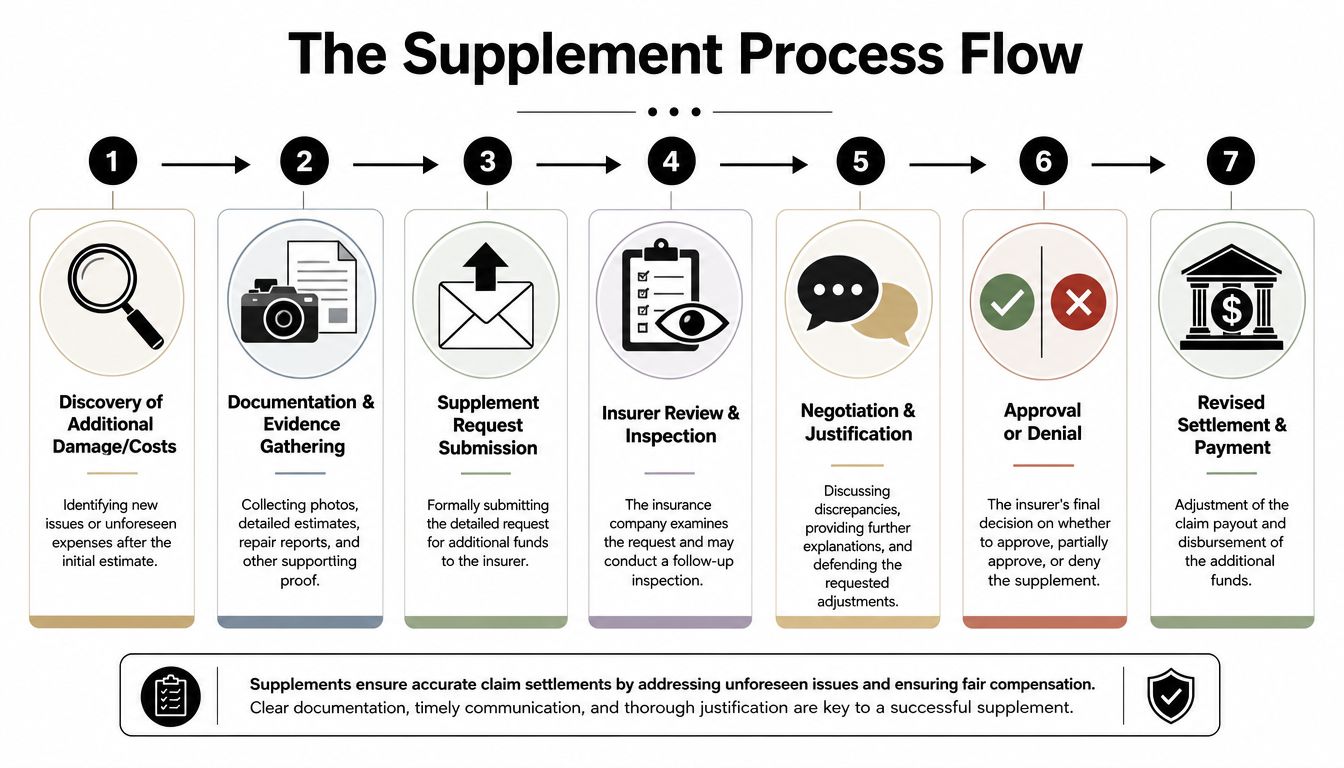

The Supplement Submission and Negotiation Process

Most supplement problems aren't caused by the damage itself. They're caused by poor sequencing. People call the insurer too late, submit half-built paperwork, or let the contractor and carrier argue without a complete written record.

The process works better when you handle it in order.

Step by step from discovery to payment

Give written notice immediately

As soon as new damage or added cost is confirmed, notify the insurer in writing that you are submitting a supplement tied to the original claim.Pause and preserve evidence

Don't let key conditions disappear before they're documented. If tear-out has begun, photograph every newly exposed condition before repair progresses.Get a detailed estimate

The supplement should come with an itemized estimate. In practice, many professionals use Xactimate because carriers recognize the format and line-item structure.Submit a complete package

Send the estimate, photos, code support if applicable, contractor notes, and a concise explanation tying the added scope to the original loss.Attend the reinspection carefully

If the carrier wants a second inspection, have the contractor or public adjuster present. Unrepresented reinspections often produce avoidable omissions.Negotiate line by line

Many supplements are won or lost during line-by-line negotiation. General statements like “the estimate is too low” don't help. Specific disputes over scope, quantity, pricing, and code support do.Confirm the revised settlement in writing

Once approved, verify what was accepted, what was denied, and whether depreciation, holdback, or invoice conditions still apply.

Sample email language

Use something simple and direct:

I am providing written notice that additional covered damage and repair costs have been identified under claim number [claim number] for the loss on [date of loss]. Please treat this as a supplemental claim request. We are gathering updated documentation, including a revised estimate, photos, and supporting repair information, and will submit the full package promptly.

That email matters because it creates a clean record of when the supplement was raised.

Timing matters, but don't assume Texas rules apply

Insurance codes often require insurers to acknowledge a written supplement within 10 to 15 days, accept or reject it within 15 business days, and issue payment for approved items within 5 business days, as outlined in this overview of supplemental insurance claim procedures. But homeowners in Oregon and Washington should be cautious about lifting timing advice from national articles without checking local applicability.

Where negotiations usually break down

A supplement negotiation usually fails for one of three reasons:

| Pressure point | What goes wrong | What works better |

|---|---|---|

| Scope | The added item isn't clearly tied to the loss | Show photos, contractor notes, and repair logic |

| Pricing | The carrier says the item is already included or overpriced | Respond line by line, not in broad totals |

| Causation | The insurer says it's wear, old damage, or separate loss | Anchor everything to the original event and repair sequence |

Keep the communication disciplined

Don't scatter documents across calls, texts, and verbal promises. Send organized emails. Label attachments clearly. Summarize calls in writing afterward.

If the back and forth starts stalling, this guide on negotiating with an insurance company is worth reviewing before you give ground on scope or price.

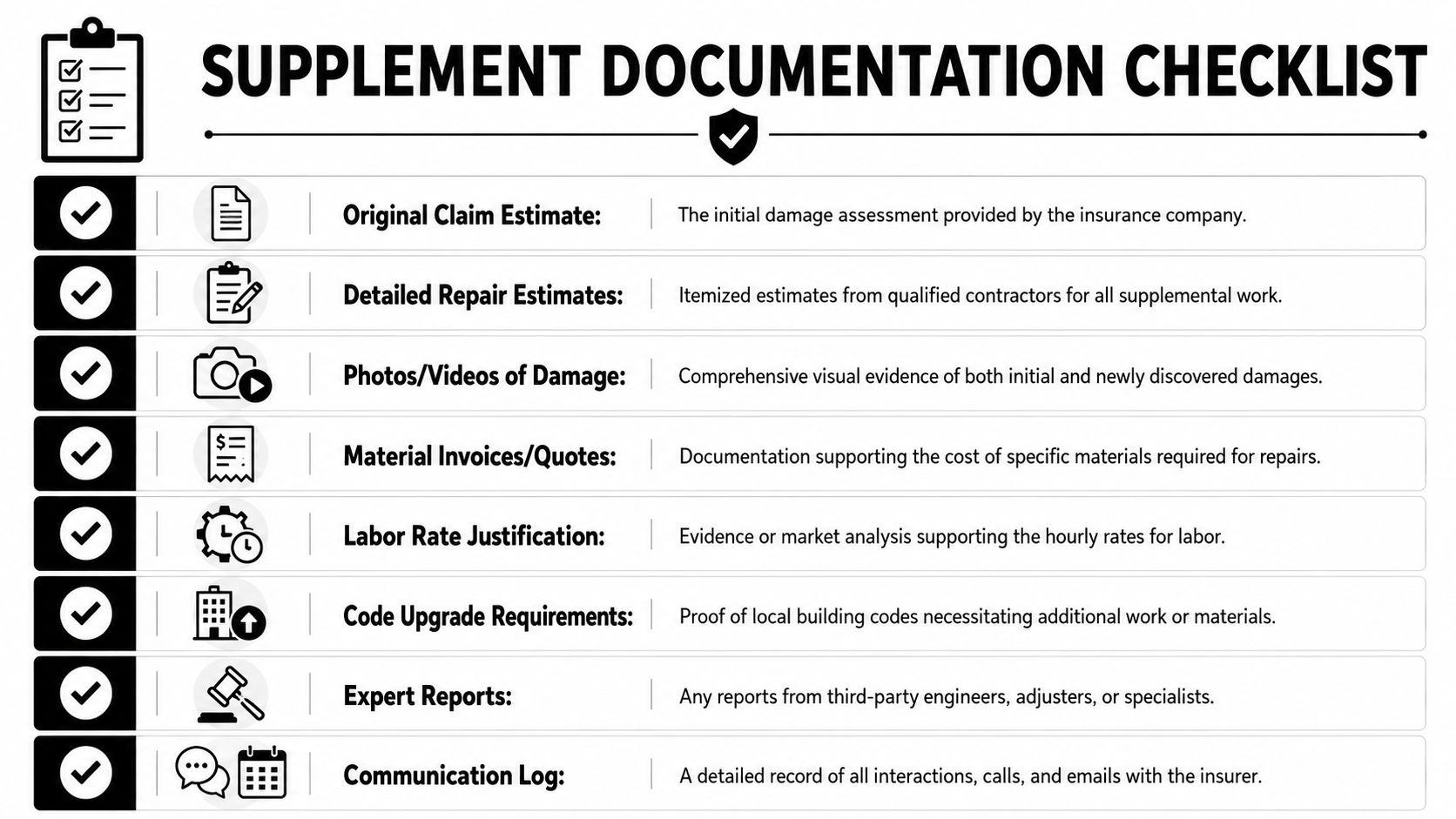

Your Essential Supplement Documentation Checklist

A supplement is only as strong as the file behind it. When owners lose these disputes, it usually isn't because the damage wasn't real. It's because the proof was thin, disorganized, or disconnected from the original loss.

Use the checklist below like a working packet, not a loose collection of photos.

What belongs in the file

Original carrier estimate

You need the baseline scope to show what was omitted, underpriced, or miscategorized.Revised contractor estimate

This should be itemized. Lump-sum bids are weak supplement evidence because they don't show exactly what changed.High-resolution photos and video

Show the damage in context, then close up. Wide shots establish location. Detail shots prove condition. If the issue appeared after tear-out, document that sequence.Annotated images

Mark arrows, labels, and room or elevation references directly on photos where needed. Adjusters move fast. Make the point impossible to miss.Code support

If the added item is code-driven, include the applicable local requirement or contractor documentation identifying the required repair standard.

The documents that separate a weak supplement from a strong one

Material quotes or invoices

These help support disputed product selections, specialty items, or nonstandard components.Written causation explanation

A short memo from the contractor, consultant, or other qualified party should explain why the newly discovered issue comes from the same covered event.Trade reports when needed

Electricians, roofers, mitigation firms, engineers, and specialty contractors often identify damage the original field inspection didn't capture.Communication log

Track every email, phone call, inspection date, and document submission. If the claim drifts, your timeline becomes evidence.

Bring order to the file before you bring emotion to the conversation.

A simple checklist you can print

| Item | Why it matters |

|---|---|

| Original estimate | Shows the starting point |

| Revised line-item estimate | Defines the supplement request |

| Photos before and after tear-out | Proves discovery sequence |

| Code documents or contractor code notes | Supports mandatory added work |

| Quotes and invoices | Supports pricing |

| Expert or trade reports | Strengthens causation and scope |

| Email log and call notes | Proves notice and follow-up |

One more issue gets overlooked all the time. Personal property losses can overlap with building damage documentation, especially after water or fire losses. If contents are part of the broader claim, a personal property inventory template helps keep that side organized without mixing it into the building supplement packet.

Common Insurer Tactics and How to Respond

Insurers don't review supplements casually. Fraud pressure is part of the reason. With insurance fraud costing the industry billions annually and nearly 10% of all claims estimated to be fraudulent, carriers scrutinize supplements closely, which is why legitimate claims need strong evidence, according to the NAIC-linked discussion summarized here.

That scrutiny doesn't mean your supplement is invalid. It means you should expect resistance and prepare for it.

Tactic one. Wear and tear

This is one of the most common positions. The insurer may agree there is damage, but argue the newly discovered condition was pre-existing deterioration rather than part of the covered event.

Your response should focus on causation and sequence.

If decking looked stable until the roof covering was removed and storm-related intrusion made the issue visible, document that progression. If a wall cavity shows water migration tied to the same leak path already accepted elsewhere in the claim, connect those points clearly. Don't argue in general terms. Tie each item to the date of loss and physical evidence.

Tactic two. Separate cause of loss

Another version is this: the insurer says the added damage comes from a different event, not the one already reported.

That argument gains traction when the file is sloppy. If your contractor discovered the issue during repair of the accepted loss, say so plainly and support it with dated photos, inspection notes, and written reporting. The supplement should tell a chronological story.

If the carrier can split the timeline, it can split the claim.

Tactic three. Code work labeled as an upgrade

Owners hear this constantly. The adjuster says, “That's betterment,” or “We don't owe for improvements.”

Sometimes that objection is fair. Sometimes it isn't. If the added item is required to complete covered repairs lawfully, then the issue isn't whether the building becomes newer. Repair work often has to comply with current standards. The argument has to stay grounded in what the jurisdiction requires and what the policy covers.

Tactic four. Low line-item pricing

This shows up in labor, materials, detach and reset items, access issues, and specialty work. The insurer may agree the item belongs, but price it below what the actual job requires.

Homeowners often lose patience and accept the shortfall. Don't negotiate from the total only. Challenge the estimate by individual line. Ask what pricing source was used. Ask whether the omitted tasks are included elsewhere. Get your contractor to explain why the selected line items don't match the actual repair.

Tactic five. Delay by document drip

Instead of denying the supplement outright, some carriers ask for one additional item at a time. Then another. Then another. The file never quite reaches decision stage.

You counter that by submitting a complete packet up front and confirming in writing what has already been provided. If a new request comes in, answer it specifically and ask whether the carrier now has everything needed to conclude review.

The right tone wins more than anger does

A supplement dispute is not the place for outrage-heavy communication. Firm beats furious. Specific beats dramatic.

Use language like this:

- Ask for position clarity by requesting the exact reason an item was denied or reduced

- Pin the dispute to documents by referring to photo numbers, estimate pages, and contractor notes

- Close each email with a decision prompt asking whether the carrier approves, partially approves, or denies the item

That approach puts the burden back where it belongs, on the claim decision.

Special Considerations for Oregon and Washington Claims

Property owners in Oregon and Washington run into a problem that many national guides gloss over. They read a supplement article based on Texas law, assume the same deadlines apply everywhere, and wait for a response window that may not govern their claim at all.

That misunderstanding causes delay.

The issue is straightforward. Many online guides cite strict 15-day insurer response windows tied to laws like the Texas Prompt Payment Act, but those timelines do not apply in Oregon or Washington, which leaves policyholders in those states with less clarity about when to escalate supplement delays, as noted in this discussion of how supplements are handled after insurance pays out.

Why this matters in the Pacific Northwest

In Oregon and Washington, the practical challenge is not that supplements are unavailable. It's that homeowners often don't know what delay is normal, what delay is strategic, and when silence turns into a consumer complaint issue.

That matters more after major storms, widespread water events, or regional claim surges, when adjusters are overloaded and files move unevenly. If you rely on a generic national countdown, you may either escalate too early without a complete file, or wait too long while the claim goes stale.

What owners should do instead

Use a documented follow-up rhythm.

- Send the supplement in writing with a full package or a clear notice that the package is coming

- Request confirmation of receipt and the name and contact information for the assigned handler

- Set your own follow-up dates rather than waiting indefinitely for the insurer to choose the pace

- Summarize every phone call by email so the file has a written timeline

- Ask direct status questions such as whether additional information is needed and when a coverage or payment decision should be expected

When to escalate in Oregon and Washington

If the carrier stops responding, keeps shifting handlers, or repeatedly requests information already submitted, start thinking in terms of regulatory and professional escalation.

In Oregon, property owners can contact the Division of Financial Regulation. In Washington, they can contact the Office of the Insurance Commissioner. Those offices aren't a substitute for claim preparation, but they can become important when communication breaks down or handling appears unreasonable.

Don't file a complaint as your first move. File it when your written record shows a pattern.

That record matters. A clean paper trail gives the regulator, and anyone later reviewing the claim, a concrete timeline of what was submitted and how the carrier responded.

When to Hire a Public Adjuster for Your Supplement

Some supplements are manageable with a strong contractor, a responsive adjuster, and clean documentation. Others turn into technical disputes over causation, code, pricing, scope, and policy interpretation.

That's usually the point where a property owner should stop trying to quarterback the whole process alone.

A public adjuster works for the policyholder, not the insurance company. On a supplement, that means organizing the loss file, reviewing the carrier estimate, building the revised scope, handling communications, attending reinspections, and pressing the negotiation until the claim reaches a defensible outcome.

Good reasons to bring one in

- The supplement is large or complicated because multiple trades, hidden damage, or code issues are involved

- The carrier is pushing back with repeated partial denials, causation arguments, or pricing reductions

- The claim has stalled and you're getting delay without a clear written position

- You don't have time to manage it while also trying to run repairs, work, family, or business operations

A practical threshold

If you're re-reading policy language at night, chasing contractors for paperwork, and getting vague insurer responses during the day, the claim has probably crossed from inconvenience into representation territory.

If you're weighing that decision, this guide on when to hire a public adjuster is a useful next step.

If your property claim in Oregon or Washington was paid but not fully scoped, NW Claims Management can help you evaluate whether a supplement is justified and how to pursue it properly. The firm represents policyholders only, handles residential and commercial losses, and works under Oregon and Washington public adjuster licenses. If you need experienced help documenting damage, organizing the supplement file, and negotiating for a fair payout, reach out for a claim review.