The first hours after a major property loss rarely feel orderly. A homeowner is standing in wet drywall and soot, trying to remember what was in the back bedroom. A restaurant owner is looking at a shut-down kitchen, spoiled inventory, and a landlord who still expects answers. The insurance carrier wants a claim opened right away. Contractors start calling. Family, staff, tenants, and customers all need direction.

That's the moment when people usually realize the claim itself is now a second emergency.

Most policyholders don't deal with large losses often enough to know what to photograph, what to save, what to say, or what not to sign. They know something is wrong. They usually don't know how quickly a claim can get narrowed by incomplete documentation, rushed inspections, or a settlement scope that misses hidden damage.

Home and business public adjusters exist for that exact moment. Not to add drama, but to take control of the claim file before important facts are lost.

After Disaster Strikes You Are Not Alone

A family gets back into the house after the fire department leaves. The obvious damage is easy to see. Burned framing, broken windows, soaked floors. The less obvious damage starts showing up later. Smoke in the HVAC system. Water trapped behind cabinetry. Odor in soft goods. A list of missing contents that no one can fully remember on the first night.

A business owner faces the same confusion in a different form. The storefront may still be standing, but operations are frozen. Equipment is damaged. Records are scattered. Staff need updates. The insurance process starts asking technical questions before the owner has had time to stabilize the business.

That's where many claims go sideways. People assume the insurance company's process will naturally uncover every loss category. It often doesn't. A large property claim rewards whoever documents best, ties damage to policy language, and stays organized under pressure.

When your property is damaged, your first job is safety. Your second job is preserving evidence.

In the middle of that chaos, practical help matters. If a fire has displaced your household, local community resources such as assistance for fire relief can help with immediate needs while the insurance side gets sorted out. That kind of support can buy time to make better claim decisions instead of rushed ones.

What property owners should do first

- Protect life and health: Don't re-enter unsafe structures, and follow fire, utility, or emergency instructions.

- Document before cleanup: Take photos and video of every room, exterior elevation, mechanical area, and damaged item before disposal.

- Save early paperwork: Keep emergency repair invoices, hotel receipts, board-up bills, and any notices from the insurer.

- Slow down on statements: Give factual notice of the loss, but don't guess about cause, scope, or price.

A public adjuster becomes the person handling the claim when you're still trying to get your footing. That shift matters more than is often realized.

Your Advocate in a Crisis What Is a Public Adjuster

A public adjuster is a licensed insurance claims professional who represents the policyholder, not the insurance company. That's the key distinction. In a serious loss, that difference affects inspection strategy, documentation standards, valuation, and negotiation.

Think of the three adjuster roles this way. If a claim is a dispute over what must be paid, the company adjuster is on the insurer's side of the table. The independent adjuster may be an outside contractor, but still works for the insurer on that claim. The public adjuster sits beside the policyholder and builds the case for coverage and value.

The three roles are not interchangeable

- Public adjuster: Represents the insured and prepares, documents, and negotiates the claim on the insured's behalf.

- Company adjuster: Works directly for the insurance carrier.

- Independent adjuster: Is hired by the insurance carrier for claim handling, but still serves the carrier's interests on that file.

Core legal point: Public adjusters operate under a fiduciary duty exclusively to the policyholder. That legal separation enables independent, forensic-level damage assessment and aligns their incentive with the policyholder's recovery through a contingency fee model, according to Sill's guide to public adjuster cost and value.

That fiduciary role is why the relationship matters. A public adjuster doesn't start from the insurer's estimate and only argue over line items. The work starts with the policy, the physical evidence, and the full scope of loss.

Why homeowners and business owners hire one

Home and business public adjusters are usually brought in when the claim is too large, too technical, too emotional, or too disruptive to manage alone. That includes fire losses, water losses, storm damage, vandalism, and complex commercial interruptions.

If you want a straightforward definition of the role, this overview of what a public adjuster is is a useful starting point. The practical test is even simpler. Ask one question: who does this person legally represent on my claim?

If the answer isn't “you,” they are not your advocate.

Home Claims vs Business Claims Different Needs

Residential and commercial claims may start with the same event, fire, water, wind, or vandalism, but they do not unfold the same way. A homeowner is often trying to restore shelter, replace daily-life contents, and manage temporary living arrangements. A business owner is trying to restore operations, protect revenue, answer to customers, and preserve contractual obligations.

Treating those claims the same is a mistake.

Residential losses are personal and inventory-heavy

A home claim usually turns on two things. First, how thoroughly the building damage is scoped. Second, how accurately contents and living-displacement costs are documented. Families often underestimate how much detail insurers expect for personal property. Rooms that look simple on the surface can contain dozens of compensable items once you slow down and list them.

Home claims also carry a strong emotional component. People are making decisions while displaced, tired, and under stress. That's when they miss smoke migration, hidden moisture, code-related repair issues, or the true cost of replacing what was lost.

Commercial losses add operational pressure

A business claim has another layer. The building may be only one part of the damage. Equipment, tenant improvements, stock, records, extra expense, and loss of income can all become central. Timelines matter because every day of delay can affect payroll, vendor relationships, and customer confidence.

For many businesses, the hardest part isn't proving there was damage. It's proving how that damage disrupted operations and what the policy allows during the restoration period. If your claim involves downtime questions, this explanation of the extended period of indemnity helps clarify why some losses continue after repairs are technically complete.

Residential vs Commercial Claim Considerations

| Factor | Residential Claim (Home) | Commercial Claim (Business) |

|---|---|---|

| Main priority | Restore safe living conditions | Restore operations and stabilize cash flow |

| Key documentation | Room-by-room contents list, building damage photos, displacement records | Financial records, equipment lists, repair scope, operational interruption support |

| Hidden issues | Smoke in soft goods, moisture in walls, HVAC contamination | Equipment calibration, partial shutdown effects, tenant obligations, inventory spoilage |

| Decision pressure | Housing, family routines, school, pets | Payroll, customers, leases, vendors, regulatory demands |

| Common mistake | Accepting an incomplete contents valuation | Focusing only on property damage and missing income-related claim elements |

A homeowner often asks, “How do I replace what I lost?” A business owner asks, “How do I keep operating?” The claim strategy has to answer the right question.

The best home and business public adjusters know how to shift between those realities without forcing one claim model onto another.

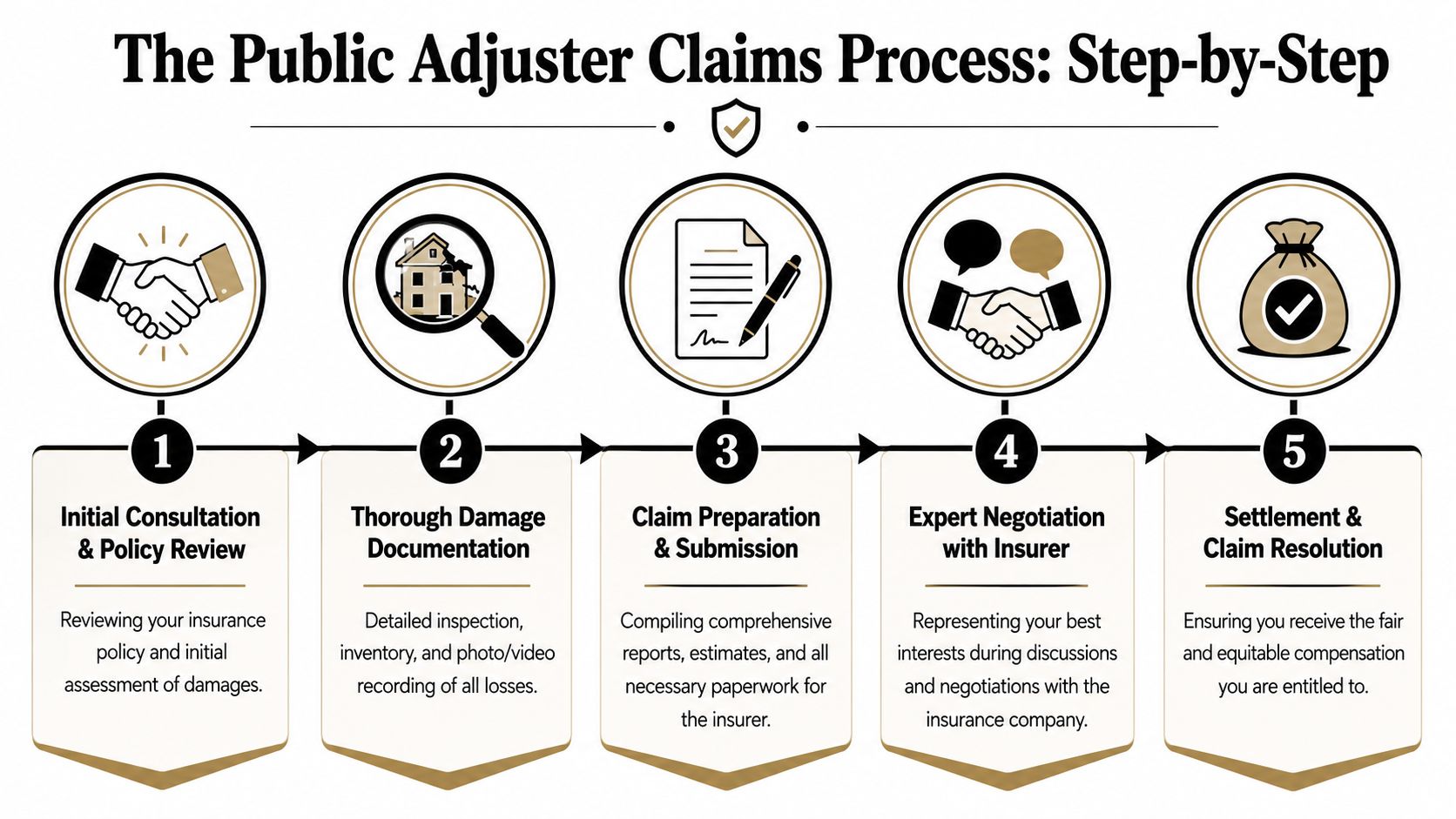

The Public Adjuster Claims Process Start to Finish

Most strong claims follow a disciplined sequence. Not a rushed estimate, not a stack of disconnected photos, and not a phone call hoping the carrier fills in the blanks. The work is methodical because the claim file becomes the proof.

Phase one begins with the policy, not the estimate

The first task is understanding what the contract says. Coverage parts, exclusions, endorsements, valuation language, and duties after loss all shape the path forward. Good claim handling starts by reading the policy carefully before debating price.

That early review also helps avoid self-inflicted problems. Property owners often make avoidable mistakes by discarding damaged materials too soon, missing deadlines, or assuming the carrier's first scope defines the universe of damage.

Phase two is field work and forensic documentation

The next stage is a site inspection with purpose. Public adjusters use tools and support professionals to build a damage record that can survive scrutiny. That can include 3D visual evidence, structural estimating, detailed inventories, and specialist input where needed.

According to Crestview's explanation of public adjuster claim workflow, the technical process includes policy analysis, forensic damage assessment, direct negotiation, and use of tools such as 3D visual evidence and structural estimators. That same source also notes that public adjusters in places like Oregon and Washington operate under state licensing requirements.

What gets built during claim preparation

- Building scope: Room-by-room and system-by-system identification of visible and hidden damage.

- Contents inventory: Itemized personal property or business personal property documentation with enough detail to support valuation.

- Repair and replacement pricing: Estimating based on current market conditions, not guesswork.

- Proof of loss package: Organized submission materials that tie facts to the policy.

The carrier doesn't pay for a feeling that the loss was severe. It pays against documented damage, policy terms, and supported valuation.

Negotiation only becomes effective after that groundwork is done. At this stage, many owners get frustrated if they're handling the claim alone. They may know the offer is short, but they can't yet prove why in a format the insurer has to address.

Phase four and five are negotiation and closure

Once the file is built, the discussion with the insurer becomes more precise. The argument is no longer “this feels too low.” It becomes “this line item is incomplete, this damage category was omitted, this depreciation is unsupported, and this policy provision applies.”

That back-and-forth can involve reinspections, revised estimates, supplemental submissions, and clarification of scope. A practical overview of the home insurance claim process can help property owners understand where those stages fit.

Final resolution doesn't just mean a check arrives. It means the claim has been evaluated for completeness before the file is closed. That's especially important when hidden damage, code issues, or business interruption components tend to surface late.

Rules of Engagement Licensing and Fees in Oregon and Washington

Two questions come up fast after people learn what public adjusters do. Is this legitimate, and how are they paid? In Oregon and Washington, those questions have concrete answers.

Licensing matters in both states

A public adjuster is not merely someone who knows construction or has insurance experience. In Oregon and Washington, public adjusters must be properly licensed and comply with state insurance rules. That matters because licensing sets a legal standard for who may represent policyholders in a claim and how that representation must be handled.

For local property owners, this is one of the easiest screening points. Ask for the state license. Verify that it's active. If the adjuster says licensing is unnecessary, that conversation should end there.

If you want a broader look at the profession and the path into it, this page on how to become a public insurance adjuster gives useful context for what licensed practice involves.

The fee model is contingency based

Public adjusters typically work on a contingency fee, usually 10% to 20% of the final settlement amount. They are paid when the claim is paid. That structure removes the upfront billing problem many property owners can't absorb right after a loss.

The practical question isn't whether there's a fee. It's whether the net result improves the policyholder's position. Verified industry examples show that public adjusters can increase settlements by 40% to 700%, and one simple example illustrates how the math can still favor the client: a claim that increases from $10,000 to $17,000 leaves a $7,000 increase; even with a 20% fee ($3,400), the client still nets $3,600 more than they would have received otherwise.

Trade-offs property owners should understand

- You give up a slice of the recovery: That's real, and it should be discussed plainly.

- You may gain a stronger claim file: Better scoping, fuller documentation, and firmer negotiation can change the outcome.

- Not every claim needs one: Small, straightforward losses may not justify representation.

- Large or disputed claims usually benefit from structure: The more moving parts, the more valuable disciplined claim management becomes.

Plain advice: Don't judge the fee in isolation. Judge the fee against the likely net outcome, the complexity of the claim, and the risk of leaving covered damage undocumented.

That's the right frame for Oregon and Washington property owners. Legitimacy starts with licensing. Value starts with net recovery, not sticker shock.

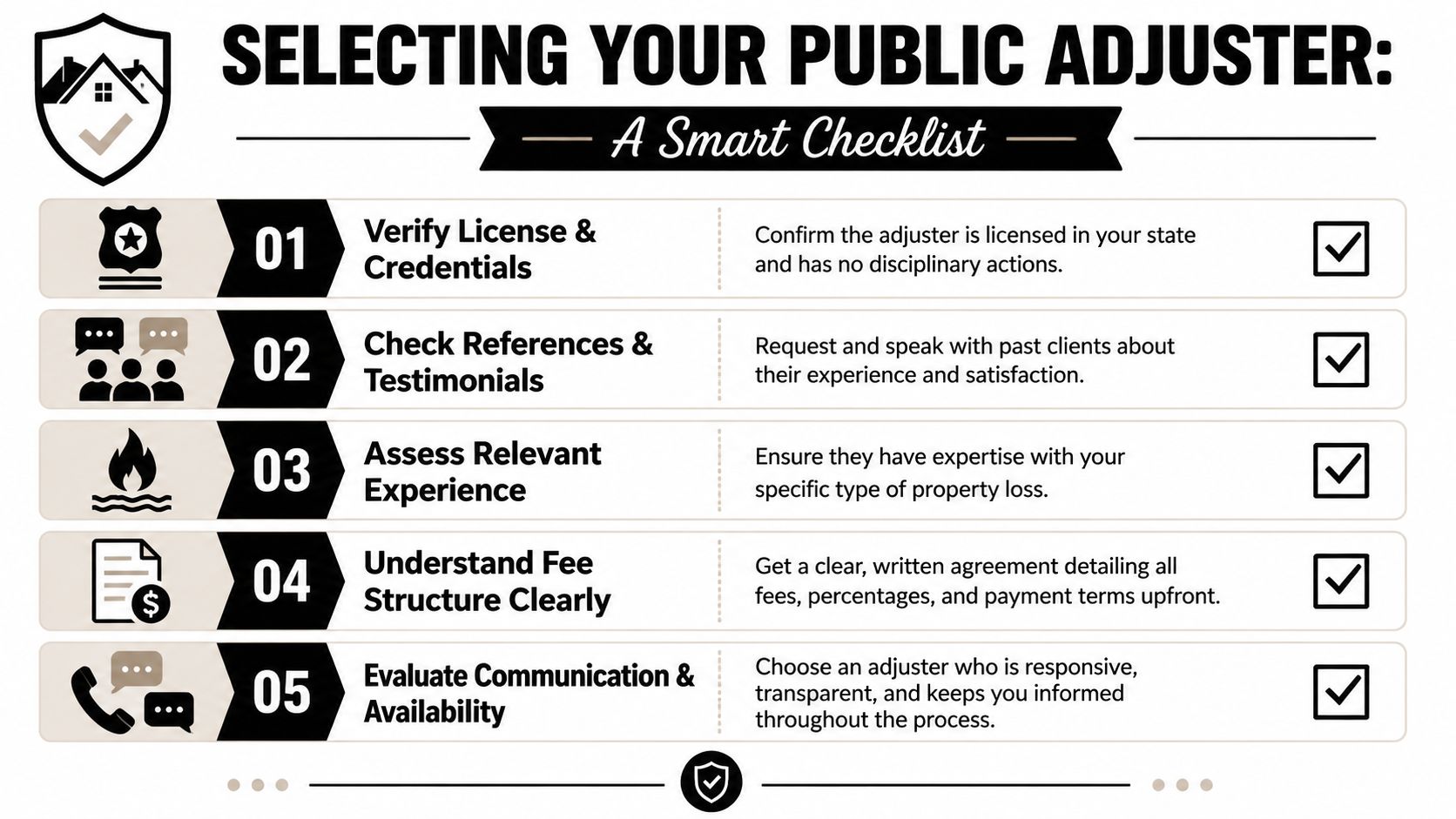

How to Choose the Right Public Adjuster for Your Claim

There are a lot of firms and individual adjusters in the market. The U.S. claims adjusting industry includes approximately 37,176 businesses as of 2025, and the market is projected to reach $10.8 billion in 2026, even though the number of businesses declined at a 0.9% CAGR from 2020 to 2025 while market size grew at a 1.5% CAGR over the same period, according to the industry and labor data summarized in the verified research. In a field that large, selection matters.

Start with verification, then move to fit

A license tells you the person is authorized. It does not tell you whether they're right for your loss. A residential fire claim, a church water loss, and a commercial interruption claim each require different habits, documentation skills, and communication style.

Ask direct questions. Good adjusters won't be annoyed by that. They'll expect it.

Questions worth asking in Oregon and Washington

- Are you currently licensed in my state? Ask for the license details and verify them.

- Have you handled my type of loss before? Fire, water, wind, vandalism, commercial property, nonprofit, and municipal claims all have different pressure points.

- Who will inspect the property and prepare the file? You want to know whether the person you're meeting is the person doing the work.

- How do you document hidden damage? Listen for specifics such as inventories, structural estimating, specialized inspection methods, and support for supplemental claims.

- How do you communicate during the claim? Ask how often you'll get updates and who returns calls.

- What is your fee, in writing? Don't accept vague answers. The contract should be clear.

- What happens if the insurer disputes scope or value? This reveals whether the adjuster has a plan beyond submitting paperwork.

Red flags that deserve caution

- Pressure to sign immediately: Serious professionals understand you're making a stressed decision.

- No written explanation of fees: If the compensation structure isn't clear, stop.

- Promises of a specific payout: No one can guarantee an exact settlement.

- Weak answers about Oregon or Washington rules: Local compliance isn't optional for local claims.

One local option is NW Claims Management's public adjuster services, which outlines policy review, damage documentation, and negotiation support for residential, commercial, and nonprofit claims in Oregon and Washington. Whether you speak with that firm or another, the same rule applies: hire the adjuster who can explain process, not just sell confidence.

Real Results and Your Next Steps with NW Claims Management

When people ask whether representation changes outcomes, the most honest answer is this: it changes the quality of the claim file, and that often changes the result.

A residential example from the verified industry data is straightforward. One claim moved from $22,000 to $68,000 after public adjuster involvement, based on the documented increase examples included in the verified source set. That kind of shift usually comes from a fuller scope, stronger proof of loss, and harder scrutiny of what was left out the first time.

A second example is the fee-and-net-recovery scenario discussed earlier. A claim that rises from $10,000 to $17,000 can still leave the policyholder ahead after the contingency fee because the issue isn't the gross increase alone. It's what the owner keeps after representation.

Commercial claims have another problem now. Verified research notes a 35% surge in automated claim denials for commercial policies in 2025, which makes manual file-building and forced human review more important for businesses and nonprofits facing fast digital denials, as described in this discussion of public adjusters and commercial claim barriers.

If you're in Oregon or Washington and your claim feels larger than your capacity to manage alone, the sensible next step is a professional review. You can compare policy language, damage documentation, and claim strategy before deciding how to proceed.

If you need help evaluating a home, business, nonprofit, or municipal property claim, NW Claims Management offers a no-obligation starting point. A licensed public adjuster can review the loss, explain whether the claim appears under-scoped or under-documented, and tell you plainly whether professional representation makes sense for your situation.