Home insurance typically covers arson if a third party committed it, but denies the claim if the policyholder caused the fire. The outcome usually turns on one issue more than any other: who set the fire, and what you can prove about it.

If you're reading this after a suspicious fire, you're probably dealing with more than smoke damage. You're dealing with a locked property, calls from the insurer, pressure to give statements, and the fear that one accusation could derail your recovery. That fear is justified. Fire is usually covered under a standard homeowners policy, but arson changes everything because the claim stops being only about damage and starts becoming a question of intent, involvement, and evidence.

That makes does home insurance cover arson the wrong question if you stop at yes or no. The better question is: what does the insurer need to see before it will treat the fire as a covered third-party loss instead of an excluded intentional act?

Arson and Your Home Insurance Policy

A common version of this claim starts the same way. A homeowner gets a late-night call, rushes over, and finds firefighters still on scene. The next morning, someone mentions the fire looked suspicious. From that point on, the claim doesn't move like a routine kitchen fire or electrical fire claim.

In standard U.S. homeowners insurance, fire is usually a covered peril, but coverage changes when the fire was intentionally set by the homeowner or someone in the household. Consumer guidance from the National Association of Realtors explains that standard policies typically cover fire and smoke damage to the home, detached structures, and personal belongings, but may exclude damage caused by arson or other intentional loss. It also notes that insurers generally deny claims when the policyholder set the fire because intentional acts are excluded from most property policies, while a fire set by a third party may still be covered depending on the policy language and proof available in the claim National Association of Realtors consumer guide on fire damage and policy coverage.

That basic rule is simple. The hard part is everything that comes after.

The real issue is proof

Most homeowners don't lose these claims because they misunderstand the word arson. They lose them because they assume the fire report alone will settle the insurance question. It usually doesn't. The carrier wants to know who had access, whether there was a motive, how the fire started, and whether the evidence supports non-involvement by the insured.

Practical rule: If the fire was suspicious, treat the claim like both a property loss and an evidence file from the first day.

A solid understanding of the home insurance claim process after a major loss helps here. Suspicious-fire claims often move slower, require more documentation, and involve more scrutiny than homeowners expect.

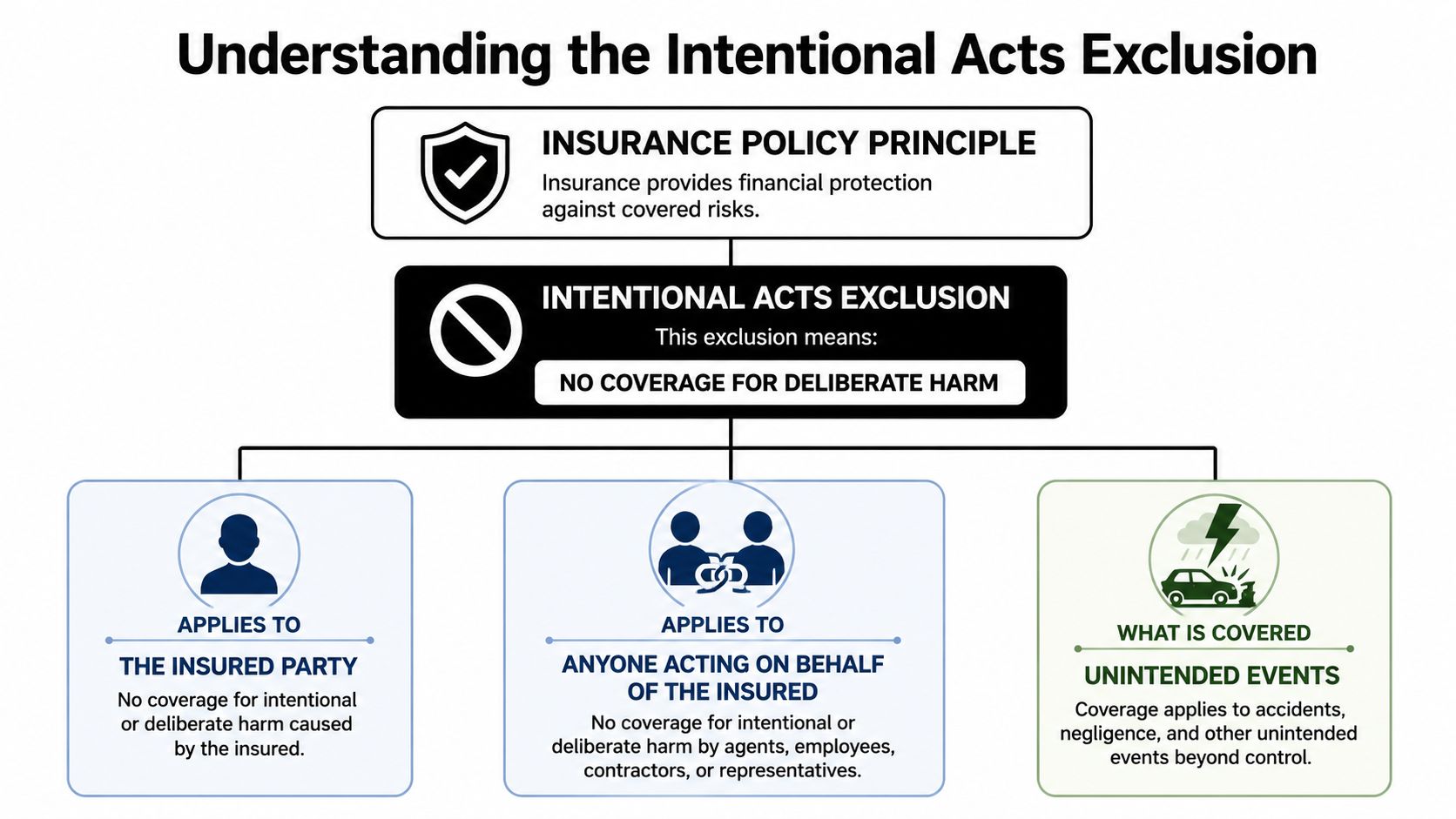

Understanding the Intentional Acts Exclusion

Insurance covers risk. It doesn't cover deliberate destruction by the person who bought the policy.

That principle sits underneath nearly every arson decision. A homeowners policy is meant to respond to sudden, accidental loss. If the insured intentionally causes the loss, the policy usually treats that act as outside the agreement from the start.

What the exclusion means in practice

From a claims perspective, arson is not just a criminal term. It also becomes a coverage issue. If a homeowner set the fire, or if someone in the household set it, the insurer will usually position the loss as an excluded intentional act. The same concern can extend to anyone the insurer believes acted on the insured's behalf.

The easiest analogy is auto insurance. If you accidentally slide into another car on black ice, that's one kind of event. If you intentionally ram your own vehicle into a wall hoping for a payout, that's a different event entirely. Fire claims work the same way. The policy responds to accident, not self-inflicted property loss.

Why identity matters more than the flames

This is why the same burned house can lead to two very different outcomes. The structure damage may look identical. The contents loss may look identical. But coverage can rise or fall based on the identity of the person who started the fire.

What helps homeowners most at this stage is reading the policy with the claim in mind, not just scanning the declarations page. Look for language tied to:

- Intentional loss that excludes damage caused intentionally by an insured

- Resident relatives or household members who may fall within the insured definition

- Duties after loss that require cooperation, records, inventories, and examination

If the carrier has already signaled denial or reservation of rights, it helps to understand the process of fighting an insurance claim denial before giving broad statements or assuming the insurer's position is final.

The central question isn't whether fire is covered. It's whether the insurer can connect the fire to an excluded person under the policy.

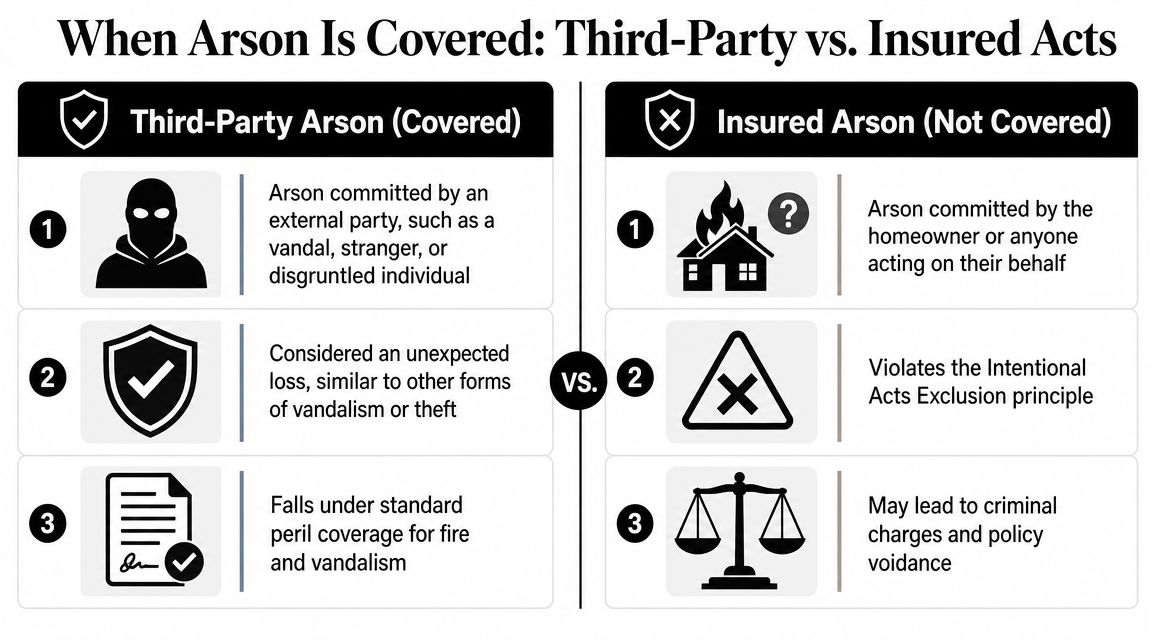

When Arson Is Covered as Third-Party Vandalism

Not every intentional fire is excluded. That's the point many homeowners never hear clearly enough.

If someone else set the fire, a trespasser, stalker, ex-partner, vandal, or another third party, the loss may still be covered. In standard homeowners coverage, arson is generally covered only when it was committed by someone other than the insured or a household member. If the policyholder intentionally sets the fire, insurers typically deny the claim and may treat it as fraud. That distinction follows the core legal difference between an accidental covered peril and an intentional loss under the policy Mercury Insurance fire damage coverage guidance.

Scenario A and Scenario B

Here's how I explain it to clients when the facts are still developing.

| Scenario | Likely coverage position | What usually matters most |

|---|---|---|

| Third-party fire setting | Potentially covered | Proof that the insured wasn't involved |

| Fire set by insured or household member | Usually denied | Evidence tying the loss to an excluded intentional act |

The challenge is that insurers don't take a homeowner's word for Scenario A. They investigate.

What works in a third-party claim

A third-party arson claim usually succeeds or fails on the quality of the file. Strong files tend to include several kinds of support that fit together:

- Official reports that identify the fire as suspicious or incendiary and document the scene

- Access evidence such as broken locks, forced entry, security footage, alarm history, or witness observations

- Timeline evidence showing where the insured was, who discovered the fire, and who had the ability to enter

- Property records and inventories that support the amount of loss without overstating it

A practical point matters here. The insurer may internally discuss arson, fraud, vandalism, malicious mischief, or intentional loss, but the coverage outcome often turns less on the label and more on whether the facts support third-party causation.

What doesn't work

Homeowners damage their own claims when they create avoidable inconsistencies. Common examples include:

- Guessing at facts during a recorded statement

- Throwing away damaged property too early before it can be inspected

- Submitting inflated inventories that make the whole file look unreliable

- Letting contractors alter the scene before the origin investigation is complete

If the insurer believes the homeowner had involvement, even indirectly, the claim can move from ordinary adjustment to fraud-focused investigation very quickly. At that point, casual conversations with the carrier become risky.

A suspicious fire claim is not the place for rough estimates, memory-based timelines, or off-the-cuff explanations.

How Insurance Companies Investigate Arson Claims

Fire claims draw scrutiny because the losses are large. House fires caused 2,620 deaths and $6.9 billion in property damage in a recent five-year period, and the average residential restoration cost reached $27,175 according to The Zebra's summary of house fire statistics. When financial exposure is that high, insurers investigate suspicious losses carefully.

Who usually gets involved

Most suspicious-fire claims involve several people with different jobs.

- Fire department and fire marshal personnel document the emergency scene and may form an early opinion about origin and cause.

- The insurer's field adjuster handles the claim file, gathers records, and coordinates inspections.

- Origin and cause investigators examine burn patterns, ignition sources, scene conditions, and physical evidence.

- Special investigation personnel may become involved if the carrier sees fraud indicators.

If you've never handled a major property loss, it helps to understand the different professionals who may appear in the file, including the role of surveyors and other specialists in insurance claims.

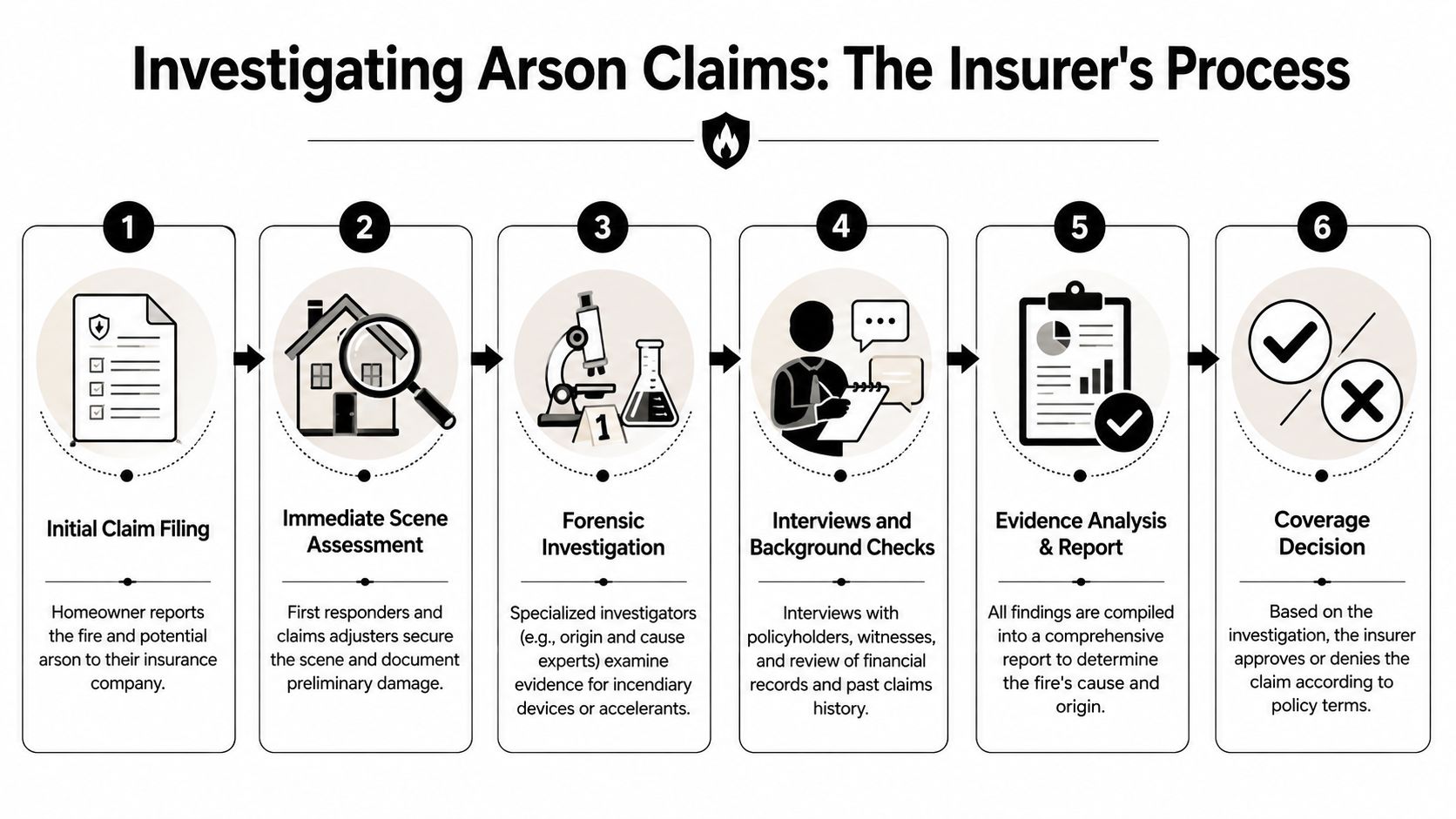

The investigation usually follows a pattern

The exact order varies, but the process often looks like this:

First notice of loss

The insurer opens the claim and flags it for fire review.Scene preservation

The carrier wants the property secured and the fire area left as intact as possible for inspection.Cause and origin inspection

Investigators examine where the fire began, how it spread, and whether there are signs of intentional ignition.Recorded statements or formal questioning

The insured may be asked about finances, occupancy, relationships, repairs, access to the home, and events leading up to the loss.Document review

The insurer may request receipts, ownership records, photos, bank or utility records, inventories, and proof of occupancy.Coverage decision

The carrier either pays, partially pays, reserves rights, or denies.

What raises concern for insurers

Insurers look for inconsistency more than drama. They compare what the scene shows against what the homeowner says. If a policyholder says no one had access, but a witness says the back door had been left open for days, that matters. If the house was under renovation, sparsely furnished, or temporarily empty, that affects how the investigation develops.

Some investigations also become more formal than homeowners expect. A carrier may request extensive records or a detailed sworn interview. That doesn't automatically mean the claim will be denied. It does mean the insurer is building a file that can support either payment or denial.

Cooperating with an arson investigation matters. So does answering carefully, accurately, and only after you've reviewed the facts.

Actionable Steps for Homeowners After a Fire

The strongest arson-related claims start with disciplined early steps. An important point many homeowners miss is that the insured often bears the burden of proving a third party caused the fire, and claim success can turn on the quality of police reports, witness statements, and forensic findings, as explained in Insurance.com's coverage discussion on arson and homeowners insurance.

The first moves that protect your claim

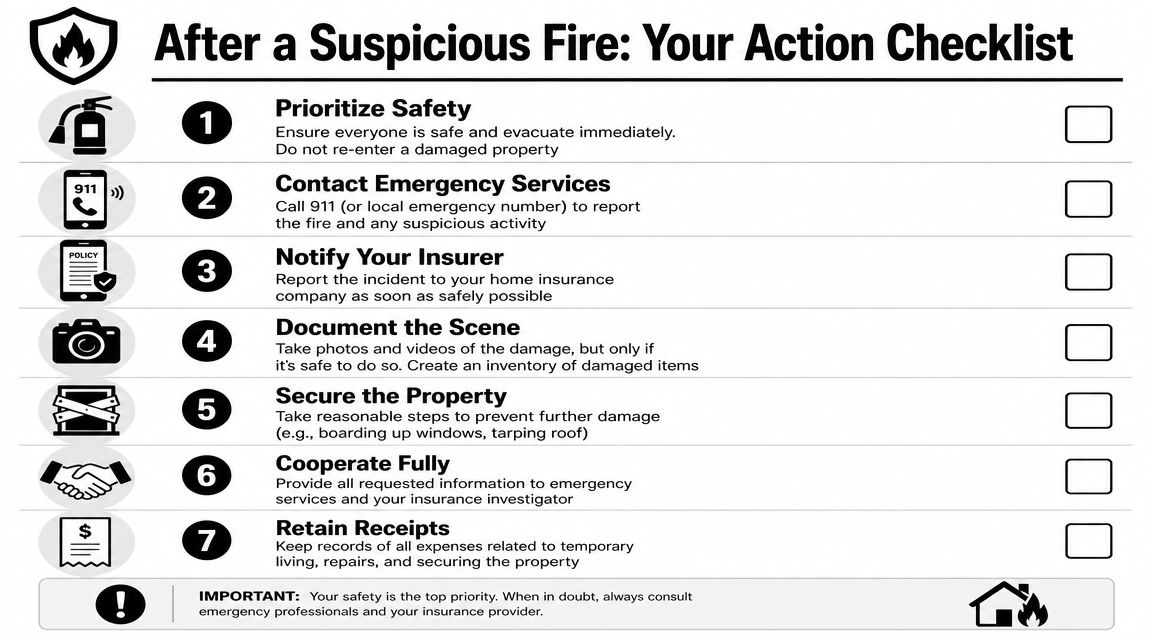

Get everyone safe first

Don't re-enter for pets, documents, or valuables unless fire officials clear it. A bad injury will complicate everything else.Make sure law enforcement is involved if the fire seems suspicious

If someone threatened you, if entry was forced, or if the circumstances don't add up, report that clearly. Don't assume the fire department already captured every detail.Notify the insurer promptly

Report the loss without trying to solve the cause on the first call. Give basic facts. Confirm the claim number. Ask what emergency steps they want documented.

Build an evidence file, not just a claim file

At this point, disciplined homeowners separate themselves from homeowners who get trapped in delays.

- Photograph broadly first so you preserve the overall condition of rooms, points of entry, detached structures, and the exterior.

- Create a timeline with times, phone calls, who arrived when, who had keys, and any prior threats or suspicious activity.

- List damaged property by room instead of trying to build one giant inventory from memory.

- Keep every receipt for hotel stays, meals that exceed your normal routine because of displacement, boarding, tarping, emergency cleaning, and temporary security.

Use a single folder, digital or paper, for every report, email, invoice, and note. If you later need help with the steps to take after a house fire insurance claim begins, that organized file will save time and reduce contradictions.

Avoid the mistakes that create leverage for the carrier

Some of the biggest problems are self-inflicted.

- Don't authorize major demolition too early. The origin area may still need inspection.

- Don't guess in a recorded statement. If you don't know, say you don't know.

- Don't hire the first cleanup or repair company that knocks on your door. After a fire, desperate owners often sign broad work authorizations they later regret. Before committing, this checklist of questions to ask before hiring a contractor is useful because it forces clear discussion about scope, pricing, documentation, and who is ultimately responsible for insurance coordination.

- Don't hand over incomplete inventories as final. It's better to submit a careful preliminary list than a rushed list full of errors.

When professional help makes sense

If the loss is large, the cause is disputed, or the insurer is requesting extensive documentation, outside claim help may be appropriate. A public adjuster can organize the damage presentation, prepare inventories, review policy duties, and manage communication with the insurer. For Oregon and Washington property owners, NW Claims Management is one example of a licensed public adjusting firm that handles fire-related property claims on behalf of policyholders rather than insurers.

Arson Claim Rules in Oregon and Washington

Oregon and Washington homeowners deal with the same core coverage rule, but claims are still handled inside state-regulated insurance systems. That matters when you have complaints about delay, unclear requests, or conduct that feels outside normal claim handling.

In Oregon, homeowners can look to the Oregon Division of Financial Regulation for insurance oversight. In Washington, the relevant regulator is the Washington Office of the Insurance Commissioner. These agencies don't replace legal advice or adjust the loss for you, but they are the bodies that oversee insurer conduct and licensing in each state.

Vacancy can change the entire analysis

A suspicious fire in a vacant home creates a different claim posture than a suspicious fire in an occupied primary residence. Recent consumer guidance notes that standard policies may exclude losses in homes vacant for 30 to 60 days, which can complicate coverage when arson is suspected consumer guidance on whether insurance protects a home after it burns down.

That issue comes up often with inherited homes, rental turnovers, homes under renovation, and properties waiting for sale. The homeowner may focus on the fire itself. The insurer may focus first on occupancy status, policy conditions, and whether the property fit the definition of vacant at the time of loss.

Why local claim representation matters

Licensed public adjusters in Oregon and Washington work inside those state rules and can help policyholders respond to documentation requests, scope building damage, and present the loss coherently. If you want a better sense of the technical side of claim handling, the background on claims adjuster training and evaluation methods helps explain why carriers document these files so methodically.

For Pacific Northwest claims, the local details often matter as much as the broad coverage rule. A vacant Portland home under renovation and an occupied Spokane residence with forced entry don't present the same issues, even if both involve suspected arson.

Navigating Your Claim with Confidence

Three truths control most arson-related homeowners claims.

First, coverage usually depends on who set the fire. A third-party act may be covered. The insured's own intentional act usually isn't.

Second, the insurer isn't just valuing damage. It's testing the story against the scene, the records, and your statements. That's why suspicious-fire claims feel more invasive than ordinary property losses.

Third, the homeowner's documentation often decides whether a borderline file gets paid or denied. Clear timelines, preserved evidence, complete inventories, and careful communication do more to protect a claim than emotional arguments ever will.

If you're also sorting through other property-loss issues, it can help to compare how documentation works across claim types. This guide to successful storm claims is useful for that reason. Different peril, same practical lesson: the file that gets built early shapes the result later.

A suspicious fire claim is stressful, but it isn't unmanageable. Stay factual. Preserve the scene. Keep records. Don't rush into statements or repairs that weaken the evidence. When the claim gets complicated, bring in qualified help before the insurer's version of events hardens into a denial.

If you're dealing with a suspicious fire loss in Oregon or Washington, NW Claims Management can review the claim, help document the damage, and represent your interests through the insurance process. A public adjuster works for the policyholder, not the carrier, which can be especially important when cause, occupancy, and proof are all under scrutiny.