You reopen the doors after months of repairs. The paint is fresh, the equipment is back in place, and the building finally looks like yours again. Then the hard part hits. Customers haven't fully returned, tenants are still shopping other options, staff turnover has slowed your ramp-up, and the revenue line on the books looks nothing like it did before the loss.

That stretch is where many property owners in Oregon and Washington get blindsided. They assume the insurance claim ends when construction ends. In practice, physical repair and financial recovery are rarely the same thing.

Public adjusters see this problem constantly after fire, storm, vandalism, and water losses. The property may be functional, but the business or rental operation is not yet back to normal. The policy language that can bridge that gap is the extended period of indemnity. It’s often overlooked at renewal, misunderstood during the claim, and undervalued when the carrier starts drawing a line at the date repairs finish.

The Recovery Gap After Your Property Is Repaired

A common post-loss scenario looks like this. A restaurant owner in the Northwest loses several months to a kitchen fire. Contractors finish the rebuild. Inspections clear. The doors reopen.

But reopening doesn’t restore the customer base on day one.

Regulars formed new habits during the shutdown. Search listings and social profiles need updating. Staff have to be rehired and retrained. Vendors may not be delivering on the same schedule. The owner is paying ongoing expenses while sales climb back slowly instead of snapping back overnight.

That is the recovery gap.

For a rental property owner, the same problem shows up differently. Repairs are done, but units don’t refill instantly. Prospective tenants want tours, applications, screening, and move-in time. If the property sat dark for months, the market may have moved around it.

For a nonprofit, the gap may be even harder to explain to a carrier. The building may be usable again, but donations, program attendance, enrollment, or event participation may still lag. Financial recovery can trail physical restoration by a wide margin.

This is why the first damage inspection matters so much. If the claim is framed only as a repair file, the financial tail of the loss gets ignored. A thorough property damage assessment should look past the drywall, roofing, flooring, and contents. It should identify how long normal operations may take to rebuild after the site is technically repaired.

Most disputes over extended recovery don't begin with accounting. They begin with a claim that was documented too narrowly from the start.

Insurers often focus on the date the property could reopen. Policyholders focus on the date they recovered. Those are not the same benchmark, and the difference can determine whether the claim supports a comeback or leaves the owner carrying the most painful losses alone.

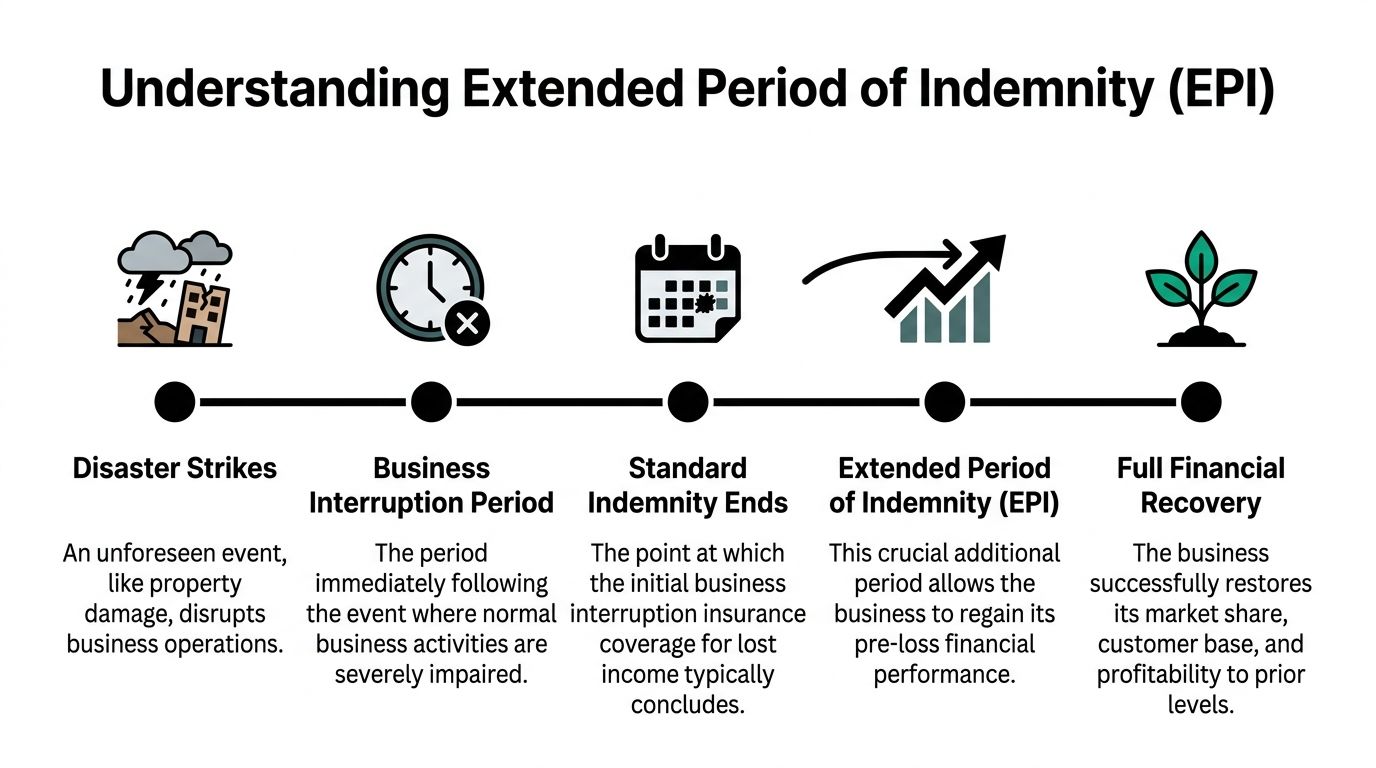

What Is an Extended Period of Indemnity

Extended period of indemnity is the part of business interruption coverage that can continue after repairs are done. It exists because a repaired property and a recovered operation are two different things.

Consider an athlete returning after an injury. Medical clearance means the healing period is over. It doesn’t mean performance is instantly back to pre-injury form. Insurance has a similar split. One period covers the time needed to repair or rebuild. The extended period of indemnity addresses the time needed to regain normal income after that point.

How the clause usually works

Standard business interruption insurance policies often include an extended period of indemnity endorsement or option that provides coverage beyond the physical repair period, typically up to 60 days after repairs are complete, with options to increase that to 30, 90, or more days depending on the policy, according to IRMI’s explanation of the extended period of indemnity endorsement or option.

That basic structure matters because many losses don't end when construction ends. A commercial rebuild might take six months, and getting revenue back to pre-loss levels can take longer, as described in the same IRMI reference.

What it covers in practical terms

The wording varies, but the purpose is consistent. This coverage is designed to respond when you can technically reopen, yet income still trails because of the interruption.

Examples often include:

- Customer return lag. A business reopens, but sales remain soft because customers found substitutes during the shutdown.

- Lease-up delay. A repaired rental property still needs time to market units, process applications, and restore occupancy.

- Reopening costs tied to recovery. Some policies may support extra expenses connected to restoring operations, such as advertising the reopening or hiring replacement staff, where the policy wording allows it.

A public adjuster reads this clause as a timing tool. The carrier may treat the claim as finished when the contractor is finished. The policyholder has to test whether the policy instead allows recovery until operations regain their pre-loss footing, subject to the wording, limits, and selected duration.

What it is not

It isn’t unlimited. It doesn’t cover every financial disappointment after a loss. And it doesn’t fix an indemnity period that was set too short before the loss happened.

What works is reading the exact trigger, end point, and time limit. What doesn’t work is assuming that any post-repair revenue dip is automatically covered. The best claims connect the continued shortfall directly to the covered damage and the interruption it caused.

Practical rule: If your claim timeline ends at substantial completion of repairs, you may be stopping the analysis too early.

Why This Coverage Is Essential for Your Financial Survival

The financial danger after a loss isn't confined to the shutdown itself. It often peaks after reopening, when revenue is still weak but payroll, debt service, utilities, taxes, and vendor obligations are back in motion.

Why repaired property doesn't mean recovered income

Owners usually know how to plan for construction. What they underestimate is the drag that comes afterward.

A business may reopen into a changed market. Staff may have moved on. Inventory levels may still be uneven. Customers may assume the location is still closed. A multifamily owner may have units ready but still need time to restore occupancy and stabilize rent collections.

Extended period of indemnity becomes less of a technical clause and more of a survival provision.

The practical value is clear in real estate losses. The Extended Period of Indemnity addresses the gap between completed repairs and lagging revenue, and for a fire-damaged apartment building it can cover ongoing vacancies during the lease-up period, potentially recovering millions in lost rent, according to this explanation of extended period of indemnity in practice. The same source also notes industry benchmarks indicating 25-30% of disrupted businesses fail within 2 years when cash flow breaks down after the interruption.

The pressure points public adjusters watch

When this coverage is absent or too short, the same problems show up over and over:

- Reopening without momentum. The doors are open, but sales volume isn't there yet.

- Income trailing while expenses normalize. The operation is paying like a healthy business before it’s earning like one.

- Rental operations losing time twice. First during repair, then again during lease-up.

- Insurer end-date pressure. The carrier points to completion of repairs as if that ends the economic damage.

If you're trying to maximize insurance claim payout, this is one of the clauses that can make a major difference. Not because it changes the physical damage claim, but because it recognizes that income loss often continues after the contractor leaves.

What works and what doesn't

A few patterns are consistent.

| Approach | What usually happens |

|---|---|

| Treating the claim as a construction timeline only | Post-repair losses get minimized or missed |

| Documenting recovery lag from the start | The claim has a stronger path to extended income support |

| Assuming customers or tenants return immediately | Financial projections look unrealistic and can hurt credibility |

| Tying the revenue shortfall to the covered interruption | The claim becomes easier to defend |

A repaired building can still be a distressed operation. Policies that ignore that gap leave owners financing their own recovery.

For commercial owners, landlords, and nonprofits, that gap can be the difference between a manageable claim and a second crisis after the first one supposedly ended.

How to Calculate and Document Your EPI Claim

Most extended period of indemnity disputes are won or lost in the records. Good claims don't just say revenue stayed down. They show what normal performance would likely have been, what happened after reopening, and why the shortfall remained tied to the covered loss.

Start with the timeline, not the total

Build the claim in two phases.

Phase 1 is the repair and restoration period. Phase 2 is the post-repair recovery period, when operations are open but still below pre-loss performance. One expert calculation for total indemnity need is Phase 1 (repair timeline x 1.5 buffer for delays) + Phase 2 (historical recovery data x industry factor), and the same analysis notes that a $10M rebuild might take 18 months, plus additional Phase 2 recovery time, in this discussion of extended indemnity planning.

That planning concept is useful even after the loss. It forces you to separate physical restoration from economic stabilization.

The documents that usually matter most

Insurers tend to ask for broad financial support. The stronger move is to organize it before they dictate the narrative.

Gather:

- Pre-loss profit and loss statements for a meaningful baseline.

- Sales reports and bank deposit records that show normal trends before the interruption.

- Post-reopening income records by week or month.

- Payroll records if staffing changes affected recovery speed.

- Leases, rent rolls, and vacancy records for rental property claims.

- Invoices for extra expenses tied to rebuilding demand, such as reopening promotion, temporary staffing, or tenant reacquisition efforts where the policy supports those items.

- Operational records that show resumed capacity versus actual market response.

Build a but-for model

The core question is simple. What would the business or property likely have earned but for the covered loss?

That model should be grounded in your own history. Seasonal businesses should account for seasonality. Growing businesses should account for credible pre-loss trends. Rental properties should compare expected occupancy and rent flow against actual post-repair lease-up.

A clean way to present it is:

- Establish the baseline using pre-loss operating history.

- Mark the repair completion date clearly.

- Track the post-repair shortfall month by month.

- Tie the shortfall to the interruption, not to unrelated business choices.

- Separate extra expense from lost income if the policy treats them differently.

For owners who want a more technical outside reference, Lighthouse Consultants has a useful guide on proving loss in business interruption insurance claims. It’s helpful because it focuses on the evidence behind the numbers rather than slogans about coverage.

Present the claim in a way adjusters can follow

A strong claim file is readable. That matters.

Use a short cover memo, a chronology, and supporting schedules. Label each exhibit. If there was a delayed reopening campaign, attach the invoices. If customer return was gradual, show the sales curve. If a building was repaired but units remained vacant, provide the leasing timeline and rental records.

This is also where understanding the property damage claim process helps. The income claim should not be floating separately from the physical damage claim. The dates, causation story, and repair milestones all need to line up.

The insurer doesn't have to guess your loss. But if you make them guess, they usually guess low.

Common mistakes that weaken EPI claims

- Using rough estimates instead of source documents

- Lumping all bad months together without identifying when repairs ended

- Ignoring seasonality

- Failing to document extra expense

- Submitting financials without explanation

The best submissions read like a file prepared for scrutiny. They are specific, dated, and tied back to the policy language.

Decoding Your Policy and Negotiating Your Rights

Extended period of indemnity claims often turn on a few phrases buried in the policy. Owners who don't slow down and read those phrases carefully can leave significant money on the table.

Three phrases that control the fight

Period of restoration usually describes the repair window. That’s the time needed to rebuild, repair, or replace damaged property and resume basic operations.

Resumption of operations often gives the insurer room to argue that once you can reopen in some form, the claim should narrow. The dispute usually becomes whether “resumed” means merely functioning or meaningfully restored.

Actual loss sustained sounds favorable, but it still requires proof. You need to show the amount of income lost because of the covered interruption, not just a disappointing reopening.

Why the time limit matters so much

Many policyholders discover too late that the claim is constrained by a short Maximum Indemnity Period. Sedgwick’s analysis states that the MIP is often set too short at 12 months, which is insufficient for nearly all businesses, and notes that a six-month repair can require another 12 months to recapture lost customers. The same analysis adds that even 18- and 24-month periods can be concerning, and Allianz recommends no less than 24 months in today’s climate, as summarized in Sedgwick’s discussion of whether 12 months is long enough.

That issue changes negotiation strategy. If the policyholder has a short MIP and only a modest extended period endorsement, the insurer may know the clock is more valuable than the damage estimate.

What insurers commonly argue

Carriers rarely say the same thing the same way, but the themes are familiar.

| Insurer position | Practical response |

|---|---|

| Repairs are complete, so income loss has ended | Point to the extended period wording and post-repair revenue evidence |

| The business could have resumed sooner | Use contractor schedules, permitting records, and operational facts |

| Sales decline was caused by market conditions, not the loss | Separate external issues from the interruption-related recovery lag |

| The insured failed to mitigate | Document reopening efforts, staffing efforts, marketing, and leasing activity |

How to negotiate from the policy outward

Start with the exact wording, not your sense of fairness. Fairness helps no one if the policy terms are ignored.

Then frame the claim around four points:

- Causation. The continued shortfall followed the covered property damage and interruption.

- Timing. Repairs ended on one date. Normal income did not return on that date.

- Evidence. Financial records and operating records prove the gap.

- Policy fit. The endorsement or business income wording contemplates this type of delayed recovery.

When communications start to drift, pin the conversation back to the policy. Ask the adjuster to identify the exact provision they rely on for any reduction, limitation, or denial. General statements about business conditions or “normal ramp-up” should not go unanswered.

If negotiations become uneven, policyholders often need a more formal approach to negotiating with insurance company. That means written position letters, organized exhibits, and a disciplined focus on dates, wording, and financial proof.

If the carrier summarizes your claim more narrowly than your policy does, correct that immediately and in writing.

What works better than outrage

Anger is understandable after a major loss. It rarely improves the outcome.

These moves tend to work better:

- Quote the policy wording directly instead of paraphrasing it.

- Tie every claimed dollar to a record.

- Create a dated recovery timeline.

- Challenge assumptions early when the insurer starts treating repair completion as claim completion.

- Escalate only after the file is organized.

A strong negotiation position isn't loud. It's documented.

Oregon and Washington Scenarios and Considerations

Oregon and Washington claims have their own rhythm. Weather-related losses, urban vacancy patterns, wildfire disruption, and contractor availability can all affect how long the road back really takes. The extended period of indemnity becomes more important when those local realities slow the return to normal operations.

Portland restaurant after a kitchen fire

A Portland restaurant may complete repairs and pass inspections, yet still reopen into thinner foot traffic and a reset customer base. The physical damage claim covers the repair side. The extended period question is whether the continued sales shortfall after reopening still flows from the covered interruption.

In practice, the strongest file includes reservation trends, point-of-sale reports, payroll restart records, vendor correspondence, and evidence of reopening efforts. A weak file indicates business was slow.

Seattle multifamily property after vandalism or fire

For Seattle-area rental owners, the issue is often lease-up rather than construction. Units may be back online, but occupancy and rental income can still lag while tenants compare options, complete applications, and wait for move-in dates.

Restoration quality also affects recovery speed. If owners are vetting contractors after a major loss, a directory of top restoration companies in Puget Sound can help narrow the field. Better repair coordination often supports a cleaner claim timeline, which matters when the insurer starts questioning when operations should have normalized.

Rural Oregon nonprofit after smoke or property damage

Nonprofits face a different challenge. Their revenue may come from grants, events, tuition, memberships, or donations rather than straight retail sales. After wildfire smoke or direct property damage, the building may reopen before attendance, programming, or community participation rebounds.

That recovery lag is real. The key is documenting it with the same discipline a commercial owner would use. Enrollment reports, canceled event records, donation timing, and program participation logs may carry more weight than generalized statements about community disruption.

Local claims are rarely just about the structure. In the Northwest, access, labor, tenant behavior, and seasonal business patterns often shape the recovery curve.

The local trade-off owners need to weigh

Owners often face a hard choice after a loss. Reopen fast in a limited way, or wait longer and reopen at fuller strength. Either path can affect the income claim.

A limited reopening can help show mitigation. But it can also give the insurer an opening to argue the business had already resumed enough to cut off the claim. That’s why the documentation needs to show not just that operations resumed, but whether operations had stabilized.

In Oregon and Washington, that distinction matters a lot. A property can be back in service while the economics remain damaged for months afterward.

When to Engage a Public Adjuster a Practical Checklist

Some extended period of indemnity claims are straightforward. Many aren't. The trouble usually starts when the policy has layered time limits, the records need forensic organization, or the insurer keeps steering the claim back to the repair completion date.

You probably need help if these apply

- Your revenue is still down after repairs are complete. That is the classic trigger for an extended period dispute.

- The policy wording is difficult to read. If you're toggling between endorsements, sublimits, and business income forms, the claim can go sideways quickly.

- The insurer keeps using the repair completion date as the end of the loss. That may or may not be right under the policy, but it should never go untested.

- Your records are spread across accountants, managers, property managers, and contractors. A scattered file usually leads to a reduced claim.

- You own a rental property, nonprofit facility, or multi-location operation. These claims often need more specific income analysis than a simple sales comparison.

- The carrier is slow, vague, or noncommittal. Delay often creates an advantage against the policyholder, especially where time-limited income benefits are involved.

What a public adjuster changes

A good public adjuster doesn't just argue for more money. Its true value is in building the claim correctly.

That usually means:

- Reading the policy for every time-based right available.

- Coordinating damage facts with financial proof.

- Presenting the claim in a structured way the insurer can't easily dismiss.

- Challenging unsupported assumptions about when the business or property was back to normal.

If you're weighing whether professional help makes sense, this guide on when to hire a public adjuster is a practical place to start.

A simple self-check

Ask yourself three questions.

Did the property recover faster than the income?

Can I prove the gap with records?

Am I confident the insurer is applying the policy language correctly?

If any of those answers is no, don't assume the claim will sort itself out. Extended period of indemnity issues are technical, but the money at stake is very real. Owners often spend months fixing the building and only then realize the larger fight is about the income that didn't come back when the repairs did.

The best time to address an extended recovery claim is before the insurer defines it too narrowly.

If your property in Oregon or Washington has been repaired but your finances still haven't recovered, NW Claims Management can review the policy, document the ongoing loss, and advocate for a settlement that reflects the full impact of the disaster, not just the construction invoice.