You filed a property claim because something went wrong. A pipe burst. A windstorm tore up the roof. A fire left part of your home unlivable. You expect the insurance company to focus on the damage, the scope of repairs, and how fast they'll pay.

Then the conversation shifts.

The adjuster starts asking for old purchase records, prior inspection reports, renovation permits, and details from the original application you signed when you bought the policy. Suddenly the claim isn't about what happened last week. It's about whether they can reopen what happened years ago.

That shift is a problem. It often signals post claim underwriting, and if you're a homeowner in Oregon or Washington, you need to recognize it early and respond with discipline.

The Unexpected Investigation After Your Claim

A homeowner in the Pacific Northwest reports a water loss. The kitchen floor is damaged, lower cabinets are swollen, and moisture has moved into the wall cavity. At first, the claim looks routine. The carrier assigns an adjuster, asks for photos, and schedules an inspection.

Then the tone changes.

The insurer asks for the original policy application. Next comes a request for prior repair invoices, old inspection reports, and any records showing when the plumbing was updated. Then they ask whether there were any prior leaks before the policy started. The focus moves away from the damaged kitchen and toward the history of the house.

That's where many policyholders get blindsided. They think, “Why are we talking about paperwork from years ago? The damage is right here.”

Because the insurer may be testing whether it can challenge the policy itself, not just the claim.

When a normal claim starts feeling abnormal

A normal investigation looks at cause, extent of damage, scope of repair, and policy coverage. An abnormal one starts digging backward into whether you should've been insured in the first place.

Sometimes that overlap appears alongside other aggressive claim tactics, including deep technical reviews and specialty inspections. If your insurer suddenly broadens the inquiry, it helps to understand how a forensic investigation in an insurance claim can be used and where that process stops being reasonable.

Practical rule: If the insurer's questions have less to do with your damage and more to do with your original application, stop treating it like a routine delay.

Why this feels so frustrating

You paid premiums. You reported the loss. You cooperated. Then, when you need coverage, the insurer starts acting like the actual issue is something buried in old paperwork.

That frustration is valid. Most policyholders never expect the claim process to turn into a retroactive eligibility review. But that's exactly what can happen, and if you miss the signs early, you can hand the insurer the material it will later use against you.

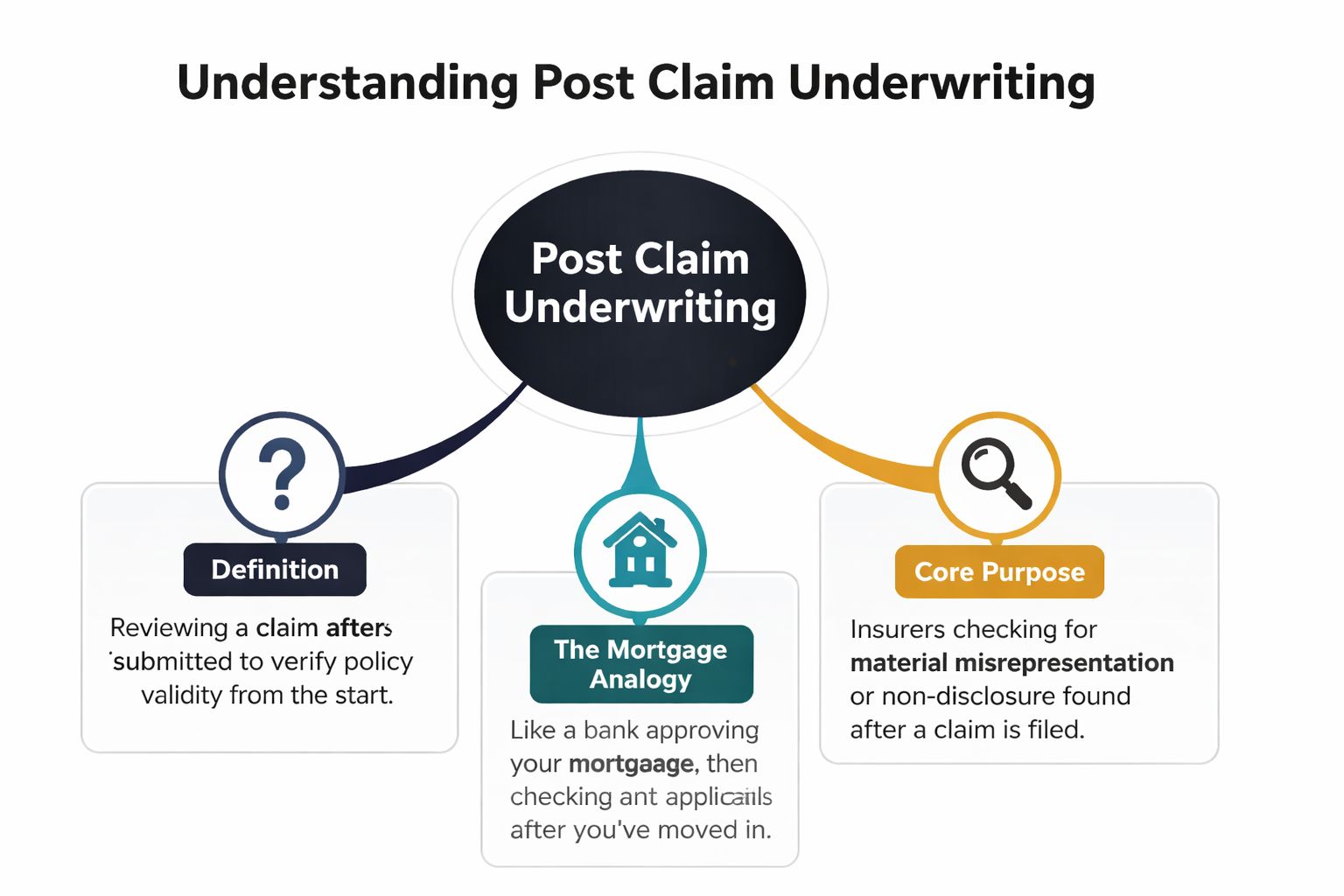

What Is Post Claim Underwriting

Post claim underwriting is simple to define and ugly to experience.

It's when an insurer performs underwriting after a claim is filed, instead of doing that work before issuing the policy. A legal summary explains that courts and scholars often treat it as a form of bad faith, and it cites the Wyoming Supreme Court's description of the practice as a failure to do actual underwriting until after a claim is made, exposing policyholders to losing coverage when they need it most, as outlined in this legal analysis of post-claim underwriting.

The mortgage analogy that makes it obvious

Think of it this way.

A bank approves your mortgage, closes the loan, and lets you move into the house. Years later, after storm damage hits, the bank says it wants to re-check your original application to see whether it should cancel the loan retroactively. Any homeowner would call that unfair.

That's the logic problem with post claim underwriting. The insurer took your premium, issued the policy, and accepted the risk. After a loss happens, it goes backward and asks whether it can undo that decision.

What it looks like in the real world

This tactic usually shows up when the insurer stops focusing on the current loss and starts building a file around policy issuance. It may ask what you knew about prior damage, whether the property condition matched the application, or whether repairs and updates were disclosed clearly enough.

That's not the same thing as ordinary claim handling. It's a deeper challenge to policy validity.

A lot of carriers now run increasingly digital workflows from quote to bind. That speed can create incomplete records, checkbox errors, and thin documentation. When that happens, insurers may later lean on internal systems and application data rather than on common sense. If you want to understand how modern carriers structure those data-heavy processes, this overview of an insurance claim management system helps explain why claim files can expand fast once a dispute begins.

If the insurer approved the policy first and started asking underwriting questions only after your loss, you should assume the stakes just changed.

Why Insurers Use This Tactic

Insurers use post claim underwriting for one reason. It gives them another path to reduce or avoid payment.

That doesn't make the tactic fair. But it does make it predictable.

The financial pressure is real. The U.S. property and casualty insurance industry reported a net underwriting loss of $7.1 billion in 2022, and that pressure can incentivize aggressive post-claim reviews when carriers want tighter control over claim costs, according to this summary of property and casualty underwriting results.

Cost pressure changes behavior

When claim severity rises and underwriting results tighten, some carriers start looking harder at anything that could support a denial, limitation, or rescission. A large property loss creates immediate exposure. If the insurer can shift the conversation from “what's covered” to “was the policy valid,” it gains an advantage.

That's why post claim underwriting often appears on larger or more complicated losses. The bigger the payment risk, the stronger the temptation to revisit the application.

Digital applications create openings

Older insurance transactions often involved more agent interaction and more back-and-forth before binding. Today, many policyholders complete applications quickly online. That speed is convenient, but it can produce bad records.

Here's where insurers take advantage:

- Checkbox ambiguity: A homeowner answers based on what they reasonably understand. Later, the carrier reads the question in the narrowest possible way.

- Thin property descriptions: Online forms don't always capture the actual condition, age, or repair history of a house.

- Missing context: A short application rarely tells the whole story behind prior water damage, roof repairs, or renovations.

That doesn't mean every insurer is hunting for fraud. It means the process itself can create gaps that become useful only after a claim lands.

Investigation and suspicion are not the same thing

Insurers are allowed to investigate claims. They are not entitled to turn every claim into a retroactive trap.

If you want to see how legitimate fraud inquiries are supposed to be framed, this insurance fraud investigation guide is useful because it separates actual investigative discipline from broad fishing expeditions. That distinction matters.

Carriers also operate inside formal risk structures long before a loss occurs. This breakdown of risk management in insurance companies helps show why an insurer's failure to do enough upfront work shouldn't become your burden after the fact.

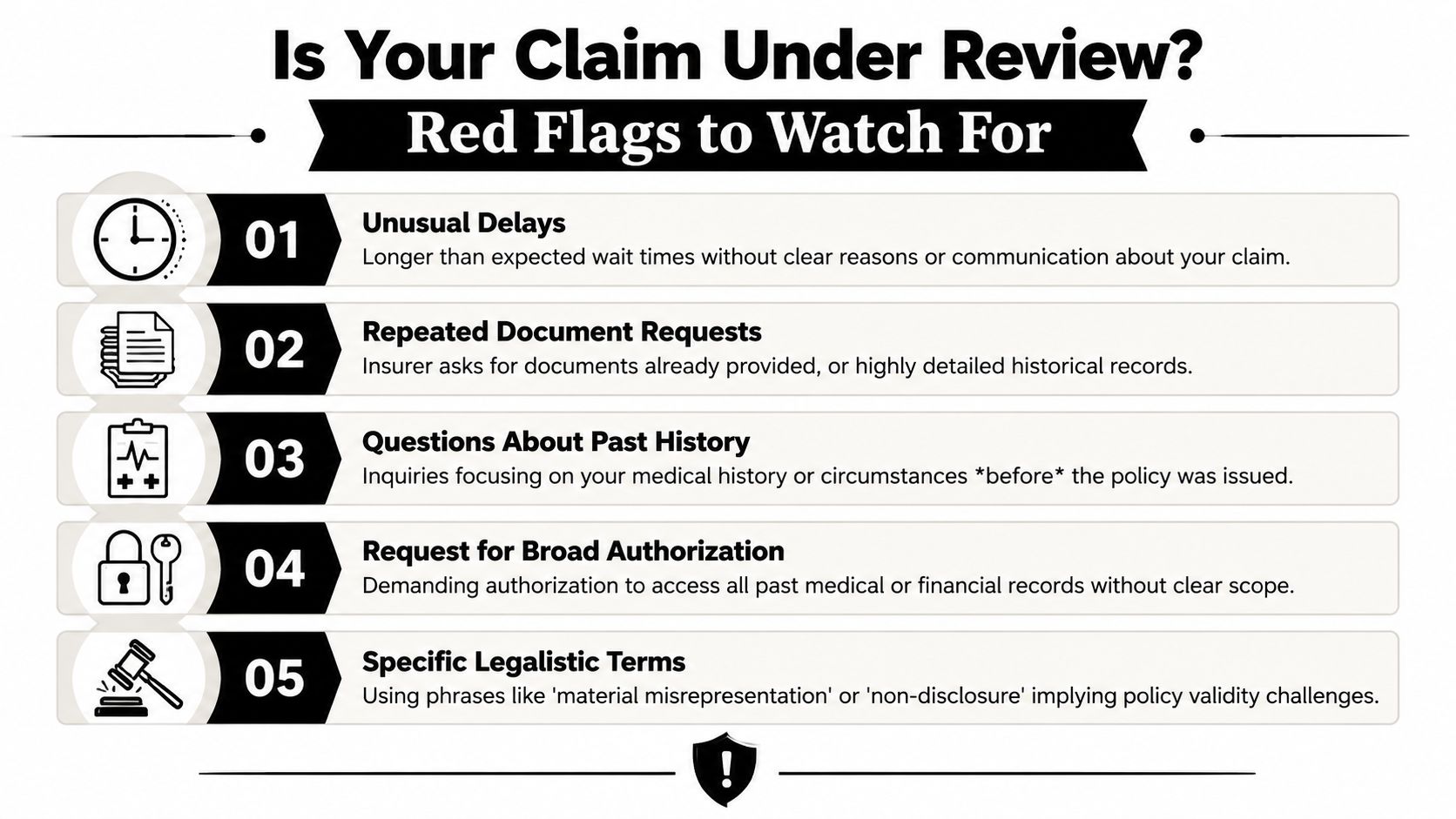

Red Flags Your Claim Is Under Post Claim Review

Post claim underwriting rarely arrives with a clean label. The insurer won't send a letter saying, “We're now looking for a reason to void your policy.” It shows up in behavior.

The clearest signal is when the evidence gathering shifts to retroactive verification. A policy analysis notes that this can include requests for old inspection reports or permits that were not part of the original application, creating a path toward rescission if the insurer treats any mismatch as material, as discussed in this review of retroactive verification in post-claim underwriting.

What you'll notice first

Most homeowners don't spot the issue from a legal term. They spot it from the pattern.

- The questions go backward in time. The adjuster spends more effort on what the home looked like before the policy started than on the current damage.

- Document requests widen without a clear reason. You already sent the claim photos and mitigation invoices, but now they want permit history, purchase documents, prior inspection records, or contractor files.

- The insurer repeats requests. That can mean they're building a paper trail, testing consistency, or hoping you'll say something imprecise.

Phrases that should get your attention

Certain wording should put you on alert immediately.

| Insurer language | What it may mean |

|---|---|

| “Material misrepresentation” | They may be preparing to argue that something on the application mattered enough to affect coverage |

| “Non-disclosure” | They may claim you left out information, even if you didn't think it was significant |

| “Reservation of rights” | They are investigating coverage while preserving the right to deny later |

| “Please provide broad authorization” | They want access to records beyond what's needed for the present damage |

Property claim examples in Oregon and Washington

For a Pacific Northwest property owner, common triggers can include older roof conditions, prior water intrusion, permit history, wood rot, foundation issues, vacancy questions, and prior repairs after storm events. Insurers may also ask about remodeling work, detached structures, or whether the home was owner-occupied in the same way the application described.

The claim should be about the loss. When the insurer starts auditing the policy's origin, treat that as a separate threat.

One red flag matters less than a pattern

A single request for an old record doesn't prove post claim underwriting. A cluster of unrelated, backward-looking requests usually does.

If you receive a broad records request, a reservation-of-rights letter, and a demand for a recorded statement about the application, don't wing it. That's when homeowners get trapped by trying to be “helpful” without realizing the insurer is changing the battlefield.

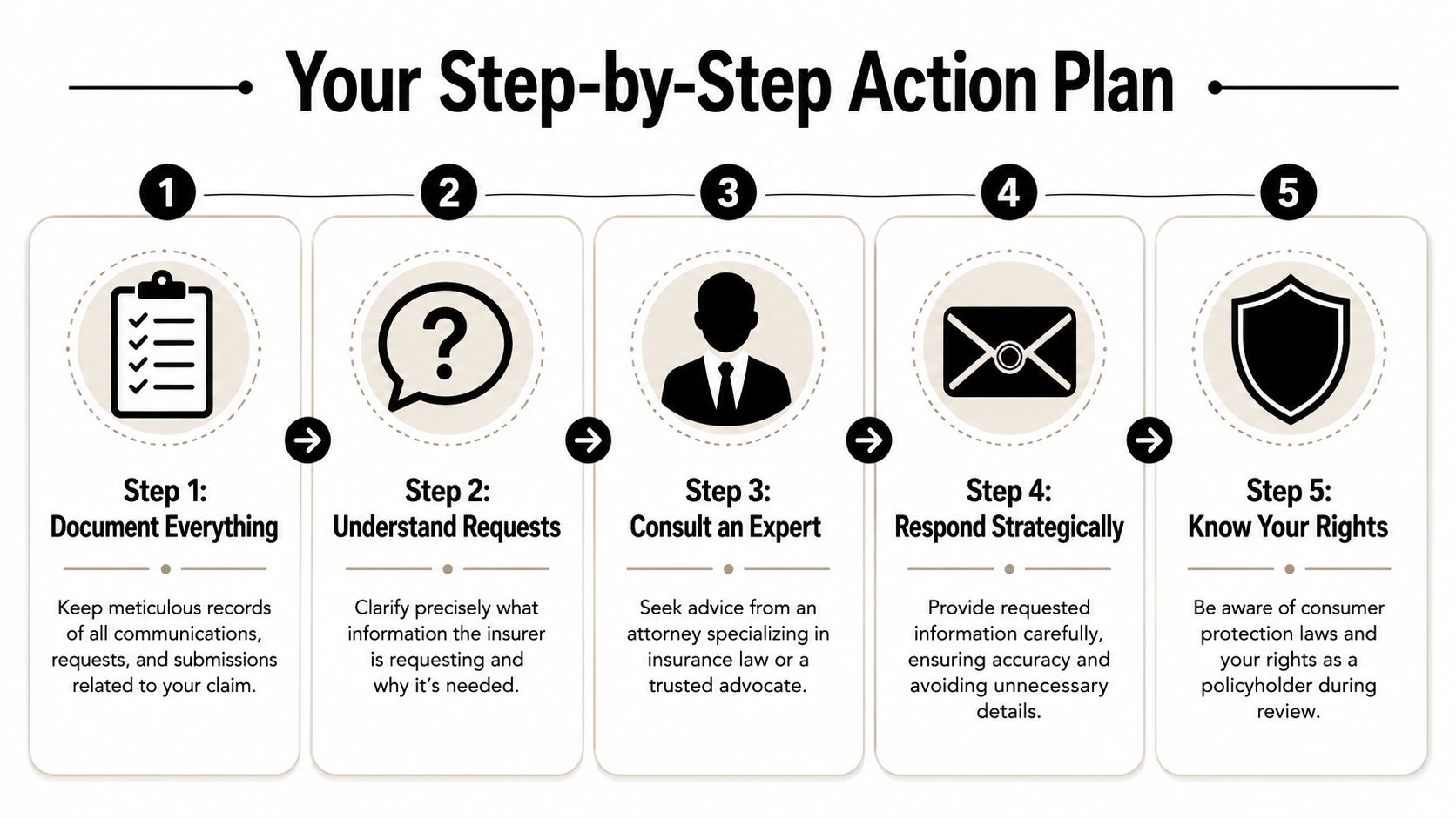

Your Action Plan When Facing Post Claim Underwriting

Stop reacting emotionally and start acting strategically. You do not need to be combative. You do need to be organized.

The insurer has people, systems, and templates working this file. You need a process too.

Start with control of the paper trail

Build one claim file immediately. Put everything in it.

Include your policy, declarations page, endorsements, any application documents you have, renewal notices, emails, letters, text messages, inspection reports, mitigation invoices, contractor proposals, photos, and a running timeline of every conversation. If you had a phone call, write down the date, time, who called, and what was said.

That file matters because insurers often move faster than policyholders when facts get muddy.

Five moves that protect you

Put communication in writing whenever possible

Phone calls create ambiguity. Email creates a record. If a call happens, send a follow-up email summarizing it.Ask why each request is relevant

You don't have to refuse every document request. But you should understand what the insurer is asking for and how it relates to the current claim.Be accurate, not expansive

Don't guess. Don't fill silence with speculation. Don't volunteer extra history because you think it makes you look cooperative.Be careful with recorded statements

If the insurer wants a recorded statement about your application, prior property condition, or what you “knew” before policy inception, slow down. Those statements can become the center of a later denial.Get help early

Once post claim underwriting starts, this is no longer a simple paperwork issue. It becomes a claim strategy problem.

What not to do

A lot of policyholders damage their own file trying to seem reasonable.

- Don't guess about dates. If you're unsure, say you need to verify.

- Don't adopt the insurer's wording. Their phrase “misrepresentation” is not your phrase.

- Don't sign broad authorizations casually. Read the scope first.

- Don't assume delay means approval is coming. Delay often means review is deepening.

Client-side rule: Your job is to provide truthful, supportable information. Your job is not to help the insurer build a rescission theory.

Bring in a professional before the file hardens

Once the insurer has framed the dispute around old disclosures, the claim can turn fast. An experienced advocate can help separate legitimate claim questions from overreach, tighten your documentation, and keep communication disciplined.

If you're unsure whether your file has crossed that line, read this guide on when to hire a public adjuster. The biggest mistake is waiting until the denial letter arrives. By then, the insurer has often shaped the story.

A simple response script

If you feel pressured on the phone, use this:

“I want to cooperate fully. Please send your request in writing, identify the documents you need, and explain how they relate to my claim.”

That response is calm, professional, and protective. Use it.

Oregon and Washington Rules and Protections

Oregon and Washington policyholders are not powerless here. Both states regulate insurer conduct, and post claim underwriting can overlap with bad faith and unfair claim handling issues.

A legal discussion of the doctrine notes that many legal experts and some courts treat post-claim underwriting as per se evidence of bad faith because the insurer failed to do its diligence before the claim was filed, which is why the issue carries weight in state consumer protection settings, as explained in this article on post-claim underwriting and bad faith.

What that means in practice for Oregon homeowners

If you live in Oregon, don't assume an insurer can casually rewrite the basis of the policy after a loss and get away with it. The carrier still has to justify its position within Oregon's claim handling framework.

That matters because some disputes are not really about whether damage occurred. They're about whether the insurer is trying to convert a claim investigation into a policy avoidance strategy.

If you need local guidance specific to the state's claim environment, this resource on working with a public adjuster in Oregon explains the role a licensed advocate can play during a property dispute.

What Washington property owners should keep in mind

Washington policyholders also benefit from consumer protection rules and oversight. In practical terms, that means the insurer's process matters, not just its conclusion.

If the carrier asks for broad historical records, delays without explaining the basis, or pivots toward allegations tied to the original application, treat that as a conduct issue as well as a coverage issue. The paper trail becomes critical.

State regulators can help, but they don't manage your claim for you

Oregon homeowners can contact the Oregon Division of Financial Regulation. Washington homeowners can contact the Washington Office of the Insurance Commissioner. Those agencies are important. They can receive complaints and review insurer conduct.

But regulators usually won't build your estimate, organize your damage file, or negotiate scope and valuation for you. Their role is oversight. Your role is still to protect the claim.

The practical standard to follow

Here's the rule I give property owners in the Northwest:

- Treat vague legalistic letters seriously

- Respond carefully and on time

- Keep every record

- Separate real claim issues from policy-origin attacks

- Escalate fast when the insurer starts reaching backward

If your insurer is handling the loss fairly, good. If it isn't, you need to act like the file may later be reviewed by a regulator, an appraiser, or a court.

FAQ About Post Claim Underwriting

How is this different from a normal claim investigation

A normal claim investigation asks what happened, what was damaged, what caused it, and what the policy covers. Post claim underwriting asks whether the insurer can revisit the policy application or property history to challenge the policy itself.

Can my policy really be canceled if I paid premiums on time

Yes, insurers may try. Paying premiums does not always stop a carrier from arguing rescission or retroactive cancellation. That's why these disputes are serious. Premium payment helps your position factually, but it doesn't end the argument by itself.

What does rescission mean

Rescission means the insurer tries to treat the policy as if it should not have been issued in the first place. In plain language, it's an effort to unwind the contract retroactively.

Should I give a recorded statement

Not casually. If the questions go beyond the current damage and start probing your original application, prior property condition, or alleged non-disclosure, slow the process down and get advice first.

Will hiring a public adjuster make the insurance company angry

A professional insurer shouldn't get “angry” because you have representation. More important, this is not about keeping the carrier comfortable. It's about protecting your rights, your file, and your recovery.

What if I already answered some bad questions

Don't panic. Gather the emails, letters, recordings if available, and your own notes. Then get the file reviewed. Early mistakes can often be managed better than homeowners think, especially when the insurer's requests were vague or overbroad.

If your Oregon or Washington property claim has shifted from damage assessment to old application questions, broad records requests, or allegations of misrepresentation, don't handle it alone. NW Claims Management represents policyholders, not insurers, and helps homeowners, businesses, nonprofits, and public entities push back when a legitimate claim starts turning into a policy dispute. Reach out for a free claim evaluation and get a clear read on where your file stands before the insurer defines it for you.