Water coming through a ceiling in the middle of a freeze is the kind of problem that scrambles your judgment fast. You hear dripping, step onto a wet floor, open a closet or utility room, and realize this isn't a small plumbing issue. It's a property damage claim in the making.

The question most homeowners ask right away is simple. Does home insurance cover frozen pipes? Usually, yes, but only under specific conditions. The difference between a paid claim and a denied one often comes down to what you did before the pipe burst, what you do in the first few hours after discovery, and how well you document the loss.

The Unwelcome Discovery of a Burst Pipe

A typical freeze-loss scene looks the same across Oregon and Washington. A homeowner wakes up to no water pressure, then finds a split supply line in a crawl space, garage wall, laundry room, or under a sink on an exterior wall. Sometimes the pipe bursts while the house is occupied. Sometimes the worst losses happen after a weekend away, when water has already soaked drywall, baseboards, flooring, insulation, and cabinets.

That panic is justified. These claims get expensive quickly. According to State Farm's frozen pipe loss data, from 2024 through mid-2025 the company paid over $628 million for more than 20,000 frozen-pipe-related claims, with the average claim payment exceeding $30,000. The same source says water damage and freezing together account for nearly 23% of all U.S. homeowners insurance losses.

Those numbers explain why insurers look at these claims so closely. A frozen pipe isn't just a pipe problem. It's often a drywall problem, a flooring problem, an insulation problem, a contents problem, and sometimes a temporary housing problem.

If you're still trying to figure out whether the leak started earlier than you thought, Engle Services' leak detection advice is a useful read because hidden leak clues can affect how an insurer frames the cause of loss. If the damage looks broad or the drying work needs to begin immediately, homeowners often also need to understand the restoration side of the loss, not just the policy side, especially with emergency water damage restoration in Bellingham.

The first mistake I see in frozen pipe claims is treating the event like a minor plumbing repair. The insurer usually treats it as a water-damage investigation.

The Core Rule of Frozen Pipe Coverage

The short answer is this. Home insurance usually covers the resulting water damage from a burst frozen pipe when the loss is sudden and accidental. It often does not cover the broken pipe itself.

According to this explanation of frozen pipe coverage, most standard homeowners policies apply coverage only when the water release is "sudden and accidental." That means the policy is built to pay for the ensuing water damage from an abrupt burst, but not usually for pipe replacement itself, especially where the failure ties back to wear, corrosion, or long-term neglect.

Think of it like a roof claim

Insurance draws a line between the event and the condition behind the event.

If lightning hits your house and damages the interior, that's the kind of abrupt event policies are written for. If a roof leaked slowly for months and no one addressed it, the carrier may argue the interior damage came from deferred maintenance. Frozen pipe claims often sit right on that same fault line.

What matters most is not just that the pipe froze. It is whether the insurer sees the water release as a covered accident or as the result of a preventable condition.

What that usually means in plain English

When a frozen pipe bursts, policies commonly respond to the damage the water caused after the rupture. That can include wet drywall, damaged flooring, ruined trim, soaked insulation, and personal property affected by the release. But the plumbing repair itself is often separated out.

Here's a practical breakdown:

| Damage Type | Typically Covered? | Important Caveat |

|---|---|---|

| Water damage to drywall, flooring, and finishes | Usually yes | Must fit the policy's sudden-and-accidental standard |

| Damage to belongings hit by released water | Usually yes | Documentation matters, especially for condition and ownership |

| Drying and cleanup tied to covered water damage | Often yes | The carrier may dispute scope, method, or duration |

| Repair of the burst pipe itself | Often no | Many policies cover resulting loss, not the failed pipe |

| Corroded, worn, or deteriorated plumbing | Often no | Insurer may classify this as maintenance, not accidental loss |

A lot of homeowners lose money here because they accept the insurer's first framing of the loss. If the carrier says, "We don't cover pipes," that may be only partly true. The better question is whether the policy covers the damage the pipe caused.

Practical rule: Separate the plumbing invoice from the water-damage invoice. They aren't always treated the same way under the policy.

If you want to understand why that distinction matters so much when a claim is valued, this guide to insurance policy limits explained helps homeowners read the numbers and categories carriers use to control payouts.

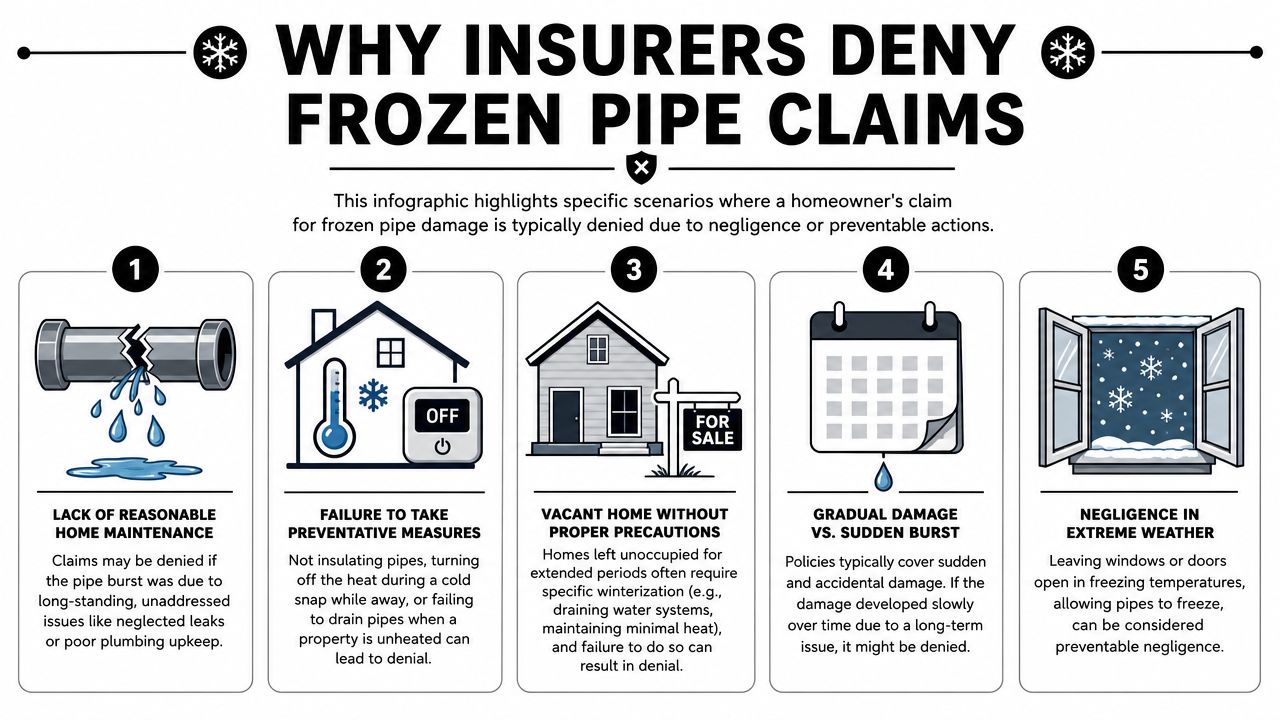

Why Insurers Deny Frozen Pipe Claims

Insurance companies don't deny most frozen pipe claims by arguing that water damage never happened. They deny them by arguing that you didn't do your part to prevent the freeze.

That argument usually comes down to heat, vacancy, maintenance, or timing. If the company can point to an unheated home, a vacant structure, ignored warning signs, or a loss that looks gradual instead of abrupt, it has a clear path to limit or deny payment.

The "reasonable steps" standard

The most important phrase in these claims is usually reasonable steps. The NAIC's consumer guidance on burst pipe water damage explains that insurers often expect a home to be kept at about 55°F (13°C) or, if the property is vacant, for the water supply to be shut off and drained. If the insurer can show the homeowner failed to take those basic precautions, it may deny the claim under policy exclusions.

That gives the carrier a checklist.

- Heat was off or set too low. If thermostat records, smart-home logs, utility usage, or inspection findings suggest the home wasn't adequately heated, the insurer may call the loss preventable.

- The home was vacant. Vacant or unoccupied homes get stricter scrutiny because no one was there to catch a freeze early.

- The pipe was already compromised. Corrosion, prior leaking, patchwork repairs, or visible deterioration can shift the claim from accidental loss to maintenance failure.

- The damage looked slow. Staining, long-term microbial growth, or repeated wetting patterns can trigger a gradual-damage defense.

- The homeowner made the facts worse. Open windows, shut-off heat, disconnected service, or no winterization plan all give the insurer something to point at.

What works and what doesn't

What works is showing the house was being responsibly maintained. Thermostat history, utility bills, service records, plumber invoices, photos of insulated pipes, and proof that someone checked on the property can all support your side.

What doesn't work is vague reassurance. Saying "we usually keep it warm" won't carry much weight if the carrier has inspection notes showing frozen lines in an unheated area.

For prevention context outside the Pacific Northwest, expert advice for South Florida homeowners on insulating pipes still reinforces a simple truth that applies anywhere. Mechanical prevention beats verbal explanations after the loss.

If the insurer has already leaned toward exclusion language, homeowners need to know how to respond strategically. This guide on how to fight insurance claim denial is useful when the carrier's position starts sounding final before the investigation is complete.

The carrier isn't just asking what froze. It's asking whether the freeze was avoidable.

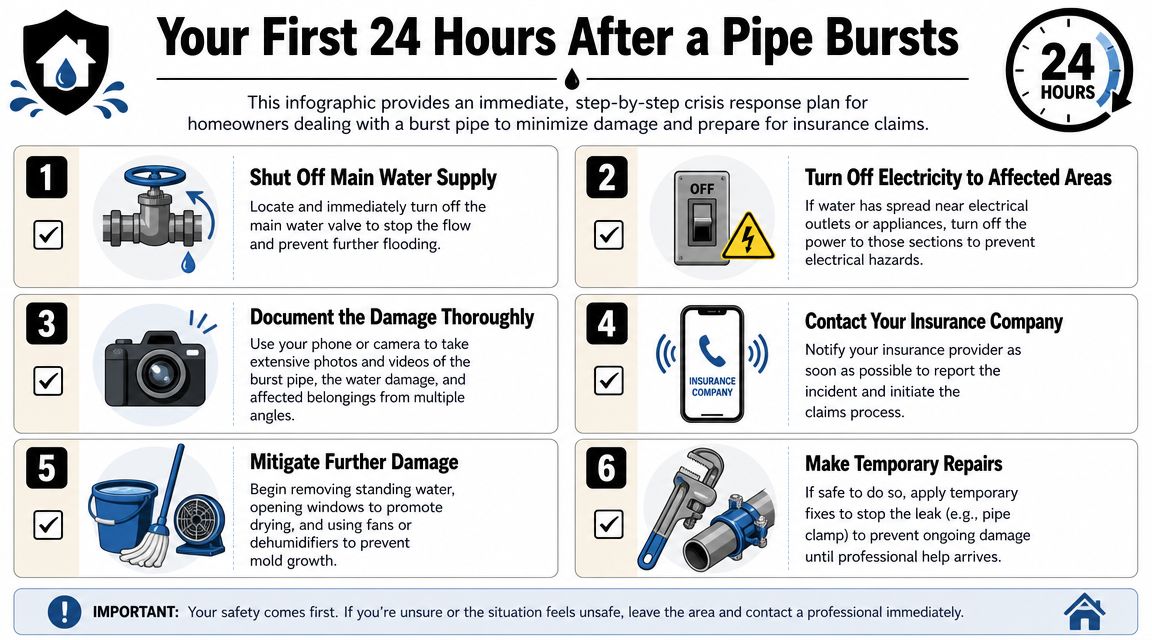

Your First 24 Hours After a Pipe Bursts

The first day matters for two reasons. You need to stop the damage, and you need to preserve the claim.

A lot of homeowners do one but not the other. They mop, tear out wet material, throw away damaged items, call a plumber, and only later realize they've erased evidence the insurer wanted to see.

Stop the loss safely

Start with control.

- Shut off the main water supply. If you don't know where it is, find it before the next freeze event, not during one.

- Cut power to affected areas if water is near outlets, fixtures, or appliances. Don't step into standing water around electrical hazards.

- Call a plumber for emergency stabilization. Ask for a written description of what they found, especially the location and condition of the failed section.

Document before cleanup changes the scene

Use your phone and be methodical.

- Photograph the source area. Take close shots and wide shots.

- Video the path of water. Show ceilings, walls, floors, cabinets, and contents.

- Capture damaged personal property in place. Don't just pile items up later and expect the same impact.

- Keep the failed pipe segment if the plumber removes it. That piece can matter if the carrier later argues wear and tear instead of freeze damage.

Mitigate without destroying evidence

You do have a duty to reduce further damage. Start drying, move salvageable contents, and use fans or dehumidifiers if it's safe. But don't begin major demolition until the loss is documented.

If you remove wet drywall before anyone has recorded the extent of saturation, you've made the insurer's job easier and your proof harder.

Start a paper trail immediately

Open a claim file on your phone or laptop.

- Save every receipt for emergency plumbing, drying equipment, hotel stays, cleanup supplies, and temporary repairs.

- Write down the timeline while it's fresh. When you discovered the issue, what you saw first, what steps you took, and who you called.

- Record every insurance conversation by date, time, name, and summary.

That simple log becomes valuable when the claim drags out, the assigned adjuster changes, or the carrier later says you failed to notify promptly.

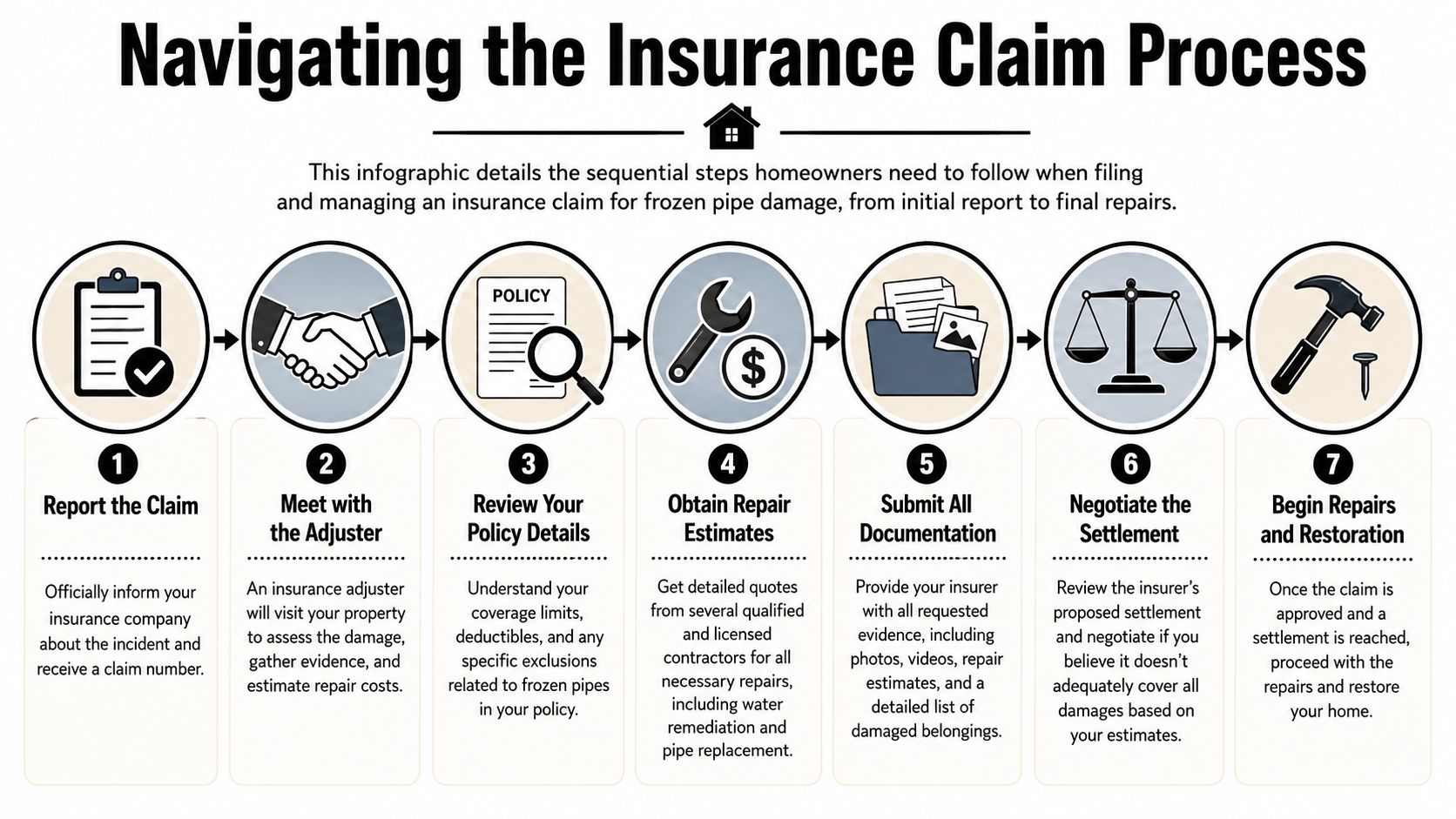

Navigating the Insurance Claim Process

Once the immediate emergency is under control, the claim shifts into a different phase. Homeowners frequently get overwhelmed in this phase. The insurer starts asking for statements, inventories, contractor bids, photos, mitigation invoices, proof of occupancy, and sometimes proof that the property was heated.

The claim process looks routine on paper. In practice, it turns on framing. The insurance company is trying to classify the loss. You're trying to prove the full scope and value of covered damage.

The first friction point is scope

According to Travelers' explanation of burst pipe coverage, a common dispute is that policies may cover water damage to walls and floors while excluding the cost to repair the broken pipe itself. That means a claim can be partially covered and partially denied at the same time. The insurer may pay for some demolition, some drying, and some finish repair while refusing the source plumbing work.

That partial-denial structure confuses homeowners because it feels like mixed messaging. It isn't. It's how many carriers contain the payout.

What to watch closely during the claim

Three things deserve your attention more than anything else.

The carrier's description of the cause

Read the adjuster's notes, letters, and estimate summaries carefully. If the insurer starts using phrases like long-term seepage, wear and tear, repeated leakage, or maintenance issue, that language may shape the outcome more than the photos do.

If the cause description is wrong, correct it early and in writing.

The estimate line items

An insurer's estimate may acknowledge damage but still understate the work required to restore the property. Common pressure points include:

- Drying scope. Not enough equipment, not enough time, or no allowance for concealed moisture.

- Demolition scope. Limited removal when materials in wall cavities, under flooring, or behind cabinets were affected.

- Finish replacement. Partial patching where matching is unrealistic or unavailable.

- Contents treatment. Inadequate valuation of furniture, rugs, electronics, clothing, or stored items.

If you're building the contents side of the file, understanding home inventory claims can help you organize what was damaged in a way insurers can process.

The difference between emergency work and permanent repair

Homeowners often assume one contractor can handle everything and one estimate tells the whole story. In reality, a solid claim file may need separate documentation for plumbing stabilization, water mitigation, demolition, rebuild, and contents damage.

How to keep control of the process

Don't hand over the entire narrative to the carrier. Build your own record.

- Request the policy language the insurer is relying on if it raises an exclusion.

- Get detailed contractor estimates, not vague one-page totals.

- Ask for the full adjuster estimate and compare it room by room.

- Respond in writing when something is omitted, misdescribed, or underpriced.

A frozen pipe claim often turns on boring paperwork, not dramatic damage photos. The side with the cleaner record usually has the stronger position.

If you want a broader view of how carriers move claims from first notice through payment, this breakdown of the home insurance claim process is a useful reference point.

When to Hire a Public Adjuster in Oregon and Washington

Some frozen pipe claims are straightforward. Many aren't. The point where homeowners usually need help is not when the water first appears. It's when the insurer's position hardens.

That can happen after a quick reservation of rights letter, a low estimate, a claim decision that covers only part of the loss, or repeated requests for the same documents while the house sits torn apart.

Red flags that justify professional help

You should seriously consider a public adjuster if any of these are happening:

- The carrier says the home may have been vacant or unoccupied and starts asking pointed questions about heat, inspections, or utility usage.

- The insurer accepts some damage but excludes key parts of the claim, especially where demolition, drying, or finish repairs seem understated.

- The estimate doesn't match what qualified contractors are telling you.

- You're being pushed to move fast on a settlement before the full scope is clear.

- The claim has turned technical and every answer seems to depend on policy wording.

A public adjuster works for the policyholder, not the insurer. That matters because the insurance company's adjuster, even when professional and courteous, is still evaluating the claim for the carrier.

Why this matters more in Oregon and Washington

Occupancy and vacancy issues can become especially important in complex freeze losses. As noted by the District of Columbia Department of Insurance guidance on frozen pipes, policy conditions for vacant or unoccupied properties are often stricter, and some policies require heat to be maintained even when the building is vacant. Failure to do so can void coverage for frozen pipe damage, and those questions often become highly fact-specific.

That matters in Oregon and Washington because many homeowners split time between properties, travel during winter, manage rentals, or leave homes unoccupied during cold periods. Those situations create exactly the kind of gray area insurers use to challenge coverage.

The practical decision point

If you're still discussing routine scheduling and straightforward payment, you may not need representation. If you're arguing over scope, cause, exclusion language, or whether your precautions were "reasonable," the claim has moved into a specialized dispute.

At that point, it helps to understand what a licensed public adjuster in Oregon does and how policyholder representation differs from insurer-side handling.

Frequently Asked Questions About Frozen Pipe Claims

Will my insurance rate go up if I file a frozen pipe claim

That depends on the insurer, your claims history, and how the carrier underwrites future risk. I wouldn't guess or promise an outcome. The better approach is to focus first on protecting the current claim, because a covered water loss can create substantial out-of-pocket exposure if it's underpaid.

Is mold covered after a burst frozen pipe

Sometimes mold-related work is included when it results from covered water damage and the homeowner acted promptly to dry and mitigate. The fight usually isn't over whether mold is unpleasant. It's over whether the insurer believes the growth resulted from the covered event, how quickly mitigation began, and whether the remediation scope is necessary.

What if I live in a condo or own a rental property

Then the first question is which policy applies to which part of the damage. In condos, building responsibility and unit-owner responsibility often overlap. In rental situations, occupancy, heat maintenance, and notice issues often get more scrutiny. Don't assume one policy covers the whole event. Read the policy language and get the association documents or lease details in front of you early.

If you're in Oregon or Washington and your frozen pipe claim is being delayed, partially denied, or undervalued, NW Claims Management can step in as your advocate. Their team represents policyholders, not insurance companies, and helps document damage, interpret policy language, challenge low estimates, and push for a fair settlement when the carrier's version of the loss doesn't match what actually happened.