You paid your premiums. You kept the policy in force. Then a fire, major leak, wind event, or burst pipe turns your week upside down, and the shock isn't from the damage. It comes from the estimate that lands on your kitchen table.

The carrier says part of the loss is excluded. The limit isn't high enough. Depreciation applies. Certain code upgrades aren't covered. Temporary business expenses aren't fully reimbursed. The policy you thought would make you whole turns out to be a narrower contract than you realized.

That moment is where insurance coverage gaps stop being an abstract insurance term and become a cash problem. For property owners in Oregon and Washington, that problem often surfaces after the loss, when decisions are urgent and power feels one-sided.

The Hidden Risk in Your Insurance Policy

A common post-loss conversation goes like this. A homeowner says, "I've had insurance for years. How can I still owe this much out of pocket?" The answer usually isn't that the policy failed to exist. It's that the policy covered some things, limited others, and never covered a few key items at all.

That gap between what people think they bought and what the contract pays is larger than most owners realize. On a global scale, the insurance protection gap reached 9 trillion U.S. dollars in 2024, equal to 8.1% of global GDP, which shows how widespread underinsurance and unmet protection needs have become, not just in one market or one policy type (MAPFRE Economics).

In property claims, this shows up in ordinary ways. A family expects a full rebuild after a fire, then learns the dwelling limit trails current construction costs. A business owner assumes all water damage is treated the same, then finds the cause of loss and policy wording matter more than the wet drywall in front of them. For a useful example of how cause and wording change a claim outcome, this guide on understanding water damage claims Florida is worth reading even if you're in the Northwest, because the logic around sudden loss versus excluded conditions applies far beyond one state.

Why the declarations page doesn't tell the whole story

The declarations page matters, but it doesn't explain everything. It tells you limits, deductibles, and named coverages. It doesn't tell you how exclusions, valuation language, sublimits, waiting periods, and endorsements will work together after a real loss.

If you've never looked past the front page, start with a plain-language breakdown of insurance policy limits explained. Property owners often focus on the premium and the big coverage number, when the true risk sits in the definitions and conditions behind it.

Practical rule: Insurance isn't a promise to pay for "damage." It's a contract to pay for specific damage, under specific terms, up to specific limits.

That's why post-claim discovery feels so brutal. You don't find the weak spots when the house is dry and quiet. You find them when contractors are waiting, materials cost more than expected, and every day of delay has a price.

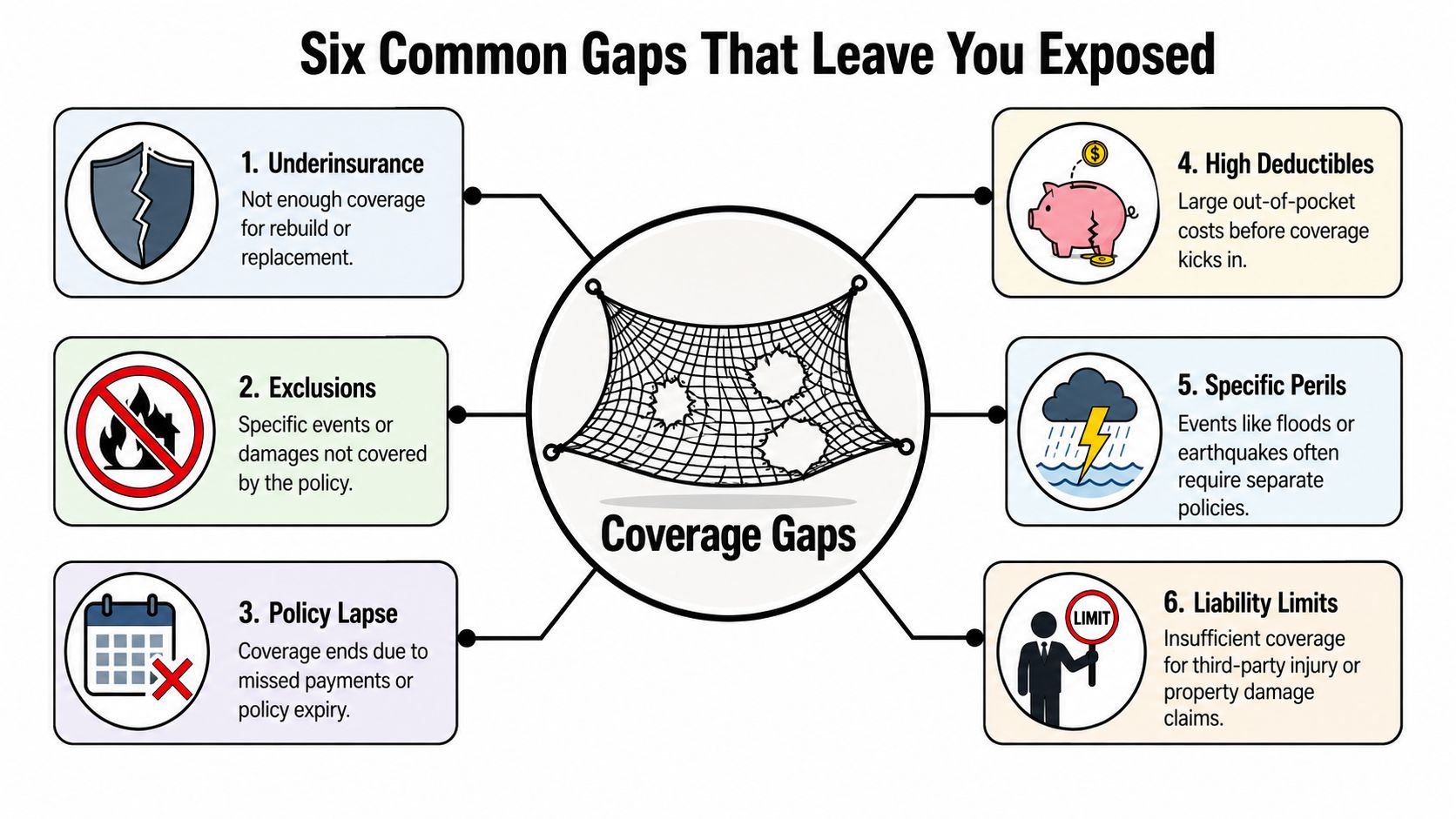

Six Common Gaps That Leave You Exposed

A policy is supposed to be a safety net. The problem is that many owners don't notice the holes until they fall through them.

Peril gaps

A peril gap means the event that caused the damage isn't covered under the policy you have. Standard property owners often assume any major physical damage must be insured. That isn't how these contracts work.

Flood, earth movement, repeated seepage, and certain types of backup or off-premises utility issues may require separate protection or added language. If the cause of loss falls outside the covered perils, the claim can stop before valuation even becomes the fight.

Limit gaps

A limit gap means the policy covers the type of loss, but not enough money is available to finish the job. This is one of the most painful claim outcomes because the owner is partly right. Coverage exists, but it runs out.

The most common version is Actual Cash Value versus Replacement Cost. In property insurance, the ACV versus RC valuation gap is especially serious because ACV deducts depreciation and can leave homeowners with 20 to 40% less than needed to rebuild, and industry analysis tied that difference to $15,000 to $45,000 shortfalls per average residential claim in Oregon and Washington (Noblepa Group technical analysis).

A roof, older flooring, aging cabinetry, or worn finishes can all look "covered" at first. Then depreciation is applied and the insured learns the check doesn't buy today's labor and materials.

Exclusion gaps

An exclusion gap is more direct. The policy says certain property, causes of loss, or costs aren't covered. Owners usually discover exclusions in denial letters and partial denials.

Some exclusions are broad. Others are tucked into narrow language around mold, vacancy, code upgrades, wear and tear, or long-term leakage. Exclusions don't care what you intended to buy. They apply based on the wording in force on the date of loss.

Endorsement gaps

An endorsement gap means the base policy may be decent, but a missing add-on leaves a predictable risk uninsured. Sewer backup is a good example. So is ordinance or law coverage. So is added protection for high-value items that exceed standard sublimits.

If you own jewelry, collectibles, instruments, firearms, camera gear, or other high-value personal items, review whether they belong on a separate schedule. This overview of scheduled personal property coverage is useful because standard personal property limits often don't match what owners own.

Coinsurance gaps

A coinsurance gap hits when the carrier decides you didn't insure the property to the required value under the policy condition. Even when the loss is covered, payment can be reduced because the stated amount of insurance didn't meet the policy's valuation formula.

Owners usually don't notice this risk during renewal. They notice it when a partial loss gets paid as though they accepted part of the risk themselves.

Liability gaps

A liability gap means your policy's legal protection may not be high enough for a serious injury or major property damage claim involving someone else. This gap is less visible during routine ownership, but it can become the most expensive one on the property.

A dog bite, a visitor injury, a contractor dispute, or a fire spreading to adjoining property can quickly test whether your underlying liability limit fits your actual exposure.

The expensive mistake is assuming "covered" means "fully covered." In real claims, scope, cause, valuation, and limits decide what gets paid.

How Gaps Devastate Home and Business Owners

In Oregon and Washington, the damage itself is only half the problem. The other half is how the policy responds when cleanup starts, estimates rise, and the owner realizes certain costs were never squarely insured.

A residential loss in Oregon

A family in an Oregon suburb loses part of their home to wildfire damage and smoke intrusion. They expect the claim to fund demolition, debris removal, reconstruction, temporary living costs, and replacement of damaged personal property with minimal friction.

Instead, the rebuild estimate pushes against the dwelling limit almost immediately. Site cleanup costs are larger than expected. Landscaping isn't restored the way they assumed it would be. Some personal property values are disputed. The contractor's pricing reflects current market conditions, but the policy language doesn't stretch because the work became more expensive after the event.

The emotional impact is obvious. The financial impact is worse. The owners must either scale back the rebuild, pay the difference, or fight over any part of the loss that may still fit within policy language.

A commercial loss in Seattle

A Seattle business owner suffers major water damage in a commercial space. The floors, walls, equipment areas, and operations are disrupted. The owner assumes property coverage plus business interruption will carry the company through repairs.

Then the pressure starts from three directions at once:

- Property valuation disputes: The carrier questions the full repair scope and pricing.

- Coinsurance issues: The insured value hasn't kept pace with the property's actual exposure, so payment is reduced under the policy condition.

- Operational strain: The business has to keep serving customers, relocate functions, or absorb lost momentum while waiting for funds.

The business owner's biggest mistake isn't carelessness. It's believing the policy would behave like a working capital reserve. Insurance can help. It doesn't automatically solve cash flow during a prolonged interruption.

For many commercial losses, the overlooked issue is time. Repairs take longer than people think. Revenue may return slowly. Extra operating costs show up fast. That's why owners need to understand extra expense coverage before the next loss, not after the accountant starts triaging bills.

Even in catastrophe losses, a large share of costs still lands on owners. Globally, 70% of natural catastrophe losses remain uninsured, which shows how often disaster costs stay outside insurance recovery (The Geneva Association).

That global reality feels very local after a fire, storm, or major escape of water. The invoice doesn't care that the policyholder believed they were protected. It only cares who is paying the balance.

Navigating Specific Risks in Oregon and Washington

Oregon and Washington owners face a version of underinsurance that generic insurance articles often miss. The issue isn't only whether the building is insured. It's whether the policy matches local hazards, local rebuilding rules, and local claim realities.

Separate the standard policy from Northwest hazards

Standard property policies often leave major regional risks outside the base contract. In the Pacific Northwest, the two that deserve immediate attention are flood and earthquake. Owners regularly assume one or both are built into the policy because they're serious hazards. Usually, they are not.

That matters because claim denials in these categories aren't usually valuation disputes. They're contract disputes. If the peril wasn't included, the carrier may have no obligation to pay for that part of the loss.

Code upgrades create hidden rebuilding costs

A second Northwest issue is ordinance or law coverage. Older homes and commercial buildings in Portland, Seattle, Tacoma, Eugene, Spokane, and many smaller communities may trigger code-related upgrades during repair. Once walls are opened or damaged systems are replaced, local building departments may require work that didn't exist when the structure was built.

That can include electrical changes, accessibility elements, structural improvements, or other mandated upgrades. Owners often learn too late that a basic policy may not fully absorb those added costs unless the proper coverage was included.

Good local questions to ask before a loss

Bring these questions to your agent or broker in writing:

- Ask about excluded Northwest perils: Is flood covered anywhere in my current program? Is earthquake covered anywhere?

- Ask how code costs are handled: If local rules require upgrades during rebuilding, which part of my policy responds?

- Ask what valuation applies: Am I insured on replacement cost or actual cash value for the building and for personal property?

- Ask what the carrier needs after a loss: What proof, records, estimates, inventories, and time deadlines could affect payment?

A local policy review should also include your state's insurance department resources and your municipality's permitting realities. In practice, Oregon and Washington claims are shaped as much by local reconstruction requirements as by the initial cause of loss.

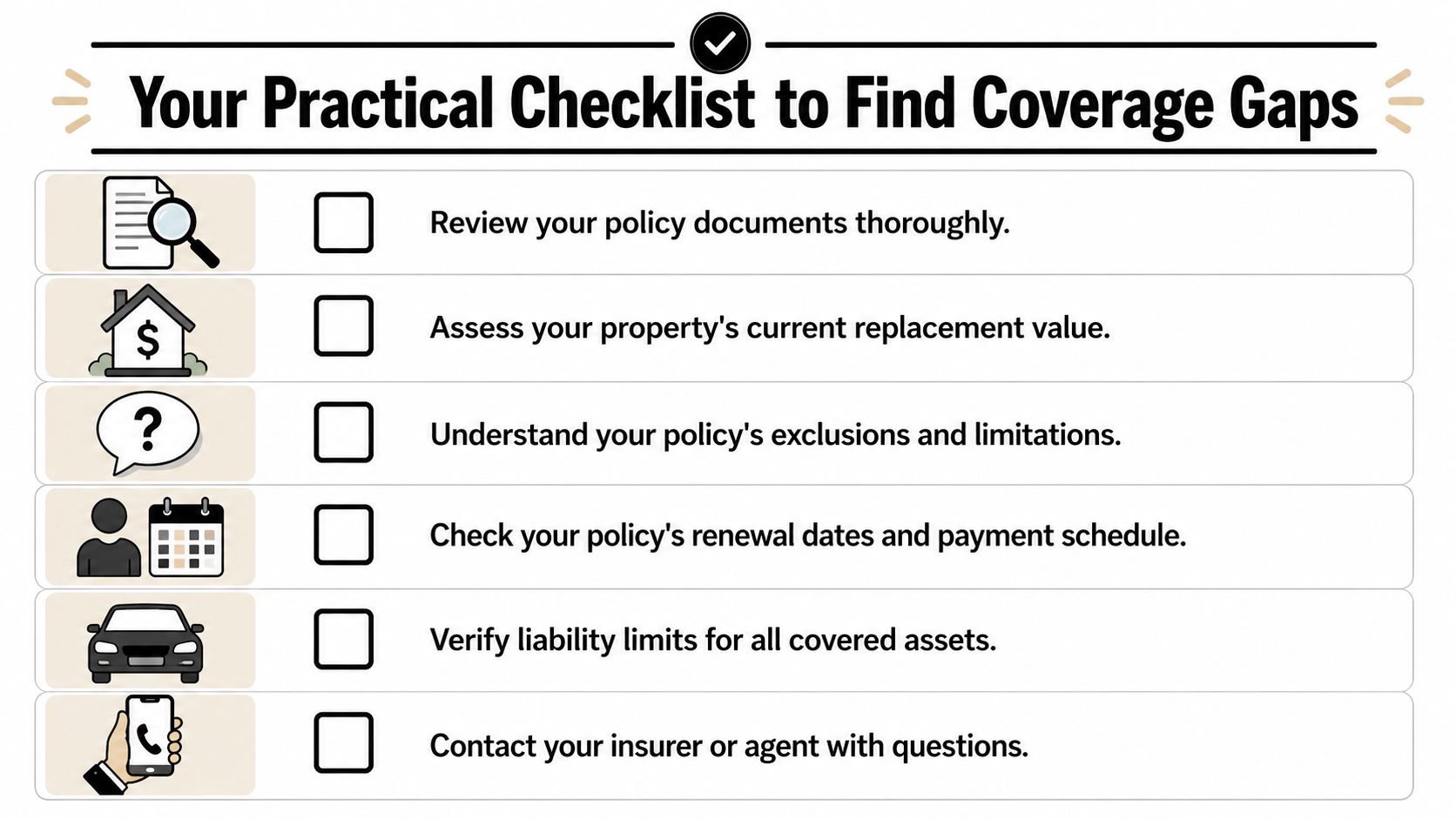

Your Practical Checklist to Find Coverage Gaps

You don't need to read your policy like a coverage lawyer to spot major warning signs. You do need to slow down and review the documents that control payment after a loss.

Start with the declarations page

The declarations page is the quickest way to see what you bought. Pull the current version, not last year's copy, and confirm the named insured, property address, policy period, deductibles, and each major limit.

Then review these six checkpoints:

Find the valuation language

Look for whether the building and contents are settled on replacement cost or actual cash value. If the wording isn't obvious on the declarations page, it may appear in endorsements or loss settlement provisions.Compare limits to present rebuilding reality

Ask whether the dwelling or building limit still matches current reconstruction conditions in your area. If you've remodeled, added structures, upgraded finishes, or renewed for years without a serious review, your numbers may be stale.Read the exclusions section slowly

Search for flood, earth movement, sewer or drain backup, mold, ordinance or law, and vacancy-related restrictions. These exclusions often conceal many insurance coverage gaps in plain sight.

Check conditions that reduce payment

The next part of the policy often matters just as much as the covered causes of loss.

- Review coinsurance or insurance-to-value wording: If the policy requires a certain level of coverage relative to property value, underinsuring can reduce what gets paid on a partial loss.

- Look for sublimits: Jewelry, tools, electronics, business property at home, detached structures, and specialty items may have lower caps than you expect.

- Confirm loss of use or business income terms: A policy can include this coverage and still limit it in ways that create pressure during a long repair.

Build a record before you need one

Documentation closes a surprising number of disputes before they start. Walk through the property with your phone. Photograph each room, major systems, upgrades, and outbuildings. Save contractor invoices, remodeling records, and receipts for major purchases.

For personal contents, a simple worksheet helps more than memory ever will. Use a personal property inventory template to record what you own, where it is, and what supports the value. After a major loss, people rarely remember everything under stress.

Watch for this red flag: If you can't explain, in plain English, how your policy pays for rebuilding, temporary living, personal property, and local code upgrades, you probably haven't reviewed the parts that matter most.

Don't try to solve every issue in one sitting. Mark the unknowns, email your questions, and keep the answers. Written clarification is far more useful than a vague memory at claim time.

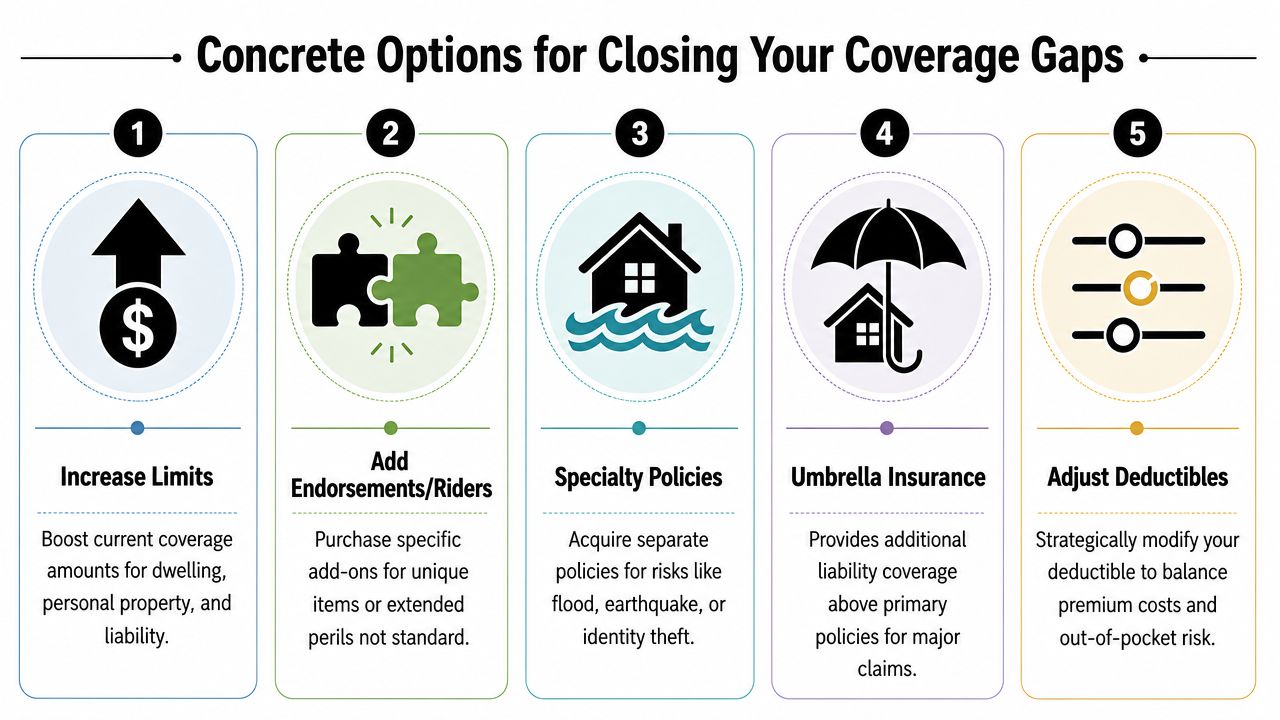

Concrete Options for Closing Your Coverage Gaps

Once you've identified weak spots, the right fix depends on the kind of exposure. Some gaps call for a higher limit. Others require a specific endorsement. Some require an entirely separate policy.

When increasing limits is the right move

If the risk is straightforward underinsurance, raising the limit is usually the cleanest fix. This applies to dwelling, other structures, contents, business personal property, and liability when the underlying coverage already fits the exposure.

Higher limits help when the problem is capacity. They don't solve excluded perils, missing endorsements, or weak valuation language.

When endorsements or riders make more sense

Endorsements are targeted tools. Use them when the base policy is close, but one missing piece creates a major vulnerability.

Common examples include:

- Ordinance or law coverage: Helps with code-driven rebuild costs.

- Sewer or water backup coverage: Addresses a frequent source of costly damage not handled well by basic forms.

- Scheduled personal property: Better for valuables that would otherwise hit sublimits.

- Extended replacement cost language: Helps when rebuilding costs exceed the basic policy limit within the terms of the endorsement.

This is also where owners should think beyond the policy form and into claim proof. If you own artwork, antiques, or delicate specialty items, documentation and handling matter before and after a loss. For owners planning storage or relocation during repairs, guidance on specialized packing for fine art can help preserve value and support cleaner claim presentation if those items are later damaged.

When a specialty policy is necessary

Some risks don't belong inside a standard property policy at all. Flood and earthquake are the clearest examples in Oregon and Washington. Identity theft, cyber exposures, or specialized commercial risks can fall in this category too.

A specialty policy is usually the right answer when the peril lies outside the core scope of the base contract, not just limited by endorsement.

When liability needs a second layer

A personal or commercial umbrella policy is different from property coverage. It adds another layer above underlying liability policies when a serious claim exceeds those primary limits.

Use umbrella protection when your concern is lawsuit exposure, not rebuilding cost. It won't substitute for property insurance, but it can protect assets when a severe liability event outgrows the base home, auto, or business policy.

A quick comparison

| Option | Best used for | Won't fix |

|---|---|---|

| Increase limits | Underinsured building, contents, liability | Excluded perils |

| Add endorsements | Backup, code upgrades, scheduled items, broader valuation | Hazards that require separate policies |

| Buy specialty policies | Flood, earthquake, other excluded risks | Ordinary underinsurance within the main policy |

| Add umbrella coverage | Large liability exposure | Physical property shortfalls |

| Improve documentation | Stronger proof of ownership and value | Missing coverage language |

The wrong fix is buying more of the same weak coverage and assuming the gap is closed. The better approach is matching the solution to the reason the gap exists.

How a Public Adjuster Finds Coverage After a Loss

By the time most owners call for help, the gap has already shown itself. A denial letter arrives. Part of the estimate is omitted. Depreciation is applied aggressively. Code work is disputed. Personal property is undercounted. The carrier's scope feels too small for what the contractor says must be done.

A public adjuster works for the policyholder, not the insurer. That's the central difference. The job isn't to manufacture coverage that isn't there. The job is to read the policy closely, document the damage correctly, present the loss in the form the contract requires, and challenge narrow interpretations that reduce payment.

What that work looks like in practice

A strong public adjuster typically does four things that owners struggle to do alone:

- Rebuilds the claim file: Photos, measurements, estimates, contents documentation, expert input, and line-by-line support.

- Tests the carrier's scope against the policy: Not just what was damaged, but what related costs may also fall within coverage.

- Frames disputed items correctly: Many underpayments come from how damage is categorized, not just whether damage exists.

- Negotiates from the contract: The basis for negotiation is found in policy language and evidence, not frustration.

In Oregon and Washington, that often means addressing smoke contamination, hidden moisture, code-related work, matching issues, cleanup costs, business interruption questions, and overlooked personal property losses with more precision than the initial adjustment provided.

Why owners bring one in after a partial denial

Owners often think they need a lawyer the moment a problem appears. Sometimes they do. But many claim disputes are still adjustment disputes before they become legal disputes.

A licensed public adjuster can step into that space and push the claim toward a fuller valuation and a more accurate coverage analysis. That matters when the insurer says, in effect, "this isn't covered" or "this is all we're paying," and the file doesn't yet reflect the whole loss.

A post-loss coverage gap isn't always a true lack of coverage. Sometimes it's a documentation gap, a valuation gap, or a narrow reading that no one has properly challenged.

That distinction can mean the difference between absorbing the shortfall yourself and recovering funds that should have been part of the claim all along.

If you're dealing with property damage in Oregon or Washington and the numbers don't make sense, NW Claims Management can review the claim, interpret the policy, and advocate for the settlement you were supposed to receive. When a carrier underpays, overlooks covered damage, or points to a gap after the loss, experienced public adjusting can bring the file back to the contract and fight for the funds your property needs.