The call usually comes after a long night.

A pipe bursts in Portland. A kitchen fire leaves smoke in every room. Wind tears roofing off a building in Vancouver. You call the insurance company expecting help, direction, and a fair process. Instead, you get forms, recorded statements, a rotating cast of adjusters, and an estimate that feels too small for what just happened.

That disconnect confuses property owners because insurance is marketed like peace of mind. In practice, a claim is handled inside a business system built around risk management in insurance companies. If you understand that system, the claim starts to make more sense. More important, you stop reacting emotionally to insurer tactics and start responding strategically.

Your Insurance Policy Is Not a Promise It Is a Product

A homeowner in the Pacific Northwest often starts in the same place. The roof leaked after a storm, or a fire department forced entry during an emergency, and now the house is damaged, the family is displaced, and every day costs money. The policyholder thinks, “I paid premiums for years. Now they’ll take care of this.”

That belief is understandable. It’s also incomplete.

An insurance policy is a financial product sold by a company that has to protect its balance sheet while meeting its contractual obligations. The carrier didn’t write your policy as a blank check. It wrote a product with limits, exclusions, conditions, depreciation rules, proof requirements, and internal procedures designed to control what gets paid and when. If you’ve ever tried to sort out sublimits, endorsements, or actual cash value versus replacement cost, a clear guide to insurance policy limits explained helps show how tightly the product is built.

Why the company looks at your loss differently

You see a damaged home or business. The insurer sees a file that affects reserves, staffing, vendor costs, reporting, and exposure.

That mindset has only sharpened. Cyber attack or data breach ranks as the top current risk facing insurers in Aon’s 2025 survey of insurance organizations, ahead of weather and natural disasters and regulatory change, according to Aon’s insurance industry risk findings. When carriers are managing pressure from cyber threats, catastrophe exposure, and compliance demands at the same time, they tend to become more cautious across operations, including claims.

Your claim may feel personal to you. Inside the insurer, it’s processed as controlled financial exposure.

That doesn’t mean every adjuster is acting in bad faith. It means the company has systems, metrics, and guardrails that shape the adjuster’s behavior. A friendly tone on the phone doesn’t change the underlying structure.

What property owners should take from this

Stop treating the claims process like customer service. Treat it like a negotiation inside a rules-based financial product.

That shift matters because it changes your behavior:

- You document before discussing value.

- You read the policy before accepting explanations.

- You assume the first estimate is a starting position, not a final answer.

- You separate politeness from agreement.

Once you understand that the policy is a product and the claim is managed exposure, the rest of the insurer’s behavior becomes easier to read.

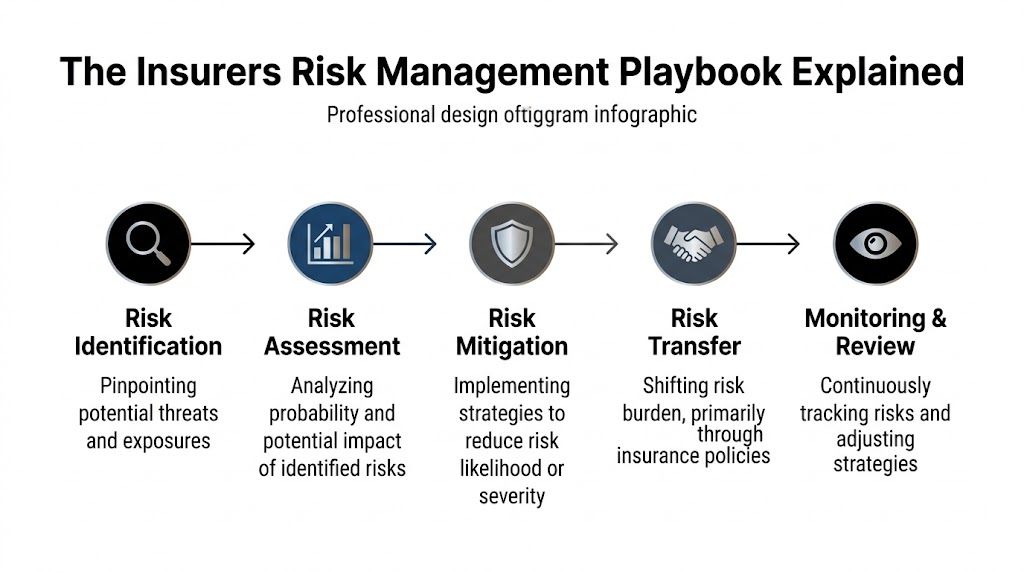

The Insurers Risk Management Playbook Explained

Insurance companies like to present claims handling as a straightforward promise. Behind the scenes, the operating model looks more like a casino’s discipline. The house doesn’t survive by guessing. It survives by controlling odds, limiting volatility, spreading risk, and monitoring results constantly.

That’s the simplest way to understand risk management in insurance companies. The carrier is always asking four practical questions. What risks should we take? What price should we charge? How much of this risk should we keep? How do we make sure one bad stretch doesn’t threaten the company?

This visual captures the core process.

Underwriting decides which bets the insurer will take

Underwriting happens before a claim ever exists. The insurer looks at the property, location, construction type, prior loss history, occupancy, and other details to decide whether it wants the risk at all.

A hillside home in wildfire country and a commercial building with deferred maintenance don’t look the same to an underwriter. Neither does a nonprofit with older systems compared to a recently renovated office building. The underwriting department is trying to avoid policies that produce losses the company doesn’t want on its books.

For property owners, the key point is this. The policy language you receive is not random. It reflects a set of business decisions made long before your loss.

Pricing sets the odds

Premium isn’t just a bill. It’s the company’s attempt to price uncertainty.

If underwriters think a type of property presents more severe or less predictable losses, the company can raise price, narrow coverage, impose higher deductibles, or decline the risk. That’s why two buildings that look similar from the street can produce very different policy terms.

A claim then gets handled in light of that pricing decision. If the insurer believes a category of loss is expensive or trending upward, adjusters often face tighter review.

Practical rule: If an insurer spent years trying to limit exposure on a type of risk, don’t expect generosity when that exact loss arrives.

Reinsurance protects the insurer from its own worst days

Insurance companies buy insurance too. That’s reinsurance.

When a wind event, wildfire, or regional freeze produces many claims at once, reinsurance can absorb part of the shock. This matters to policyholders because catastrophe-heavy periods often change how aggressively a carrier reviews files. During surge conditions, the insurer isn’t only looking at your claim. It’s watching total loss exposure across a region.

That’s one reason major storm and fire claims can feel more rigid than a simple isolated water loss. The company is managing portfolio impact, not just one damaged structure.

Capital management keeps the company standing

Even a profitable insurer can get into trouble if losses hit at the wrong time or in the wrong concentration. Capital management is about keeping enough financial strength to satisfy regulators, rating agencies, and internal risk appetite.

That pressure influences claims in subtle ways:

- Large files attract more layers of review.

- Unusual line items get challenged harder.

- Cash flow timing matters.

- Settlement authority may tighten during stressful periods.

A practical overview of the home insurance claim process helps property owners see where those review points often show up after the claim is opened.

Monitoring turns claims into data

The final part of the playbook is constant review. Insurers track patterns, compare offices, watch cycle times, and study where payouts are rising. That’s how they decide whether to change training, push more vendor programs, revise estimating standards, or scrutinize certain losses.

The key for a property owner is simple. A claim is never just your claim to the insurer. It’s also a data point inside a larger control system.

If you know that, you stop expecting the company to “just do the right thing” on its own. You present proof, challenge assumptions, and keep the discussion tied to the policy and the scope of damage.

How Insurers Manage Financial and Catastrophic Risk

The financial side of an insurance company affects your claim more than most policyholders realize. Long before a settlement check is issued, the carrier is making internal decisions about reserves, catastrophe exposure, and capital pressure. Those decisions don’t stay in the accounting department. They shape how adjusters inspect, estimate, and negotiate.

Here’s the financial lens behind the process.

Reserve setting affects the tone of the claim early

A reserve is the insurer’s internal estimate of what the claim may cost. It functions much like a project budget the company sets before all the facts are in.

If the first inspection is incomplete, the first estimate may be incomplete too. Once a low reserve is set, increasing it can require more approvals and more justification. That’s one reason early inspections matter so much. Missed damage in the first phase often creates friction later, not because the damage disappeared, but because the file was financially framed too narrowly at the start.

This is why policyholders should move fast on documentation:

- Photograph every room and elevation. Wide shots and close-ups both matter.

- Preserve damaged materials when safe. They can prove scope and causation later.

- Get repair input early. Contractors, engineers, or mitigation specialists often identify items a field adjuster misses.

- Challenge omissions in writing. A paper trail forces the file to evolve.

Catastrophe models change how Oregon and Washington risks are viewed

In the Pacific Northwest, insurers don’t price or manage all property the same way. Coastal wind, urban water damage, wildfire exposure, and earthquake concerns create different risk profiles. A carrier uses models and historical experience to decide where it wants to write business, how much exposure to keep in one area, and how aggressively to manage losses after a regional event.

For a property owner, that means your claim may be influenced by broader regional concerns even if your building is the only one damaged on the block. In a wildfire corridor, for example, a carrier may already be sensitive to concentration risk. In flood-prone areas, the company may examine causation and excluded water sources with unusual intensity. If your loss involves rising water or storm-related inundation, it helps to understand the mechanics of how to file a flood insurance claim before the insurer locks in its theory of damage.

Capital rules create pressure that reaches the claim file

One of the clearest examples is Risk-Based Capital, often called RBC. RBC modeling is the regulatory framework insurers use to determine how much capital they need relative to their risk profile. According to this explanation of RBC modeling and NAIC action levels, a severe 20 to 30% equity market drop can push an insurer’s RBC ratio below the 200% company action level threshold, triggering regulatory pressure.

That doesn’t mean every claim gets underpaid when markets move. It does mean capital stress can make insurers more defensive about preserving reserves and controlling payouts.

If a carrier is under financial pressure, “prove it” gets louder inside the claim process.

What works for policyholders and what doesn’t

Some responses help. Others backfire.

| Financial pressure point inside the insurer | Better policyholder move |

|---|---|

| Low initial reserve | Submit detailed scope corrections quickly |

| Regional catastrophe exposure | Tie your claim to property-specific facts, not general assumptions |

| Capital sensitivity | Document why each disputed item is covered and necessary |

| Internal approval bottlenecks | Ask for written explanations and escalation paths |

What doesn’t work is broad outrage with no supporting file. What does work is disciplined evidence that forces the claim team to update the insurer’s financial assumptions.

Your Claim Through the Insurers Risk Management Lens

Most policyholders think the claims department exists to solve problems. In reality, it also functions as a cost-control center. That doesn’t make every claim decision improper. It does explain why the process often feels slower, narrower, and more skeptical than people expect after a serious loss.

Look at a standard property claim from the insurer’s side and the pattern becomes clear.

The first call opens a file and starts control measures

When you report a loss, the insurer isn’t only collecting facts. It’s classifying the event, assigning personnel, opening reserves, and routing the claim according to internal rules.

The wording used in that first report can matter. A loss described loosely may get categorized loosely. Once that happens, the file can move in a direction that’s hard to correct later. This is one reason clear timelines, cause details, and immediate conditions matter so much from day one.

The inspection is about scope, but also about containment

An adjuster’s visit isn’t only about understanding damage. It’s also the moment the insurer starts deciding what category each item belongs in, what seems covered, what seems questionable, and what can be left for later.

A policyholder who relies only on that inspection often ends up with a thin record. A stronger approach is to build an independent damage file through photos, inventories, expert input, and a careful property damage assessment. If the insurer’s estimate misses affected rooms, finishes, code issues, moisture migration, smoke impact, or business-related losses, you need your own support ready.

Documentation requests are not neutral

Insurers often ask for inventories, receipts, photos, repair records, contractor bids, sworn statements, or other documents. Some of those requests are legitimate and necessary. Some are broader than they need to be, or timed in a way that slows progress.

The key is to stay organized without handing over control of the narrative. Answer what the policy requires. Keep copies of everything. Send information in dated batches. Confirm what each submission is intended to prove.

A disorganized policyholder looks less credible, even when the loss is real and significant.

Internal metrics can tighten the file behind the scenes

Insurers monitor claims performance using Key Risk Indicators, or KRIs. According to Riskonnect’s guide to insurance risk monitoring, carriers may track metrics such as claims cycle time over 30 days or a loss ratio above 65%, and automated systems can deliver 20 to 40% faster risk detection. In practical terms, managers can see when an office or adjuster is paying more than expected or taking too long, then push for tighter controls.

That helps explain a lot of real-world behavior:

- Extra estimate reviews can appear after a payment recommendation rises.

- Manager approval delays may show up on larger files.

- Vendor referrals may be steered toward cost certainty.

- Line-item challenges may increase when the file starts trending upward.

Preferred vendors serve the insurer’s needs first

Preferred mitigation or repair vendors aren’t automatically bad. Some do excellent work. But the reason carriers like managed networks is predictable pricing, standardized reporting, and tighter control over claim development.

That can conflict with the policyholder’s goals. A vendor focused on speed and insurer alignment may not document the full scope the way an owner needs for settlement. Always separate emergency mitigation from valuation. Drying the building is one issue. Proving the full amount owed is another.

When you view the file through the insurer’s risk lens, the process feels less random. Every step has a control function. Once you see that, you can respond with your own structure instead of hoping the company will build your case for you.

Common Insurer Tactics and How to Respond

The most frustrating claims are rarely denied with dramatic language. They’re narrowed, delayed, fragmented, and worn down. That approach fits the internal logic of risk management in insurance companies. A carrier doesn’t need to say “we won’t pay.” It often gets nearly the same result by shrinking scope, slowing momentum, and making the policyholder do all the heavy lifting.

The good news is that these tactics are predictable.

The quick low offer

This usually appears early, especially when the owner is overwhelmed, displaced, or desperate to start repairs. The offer may be framed as practical help. In reality, it can lock the claim into an undersized scope before the damage is fully understood.

What works is slowing the decision down without stalling the claim.

- Request the estimate in full. Don’t respond to a lump-sum number without line items.

- Compare room by room. Look for omitted demolition, finish matching, code-related work, overhead, and debris handling.

- Separate emergency cash from final value. An initial payment can be appropriate without ending the valuation dispute.

The delay game

Some delays are legitimate. Many aren’t. Files get transferred. Desk adjusters change. Supplemental reviews sit untouched. Questions get asked one at a time instead of all at once.

Delay is powerful because property owners have mortgages, rent, payroll, tenants, and contractor schedules. The insurer knows pressure builds on your side first.

A disciplined response includes:

- Create a claim timeline. Record calls, emails, inspections, submissions, and unanswered requests.

- Confirm every conversation in writing. A short email after a call changes the file.

- Ask specific questions. “What documents are still needed?” works better than “Any update?”

- Set response deadlines politely. Give dates, not open-ended requests.

Don’t argue with drift. Box it in with dates, documents, and direct questions.

The policy language squeeze

A common tactic is selective interpretation. The insurer highlights a limitation, condition, or exclusion while downplaying endorsements, restoration provisions, additional coverages, or favorable definitions.

That doesn’t always look like an outright denial. Often it shows up as a narrow reading of what must be repaired, what caused the damage, or what category of payment applies.

Your response should be just as specific:

- Read the entire policy section, not one quoted clause. Terms often interact.

- Ask the adjuster to identify the exact policy basis for each disputed item.

- Match facts to language. If the insurer says something is excluded, ask how it classified causation and why.

- Keep the dispute anchored to text and evidence. Emotion won’t beat a policy interpretation issue.

A useful breakdown of common insurance adjuster tricks can help you recognize when a “policy explanation” is really a negotiation tactic.

The undervaluation of scope

This is the most common problem in serious property claims. The insurer may agree there is covered damage, but estimate too little demolition, too few materials, too low a labor allowance, too narrow a repair area, or too little impact to contents and business operations.

In this scenario, owners incur financial losses. The file remains “open,” the adjuster sounds cooperative, and yet the estimate never reaches the true cost to restore the property.

One reason this happens is inconsistency inside the insurer itself. According to Risk & Insurance’s reporting on resilience adoption gaps, fewer than one in four insurers have successfully integrated resilience into daily operations. That implementation gap shows up as uneven handling, variable standards, and adjuster-to-adjuster differences. For policyholders, that inconsistency creates openings. If one representative says one thing and another says something else, document the difference and press for a written position.

Insurer tactics vs policyholder responses

| Insurer Tactic (Driven by Risk Management) | Your Empowered Response |

|---|---|

| Early low estimate to cap the file | Demand a line-item breakdown and compare it to actual damage |

| Slow rolling requests and reviews | Maintain a dated log and force specific written answers |

| Narrow reading of policy terms | Request exact policy support for each limitation or denial |

| Partial scope acceptance | Build a complete room-by-room or system-by-system damage package |

| Staff inconsistency across adjusters | Use the insurer’s conflicting statements against the weak position |

| Preferred vendor steering | Separate mitigation needs from settlement valuation |

What property owners in Oregon and Washington should remember

Wildfire smoke claims, wind-driven rain, frozen pipe losses, commercial water intrusions, and storm-damaged roofs often involve hidden scope. The insurer benefits when those hidden items stay hidden.

Your influence grows when you do three things well:

- Build a better factual record than the insurer has.

- Keep every dispute tied to the policy and the physical damage.

- Refuse to let speed pressure turn into value pressure.

The insurer’s system is designed to manage risk. Your job is to make underpayment riskier for the insurer than fair payment.

Taking Control of Your Claim in Oregon and Washington

Once you understand how insurers think, the next move is practical. Build a claim that is harder to minimize.

That means acting early, documenting thoroughly, and knowing when to bring in help. Property owners in Oregon and Washington often wait too long because they assume the carrier will catch up. It usually won’t. The stronger file wins.

Build proof before the dispute grows

Start with the property itself. Walk the site slowly. Capture wide video, close-up photos, and every affected area, even if the damage seems obvious. In smoke, water, or storm claims, conditions can change fast after mitigation and cleanup begin.

Then build the claim file around categories of loss:

- Structure means finishes, framing, roofing, windows, built-ins, mechanical systems, and code-related items.

- Contents means damaged personal property, business personal property, stock, equipment, and specialty items.

- Use and income impacts mean extra living expense, loss of rents, business interruption, relocation costs, and related disruption.

Use outside experts when the damage is technical

Not every claim needs a large team. Some do.

Contractors can identify repair scope. Engineers can address structural movement or causation disputes. Hygienists can document contamination issues. Accountants can help with business loss calculations. The point isn’t to overcomplicate the file. The point is to avoid letting the insurer define technical issues without challenge.

Insurer systems are often less coordinated than they appear. According to Secureframe’s 2025 risk management statistics summary, only 35% of financial leaders report thorough ERM processes and just 32% rate their oversight as mature. In plain language, internal insurer processes can be fragmented. A well-supported policyholder file can expose those gaps.

When the insurer’s departments don’t line up, a clear and fully documented claim package can force alignment.

Know when a public adjuster becomes a smart move

Some claims are manageable without representation. Others stop being simple the moment the numbers, damage pattern, or policy issues expand.

Consider getting professional help when:

- The loss is large or multi-layered. Fire, major water, storm, collapse, or mixed-cause losses can overwhelm an owner fast.

- The insurer’s estimate feels incomplete. Missing rooms, low quantities, excluded line items, or unexplained depreciation are warning signs.

- The file keeps changing hands. Rotating adjusters often mean lost momentum and conflicting instructions.

- You’re too busy to run the claim properly. Business owners, nonprofits, schools, and municipalities often can’t spare the internal time.

- Coverage issues are emerging. Once the dispute shifts from price to policy interpretation, precision matters more.

A local action plan that actually helps

For Oregon and Washington property owners, the most useful approach is plain and disciplined:

- Protect the property and stop further damage where safe.

- Notify the insurer promptly and keep the first report accurate.

- Document all damage before repairs alter the scene.

- Read the policy, especially duties after loss and valuation provisions.

- Get independent repair or replacement input.

- Track every extra cost and every insurer communication.

- Escalate early if the claim starts drifting or shrinking.

This is how you take control back. Not by arguing louder. By building a file the insurer has to respect.

From Risk Subject to Empowered Advocate

After a major property loss, policyholders often feel outmatched. That reaction makes sense. The insurer has systems, software, internal guidelines, approved vendors, and experienced adjusters. You have a damaged property and a stack of unfamiliar paperwork.

But the gap closes once you understand what’s really happening.

Your policy is a product. Your claim is a negotiation inside that product. The insurer’s decisions are shaped by underwriting choices, financial controls, operational metrics, and internal risk management priorities. Once you stop treating the process like a simple request for help, you start making better moves. You document more carefully. You ask narrower questions. You challenge unsupported positions. You strengthen your position.

That shift is the primary advantage.

You don’t need to become an insurance executive to protect yourself. You just need to see the claim from both sides. The insurer is managing exposure. You should be managing proof.

For homeowners, business owners, nonprofits, schools, and municipalities in Oregon and Washington, that perspective changes everything. It turns a confusing process into a structured one. It turns delay into a record. It turns a low estimate into a rebuttable position. And it turns you from the subject of the insurer’s risk process into the advocate for your own financial recovery.

If your property claim in Oregon or Washington feels stalled, undervalued, or far more complicated than it should, NW Claims Management can help you level the field. Their licensed public adjusters represent policyholders, not insurers, and handle the documentation, policy analysis, damage assessment, and settlement negotiation needed to pursue a fair result.