After a major fire, flood, or storm, your property has a story to tell. A forensic investigation is how we translate that story into hard, scientific fact. It's an in-depth analysis designed to uncover the exact cause, timing, and full extent of the damage your property suffered.

Understanding a Forensic Investigation for Your Property

The word "forensics" often brings crime scenes to mind, but for property owners, it’s one of the most powerful tools you have during an insurance claim. Think of it less like a criminal case and more like a scientific mission to piece together exactly what happened, why it happened, and what it will truly take to make things right.

This process goes miles beyond the standard, often brief, inspection an insurance adjuster might perform. A forensic investigation is all about gathering and analyzing physical evidence to build a fact-based case that leaves no room for doubt.

What Does This Investigation Involve?

For a property claim, a forensic investigation isn't about assigning blame; it's about establishing certainty through science. We're replacing assumptions and opinions with objective proof.

In practice, this means our experts are on-site performing very specific tasks:

- Detailed Documentation: We’re not just snapping a few photos. This involves extensive photography, 3D scanning of the structure, and creating meticulous notes on every detail of the damage.

- Evidence Collection: We gather physical samples right from the site. This could mean collecting pieces of charred wood after a fire, sections of wet drywall from a flood, or shingles torn from a roof during a storm, all for lab analysis.

- Scientific Analysis: Back in the lab, specialized tools come into play. We might use moisture meters to pinpoint hidden water damage behind walls or conduct soot analysis to trace a fire's precise origin and burn pattern.

- Data Reconstruction: All this information allows us to build a clear, verifiable timeline of events. We can prove whether damage happened suddenly and accidentally or was the result of a pre-existing, long-term issue.

This rigorous method provides the concrete evidence needed for a truly comprehensive property damage assessment, ensuring no corner is cut and no detail is missed.

From Ancient History to Modern Claims

Using science to establish facts is hardly a new concept. The core principles of forensic investigation have been around for thousands of years. For instance, in 200 BC Babylon, merchants would press their fingerprints into clay tablets to validate contracts—an early form of evidence-based authentication.

This long history shows just how vital expert analysis is for documenting the truth, whether it's for an ancient contract or a complex property claim here in Oregon or Washington.

A forensic investigation transforms your property claim from a battle of opinions into a discussion of facts. It provides the objective, scientific proof needed to ensure your insurance company sees the complete picture and provides a fair settlement.

The same rigorous principles are applied in other high-stakes situations, like an NCAT independent building dispute inspection, where objective evidence is needed to resolve construction conflicts. At the end of the day, forensics is your most effective tool for holding an insurer accountable to their policy.

The Forensic Investigation Process from Start to Finish

If you're wondering what a forensic expert actually does, you're not alone. The whole process can feel like a bit of a black box, but it's really a systematic, science-based investigation with a clear beginning and end.

Let’s make this real. Imagine a pipe bursts inside a wall, causing massive water damage. Your insurance company suggests it might have been a slow, pre-existing leak, which your policy doesn't cover. This is exactly when a forensic investigation becomes your single most important asset.

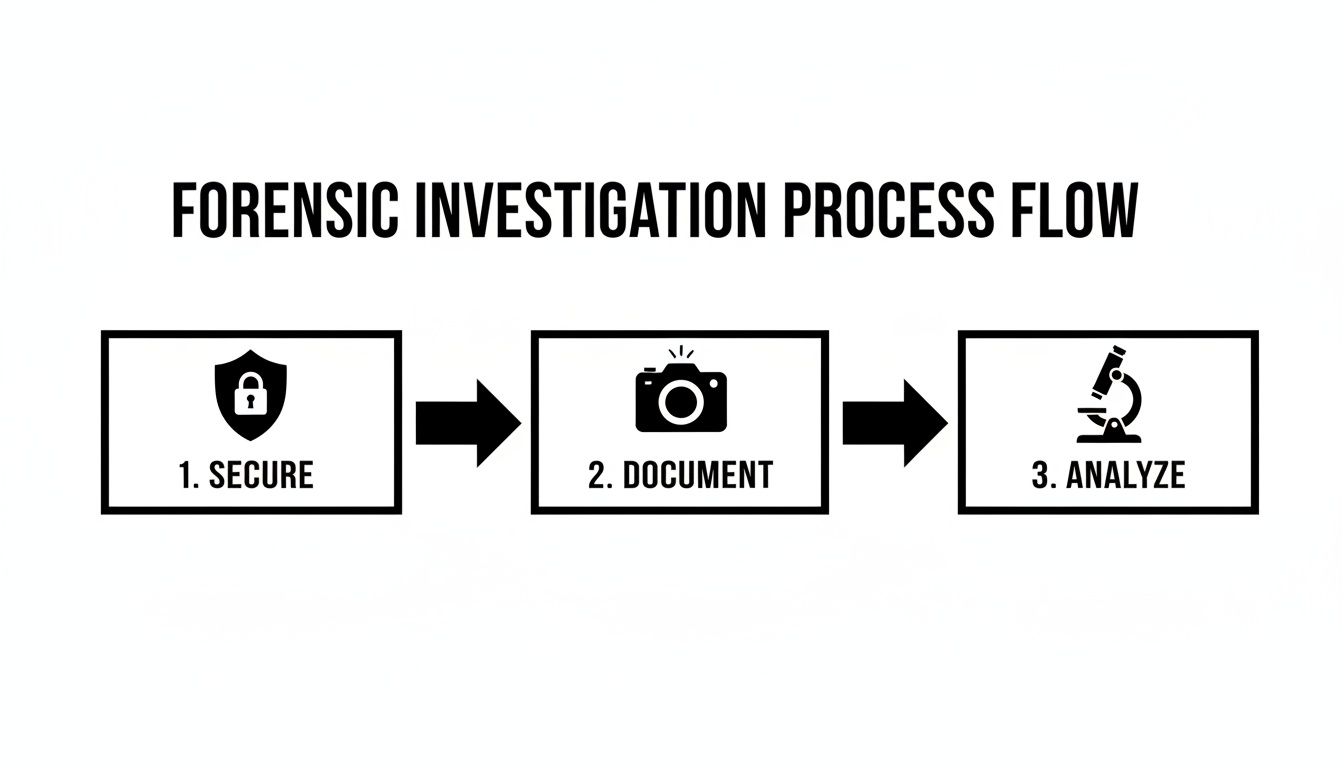

Securing the Scene

The first thing any good investigator does is secure the property. This isn’t just about locking the doors. It’s about preserving the scene exactly as it was found, much like a detective at a crime scene. The entire goal is to prevent anyone from disturbing the physical clues.

Think of it as a puzzle. If a well-meaning contractor starts ripping out wet drywall or you start moving damaged furniture around, you're essentially throwing away the puzzle pieces. Securing the scene ensures the evidence can tell its own, unbiased story.

This first step is absolutely critical. An investigator has to see the property in its immediate post-loss state to form a credible, scientific opinion about what caused the damage and when it started.

Meticulous Documentation

With the scene locked down, the investigator gets to work on documentation. This isn't just snapping a few photos on a smartphone; it's a deep dive to create a permanent, minutely detailed record of the entire area.

This phase almost always includes:

- High-Resolution Photography: We're talking hundreds of photos. They’ll capture wide-angle shots of the room, but also macro shots of corroded pipe fittings, specific water stain patterns, and warped floorboards. Every detail matters.

- 3D Scanning: Using technology like Matterport or LiDAR, an investigator can create a perfect digital replica of your property. This gives them precise measurements and an immersive model they can "walk through" again and again.

- Detailed Notes and Sketches: The expert will also be taking extensive handwritten notes and drawing sketches, mapping out where key items were, how the damage flowed, and any initial thoughts or observations.

This wealth of data creates a completely objective snapshot of that moment in time, which becomes the foundation for everything that follows.

Evidence Collection and Analysis

Next, the investigator shifts to collecting physical evidence. This is where the real science begins. Based on what they've seen and documented, they will strategically gather samples that can answer specific questions.

In our burst pipe scenario, this might look like:

- Carefully cutting out sections of the water-stained drywall.

- Taking core samples of the subfloor to test for moisture content.

- Collecting the actual failed pipe fitting that is believed to be the culprit.

These items are bagged, tagged, and sent to a specialized lab. There, technicians can run tests to determine how long materials were wet, check for contaminants, or perform a metallurgical analysis on the failed pipe. The results turn the investigator's on-site observations into cold, hard data.

Compiling the Final Report

With all the data in hand, the final step is to produce a comprehensive forensic report. This document pulls together everything—the photos, scans, lab results, and expert analysis—into a single, easy-to-understand narrative.

This isn't just a summary; it's a scientific argument that lays out the undeniable story of your loss. It explains the methods used, presents the evidence logically, and delivers a clear, defensible conclusion about the cause and origin. For any policyholder, understanding how this report fits into the complete property damage claim process is crucial.

Armed with this expert report, your public adjuster now has the factual firepower needed to dismantle an insurer’s flimsy theories and negotiate a fair settlement. It’s the ultimate tool for turning opinions into facts.

When it comes to property damage, "forensic investigation" isn't a one-size-fits-all service. You wouldn't ask a cardiologist to set a broken arm, and the same principle applies here. You need a specialist whose expertise directly matches the type of damage your property has suffered.

Getting this match right is everything. Different kinds of damage leave behind completely different clues, and only the right expert has the training and tools to read them correctly. An arson investigator won't have the gear to trace a hidden plumbing leak, and a structural engineer might not know the first thing about the chemical accelerants used to start a fire. Each specialty is its own scientific discipline.

Fire and Arson Investigators

After a fire, two questions dominate everything: "Where did it start?" and "How did it start?" A Certified Fire Investigator (CFI) is the professional who finds the answers. They are trained to read the subtle language of a burn scene—interpreting char patterns, smoke deposits, and how different materials have melted or warped.

They methodically dig through the debris to locate the fire's point of origin. From there, they piece together the cause, determining if it was an accidental electrical fault or intentional arson. Their toolkit often includes highly specialized equipment, like gas chromatographs, which can detect tiny, invisible traces of accelerants like gasoline.

Water Intrusion and Mold Specialists

Water damage is incredibly deceptive. The stain you see on your ceiling is often just the tip of the iceberg. A Water Intrusion Specialist is an expert at finding where the moisture is really hiding and, most importantly, identifying its source—a critical step if the insurance company is questioning how the leak happened.

These investigators use an arsenal of non-destructive tools to see inside your walls and under your floors without tearing them apart:

- Thermal Imaging Cameras: These devices show temperature differences, quickly revealing cold, damp spots that signal hidden moisture.

- Moisture Meters: By taking direct readings from drywall, wood, and concrete, they can map the exact path water traveled through your home.

- Borescopes: A tiny camera on a flexible tube allows them to peek inside wall cavities and plumbing chases, providing a clear view of the problem.

This detailed evidence is vital for proving that the damage came from a sudden pipe burst versus a slow, long-term leak. That distinction can be the difference between a paid claim and a denied one.

To help you understand how these different experts approach a loss, we've created a simple comparison table.

Forensic Specialties for Different Property Damage Claims

| Type of Damage | Forensic Specialist | Primary Questions Answered |

|---|---|---|

| Fire | Certified Fire Investigator (CFI) | Where did the fire originate? Was it accidental or arson? |

| Water Damage | Water Intrusion Specialist | What is the source of the water? How far has the moisture traveled? |

| Mold | Industrial Hygienist / Mold Expert | Is the mold growth active? What type of mold is it and what is the source? |

| Structural Failure | Forensic Structural Engineer | Why did the structure fail? Was it due to an event, defect, or wear? |

| Ground Movement | Geotechnical Engineer | Is the damage from soil settlement, a landslide, or other ground issues? |

As you can see, each specialist is trained to answer very specific questions that are crucial for substantiating your claim.

No matter the specialty, every investigator follows this core three-step process. They secure the scene to preserve evidence, meticulously document their findings, and then analyze all the data to form an objective conclusion.

Structural and Geotechnical Engineers

When a building's integrity is in question—perhaps after an earthquake, a major storm, or due to suspected construction defects—you need a Forensic Structural Engineer. It's their job to figure out why a part of the building failed. They analyze foundation cracks, compromised beams, and collapsed roofs to pinpoint the root cause of the damage.

A structural engineer's report can prove that a building's failure was due to a specific event, like a windstorm, countering an insurer's claim that it was caused by pre-existing wear and tear or poor maintenance.

If the problem seems to be coming from the ground itself, a Geotechnical Engineer might be called in. They investigate issues like landslides, soil settlement, or other earth-related problems that can cause catastrophic damage to a property’s foundation.

These engineers apply their deep knowledge of physics, materials science, and building codes to produce reports that clearly explain the cause of loss and the necessary scope of repairs. The evidence they provide often works hand-in-hand with the efforts of a public adjuster. To better understand that relationship, it helps to compare a public adjuster vs insurance adjuster.

Ultimately, by aligning the right professional with your specific type of damage, you arm your claim with the strongest scientific evidence possible.

When Your Claim Needs a Forensic Investigation

You’ve filed your property damage claim and are hoping for a quick, straightforward process. But what happens when things go sideways? How do you know when it’s time to stop arguing with the insurance adjuster and bring in a scientific expert?

Certain red flags from your insurance company are strong signals that a forensic investigation might be your only path forward. Recognizing these signs is the first step to taking back control of your claim and arming yourself with the objective evidence needed to challenge an insurer’s flimsy arguments.

Your Insurer Denies the Claim Without a Clear Reason

Getting a denial letter is a gut punch, especially when the reasoning is vague or nonsensical. If your insurer denies your claim without providing a specific, evidence-based explanation tied directly to your policy, you should be skeptical. A form letter simply stating "the damage is not covered" just doesn't cut it.

You have a right to a detailed breakdown of why your claim was rejected. This should include the exact policy language they are citing and the physical evidence they used to reach their conclusion. A denial based purely on an adjuster's opinion or a quick, surface-level inspection is a good sign you need your own expert to find the real story.

The Settlement Offer Is Far Too Low

In other cases, the insurer might approve your claim but come back with a settlement offer that won’t even cover the cost of materials, let alone labor. This is a classic tactic. It often means their adjuster either missed significant hidden damage or intentionally wrote a low-ball estimate to save the company money.

If their number feels impossibly low compared to what local, reputable contractors are quoting, it’s time to question their math. A forensic investigator can document the true scope of the damage, creating a comprehensive report that serves as powerful leverage in negotiations.

An insurer's low settlement offer is often a tactic, not a final number. It's a starting point based on their limited view of the damage. A forensic report replaces their opinion with irrefutable proof of what it will actually cost to rebuild.

This is a frequent hurdle for policyholders. In fact, a public adjuster can often use forensic findings to significantly increase an initial low offer. You can find out more about how this works by learning when to hire a public adjuster for your claim.

The Insurer Disputes the Cause of Damage

This is where things get tricky, and it's probably the most common reason to hire a forensic expert. Insurers will often try to argue that your damage was caused by a pre-existing issue—like wear and tear, rot, or poor maintenance—instead of a sudden and accidental event that your policy actually covers.

You’ve seen it before. The scenarios sound something like this:

- Water Damage: You know a supply line burst and flooded your kitchen, but the insurance company insists it was a "long-term, slow leak" you should have noticed and fixed.

- Fire Damage: They hint that your own faulty wiring caused the fire, pinning it on homeowner negligence instead of an accidental appliance failure.

- Storm Damage: They claim the 70 mph wind gusts didn't damage your roof; they argue it failed simply because it was old.

When it becomes your word against theirs, a forensic investigator is the ultimate tie-breaker. A water intrusion specialist, for example, can analyze moisture patterns and material decay to prove the damage was recent and catastrophic, not gradual. As you learn more about navigating the roof insurance claim process, you'll see how critical proving the cause is. A solid scientific report can completely dismantle the insurer’s theory and establish the true cause of loss.

How to Hire a Qualified Forensic Investigator

When your insurance claim stalls out, it's often because you and the insurance company have two completely different stories about what happened. This is where a forensic investigator becomes your most valuable asset. But let me be clear: not just any expert will do. The difference between winning your claim and having it fall apart often comes down to hiring the right professional—one with impeccable credentials and a proven history of unbiased work.

Making this choice isn't something to take lightly. A truly qualified expert can provide the scientific proof needed to dismantle an insurer's weak arguments, while the wrong one can sink your case for good. For property owners in Oregon and Washington, knowing what to look for is your best defense.

What to Look for in a Forensic Expert

Think of this as your must-have checklist. Before you even think about signing a contract, make sure any potential investigator checks these boxes. A real professional will have no problem providing this information.

- Specific, Relevant Certifications: Don't settle for general credentials. If it's a fire claim, you want a Certified Fire Investigator (CFI). For a structural collapse, you need a licensed Professional Engineer (PE). These designations aren't just letters after a name; they prove the expert has met demanding standards.

- Active State Licensing: At a minimum, they must be licensed to practice in Oregon or Washington. This is a basic, non-negotiable requirement that confirms their legitimacy and holds them accountable.

- A Proven, Verifiable Track Record: Ask to see their work. A seasoned investigator will have a portfolio of reports from cases similar to yours and, ideally, experience giving expert testimony in court. That courtroom experience is gold—it means their findings hold up under the most intense scrutiny.

- Genuine Independence: This is the big one. You need to know, without a doubt, that they work for you, not the insurance industry. Some "experts" earn most of their income from insurance companies, creating a massive conflict of interest.

A word of caution: be wary of general contractors or restoration companies who bill themselves as forensic experts. While they're fantastic at the repair work, they rarely have the scientific background and methodical approach needed for a formal investigation.

Key Questions to Ask Before You Hire

Once you've narrowed down your list, it's time for an interview. And yes, you should treat it like an interview. Their answers will tell you everything you need to know about their process, experience, and objectivity.

- "Walk me through your process for a case like mine." You're listening for a clear, step-by-step method: securing the scene, documenting everything, collecting evidence, and methodical analysis. If you get a vague or rambling answer, that's a major red flag.

- "Have you ever testified in court on this specific subject?" An expert whose work is solid enough to be presented in a legal setting is exactly the kind of ally you want.

- "Who is your typical client? Do you work mostly for policyholders or for insurance companies?" This question gets right to the heart of potential bias. An expert who consistently represents homeowners is far more likely to be a true advocate for your claim.

- "What is your fee structure and what's included?" You need total transparency on costs. These fees are often managed alongside the services of a public adjuster. For a better understanding of how these professional costs fit into a claim, take a look at our guide on what a public adjuster costs.

Hiring a forensic investigator is about getting to the truth. Their job is to deliver objective, scientific facts that speak for themselves, ensuring your claim is decided on evidence, not opinion.

Finding the right expert means you can face your insurance company with confidence, knowing your side of the story is backed by irrefutable science. It’s the ultimate way to level the playing field.

Common Questions About Forensic Investigations

When you're dealing with a complicated insurance claim, the thought of hiring a scientific expert can feel a little overwhelming. But getting a handle on the practical side of things—like costs, timelines, and how these pros actually help—is the best way to take back control. Let’s walk through the questions we hear most often from property owners, with some straightforward answers to clear things up.

This isn't just another expense or a complicated step. It's about getting the proof you need to secure a fair outcome. With a team like NW Claims Management on your side, a forensic investigation becomes one of the most powerful tools you have.

How Much Does a Forensic Investigation Cost and Who Pays for It?

There’s no single price tag for a forensic investigation; the cost really hinges on how complex your situation is. A simple analysis, like figuring out where a small plumbing leak started, might run a few thousand dollars. On the other hand, a major investigation into a catastrophic structural collapse or a large fire that requires extensive lab work could cost tens of thousands.

Initially, the policyholder covers the upfront cost of hiring the expert. I know that can sound like a lot, but it’s best to see it as an investment in your claim. The evidence they uncover is often the very thing that turns an insurer's lowball offer into a fair settlement, making the cost well worth it in the end.

Think of it this way: you might invest $5,000 in a forensic report that proves your $250,000 claim is valid, countering an insurer’s lowball offer of just $75,000. The return on that investment is enormous.

Here’s the good news: these costs are often recoverable. Most insurance policies include coverage for "claim preparation costs," which can include expert fees. This is where a public adjuster is vital. We build the case that the investigation was a necessary step to prove your loss and argue for the insurance company to reimburse you for the expense.

How Long Does a Forensic Investigation Take?

This is where a little patience goes a long way. The timeline really depends on the extent of the damage and how deep the analysis needs to go. There isn't a standard turnaround, but any good investigator can give you a solid estimate after their first visit to the property.

As a general rule of thumb:

- Simple Cases (1-2 weeks): For issues that can be figured out with a site visit and a report based on what's visible, the process is pretty quick. A good example is finding the source of a straightforward roof leak.

- Complex Cases (4-8+ weeks): If the investigator needs to send material samples to a lab, the timeline gets longer. Things like charred wood, water-damaged drywall, or soil samples need to be carefully tested, and waiting for those results can add several weeks to the process.

While you're waiting, remember that this thorough approach is what gives the final report its power. A rushed investigation results in a weak report that the insurance company's experts can tear apart. A methodical, detailed analysis produces a rock-solid, evidence-based document they simply can't ignore.

What Is the Difference Between a Forensic Investigator and a Public Adjuster?

This is a great question, and understanding the answer is key. Both of us are on your team, but we play very different—and equally important—roles.

A forensic investigator is the scientific expert.

Think of them as the "property detective." Their job is to focus entirely on the physical evidence. They dig into the what and how of the damage—what caused it, and where did it originate? They analyze everything, run the tests, and compile their findings into a technical, fact-based report. They stick to the science; they don't negotiate with the insurance company or get into the fine print of your policy.

A public adjuster is your licensed claim advocate.

A public adjuster, like our team at NW Claims Management, is your strategist and representative for the entire claim. Our job is to:

- Read and interpret your complex insurance policy.

- Document every detail of your loss.

- Handle all the back-and-forth with the insurance company.

- Negotiate to get you the maximum settlement you're entitled to.

We’re the ones who hire and direct the forensic investigator. Then, we take their expert report and use it as powerful leverage in negotiations, turning scientific fact into your financial recovery.

Will a Forensic Report Guarantee My Claim Gets Paid?

While nothing in the world of insurance comes with an absolute guarantee, a credible forensic report dramatically tilts the odds in your favor. It completely changes the dynamic of the dispute.

Without an expert report, disagreements often turn into a frustrating "he said, she said" battle between you and the insurance company's adjuster. The insurer has their own experts and will use their opinions to justify denying your claim or making a low offer.

A forensic report cuts through all that. It replaces their opinions with objective, scientific fact. When you present the insurance company with a detailed analysis from a qualified third-party expert—the kind of report that would hold up in court—they have to take it seriously. It forces them to deal with the real evidence, not just the story they want to tell. More often than not, it’s the key to breaking a stalemate and getting the full payment you deserve.

Navigating a major property damage claim is a huge undertaking, but you don’t have to face it alone. The expert team at NW Claims Management is here to fight for you. If you're in Oregon or Washington and feel your insurer isn't treating you fairly, contact us for a free claim evaluation. Learn more at https://nwclaimsmanagement.com.