The smell hits first. Wet drywall. Burned wiring. Smoke in fabric. Or that strange muddy odor after water sat where it shouldn't have. You walk through your home trying to decide what matters most, the soaked floors, the blistered paint, the warped cabinets, the roof, the temporary place your family may need to stay, the phone calls you haven't returned.

Then the insurance claim starts, and suddenly the damage isn't just physical. It's administrative. You're asked for inventories, photos, estimates, dates, explanations, receipts, recorded statements, and forms written in language that seems designed for everyone except the person who just had the loss.

If you're in Oregon or Washington, this part can feel especially disorienting after a fire, storm, pipe break, or vandalism event. A leak that looked minor on day one can become something far bigger once moisture spreads into drywall, insulation, or framing. If you need a simple explanation of why property leaks are serious, that overview helps show why early documentation matters so much.

Most homeowners begin by trying to handle everything themselves. That's understandable. But after a serious loss, your energy belongs with your family, your housing, your routine, and your recovery. If you're dealing with fire damage, this practical guide on what to do after a house fire insurance claim can help with the first immediate steps.

A public adjuster enters the picture as your advocate. Not the insurance company's representative. Yours. Think of that role as a professional ally who takes the claim off your shoulders, organizes the facts, documents the loss properly, and pushes for the full benefits your policy may provide.

Your World Just Turned Upside Down Now What

The first days after a loss rarely feel orderly.

A windstorm tears shingles off your roof and rain finds its way into the attic. A kitchen fire leaves smoke damage in rooms that never burned. A pipe bursts while you're away for the weekend, and by the time you get home, flooring is buckled and parts of the wall feel soft to the touch. You may still be asking basic questions. Can you stay in the home? What should you throw away? Who do you call first? What if the insurance company's first assessment misses something important?

That uncertainty is where many people start making understandable mistakes. They clean up too quickly without enough photos. They trust a quick visual inspection. They assume the insurer's estimate is complete because it looks official.

The burden most homeowners don't expect

The hard part isn't only the damage. It's the claim itself.

Insurance companies speak in terms like scope, depreciation, exclusions, endorsements, actual cash value, replacement cost value, and proof of loss. Most homeowners don't use those terms until they have no choice. And when you're already sleeping poorly and juggling contractors, school schedules, work, or temporary housing, learning a new system under pressure can feel impossible.

You don't have to become an insurance expert just because your property was damaged.

A public adjuster helps restore some order. Instead of you trying to chase every form, inspection, and estimate while also living through the disruption, the adjuster steps in to manage the claim side of the recovery.

A different kind of help

This isn't the same as hiring a contractor.

A contractor repairs the property. A public adjuster evaluates the insurance claim, reviews the policy, documents the damage, and negotiates with the carrier. Those are different jobs. One rebuilds the structure. The other fights to make sure the insurance funding reflects what the policy may owe.

That distinction matters early. The sooner the loss is documented clearly and completely, the easier it is to avoid missing damage that shows up later.

Who Is Actually on Your Side in an Insurance Claim

One of the biggest points of confusion in property claims is the word adjuster. Homeowners hear it and assume every adjuster is there to help them equally. That isn't how the system works.

A public adjuster is best understood as the property claim equivalent of a representative who works only for you. By contrast, the adjuster sent by the insurance company works for the insurer. Even if that person is courteous and professional, their role is different from yours.

The three adjuster types

There are usually three categories homeowners encounter:

Company adjuster

This adjuster is employed by the insurance carrier. Their job is to investigate and adjust claims on the insurer's behalf.Independent adjuster

This adjuster isn't your independent advocate. "Independent" means they are contracted by the insurance company rather than employed directly by it. They still represent the insurer's side of the claim. This overview of an independent adjusting company can help clarify that distinction.Public adjuster

This adjuster represents the policyholder, not the insurance company. Their duty is to prepare, present, and negotiate the claim in the insured's interest.

That difference isn't semantic. It affects how the damage is interpreted, how the estimate is built, what policy benefits are pursued, and how hard someone pushes when the insurer's position falls short.

Public Adjuster vs. Company Adjuster vs. Independent Adjuster

| Attribute | Public Adjuster | Company Adjuster | Independent Adjuster |

|---|---|---|---|

| Who they work for | The policyholder | The insurance company | The insurance company that hires them |

| Who they represent in the claim | Your interests | The carrier's interests | The carrier's interests |

| How they're paid | Typically contingency-based from the settlement | By the insurer | By the insurer |

| Main objective | Document and pursue the fullest covered recovery available under the policy | Adjust the claim for the insurer | Adjust the claim for the insurer |

| Who controls the relationship | You do | The insurance company does | The insurance company does |

Why this distinction matters in real life

A homeowner often assumes the insurer's adjuster will naturally uncover every item that should be paid. Sometimes important items are included. Sometimes they aren't. The challenge is that losses are rarely simple.

Hidden moisture may not be visible at first. Smoke can travel into HVAC systems, insulation, and adjacent rooms. Roof or siding damage can create interior issues that emerge later. Business owners may also face operational losses that aren't obvious from a site visit alone.

Practical rule: If someone was assigned by the insurance company, that person is there to adjust the claim for the insurance company.

That doesn't make insurer adjusters villains. It means you should understand the structure you're operating inside. The policyholder and the insurer don't always have the same financial interests in a disputed or complicated claim.

Why homeowners in Oregon and Washington often call later than they should

Many people wait until they're already frustrated. They've had several calls with the carrier, seen an estimate that feels incomplete, or realized the process is absorbing hours every week. By then, stress has already shaped the claim.

A public adjuster can still help at that point in many situations, but the earlier your side begins documenting and valuing the loss, the better positioned you are. The strongest claims are usually built, not improvised.

What a Public Adjuster Actually Does for You

The first week after a fire, burst pipe, or wind loss often feels like a second job you never asked for. You are answering calls, trying to understand your policy, meeting inspectors, and making repair decisions while your home or business is still unsettled. A public adjuster steps into that confusion as your representative, with one job: build, present, and defend your claim from the policyholder's side.

It begins with reading the policy like a map

Homeowners usually start with the damage they can see. A public adjuster starts by pairing the facts of the loss with the language of the policy.

That means reviewing the forms, endorsements, exclusions, limits, and claim conditions that may affect payment. Repair costs are only part of the picture. Depending on the loss, there may also be questions about debris removal, code upgrades, additional living expenses, business interruption, or whether the carrier is applying replacement cost or actual cash value.

This matters for a simple reason. If a covered part of the claim is never identified and supported, it may never be paid.

Then the loss has to be documented in a way the carrier can evaluate

A public adjuster does more than take photos and send them in. The work is closer to building a case file. Every room, material, and category of damage has to connect to evidence, scope, and policy support.

That can include visible structural damage such as roofing, siding, drywall, flooring, cabinets, and finish materials. It can also include the parts of a loss that homeowners often miss at first, like smoke inside an HVAC system, moisture behind a wall cavity, odor that requires cleaning beyond the burned area, or extra costs from being displaced.

Some firms use tools such as moisture meters, thermal imaging, drones, and 3D documentation to record conditions that are hard to see from a quick walk-through. As Allied Public Adjusters explains in its overview of the role, those tools can help identify hidden damage and create a more precise record of the loss.

The estimate must be detailed enough to stand on its own

Insurance claims are often won or lost in the scope of work. If the estimate leaves out insulation behind wet drywall, paint blending in adjacent rooms, detached structures, or code-required work, the payment discussion starts from an incomplete foundation.

A public adjuster prepares a line-item estimate in a format carriers recognize, often using Xactimate. That is one reason a formal property damage assessment service can make such a difference. It turns a general complaint into a documented position with measurements, quantities, material assumptions, and pricing the insurer can review line by line.

The process works like preparing plans before construction. If the plans are vague, the result is usually incomplete and disputed. If the scope is clear, disagreements become narrower and easier to address.

Your claim file becomes your main tool in negotiation

A well-prepared submission usually includes several pieces working together:

- An itemized estimate with scope and pricing

- Photographs and imaging that show both obvious and less visible damage

- Written explanation connecting the damage to the cause of loss

- Policy support showing why each category is being claimed

- Proof of loss materials if the policy or carrier requires them

Many overwhelmed policyholders feel relief. Instead of trying to argue from memory during a stressful phone call, you have a documented file that supports the amount being requested.

If an estimate cannot be explained line by line, it becomes much harder to challenge an underpayment.

A public adjuster also handles the back-and-forth with the carrier

This part is easy to underestimate until you are living through it.

The insurer may request documents, schedule inspections, ask follow-up questions, revise estimates, or dispute parts of the scope. A public adjuster manages those communications, attends inspections, organizes the claim materials, and responds with evidence instead of frustration. You still control the major decisions. You are not left to translate insurance language on your own.

One Oregon-based example, NW Claims Management's public adjusting work, follows this model of policy review, damage documentation, valuation, and insurer communication for property claims. That is the standard to look for from any firm you are considering.

At its core, the role is simple to describe even if the work is detailed. The insurer's adjuster measures the claim for the insurance company. A public adjuster measures it for you.

The Measurable Benefits of Expert Representation

Most homeowners ask the same question at some point. Is hiring a public adjuster worth it?

The clearest answer is financial. Research summarized by Stax on the role and value of public adjusters states that public adjusters typically increase claim payouts by 25% to 75% compared to initial insurance carrier estimates. In the example provided there, a $100,000 initial offer could become $125,000 to $175,000 or more depending on the claim.

That difference doesn't come from magic. It usually comes from identifying what was omitted, documenting hidden damage, interpreting the policy correctly, and negotiating from a stronger factual record.

Better recovery usually starts with better scope

An underpaid claim often begins with an incomplete scope of loss.

Maybe the estimate covers replacing a section of drywall but not the insulation behind it. Maybe it includes roof repair but not interior staining, painting continuity, or moisture mapping. Maybe a displaced family doesn't realize they may need to document temporary living costs. Business owners can run into the same problem with income-related losses, record reconstruction, and expense analysis. In more complex files, forensic accounting services for insurance claims can support the financial side of that documentation.

A public adjuster helps build the claim around the full covered impact, not just the most visible repair.

The value isn't only the settlement amount

Homeowners often underestimate the sheer number of hours a difficult claim can consume.

Consider what falls on your plate if you handle everything alone:

- Phone calls and follow-up with adjusters, desk examiners, contractors, and vendors

- Document assembly for receipts, inventories, photos, reports, and repair estimates

- Inspection coordination when different professionals need access to the property

- Dispute management when the insurer's estimate leaves out major items

Those tasks can stretch for weeks or months, especially when the property isn't fully livable or your business is trying to resume operations.

A claim can become a second job right when your real life already needs more from you.

Stress relief is a real outcome

This benefit is harder to put into a spreadsheet, but homeowners feel it quickly.

When someone experienced takes over the claim presentation and negotiation, you stop having to decode every email or wonder whether you're missing something important. Instead of reacting to the insurer one request at a time, you have a plan, a file strategy, and a professional buffer between your family and the bureaucracy.

That doesn't mean every claim becomes easy. It means the process becomes more manageable. After a serious loss, that matters.

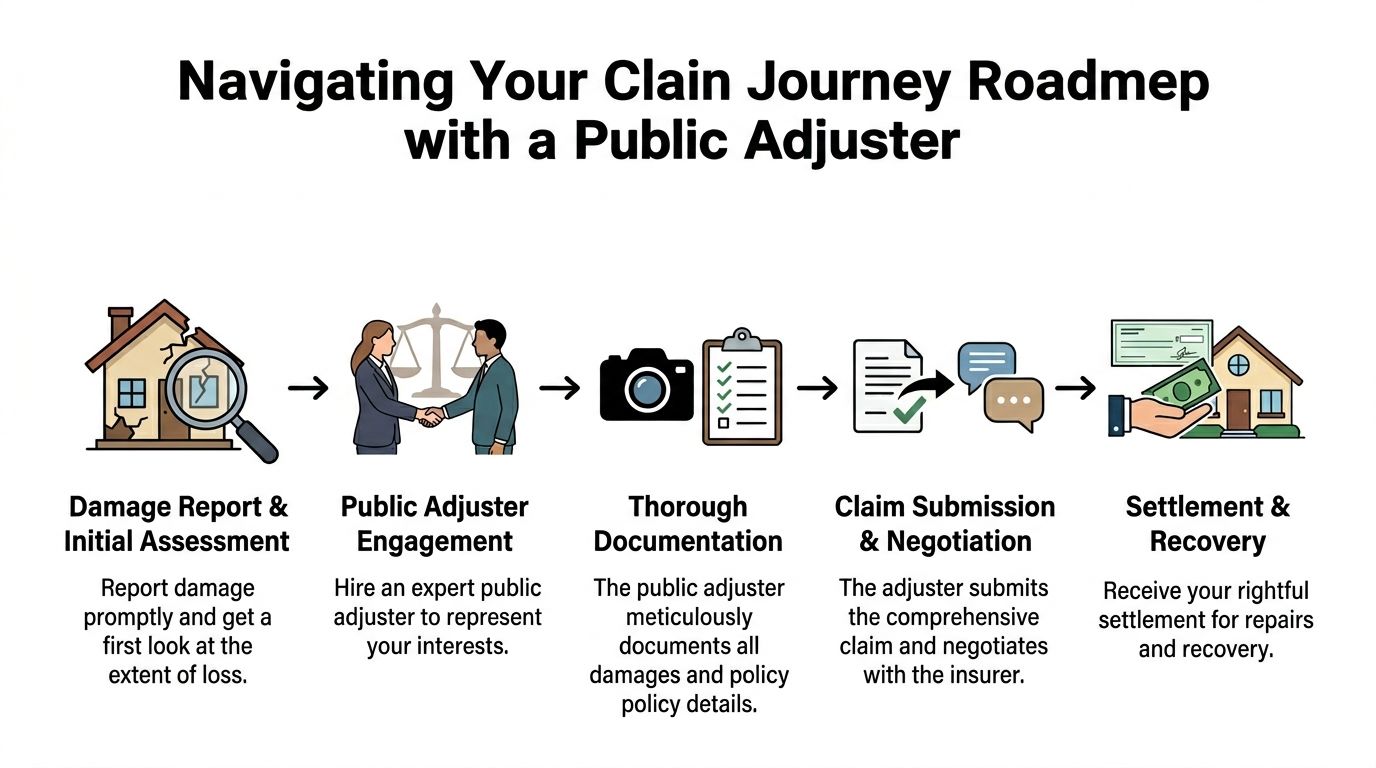

The Claims Journey: From Damage to Payout

The first days after a fire, major water loss, or wind damage often feel blurry. You are trying to protect the property, answer insurance questions, and make basic family decisions at the same time. A public adjuster brings order to that chaos, but just as important, they shift the claim from the insurer's timetable to a process built around your interests.

If you want a broader view of timing and claim stages, this guide to the home insurance claim process pairs well with the step-by-step outline below. A useful outside perspective, Awesim Building Consultants on home insurance, also explains the practical sequence from damage to documentation to settlement.

Step 1 starts with understanding the loss and the policy

A good claim does not begin with arguing about numbers. It begins with getting clear on what happened, what the policy may cover, what the insurer has already done, and what problems could slow the claim down later.

That early review usually includes the date and cause of loss, emergency mitigation work, prior inspections, temporary repairs, living situation issues, and any payments or reservation of rights letters already issued. For homeowners in Oregon or Washington, this stage matters because weather-related losses, hidden moisture, smoke migration, and code-related repairs can create questions that are easy to miss at the start.

Step 2 changes who is carrying the claim

Once you hire a public adjuster, the insurance company is notified that you have your own representative.

That matters more than people expect. The carrier's adjuster still represents the insurance company. Your public adjuster represents you. From that point on, requests, scheduling, document flow, and claim discussions have a professional structure instead of landing on your kitchen table one email at a time.

Many homeowners feel their first real sense of relief here.

Step 3 builds the factual record

Insurance companies pay based on what can be supported. If the file is thin, the claim usually stays smaller than it should.

So this phase is about building a record that reflects the full covered impact. The public adjuster inspects the property closely, measures damaged areas, reviews photos and mitigation records, studies contractor findings, and identifies losses that are less obvious than torn drywall or burned framing. Smoke damage in adjacent rooms, moisture trapped behind finishes, debris handling, code upgrades, and personal property issues often become clearer during this stage.

A claim file works like a blueprint. If key rooms, materials, or costs are missing from the plan, they rarely appear in the finished result.

Step 4 turns damage into a claim presentation

After the evidence is organized, the public adjuster prepares the formal submission for the insurer. That can include line-item estimates, inventories, summaries of damage, supporting reports, and policy-based explanations for why certain items belong in the claim.

For the homeowner, the process often becomes easier to follow. You are no longer looking at a pile of disconnected photos, invoices, and notes. You have a claim package that tells a coherent story and ties the loss back to the policy.

That difference is important. The insurer's adjuster is evaluating what the carrier owes. Your public adjuster is presenting the fullest supported version of what you are entitled to recover.

Step 5 is the back-and-forth with the insurer

Submission is rarely the finish line. It is usually the point where the dispute, if there is one, becomes visible.

The insurance company may agree with part of the estimate, reject part of it, ask for more support, or rely on a competing scope and price sheet. Your public adjuster answers those positions with documentation, revised calculations where appropriate, and direct discussion about coverage, pricing, and scope. A strong file gives the insurer less room to dismiss major items with a short explanation.

Good negotiation usually starts long before the first phone call. It starts in how well the loss was documented.

Step 6 ends with payment, and sometimes follow-up

Once the covered amount is agreed on, the insurer issues payment according to the policy terms and the claim's status.

That can mean more than one check. Some claims involve actual cash value first, then recoverable depreciation later. Others involve mortgage company endorsement, supplemental claims for damage found during repairs, or separate handling for contents and structure. Settlement is a major milestone, but it is not always the last piece of paperwork.

What your role looks like along the way

You still make the decisions. You still review major developments. You may still need to provide receipts, photos, or access to the property.

But you are no longer expected to decode policy language, spot missing categories of loss, or answer every insurer request without help. That is the practical difference between facing the claim alone and having a dedicated advocate whose job is to protect your side of the file.

How to Choose the Right Public Adjuster Firm in 2026

Not every firm offering public adjuster services works the same way. After a major loss, that matters. You need someone who can build a claim, not just promise to "fight for you."

Start with licensing and claim type fit

For Oregon and Washington property owners, first confirm the firm is properly licensed for the jurisdiction involved. Then ask a more practical question. Have they handled your type of claim before?

A residential fire, a commercial water loss, a church roof collapse, and a wind-driven rain claim may all fall under property insurance, but they don't present the same challenges. Some require stronger building documentation. Others require business records, code-related analysis, or coordination with multiple stakeholders.

Ask how they build the claim

Don't settle for general assurances. Ask direct questions like:

- What does your damage documentation include

- Do you prepare line-item estimates

- How do you identify less obvious categories of loss

- Who communicates with the insurer once you're hired

- Will I receive copies of the estimate and claim package

A serious firm should be able to explain its process in plain language. If the answer sounds fuzzy, overly sales-driven, or evasive, keep looking.

Understand the fee before you sign

Public adjuster fees typically range from 5% to 15% of the final settlement, and many states impose caps, according to the AAICP claims professionals survey reference. That same source notes examples such as 10% caps on residential claims in California and Texas.

For homeowners, the practical point is this. Don't ask only, "What's your fee?" Ask, "How is the fee calculated, when is it earned, and are there any state-specific caps or restrictions that apply to my claim?"

Disaster claims require extra fee questions

This is one of the least explained parts of the industry.

During catastrophic events, some states have emergency fee caps. Homeowners dealing with wildfire, flood, or storm damage are often under the most pressure exactly when they have the least bandwidth to compare contracts carefully. If a loss happened during a declared disaster or widespread catastrophe, ask whether any special fee rule applies.

Use questions like these:

- Was this loss part of a catastrophe for fee-cap purposes

- Does my state limit the fee differently after a wildfire, storm, or flood event

- Is your contingency percentage the same in disaster and non-disaster claims

- Will every fee term be disclosed in writing before I sign

If a firm is reluctant to explain its fee structure clearly, that's a warning sign.

Watch for red flags

Some concerns are less about technical skill and more about ethics and professionalism.

Red flags that deserve caution

- High-pressure signing tactics right after the loss, before you've had time to review anything calmly

- Vague promises of huge outcomes without a discussion of evidence, coverage, and scope

- Conflicts of interest where repair work and claim representation are blended unclearly

- Poor document transparency if the firm won't show you what is being submitted in your name

A trustworthy firm should welcome careful questions. You're not being difficult. You're hiring someone to represent a major financial recovery process.

The best fit usually feels clear, not rushed

After speaking with a few firms, one pattern usually emerges. The right one tends to educate instead of pressure. They answer directly. They explain the hard parts without hiding the uncertainty. They tell you what they'll do, what they need from you, and how the fee works.

That tone matters. You're choosing not just technical help, but a working relationship during a very stressful period.

Taking Control of Your Financial Recovery

After a major property loss, those affected often feel like they've lost control twice. First to the damage itself. Then to the claim process that follows.

Public adjuster services help change that. Not by erasing the disruption, but by giving you qualified representation inside a system that can otherwise feel one-sided. The insurer has professionals handling its side of the file. You have the right to your own.

That shift matters. When your claim is documented thoroughly, tied to the policy, and negotiated by someone who understands the process, you're no longer guessing your way through one of the most important financial events tied to your home or business.

If you're in Oregon or Washington and you're overwhelmed, underpaid, or unsure whether the claim has been handled completely, don't wait for confusion to harden into a bad outcome. Ask questions. Get the policy reviewed. Find out what your options are while they can still make a difference.

Frequently Asked Questions About Public Adjusting

Can I hire a public adjuster after my claim has started?

Yes, in many cases.

Many homeowners do not call until the insurer has already inspected the property, sent an estimate, or issued a payment that feels too low. That does not mean you missed your chance. A public adjuster can review the file, compare the insurer's position to the damage and the policy, and point out what may still need to be documented or challenged.

A claim works a bit like a repair estimate on a damaged home. If part of the damage was missed the first time, the file may need to be updated rather than abandoned.

What if my claim was denied or underpaid?

You may still have room to respond.

A denial or low payment can happen for several reasons. The carrier may have received incomplete documentation. The adjuster assigned by the insurer may have interpreted the cause of loss differently. The estimate may have left out items that belong in the claim. A public adjuster reviews the denial letter, policy language, photos, reports, and estimates to see whether the carrier's position holds up.

That review matters because the insurer's adjuster works for the insurance company. A public adjuster works for you.

Can I hire a public adjuster if I already accepted a check?

Sometimes, yes.

The answer depends on what that check was for and whether the claim is still open. An initial payment, an undisputed payment, or a payment for one part of the loss does not always end your right to seek more if covered damage remains unpaid. A signed final release can limit those options, which is why it helps to have the paperwork reviewed before you assume the claim is over.

How do I ask about fees after a wildfire, storm, or flood?

Ask directly. Ask in writing. Ask for the answer before you sign anything.

Fee rules can change after major disaster events, and they can also vary by state. If your loss followed a wildfire, windstorm, flood, or other large catastrophe in Oregon or Washington, ask the firm what fee applies to your claim, whether any state cap affects that fee, and how the percentage is calculated. Clear answers at the start prevent confusion later.

The goal is simple. You should know who is being paid, how they are being paid, and when.

Will a public adjuster repair my property?

No. A public adjuster handles the insurance claim.

Contractors rebuild. Engineers evaluate structural issues. Mitigation crews dry out water damage. A public adjuster prepares, values, and negotiates the claim so the insurance side is handled with the same level of care as the repair side.

Keeping those roles separate protects you because it makes each person's job easier to evaluate.

If you want a clearer picture of what your policy may cover and whether your current claim handling is complete, NW Claims Management offers claim evaluations for Oregon and Washington property owners dealing with fire, water, storm, vandalism, and other property losses.