The fire is out, but the claim fight is just starting.

You are standing in a damaged home, trying to answer the same questions from the insurer, the mortgage company, the contractor, and your family. Then the denial letter arrives. Many policyholders read that letter as the final word. In practice, it is often the insurer's opening position, based on the documents it has, the timeline it built, and the parts of the policy it believes favor denial.

That distinction matters.

A fire claim denial usually turns on a handful of repeat issues: coverage status, application accuracy, exclusion wording, maintenance history, cause and origin disputes, occupancy rules, policy limits, and post-loss compliance. Some denials hold up. Others fall apart once the record is corrected, the timeline is tightened, or the carrier's reading of the policy is challenged with better evidence.

I have seen carriers deny claims over a billing error, a vague application answer, a missing inspection record, or a premature arson theory before the full fire investigation was finished. Those cases are won or lost on documents, experts, deadlines, and how early the policyholder takes control of the file.

That is the focus here.

If you are dealing with a denial in Oregon or Washington, generic tips will not help much. You need a working plan for each denial type: what the insurer is likely relying on, what evidence moves the claim, what to do before positions harden, and when to bring in a public adjuster, coverage counsel, an electrician, a fire investigator, or a forensic accountant. For a broader overview of denial issues, start with this homeowner's guide to denied claims.

The sections that follow are built as a public adjuster's playbook, with practical trade-offs, contest strategy, and state-specific considerations for Oregon and Washington policyholders who need to turn a denial into a fair review.

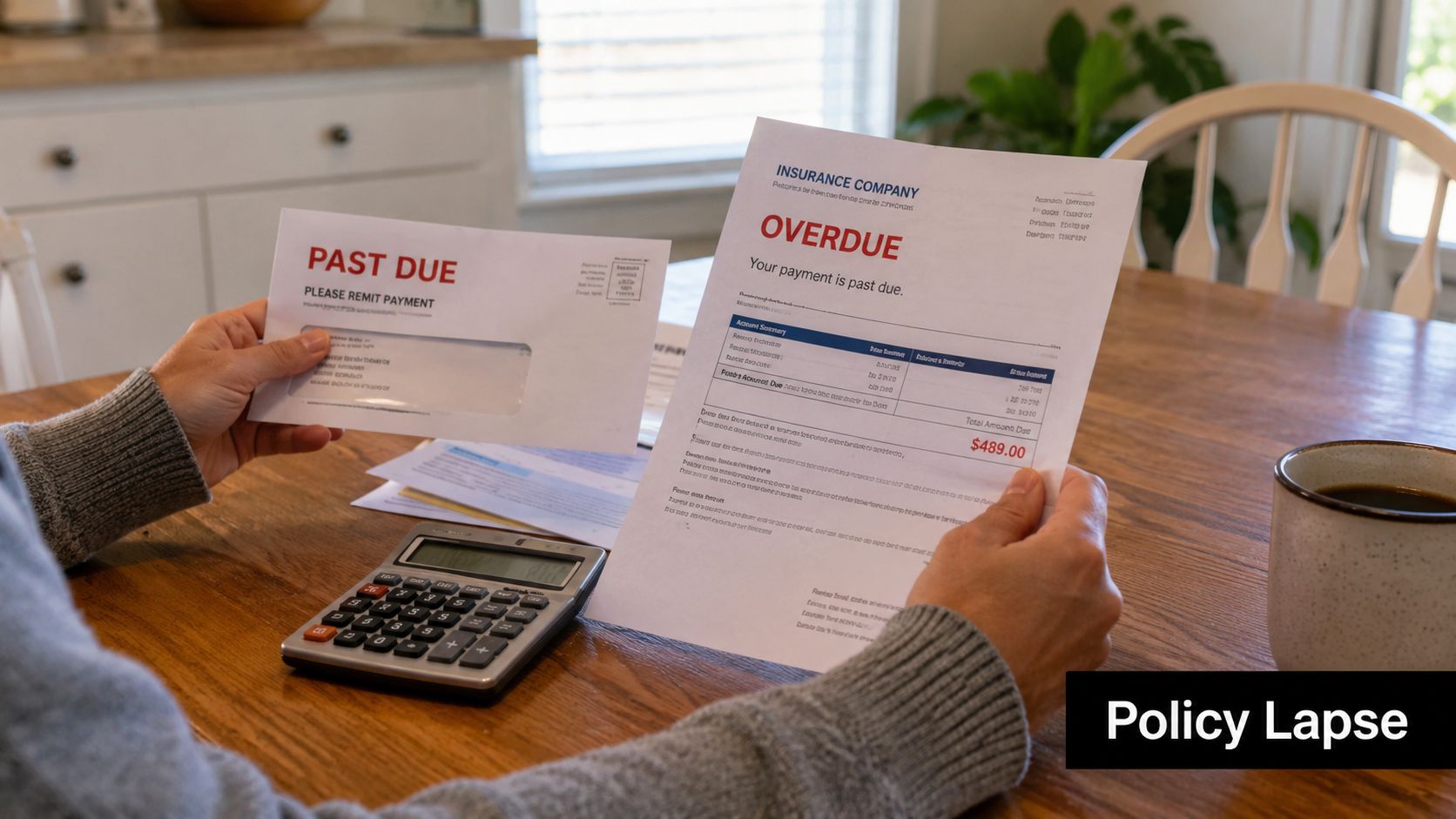

1. Policy Lapse or Cancellation at Time of Loss

This is one of the cleanest denial positions an insurer can take. If the policy wasn't active on the date of loss, the carrier will argue there was no contract in force, so there was nothing to pay under.

That sounds simple, but the actual dispute often isn't simple at all. I've seen denials tied to missed mail, failed autopay cards, mortgage escrow confusion, or a reinstatement that the policyholder believed was already effective. A homeowner may be only a few days behind and still face a full denial after a fire.

What the insurer usually looks for

The carrier will pull the declarations page, billing history, cancellation notices, and reinstatement records. If the timeline shows nonpayment before the fire, the denial letter almost writes itself.

Alliance Adjustment notes that a lapsed policy due to non-payment automatically voids coverage regardless of the fire's cause in many claim disputes, as discussed in its summary of why insurers deny fire claims.

What actually helps

You need the paper trail before you argue fairness.

- Pull payment proof: Bank statements, card statements, escrow records, and insurer receipts matter more than phone recollections.

- Request the full policy transaction history: Ask for cancellation, reinstatement, and notice logs, not just the denial letter.

- Check who was responsible for payment: If your mortgage servicer handled insurance, the servicing record may be central.

- Look for timing issues: If payment was accepted after cancellation, or the carrier sent conflicting notices, the denial may be less solid than it first appears.

Practical rule: Never argue coverage first if you haven't confirmed the effective dates. Date control wins these disputes.

For Oregon and Washington property owners, this is where a disciplined document review matters. If the lapse is real, your energy may be better spent on any available mortgagee protections, additional policies, or recovery against a responsible third party. If the lapse is questionable, challenge the timeline immediately and in writing.

2. Misrepresentation or Material Non-Disclosure on Application

A fire claim often triggers a second underwriting review. The insurer stops looking only at the loss and starts looking backward at the application. If they find a wrong answer, omitted condition, or outdated property description, they may claim the policy should never have been issued on those terms.

Policyholders often get blindsided. The issue may have nothing to do with what caused the fire. It may be a prior loss not listed, an unreported renovation, an incorrect occupancy description, or a property use the carrier now says it didn't insure.

Why this denial can be dangerous

Misrepresentation arguments can let the insurer attack the policy itself, not just one line item of damage. That gives them power far beyond a routine valuation dispute.

The strongest counter is usually the application file. Get a copy of what was submitted, what the agent entered, what was electronically signed, and whether the insurer inspected the property before accepting the risk. This is the core of post-claim underwriting issues, where carriers scrutinize old application answers after a major loss.

The public adjuster playbook

Start by separating innocent inaccuracy from material concealment. Those are not the same thing.

- Compare the application to reality: Roof type, square footage, occupancy, business use, prior claims, and renovations are common flashpoints.

- Identify agent involvement: If an agent completed the form and the insured didn't review a final version carefully, that fact can matter.

- Gather change records: Permits, contractor invoices, emails to the agent, and inspection reports can show disclosure or good-faith updating.

- Tie the dispute to materiality: Even if something was wrong, the insurer still has to support why it mattered to underwriting.

A typical scenario is a homeowner who converted part of a detached structure into living space, told the local contractor, told a broker casually, but never confirmed the policy was updated. After the fire, the carrier calls it a material omission. The response isn't outrage. It's documentation.

The best defense here is a complete file, not a loud explanation.

For Oregon and Washington claims, I push hard for the underwriting record early. If the insurer is using application language as a sword, they need to produce the exact question, the exact answer, and the exact policy consequence they say should follow.

3. Exclusions in Policy Language

Many policyholders hear "fire loss" and assume that ends the coverage question. It doesn't. Fire may be covered generally, while the insurer still argues that this specific fire, this building status, or this category of damage falls inside an exclusion or limitation.

That dispute often shows up in vacant property losses, intentional loss allegations, code-related conditions, or property classes that weren't scheduled as the owner believed.

Read the exclusion with the facts beside it

The insurer's advantage is that policyholders often read only the denial letter excerpt. That's a mistake. You need the full policy wording, endorsements, definitions, and any forms that modify the exclusion.

A common example is an insurer pointing to intentional loss language when there is an arson investigation. That doesn't mean the exclusion automatically applies. It means the carrier is positioning itself for a broader denial. This is especially important in losses involving suspected intentional fire setting, which is why understanding whether home insurance covers arson matters before you answer the insurer's theory with the wrong argument.

What works and what doesn't

What works is a clause-by-clause challenge. What doesn't work is saying, "But my house burned, so it should be covered."

Try this approach instead:

- Match each denial citation to the policy form: Make the carrier identify the precise wording it relies on.

- Check endorsements first: Endorsements often change base policy language.

- Look at definitions: Terms like "vacant," "residence premises," or "intentional loss" may be narrower than the denial letter suggests.

- Demand factual support: The insurer must connect the exclusion to evidence, not just suspicion.

In Oregon and Washington, exclusion fights often turn on details the policyholder can still prove after the loss: utility records, occupancy proof, inspection logs, photos, lease documents, and maintenance history. Exclusions are powerful, but only when the facts line up tightly with the policy wording.

4. Inadequate or Missing Maintenance Records

Sometimes the insurer doesn't say the fire wasn't real. It says you failed to maintain the property, and that failure either caused the fire or made the damage worse. This is common when there are allegations about wiring, detector maintenance, extinguishers, roof debris, or long-ignored repair issues.

These cases get personal fast. Homeowners hear "neglect" or "poor maintenance" as a moral accusation. From a claims perspective, it's an evidence fight.

The records that usually decide it

The insurer will ask whether smoke detectors were working, whether known electrical problems were repaired, and whether required safety measures were in place. Wallace Insurance Law notes that insurers often deny fire claims when they believe the policyholder failed to maintain adequate fire safety measures, including functional smoke detectors or repairs to faulty wiring, as explained in its discussion of fire claim denials tied to negligence and safety compliance.

If your answer is "I know we handled that," but you can't prove it, the carrier gains an advantage.

What to gather immediately

- Service invoices: Electrician work orders, panel upgrades, detector installations, chimney cleaning, HVAC service, and alarm maintenance.

- Purchase records: Receipts for smoke detectors, extinguishers, batteries, and monitored alarm systems.

- Photo history: Listing photos, family photos, remodel photos, or move-in photos often show detectors and general condition.

- Witness statements: Tenants, contractors, property managers, and neighbors may confirm recent upkeep.

A real-world version of this is a rental house with an older panel and prior tenant complaints about flickering lights. If the owner repaired the issue but can't find the electrician invoice, the insurer may characterize the property as knowingly unsafe. If the owner can produce the invoice, the story changes.

Maintenance arguments weaken quickly when the file shows a pattern of repairs, inspections, and safety checks.

For Oregon and Washington owners, wildfire interface properties and older housing stock can make maintenance a recurring issue. Don't wait for the insurer to define your property condition for you. Build that timeline yourself.

5. Misclassification of Fire Cause or Arson Allegation

Arson allegations are among the most serious reasons insurance companies deny fire claims. Once the insurer suspects intentional loss or fraud, the whole claim changes tone. Every inconsistency gets magnified. Every delay looks suspicious. Innocent errors start getting treated as deception.

The problem is that cause investigations are not infallible. A fire can be ruled undetermined by public authorities while the insurer still leans toward incendiary origin. Or an accidental electrical event gets framed as suspicious because the burn pattern is complex.

How to answer a cause dispute

The first move is not to argue with the field adjuster. The first move is to obtain the entire cause-and-origin basis for the denial or reservation of rights.

That means fire department reports, scene photographs, laboratory results if any exist, recorded statements, and the insurer's expert materials. If the carrier has launched a deeper technical review, you need to understand what a forensic investigation involves before responding.

Evidence that changes the file

When arson is implied, I want parallel evidence, not just rebuttal language.

- Scene records: Fire department reports, dispatch logs, and suppression notes.

- Independent expert review: A qualified origin-and-cause expert can challenge unsupported conclusions.

- Timeline proof: Phone records, work records, travel receipts, video, and witness accounts establishing whereabouts.

- Financial context: If the insurer is hinting at motive, be ready for document requests and answer them carefully.

Allied Public Adjusters reports that three major California insurers denied nearly half of submitted fire claims in 2023, with documentation gaps and late filing cited as major drivers in those denials, according to its analysis of common fire claim denial reasons and proof-of-loss problems. In practice, arson-suspicion claims often overlap with those same file weaknesses. Once the carrier distrusts the claim, missing records become even more damaging.

For Oregon and Washington policyholders, don't guess your way through an arson-related examination. If intentional loss is on the table, treat every submission as if it may later be reviewed by experts, counsel, and regulators.

6. Occupancy Status Violations

A property doesn't have to be abandoned to trigger an occupancy dispute. It may be vacant too long, between tenants, under renovation, seasonally unused, or only partially occupied. Those facts matter because many policies treat vacancy and unoccupancy as coverage-limiting conditions.

This catches people who assume "I still own it" means "it's still covered the same way." It often isn't.

Where these disputes come from

A house listed for sale after a move, a rental waiting on a new tenant, a cabin unused for part of the year, or a commercial building closed during repairs can all invite scrutiny. The carrier will look at utility usage, mail delivery, lease records, security footage, neighbors' statements, and inspection notes.

If the policy required notice of extended vacancy and that notice wasn't given, the insurer may deny the loss outright or apply reduced coverage language.

The practical response

Occupancy disputes are won or lost on ordinary records most owners don't think to preserve.

- Show active use: Utility bills, internet service, alarm logs, cleaning invoices, property manager visits, and delivery records help.

- Show insurer notice if it happened: Emails to the agent, endorsement requests, and renewal discussions matter.

- Show protective measures: Boarding, locks, cameras, winterization, and caretaker visits support responsible management.

- Check the exact wording: Some policies define "vacant" and "unoccupied" differently. That distinction can be critical.

A common Washington scenario is a mountain property used part-time and left empty between stays. A common Oregon scenario is a Portland rental turning over after tenant move-out. In both, the carrier may overstate what "vacant" means. The answer is not to rely on common sense. The answer is to prove actual status against the policy definitions.

If the insurer says the building was vacant, make them prove the policy definition, not just the appearance of emptiness.

7. Uninsured or Underinsured Property

The fire is out. The carrier accepts coverage. Then the estimate comes back and the numbers do not work. The dwelling limit is too low, the detached shop was never properly scheduled, or upgraded finishes are being valued like builder-grade materials. Policyholders often experience that result as a partial denial, even when the insurer says the claim is "covered."

I see this after remodels, additions, rising construction costs, and long renewal cycles where no one revisits the replacement cost assumptions. Oregon and Washington owners run into it often after basement conversions, ADU work, shop improvements, and code-driven rebuild issues that push costs well beyond older limits.

Why this problem is different from a straight denial

Underinsurance cases require a different strategy. The central question is usually not whether the fire happened or whether the policy was active. The question is whether every part of the damaged property was insured correctly, valued correctly, and placed in the right coverage bucket.

That distinction matters.

A carrier may be right about the stated limit and still wrong about how it applied sublimits, endorsements, depreciation, debris removal, ordinance and law coverage, or personal property classifications. Before accepting a short payment, compare the policy to the property as it existed on the date of loss. Insurance coverage gaps often become visible during that review.

The practical response

Start with the declarations page and build outward.

- Check each coverage line separately: Dwelling, other structures, business personal property, contents, loss of use, debris removal, and ordinance or law may all respond differently.

- Review endorsement language: Extended replacement cost, guaranteed replacement cost, inflation guard, increased limits for recent improvements, and scheduled property can change the outcome.

- Match the insured description to the property: Finished basements, converted garages, detached structures, custom cabinetry, upgraded electrical, and added square footage are frequent trouble spots.

- Document pre-loss condition and upgrades: Permits, contractor invoices, photos, appraisal updates, real estate listings, and financing records help establish what was there.

- Press allocation issues: Even when the main building limit is capped, a careful allocation across dwelling, other structures, contents, and debris removal can reduce the uncovered gap.

Agent communications can matter too. If the owner reported renovations, requested higher limits, or relied on specific advice during renewal, preserve those emails and notes. That does not guarantee recovery, but it can change the conversation, especially if the file shows the insurer or agent had notice of material upgrades.

A common Washington dispute involves a home with a finished daylight basement and high-end interior updates that never made it into the replacement cost worksheet. A common Oregon dispute involves older homes in Portland or Eugene where current code upgrades make rebuilding far more expensive than the original limit anticipated. In both situations, the path forward is evidence, not frustration. Build a valuation file, compare it against the policy wording, and challenge any coverage position that lumps everything into one exhausted limit without analysis.

If the insurer says the payment is all the policy allows, ask for the estimate, the valuation assumptions, the endorsements relied on, and the exact policy language supporting each cap. Then compare that to your own scope and pricing. This guide on what to do after a house fire for insurance purposes helps policyholders organize that record early, before key proof gets lost.

For readers trying to understand reconstruction math, these property insurance valuation insights help explain why policy limits and rebuilding costs drift apart.

8. Failure to Comply with Policy Conditions or Post-Loss Requirements

The house is burned, the family is out of the home, and the insurer is already asking for a recorded statement, an inventory, mitigation receipts, photos, and a sworn proof of loss. Then the denial letter arrives. It does not say the fire was excluded. It says the claim file was late, incomplete, or noncooperative.

I see this denial category often because post-loss duties are easy to underestimate and easy for carriers to weaponize. A valid fire claim can stall if notice was delayed, inspections were missed, damaged property was discarded too early, or the proof of loss was never submitted in the form the policy required.

The practical issue is prejudice. Insurers often argue that a policyholder's delay or incomplete response prevented a proper investigation. That argument does not win automatically in every dispute, especially in Oregon and Washington, but it becomes much harder to fight if the file is disorganized.

Start with the policy itself. Read the sections on "Duties After Loss," "Your Duties," "Proof of Loss," and any cooperation language. Then build a deadline list the same day. This step alone prevents many avoidable denials.

A working file should include:

- Prompt written notice: Report the loss immediately and save the claim confirmation, email, and claim number.

- Protection of the property: Board up openings, dry wet areas if safe, and keep invoices, photos, and dates for every mitigation step.

- Inspection control: Give reasonable access, but document who inspected, when they came, and what areas or items they examined.

- Inventory support: List damaged contents room by room, with age, condition, and replacement information where possible.

- Proof of loss tracking: If the insurer requests a sworn proof of loss, calendar the deadline and confirm whether an extension is needed in writing.

- Communication log: Keep one running record of every call, request, document submission, and unanswered insurer question.

Do not submit rough numbers just to fill the silence. Incomplete inventories and guessed values create credibility problems that can follow the claim for months. It is better to submit a supported partial inventory with a written note that supplementation will follow than to lock yourself into bad figures early.

Oregon and Washington policyholders should pay close attention to timing and documentation. In both states, carriers still expect cooperation, preservation of evidence, and timely notice, but a missed step does not always end the claim if the insurer cannot show real harm or if its own requests were unclear, duplicative, or unreasonable. That is where the claim file matters. If you asked for forms, requested clarification, or sought more time because you were displaced, those emails can become part of the coverage argument.

For the first week after the loss, use this checklist on what to do after a house fire for insurance purposes to get the file organized before deadlines start stacking up.

One more trade-off matters here. Policyholders often focus so heavily on contents documentation that they lose track of the building claim, code upgrade issues, and replacement cost support. These disputes can overlap. Good property insurance valuation insights help explain why accurate rebuilding support should be gathered early, not after the insurer has already framed the loss as a paperwork failure.

If the carrier denies for noncompliance, ask for the exact policy condition allegedly breached, the date it says compliance was due, every prior request it sent, and a clear explanation of how the delay or omission affected its investigation. Then answer with documents, not emotion. In many fire claims, that is the point where a weak procedural denial starts to crack.

8-Point Fire Claim Denial Comparison

| Item | 🔄 Implementation Complexity | ⚡ Resource Requirements | 📊 Expected Outcomes | ⭐ Ideal Use Cases | 💡 Key Advantages / Tips |

|---|---|---|---|---|---|

| Policy Lapse or Cancellation at Time of Loss | Low, factual check of dates/payments | Low–Moderate: billing records, insurer notices | Likely denial if lapse proven; possible reinstatement in narrow cases | Clear non-payment or documented cancellation disputes | Set up autopay, keep payment records, seek immediate reinstatement |

| Misrepresentation or Material Non‑Disclosure on Application | High, must prove materiality and intent | High: application files, underwriting records, legal review | Policy rescission or full denial if misstatement is material | When false answers or omissions are discovered in underwriting | Disclose fully, keep copy of application, notify changes promptly |

| Exclusions in Policy Language (Fire Exclusions or Limitations) | Moderate–High, policy interpretation and legal analysis | Moderate: policy review, adjuster/legal input, possible expert testimony | Denial if exclusion clearly applies; may be overturned if ambiguous | Losses that match explicit exclusion language (vacancy, arson, code violation) | Review exclusions, request endorsements, document code compliance |

| Inadequate or Missing Maintenance Records | Moderate, must link maintenance failure to causation | Moderate: maintenance logs, receipts, inspections, expert review | Denial or reduced payout if negligence materially contributed | Claims alleging lack of upkeep or faulty safety systems | Keep dated inspections/receipts, photograph maintenance, test detectors |

| Misclassification of Fire Cause or Arson Allegation | Very High, technical forensics and legal challenge required | Very High: certified fire investigators, engineers, legal counsel | Possible denial if insurer proves intentional act; disputed cases need experts | When insurer alleges arson or origin of fire is contested | Preserve scene, hire independent investigator, obtain official reports |

| Occupancy Status Violations (Vacant or Unoccupied Property) | Moderate, verify occupancy timelines and policy thresholds | Low–Moderate: lease records, utility bills, visitor logs | Denial if vacancy clause triggered; challengeable for short/temporary absences | Seasonal homes, rental vacancies, properties left empty long‑term | Notify insurer of vacancies, request vacancy endorsements, secure property |

| Uninsured or Underinsured Property (Coverage Limits Exceeded) | Low–Moderate, compare limits to replacement estimates | Moderate: appraisals, reconstruction estimates, inventories | Payment capped at policy limits; insured bears shortfall | Situations with inflated rebuild costs or high‑value personal property | Update replacement cost, schedule valuables, use inflation protection |

| Failure to Comply with Policy Conditions or Post‑Loss Requirements | Moderate, legal nuance re: materiality and waiver | Moderate: communications records, mitigation evidence, legal help | Denial if breach is material; may be defended if waiver or immaterial | Late notice, refusal to allow inspection, failure to mitigate additional damage | Report promptly, cooperate fully, document mitigation and all communications |

Don't Accept a Denial: Your Path to a Fair Settlement

A denial letter feels final because insurers write it that way. The tone is confident, the policy citations look technical, and the burden shifts onto you at the worst possible time. But a denial is still a position taken by the insurer. It isn't automatically the last word.

The strongest responses are organized, fast, and evidence-based. Start with the denial letter, then line it up against the full policy, every endorsement, all claim correspondence, and your underlying records. If the insurer says the policy lapsed, build the payment timeline. If it alleges misrepresentation, obtain the full application and underwriting file. If it relies on an exclusion, make it tie that exclusion to actual evidence. If it claims post-loss noncompliance, audit every request, every response, and every deadline.

That's the practical difference between reacting emotionally and contesting the denial effectively. Fire claims are won on documents, chronology, and policy language. The policyholder who can prove occupancy, maintenance, timely notice, and the scope of loss is in a far better position than the one who argues that the insurer is being unfair.

Oregon and Washington residents have another challenge. Many losses here involve older homes, seasonal occupancy patterns, rural properties, mixed-use structures, and wildfire-related conditions that create more room for insurer scrutiny. A vacant home in the Gorge, a rental in Portland between tenants, a cabin in Central Oregon, or a small commercial building in Southwest Washington can each trigger a different denial theory. You need a response built around the exact policy and the exact facts.

A licensed public adjuster can change the trajectory of the claim. A good public adjuster doesn't just "help with paperwork." They reconstruct the claim file, document the loss properly, identify weak denial theories, and negotiate from the policyholder's side only. They know what evidence matters, what requests are reasonable, what the carrier is likely building toward, and when a technical denial can be pushed back successfully.

If your fire claim has been denied, delayed, or narrowed into something far below what you need to recover, don't assume the insurer's first answer is the correct one. Review the policy. Preserve every record. Get independent help before giving repeated statements, accepting low valuation logic, or missing another deadline.

NW Claims Management represents policyholders in Oregon and Washington and works to level the playing field when insurers overreach. If your fire claim was denied, contested, or underpaid, a professional review can tell you whether the carrier's position is solid, vulnerable, or flatly wrong.

If your fire claim was denied in Oregon or Washington, NW Claims Management can review the denial, analyze the policy language, document the loss, and help you challenge the insurer's position. The firm represents policyholders only, not insurance companies, and offers a free claim evaluation so you can understand your options before the next deadline arrives.