Water is coming through the ceiling. Or your kitchen is blackened after a stove fire. Or a neighbor's failed supply line has warped your floors, soaked your baseboards, and left your unit smelling like wet drywall.

You're standing in the middle of it asking the same questions almost every condo owner asks. Is this covered? Who pays for what? Do I call my insurance company, the HOA, or both? And if you're in Oregon or Washington, you're also dealing with a regional insurance market that has gotten tighter, pickier, and less forgiving about documentation and valuation.

Condo insurance claims are rarely simple. They're a tug-of-war between your association's master policy, your HO-6 policy, the board, the property manager, contractors, and at least one adjuster who does not work for you. If you handle that mess casually, you can leave real money on the table.

That Sinking Feeling Discovering Condo Damage

It usually starts with something small enough to ignore for a minute.

A drip under the sink. A faint stain near the ceiling line. A weird buckling in the hardwood by the patio door. Then you step on the floor in socks and feel the water. Suddenly you're moving furniture, calling the HOA voicemail, trying to shut off a valve you've never touched before, and wondering whether every minute of delay is making the damage worse.

That panic is normal. So is the confusion. Condo owners are often told, “The HOA covers the building.” That sounds reassuring until you realize “the building” may not include your flooring, cabinets, interior paint, built-ins, or upgrades. If the loss is from fire, smoke, or water, you may also have urgent mitigation decisions to make before the insurance side is even sorted out. If fire is involved, this post-fire insurance checklist is a useful starting point.

What owners usually get wrong in the first hour

The first mistake is assuming coverage questions can wait. They can't. Early decisions shape the claim.

The second mistake is cleaning up too aggressively. Mop the standing water. Move property out of danger. But don't tear out damaged materials or throw away evidence before it's documented.

If wood flooring is involved, practical repair timing matters too. A good example is this Savera Wood Floor Refinishing advice on how water affects hardwood and why rushed cosmetic fixes often miss the full scope.

You do not need perfect answers on day one. You do need a clean record of what happened, what was damaged, and who was notified.

The real problem isn't just damage

The damage is only half the problem. The other half is allocation.

In condo insurance claims, insurers and associations often start by sorting responsibility before they talk seriously about money. That means while you're focused on drying the unit and getting back home, the file is already being framed around a harder question: Is this the association's problem, your problem, or both?

That's where most disputes begin.

The Two-Policy Puzzle Master Policy vs HO-6

Condo claims split into building loss and unit-owner loss. That isn't just industry jargon. It drives who inspects, who pays, and who argues over finishes. As Allstate's condo claims overview explains, the adjuster has to determine whether the damaged item falls under the condominium association's master policy, the owner's HO-6 policy, or both. In practice, the claim file needs the declaration pages and bylaws before any estimate should be finalized.

Think of it this way

The master policy usually covers the building's shared structure and common elements. Think skin and bones.

Your HO-6 policy usually covers what makes your unit yours. Think paint-in, personal property, interior finishes, upgrades, and living expenses if the unit can't be occupied.

That sounds clean on paper. It rarely is in real life.

Some associations insure units on a more inclusive basis. Others stop at bare walls. Some declarations put original finishes on the association and upgrades on the owner. Some shift deductibles back to owners depending on the cause of loss. If you don't read the condo declaration and bylaws with your policy in hand, you're guessing.

Master Policy vs. HO-6 Coverage at a Glance

| Damaged Item | Typically Covered by Master Policy | Typically Covered by Your HO-6 Policy |

|---|---|---|

| Roof, exterior walls, hallways, shared plumbing lines | Usually yes | Usually no |

| Drywall framing and common structural components | Often yes, depending on governing documents | Sometimes, if the master policy stops short |

| Interior paint and wallpaper | Sometimes no | Often yes |

| Flooring inside your unit | Sometimes, but often disputed | Often yes, especially upgrades or owner responsibility items |

| Cabinets and countertops | Depends on whether they're original building components or owner improvements | Often yes if not included under the master policy |

| Appliances inside your unit | Usually no | Usually yes |

| Furniture, clothing, electronics | No | Yes |

| Temporary housing and extra living costs | No | Often yes if your policy includes loss of use |

| Liability for injuries inside your unit | No | Usually yes |

What creates the fight

The biggest conflict point is not whether damage happened. It's where the line is drawn.

A water loss from a common pipe may damage drywall, flooring, cabinets, and personal property all at once. The association's carrier may say it covers only the common element repair. Your HO-6 carrier may say it won't move until the master policy position is clear. Meanwhile, the drying bill is real, and your kitchen is unusable.

Common gray areas include:

- Original vs. upgraded finishes: If the builder installed basic flooring but you later installed engineered hardwood, the carriers may split responsibility or deny portions.

- Cause vs. location: A common element failure doesn't automatically mean the master policy pays every damaged item inside your unit.

- Deductible shifting: Some associations assess owners back for deductibles or uninsured portions depending on the bylaws.

- Shared evidence problems: If the HOA or property manager doesn't produce key records promptly, your individual claim can stall.

Practical rule: Never let an insurer finalize scope before you have the HOA declaration pages, relevant bylaws, and the association's coverage position in writing.

If you don't pin down the policy boundary early, the same loss gets chopped into pieces. That's how condo owners end up underpaid without realizing it until repairs are underway.

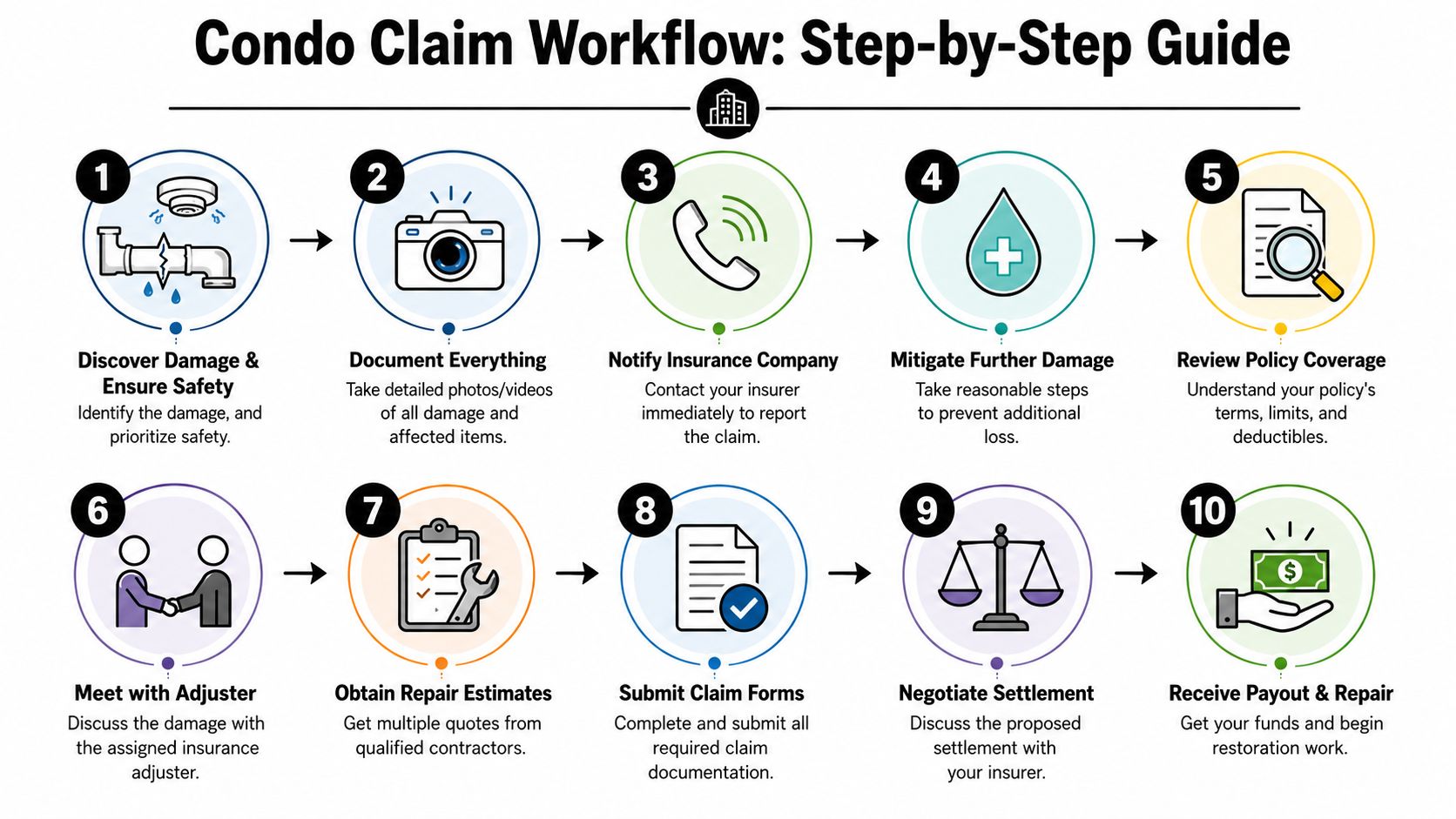

Your Step-by-Step Condo Claim Workflow

When a loss hits your condo, don't wing it. Follow a sequence. Chaos helps the insurer, not you.

For a broader overview of how claims move from notice to payment, this home insurance claim process guide is useful. For water-specific practical tips on mitigation and claim handling, this important water damage claim advice is also worth reviewing.

Step 1 Secure safety and stop additional damage

Turn off water if you can. Shut off power in affected areas if there's active water near outlets or fixtures. If there's fire or smoke damage, don't re-enter unsafe areas just to grab property.

Your policy requires you to take reasonable steps to prevent further damage. That means emergency drying, tarping, board-up, and moving items out of harm's way are usually appropriate. It does not mean tearing out half the unit before anyone inspects it.

Step 2 Notify every party that matters

Notify your insurer. Notify the HOA or property manager. If another unit caused the problem, notify them too in writing.

Keep the notice simple and factual. Include:

- Date and time discovered

- Suspected cause

- Areas affected

- Whether emergency mitigation has started

- A request for the association's insurance information and coverage position

Do this by email if possible. Phone calls disappear. Email creates a record.

Step 3 Build your evidence file before the adjuster arrives

Insurers expect contemporaneous proof of loss. The National Association of Realtors notes that claims documentation should include wide-angle room photos, close-ups of damaged materials, receipts, repair estimates, and an itemized inventory, and that incomplete documentation can delay payment or trigger disputes. It also notes that CLUE reports retain claim history for seven years in underwriting records, which is another reason to be deliberate about what gets reported and how it's documented in the file, as described in this CLUE report overview.

Take:

- Wide shots of each room to show overall scope.

- Mid-range photos showing how damaged materials connect.

- Close-ups of swelling, staining, charring, cracking, or residue.

- Video walkthroughs with narration of what you're seeing.

- Photos of serial numbers, model tags, and labels for appliances and electronics.

Step 4 Meet the adjuster prepared

Don't treat the inspection like a casual walkthrough. It's evidence gathering.

Have a printed or digital packet ready with:

- Your policy declaration page

- HOA contact information

- Bylaws or declaration excerpts

- A room-by-room damage list

- Mitigation invoices

- Contractor observations if available

Walk the adjuster through the loss slowly. Point out every affected surface, not just the obvious damage. Water travels. Smoke settles. Heat affects adjacent materials. If the adjuster doesn't document something, it may not make the estimate.

Ask one direct question during every inspection: “Are you including this item in your scope, or are you reserving it for later review?”

Step 5 Review the estimate before you agree to anything

The first estimate is often incomplete. That's common in condo insurance claims because the master-policy boundary, access issues, and hidden damage all complicate scope.

Check the estimate for missing line items, low-grade materials, omitted detach-and-reset work, and finish mismatches. If your damaged flooring runs continuously through the unit, partial replacement can create a practical and valuation dispute. The insurer may focus on what is cheapest to patch. You need to focus on what it takes to restore the unit properly under the policy.

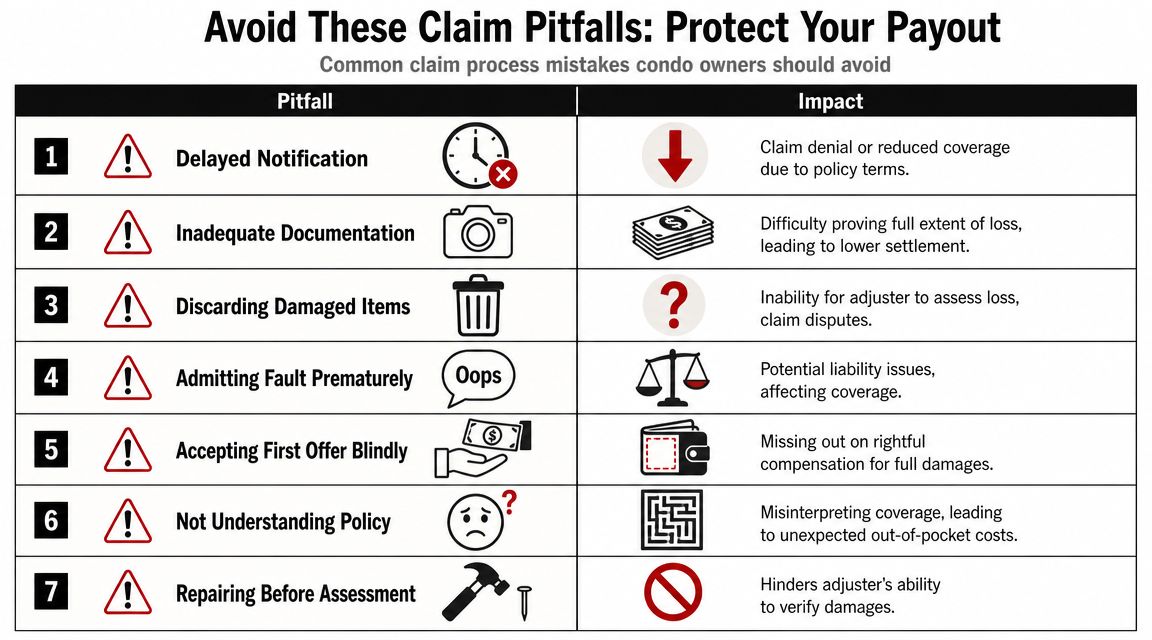

Common Pitfalls That Reduce Your Claim Payout

A lot of bad claim outcomes are predictable. They don't happen because the owner was careless. They happen because the insurer controls the pace, asks narrow questions, and frames the file before the owner understands the stakes.

If you want a clearer view of how carriers shape conversations and settlement expectations, review these insurance adjuster tricks.

The mistakes that cost owners money

- Reporting late: Delay gives the carrier room to question cause, timing, and preventable damage.

- Throwing away evidence: Damaged flooring, cabinets, drywall cuts, and ruined contents may need inspection before disposal.

- Talking too loosely: Casual comments like “it's probably minor” or “maybe it's my fault” can turn into claim-position language later.

- Accepting the first estimate: Early estimates often miss hidden moisture, smoke cleaning, code issues, and finish matching.

- Letting the HOA stay vague: If the association won't state what its master policy covers, your individual claim can stall in limbo.

The code-upgrade trap

One of the most overlooked conflict points in condo insurance claims is who pays for building-code upgrades after a loss. Maryland insurance guidance highlights that condo coverage can be split between the association and the unit owner, and rebuilding may trigger modern code compliance requirements that create a surprise expense, as noted in these Maryland condo insurance webinar slides.

That matters because restoration isn't always a simple replace-what-was-there job. If repairs trigger code requirements, someone has to pay for that added work. Owners often assume the master policy handles it. Many find out too late that it doesn't, or that it only handles part of it.

Typical trouble spots include:

- Electrical updates required during rebuild

- Insulation or ventilation changes

- Drywall or fire-separation requirements

- Accessibility or common-area interface changes

If code upgrades are in play, get the insurer and the association to state their position in writing before repairs move too far.

The insurer's quiet tactics

Most underpayment doesn't arrive with a dramatic denial letter. It arrives through smaller moves.

A narrow inspection. A missing room. A lower-grade material allowance. Silence after you submit documents. A request for “just one more item” while your contractor waits. A claim that gets segmented so each piece looks too small to fight over.

That's why you can't treat the process like customer service. It's a financial negotiation built on policy language, documentation, and advantage.

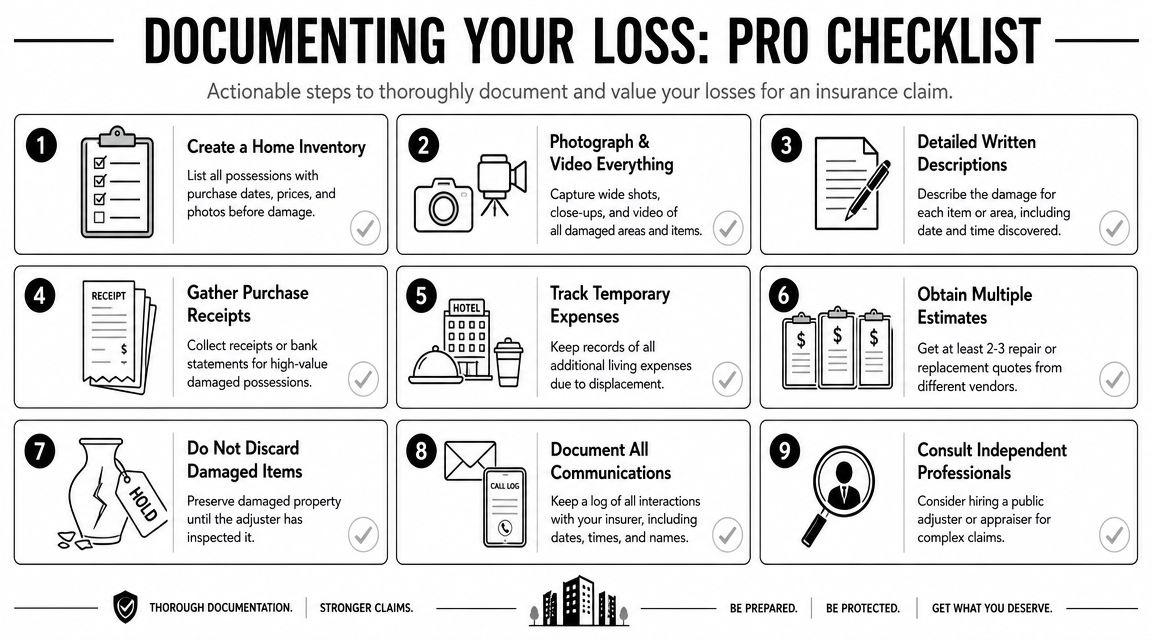

How to Document and Value Your Loss Like a Pro

Documentation wins condo insurance claims. Not emotion. Not fairness. Not the fact that the damage is obvious when you stand in the room.

If you're comparing settlement language in your policy, especially around depreciation and repair valuation, this explanation of actual cash value vs. replacement cost will help.

Build a claim file like an adjuster would

Create one folder for the claim. Inside it, keep subfolders for photos, videos, policy documents, HOA documents, contractor estimates, receipts, communications, and temporary living expenses.

Then create a simple inventory sheet with columns for:

- Room

- Item or building component

- Brand or material

- Approximate age

- Condition before loss

- Damage observed

- Replacement or repair notes

- Receipt or proof attached

Do this for both contents and building components inside your unit. Owners often inventory furniture and forget the expensive interior finishes. Don't.

Take photos that prove scope, not just damage

Bad photos show that something is wrong. Good photos show where, how much, and what it affects.

Use a three-layer method:

- Wide-angle shot showing the whole room.

- Context shot showing the damaged area in relation to nearby materials.

- Close-up shot showing the actual swelling, staining, burn pattern, cracking, soot, or warping.

If flooring or cabinetry is affected, photograph transitions and continuity. If one damaged area ties into a larger continuous finish, that matters for replacement arguments.

Keep one untouched set of originals. Don't overwrite, crop aggressively, or rely only on photos texted to contractors.

Value the loss from the ground up

Don't just wait for the insurer's number and react to it. Build your own.

Use:

- Contractor estimates for structural and finish repairs

- Specialty vendor opinions for flooring, cabinets, countertops, or smoke cleaning

- Receipts and bank statements for contents when available

- Model numbers and current retail listings when receipts are gone

If your unit is uninhabitable, track every extra cost tied to displacement. Hotel bills, pet boarding, added meal expense, laundry, and short-term housing can become part of the claim if covered.

Keep a communication log

This is simple and powerful. Use a note app, spreadsheet, or paper notebook.

Record:

- Date and time

- Who you spoke with

- Their role

- What they said

- What they promised

- What you sent after the call

When a file starts drifting, that log becomes your timeline. It also helps expose when the carrier keeps moving the goalposts.

When and Why to Hire a Public Adjuster

You should understand one thing immediately. The insurance company's adjuster works for the insurance company. That person may be polite, responsive, and experienced. They still do not represent you.

A public adjuster represents the policyholder. In a condo loss, that matters because the hardest fights usually aren't about whether damage exists. They're about scope, valuation, policy interpretation, and responsibility splits between the master policy and HO-6 coverage.

Why this matters more now

The insurance environment has tightened. The U.S. Treasury's Federal Insurance Office reported that from 2018 to 2022, homeowners insurance premiums rose 8.7% faster than inflation, consumers in the highest-risk ZIP codes paid $2,321 on average, which was 82% more than consumers in the lowest-risk ZIP codes, and nonrenewal rates were about 80% higher in those highest-risk ZIP codes, according to the Treasury release on climate-related insurance costs and availability.

For condo owners, the practical takeaway is simple. Carriers are operating in a more strained property-insurance environment. Large losses get scrutinized harder. Coverage lines get drawn tighter. Documentation standards don't get more forgiving.

When you should stop handling it alone

Hire help when the claim has any of these characteristics:

- The master policy and HO-6 policy are pointing at each other: That allocation fight can drag on while your repair timeline slips.

- The damage affects multiple categories at once: Building components, improvements, contents, and temporary housing all require different proof.

- The insurer's estimate misses obvious scope: If rooms, materials, or mitigation costs are left out, that's not a paperwork issue. It's a valuation issue.

- Communication slows down after inspection: Delay often means the file is being narrowed, reviewed, or deprioritized.

- You're exhausted and busy: Condo claims are administrative work piled on top of property damage. That alone is a valid reason to bring in representation.

What a public adjuster actually does

A good public adjuster doesn't just “argue with the insurance company.” They organize the claim into something the carrier has to answer.

That includes:

- Reviewing policy language

- Separating master-policy issues from HO-6 issues

- Preparing detailed scopes of loss

- Documenting damaged building components and contents

- Meeting adjusters and contractors

- Challenging under-scoped or underpriced estimates

- Negotiating the settlement from evidence, not frustration

If you're in Oregon or Washington, NW Claims Management is one example of a licensed public adjusting firm that handles property damage claims for policyholders rather than insurers.

The right time to get help is before you accept a weak scope, not after repairs lock the file into the insurer's version of the loss.

Don't treat representation like a last resort

A lot of owners call for help only after a denial or a bad offer. That's understandable, but earlier is often better.

Once demolition is done, temporary repairs are complete, and the carrier has framed the file around a limited scope, some advantage is already gone. You can still challenge it. It's just harder. In condo insurance claims, early strategy matters because so much depends on how the loss gets categorized in the first place.

Finalizing Your Claim in Oregon and Washington

Condo claims in Oregon and Washington don't happen in a vacuum. They happen in a Pacific Northwest setting where water intrusion, winter storms, smoke damage, and wildfire-related losses can all complicate repair scope and habitability.

You also need to assume carriers will be more exacting about proof and valuation than they were a few years ago. A benchmark coastal property report noted that average per-event costs were up more than 31% versus the previous decade's average, and the same report showed how insurance availability can shift sharply over time in stressed markets, as reflected in the 2025 South Carolina Coastal Property Report. For condo owners in Oregon and Washington, that rising-severity trend translates into more scrutiny on estimates, more resistance on finish valuation, and more pressure to document every category of loss carefully.

What to do before you sign off

Before you close the claim or cash a final payment without questions, confirm a few things:

- The master-policy position is documented: You should know what the association's carrier paid, denied, or reserved.

- Your HO-6 claim addresses gaps clearly: Interior finishes, betterments, contents, and living expenses shouldn't be left vague.

- Supplemental damage has been addressed: Hidden moisture, smoke residue, and access-related repair costs often surface later.

- The release language is understood: Don't sign broad final paperwork if significant items are still unresolved.

The local reality

Oregon and Washington condo owners need to be disciplined. Not dramatic. Disciplined.

That means prompt notice, complete records, a written HOA coverage position, and a refusal to accept blurry policy lines. If the claim starts to drift, if the scopes don't match the actual damage, or if you're getting boxed into a split-coverage mess, bring in professional help before the file hardens against you.

If you're stuck in the middle of a condo claim and don't know whether the master policy, your HO-6 policy, or both should respond, talk to NW Claims Management. They're a licensed public adjusting firm serving Oregon and Washington, and they can review the loss, identify coverage gaps, document the damage properly, and handle negotiations with the insurer so you're not trying to fight a two-policy battle alone.