The house is still damp from the fire department's hoses. Your clothes smell like smoke. Family members are texting. The insurance carrier wants a recorded statement. A contractor has already left a card at the front door. You haven't even had time to decide where you'll sleep tonight, and people are already asking you to make decisions that affect your claim.

That first stretch after a fire is where a lot of owners lose control of the process without realizing it. They assume the insurance company will investigate everything, value everything correctly, and tell them what matters. Sometimes parts of that happen. Often, important damage gets missed, especially in Oregon and Washington where wildfire smoke, moisture intrusion, and local rebuilding requirements can change the value of a claim in ways national advice rarely addresses.

A fire claim adjuster can mean two very different people. One works for the insurer. The other works for you. If you understand that difference early, you can avoid the most common mistakes, protect your documentation, and make better decisions from day one.

After the Fire Your First 24 Hours

At 10 p.m., the fire crew leaves, the plywood goes up, and the questions start coming fast. Can you go back inside for clothes? Should you sign the emergency services authorization the mitigation company put in front of you? Do you tell the carrier the house is a total loss, or wait until someone qualified has inspected it?

The first 24 hours set the claim up for the next six months.

In Oregon and Washington, early mistakes can cost more than owners expect. Wildfire smoke can travel well beyond the burn area. Water used to put out the fire can migrate into wall cavities and subfloors. Local code requirements, especially in parts of the Pacific Northwest with stricter energy, ventilation, and rebuild standards, can change repair scope and cost. If damaged materials are removed before they are documented, it gets harder to prove what was there and what the loss entailed.

What to do first

Start with safety, shelter, and control of the site. If the fire department, city, or county says the structure is unsafe, stay out until you have clearance. If you do enter, wear proper protection and do not go in alone.

Then work in this order:

- Handle immediate living needs. Secure a place to stay, get medications, charge phones, and make sure pets and family members are accounted for.

- Report the loss to the carrier. Give the date, address, and basic facts. Keep the description accurate and limited until the damage has been fully inspected.

- Photograph before cleanup starts. Get exterior elevations, roofline views from the ground, every room, contents, appliances, closets, utility areas, and detached structures.

- Prevent further damage. Board-up, roof tarping, and water extraction may be appropriate, but only after the condition of the property is documented.

- Track every expense. Save receipts for lodging, food, clothing, toiletries, and emergency purchases. In many policies, additional living expense coverage depends on records, not memory.

One practical rule matters here. Do not let a mitigation crew, contractor, or well-meaning family member throw out damaged items on day one.

Even heavily damaged contents can help prove quality, age, quantity, smoke spread, and whether a room was affected by heat, soot, or suppression water. I have seen claims in Oregon and Washington turn on details owners thought were worthless at the time, including partially burned cabinets, packaging from electronics, and insulation removed too early from attic areas after a wildfire ember event.

If you need a straightforward checklist, this guide on what to do after a house fire insurance loss is useful because it focuses on immediate decisions owners have to make before the file starts taking shape without them. If your loss includes roof or exterior damage from the same event or from separate weather exposure after the fire, the process of preserving proof is similar to winning a hail damage roof insurance claim. Conditions change quickly once tarps go on and debris gets moved.

Mistakes that create trouble early

Three patterns cause problems again and again:

- Giving a detailed recorded statement too soon: early descriptions are often incomplete, especially when smoke migration and hidden moisture have not been assessed.

- Signing broad work authorizations without reading the price terms: emergency service contracts can become expensive, and those charges still have to be justified in the claim.

- Assuming the visible fire area is the whole loss: in Pacific Northwest claims, smoke contamination, HVAC spread, water damage, and code upgrades often become larger valuation issues than the charred area itself.

Owners do not need to know every coverage issue in the first day. They do need to slow the process down enough to preserve evidence, protect their living situation, and keep options open. That is how you keep the claim from being defined by the first rushed conversation or the first cleanup invoice.

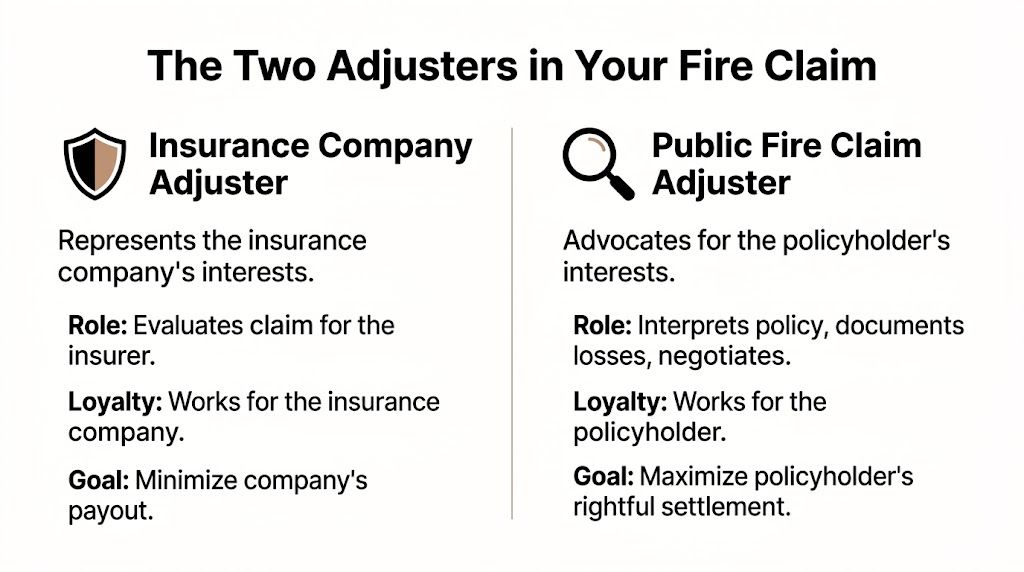

The Two Adjusters in Your Fire Claim

Most owners hear the word "adjuster" and assume everyone involved is doing the same job. They aren't. In a fire loss, the most important question is simple. Who does this person represent?

The claims industry employs nearly 365,300 adjusters, but only about 14,857 are fire claims adjusters, which shows how specialized fire losses are and why role confusion is so common, as noted in Zippia's fire claims adjuster workforce trends.

The insurance company's adjuster

The insurance company adjuster may be a staff adjuster or an independent adjuster hired by the carrier. Either way, that adjuster handles the claim on behalf of the insurer. They inspect, estimate, request records, and communicate the carrier's position.

That doesn't make them dishonest by definition. It does mean their job is tied to the insurer's process, the insurer's file, and the insurer's interpretation of the loss.

The public fire claim adjuster

A public fire claim adjuster represents the policyholder. That adjuster documents damages, reviews policy language, prepares the claim, and negotiates with the carrier from the owner's side.

The cleanest analogy is legal representation. If you were in a dispute, you wouldn't ask the other side's lawyer to advise you. Fire claims work the same way.

For a more focused breakdown, this explanation of public adjuster vs insurance adjuster covers the relationship clearly.

Public Adjuster vs. Insurance Company Adjuster

| Attribute | Public Adjuster (Your Advocate) | Insurance Company Adjuster |

|---|---|---|

| Who they represent | The policyholder | The insurance company |

| Primary role | Interprets policy, documents losses, negotiates | Evaluates the claim for the insurer |

| Loyalty | To your recovery under the policy | To the carrier's claim process |

| How they approach damage | Builds the fullest supportable scope of loss | Reviews damage through the insurer's file and standards |

| Compensation | Usually contingency-based, tied to recovery | Paid by the insurer or contracted through the insurer |

| Communication focus | Explains coverage, strategy, and documentation needs to you | Requests information and advances the insurer's handling of the file |

| Negotiation goal | Maximize the rightful settlement supported by evidence | Resolve the claim on terms the insurer accepts |

Where the conflict shows up in real life

The difference becomes obvious during inspections and estimate review.

An insurer's adjuster may focus first on visible structural damage, basic line items, and whether a component can be cleaned instead of replaced. A public adjuster starts from a different question. What must be proven so the full loss is recognized, including contamination, code impacts, and hidden damage?

The same burned room can produce two very different estimates depending on who is asking the questions.

This is why homeowners in Oregon and Washington often feel confused after the first inspection. The insurer's adjuster may appear helpful and professional, but helpful isn't the same as independent. If the owner doesn't have someone reviewing the scope from their side, missed items can become the owner's problem later.

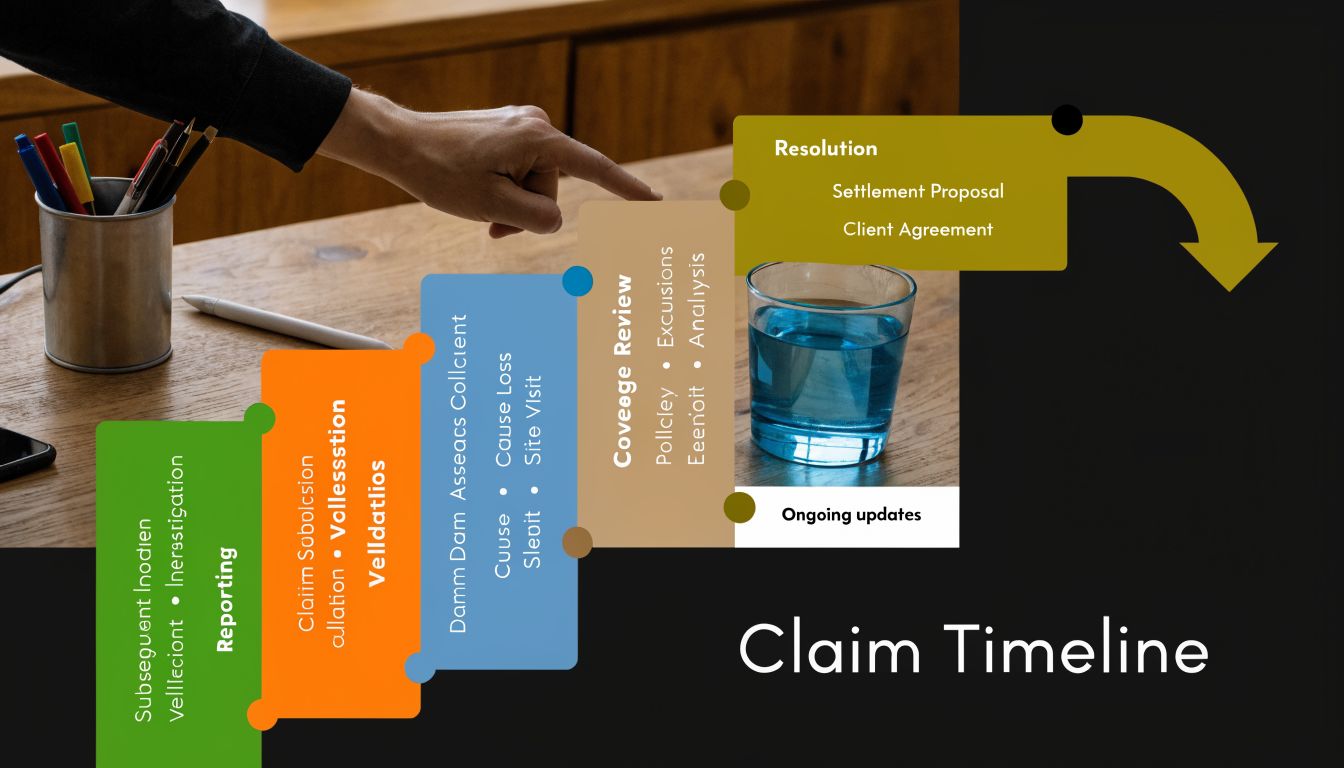

The Fire Claim Timeline from Start to Finish

A fire claim feels chaotic because too many things happen at once. The process is easier to manage when you separate it into stages and understand what each stage is supposed to produce.

Stage one, emergency response and mitigation

The first stage is about protecting the property from further damage. That may include board-up, roof tarping, water extraction, or controlled drying. The point is not cosmetic cleanup. The point is preservation.

Keep invoices and authorizations. If a vendor is asking you to sign broad work assignments before you've had time to review your situation, slow down and read carefully.

Stage two, claim reporting and first carrier contact

Once the claim is reported, the insurance company opens the file and assigns an adjuster. You may receive requests for a recorded statement, proof of occupancy, emergency expense receipts, and basic details about the fire.

Answer truthfully, but don't speculate. If you don't know the extent of damage yet, say that you don't know yet.

Stage three, initial inspection

The carrier's first inspection is rarely the final word. It is an early view of the loss. The adjuster may inspect the exterior, interior, attic, crawlspace, detached structures, and personal property if accessible.

Bring a notebook. Record what was inspected and what was not. If the adjuster didn't open an area, examine HVAC contamination, or ask about moisture migration from firefighting, note that too.

Stage four, full damage assessment

It is precisely at this stage that many underpaid claims separate from well-supported claims. A full assessment goes beyond char and ash. It looks at smoke spread, soot type, water intrusion, electrical impact, hidden heat damage, and whether local building requirements affect repair scope.

A practical overview of the home insurance claim process can help you track what belongs in the file at this point.

Stage five, policy review and scope building

A claim isn't just a construction estimate. It is a policy claim. Someone has to match the facts on the ground to the language in the policy, including structures, contents, debris-related issues, temporary living costs, and any endorsements that expand or limit coverage.

This is also where Oregon and Washington owners need local awareness. Generic claim advice often misses state-specific timing expectations and local rebuild realities. If you're also trying to understand remediation logistics, this piece on navigating the complex process of fire damage and insurance claims gives a practical restoration-side view of what property owners deal with after the fire is out.

Stage six, proof of loss and supporting submission

At some point, the carrier may request a formal proof of loss or the file may require a detailed claim package. That package usually includes:

- Structure documentation: room-by-room scope, measurements, photos, specialist findings, and estimate support.

- Contents inventory: item description, age if known, quantity, quality, and valuation basis.

- Temporary living or business records: receipts, housing costs, operational impacts, and related documentation if covered.

A weak claim package invites argument. A documented claim package narrows it.

Stage seven, negotiation and resolution

Negotiation usually begins after scope and pricing differences appear. One side says an item can be cleaned. The other says it must be replaced. One estimate includes local code work. The other leaves it out. This is normal.

What matters is whether the file contains enough support to move the discussion from opinion to evidence.

Stage eight, payment and supplemental issues

Even after an initial payment, the claim may not be over. Additional damage can surface during demolition, specialty testing, or contractor review. When that happens, the file may need a supplemental submission.

That is common in fire losses. The timeline is rarely one straight line from first call to final check.

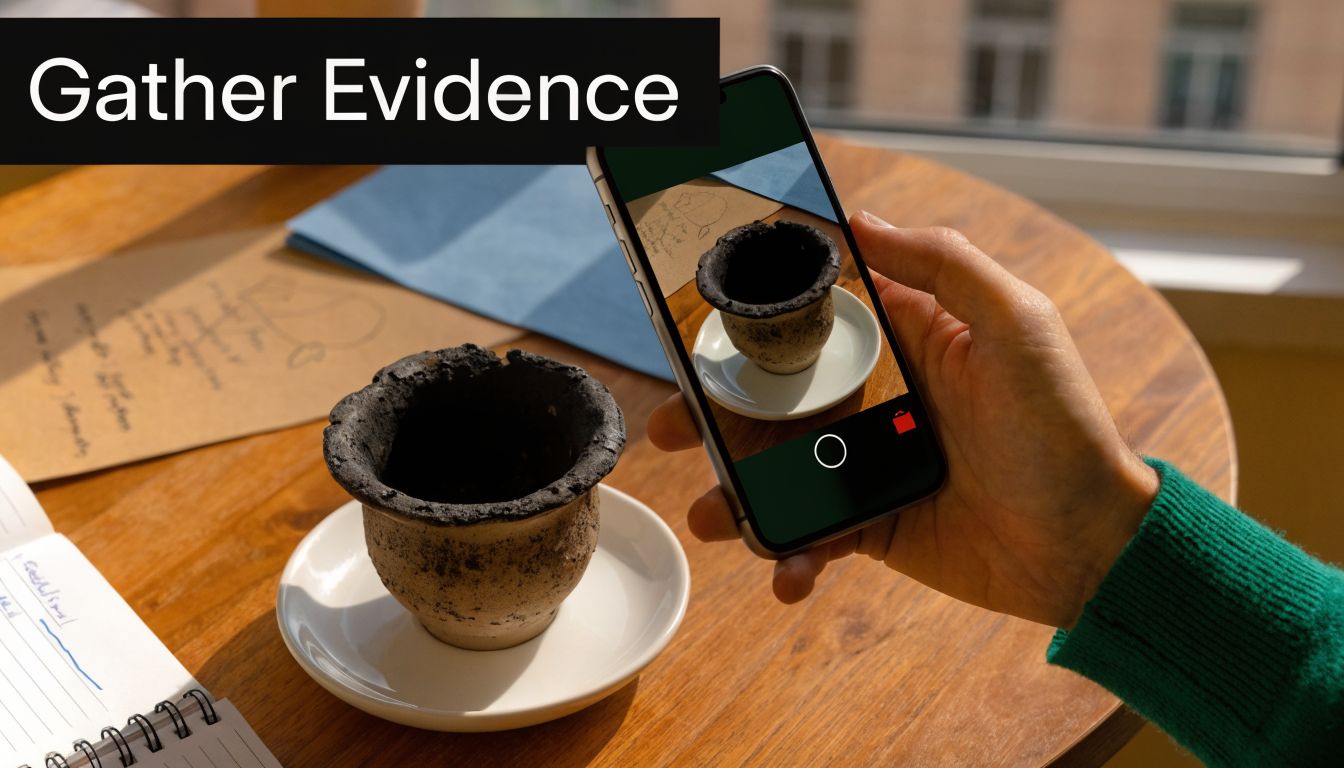

Gathering Evidence for Your Fire Damage Claim

On fire losses, the file often gets shaped before anyone realizes it. A cleanup crew starts wiping surfaces. Damaged items go into dumpsters. A homeowner gives a quick recorded statement while still trying to process what happened. In Oregon and Washington, especially after wildfire smoke events or winter fires where suppression water sits in the building for days, those early decisions can leave major parts of the loss undocumented.

Photos matter, but useful evidence goes beyond a camera roll. The carrier evaluates what can be tied to the fire, smoke, heat, soot, and firefighting efforts, then supported with records, inspection findings, and a clear explanation of why repair, cleaning, or replacement is needed.

What to document in every category

Start with the structure while the scene is still unchanged.

Photograph each room from multiple corners, then move closer. Capture ceilings, walls, flooring, trim, windows, doors, cabinets, insulation exposure, attic access points, crawlspace access, HVAC components, and detached structures. Include rooms that look lightly affected. In Pacific Northwest homes, smoke often travels through ductwork, wall cavities, and open framing in ways that are not obvious on day one.

For contents, document individual items and grouped categories. Piles of damaged property are hard to value later. Open cabinets, closets, and drawers if it is safe to do so. Photograph brand labels, model numbers, serial numbers, and anything that shows age, quality, or quantity.

Keep displacement costs in a separate folder from the start. Save hotel bills, short-term rental records, meal receipts if your policy allows them, pet boarding invoices, replacement clothing, laundry, fuel, parking, and extra transportation tied to being out of the home.

Hidden damage causes some of the biggest disputes

Fire claims in Oregon and Washington often involve more than char and ash. Wet insulation, smoke residue inside ducting, corrosion on electronics, and odor trapped in porous materials can expand the scope well beyond the burn area. That is one reason partial-loss claims become contested. The home may look repairable in a quick walk-through, while the affected materials and systems tell a different story.

A careful inspection usually includes heat-affected materials, moisture from suppression, and the path smoke took through the building. If you want a clearer sense of what that inspection should cover, this property damage assessment process gives a useful framework.

Local building practices also matter here. Many homes across the Pacific Northwest have vented attics, crawlspaces, wood framing, and insulation assemblies that hold odor and residue longer than owners expect. In wildfire-prone parts of Oregon and Washington, outside smoke intrusion can also complicate the line between direct fire damage and broader contamination, so documentation needs to be precise.

A field checklist that holds up later

Use a practical evidence list before cleaning, demolition, or hauling begins:

- Room condition first: photograph each room before anything is moved, wiped down, or boxed.

- Structural details: ceilings, wall finishes, flooring transitions, trim, cabinets, and any visible cracking, staining, or soot patterns.

- House systems: electrical panels, HVAC equipment, duct registers, appliances, water heater area, plumbing penetrations, attic and crawlspace conditions.

- Exterior areas: siding, soffits, vents, roof edges, windows, decks, fences, garages, and sheds.

- Contents by category: furniture, clothing, tools, electronics, paperwork, kitchen items, hobby equipment, and seasonal storage.

- Moisture evidence: wet insulation, swollen baseboards, warped flooring, staining, damp framing, and notes about odor or humidity.

Document first.

If you hire help, expect detailed inspection notes, organized photo logs, and support for hidden damage, not just visible burn marks. NW Claims Management works with Oregon and Washington policyholders on loss documentation and assessment. The standard should be the same with any licensed professional. Clear records, defensible scope, and enough evidence to show the full extent of the damage before cleanup decisions narrow the claim.

Public Adjuster Fees and Licensing in Oregon and Washington

After a fire, fee questions get personal fast. You may be paying for a hotel in Eugene, extra mileage from a rental in Vancouver, or replacement basics while your insurer is still sorting out coverage. The right question is not only what a public adjuster charges. It is what the contract covers, when the fee is earned, and whether the person handling your claim is legally allowed to represent you in Oregon or Washington.

Most public adjusters handling fire losses work on a contingency fee. The fee is paid from claim proceeds rather than as an upfront retainer. That structure helps property owners who cannot fund months of documentation, estimate review, contents work, and insurer meetings out of pocket. It also creates real contract issues to review before signing.

Read the agreement carefully.

Ask how the percentage applies to initial payments, supplemental payments, reopened portions of the claim, and code-related increases. Ask whether the fee applies to amounts already offered by the carrier before the adjuster is hired. Ask who prepares the estimate and inventory, and whether those services are included or billed separately. Homeowners comparing options can get a clearer sense of typical contract terms and pricing models in this guide to public adjuster cost.

The Oregon and Washington piece matters more than many owners realize. Fire claims in the Pacific Northwest often involve smoke migration from wildfires, debris and ash contamination, steep-site access problems, and rebuilding under current local code rather than the code in effect when the house was built. In parts of Oregon, that can mean updated defensible space expectations or permit review tied to wildfire risk. In Washington, urban interface rebuilding and local enforcement practices can change scope and timeline. A fee agreement should be clear enough that you know who is handling those added layers of work.

Licensing is the first screen.

Before signing anything, verify that the adjuster holds an active license in the state where the damaged property sits. Oregon and Washington regulate public adjusters through their state insurance systems, and that matters for consumer protection. If your home is in Oregon, the adjuster needs Oregon authority. If the loss is in Washington, the adjuster needs Washington authority. Border-area owners around Portland, Vancouver, Longview, and the Columbia Gorge should not assume one license covers both states.

Use a practical screening list:

- Verify the state license directly: check the current license status with the appropriate state regulator, not just a website or business card.

- Read the fee section line by line: look for cancellation terms, timing of payment, and how supplemental claims are treated.

- Confirm who will work the file: some firms sign the client, then hand daily claim work to someone else.

- Ask about Oregon or Washington fire claim experience: local permitting, smoke damage disputes, and code upgrade issues are region-specific.

- Get plain answers: if the adjuster cannot explain the contract in clear language, that problem usually gets worse later.

A qualified public adjuster in this region should be able to discuss wildfire smoke, local rebuild friction, ordinance or law issues, and the difference between a simple structure estimate and a fully supported fire claim. That is the standard to use before you sign.

How to Choose the Right Public Fire Claim Adjuster

Hiring a public adjuster is not a small administrative choice. It is a representation decision. You're choosing who will interpret your policy, organize your evidence, and negotiate with the insurer while you're dealing with displacement and repair pressure.

What to look for first

Start with credentials and relevance.

A good candidate should be able to show a current Oregon or Washington license, explain their process in plain language, and discuss fire-specific issues without slipping into vague sales talk. Fire losses are different from simple water losses or basic wind claims. The adjuster should be comfortable discussing smoke spread, contents inventory, code impacts, and negotiation strategy.

Professional affiliation also helps. The verified background for this topic notes credentials such as NAPIA membership and state licensing as meaningful markers of compliance and authority in public adjusting practice.

Questions worth asking in the first call

Don't ask only, "How much do you charge?" Ask how they work.

Use questions like these:

- How do you document hidden smoke and water damage?

- Who prepares the estimate and contents inventory?

- How often will I hear from you during the claim?

- Have you handled fire losses in my part of Oregon or Washington?

- What do you need from me in the first week?

The answers should be concrete. If someone stays general, pushes for an immediate signature, or avoids specifics about who handles the file, keep looking.

Red flags that deserve a hard stop

Some warning signs are easy to miss when you're under stress.

| Red flag | Why it matters |

|---|---|

| Pressure to sign immediately | You may not have had time to review terms or compare options |

| No clear license information | You can't confirm authority to represent you |

| Vague communication promises | Claims stall when no one owns updates and deadlines |

| Upfront fee demands without clarity | The financial arrangement should be easy to understand |

| Little discussion of local issues | Fire claims in OR and WA often require regional knowledge |

The right adjuster should lower confusion, not increase it.

Choose someone who can explain trade-offs

The strongest public adjusters don't promise magic. They tell you where the work is. They explain what can be documented, what may be disputed, and how long parts of the process may take.

That kind of honesty is useful after a fire. You need a professional who can look at a claim calmly, identify the critical elements, and keep the file moving without creating false expectations.

Your Advocate in Oregon and Washington NW Claims Management

For property owners in Oregon and Washington, local knowledge matters more than most national articles admit. A fire loss in this region can involve wildfire smoke spread, moisture complications from suppression efforts, local permitting delays, and building code issues that affect the repair scope long after the fire scene is cleared.

NW Claims Management is a licensed public adjusting firm based in Portland and serves policyholders across Oregon and Washington. The firm's role is straightforward. It represents property owners, not insurance carriers. That includes residential claims, commercial property losses, and claims involving nonprofit or public-serving organizations.

What local representation changes

A local public adjusting team should be able to do more than write an estimate. It should be able to review policy language, coordinate documentation, organize specialists when needed, and negotiate from a record that reflects Pacific Northwest realities.

That matters if your property needs more than a basic repair allowance. Smoke contamination, code-related rebuild costs, and disputed scope items usually aren't resolved by a quick inspection alone.

When a call makes sense

You don't have to wait for a denial to ask for help. Owners usually benefit from representation when any of the following are happening:

- The carrier's scope looks too narrow

- You suspect smoke or moisture damage beyond the burned area

- The claim paperwork is taking over your life

- You're being asked to make decisions before the damage is fully assessed

NW Claims Management offers claim evaluations for Oregon and Washington policyholders and handles communication, documentation, and negotiation throughout the process. If you're overwhelmed, that kind of support can give structure to a situation that often feels scattered and adversarial.

Frequently Asked Questions About Fire Claims

What if my insurance company already made an offer

An offer is not automatically the final value of the claim. Review it carefully before signing anything that releases the carrier. Many owners seek help only after the first estimate arrives and key damage appears to be missing.

Can I handle a small fire claim myself

Sometimes, yes. If the damage is limited, the scope is obvious, and there are no disputes over smoke, water, or code issues, some owners handle the claim directly. The problem is that "small" fires often create larger contamination or repair issues than the visible burn area suggests.

What happens if my claim is denied

A denial is not the same as the end of the matter. First, get the denial reasoning in writing. Then compare that reasoning against the policy language and the actual damage record. Denials tied to causation, scope, or incomplete documentation often require a more technical response than a homeowner can reasonably build alone.

How long do I have to file a fire claim in Oregon or Washington

The exact deadline depends on the policy and the circumstances of the loss. The safest move is to report the fire promptly, preserve evidence immediately, and review the policy for notice and suit-limitation language as early as possible. If there is any uncertainty, get professional guidance quickly rather than relying on assumptions.

Should I accept the first check

Not until you understand what it covers. Some payments are partial or advance payments. Others may be presented in a way that feels final. Before depositing or endorsing any payment tied to settlement language, confirm whether more claim components remain open.

Do smoke and water damage count even if the flames were contained to one area

Often, yes. Fire claims frequently involve more than direct flame contact. Smoke migration, soot contamination, and water from firefighting can affect rooms and systems well beyond the origin area, especially in attics, ducting, insulation, and contents storage areas.

If you're facing a fire loss in Oregon or Washington and need help understanding what your policy covers, what damage may have been missed, or how to respond to a low estimate, contact NW Claims Management for a free, no-obligation claim evaluation.