The call usually comes after a hard day and a harder discovery. Water on the floor. A ceiling stain that wasn't there yesterday. Shingles in the yard after a windstorm. Smoke damage in every room. In that moment, most homeowners aren't thinking about policy language, evidence preservation, or claim strategy. They're thinking, “How bad is this, and what do I do first?”

That's exactly when mistakes happen.

A homeowners insurance claim is not just paperwork. It's a documented business process with deadlines, evidence rules, and financial consequences. If you handle the first few days well, you protect both your property and your bargaining position. If you rush repairs, give incomplete information, or trust that the insurer will “sort it all out,” you can weaken your own claim before actual negotiation even starts.

People who are recovering from natural disasters often need more than sympathy. They need a calm sequence of decisions. That's what this guide is for. It lays out how to file homeowners insurance claim the right way, how to document loss so it holds up under scrutiny, and how to respond when the insurance company's numbers don't match the actual cost to repair your home.

Introduction Navigating Your Property Loss

The first hours after a property loss are disorienting. You may be dealing with emergency cleanup, a frightened family, a contractor knocking on the door, and an insurer asking for information before you've had time to think clearly. That pressure is real, and it often pushes homeowners into preventable errors.

The right approach is steady, not fast for the sake of speed. Report the loss promptly, protect the property, document everything before conditions change, and avoid making decisions that lock you into an unfair result. A claim can still go sideways even when the damage is obvious. That's why the process matters as much as the loss itself.

Practical rule: Treat the claim like a file you may need to defend later. If you can't prove it with photos, receipts, notes, or estimates, expect it to be questioned.

Insurers work from documentation. Adjusters evaluate what they can see, what they can verify, and what the policy allows. Homeowners who build a complete record early usually stand on firmer ground than homeowners who rely on memory, verbal conversations, or hurried cleanup.

There's also a human side to this. Home is where routines happen. When part of it is torn open by storm, fire, water, or vandalism, the claim becomes personal very quickly. You don't need to become an insurance expert overnight. You do need a roadmap, and you need to know where the common traps are.

Your Immediate Actions After a Loss

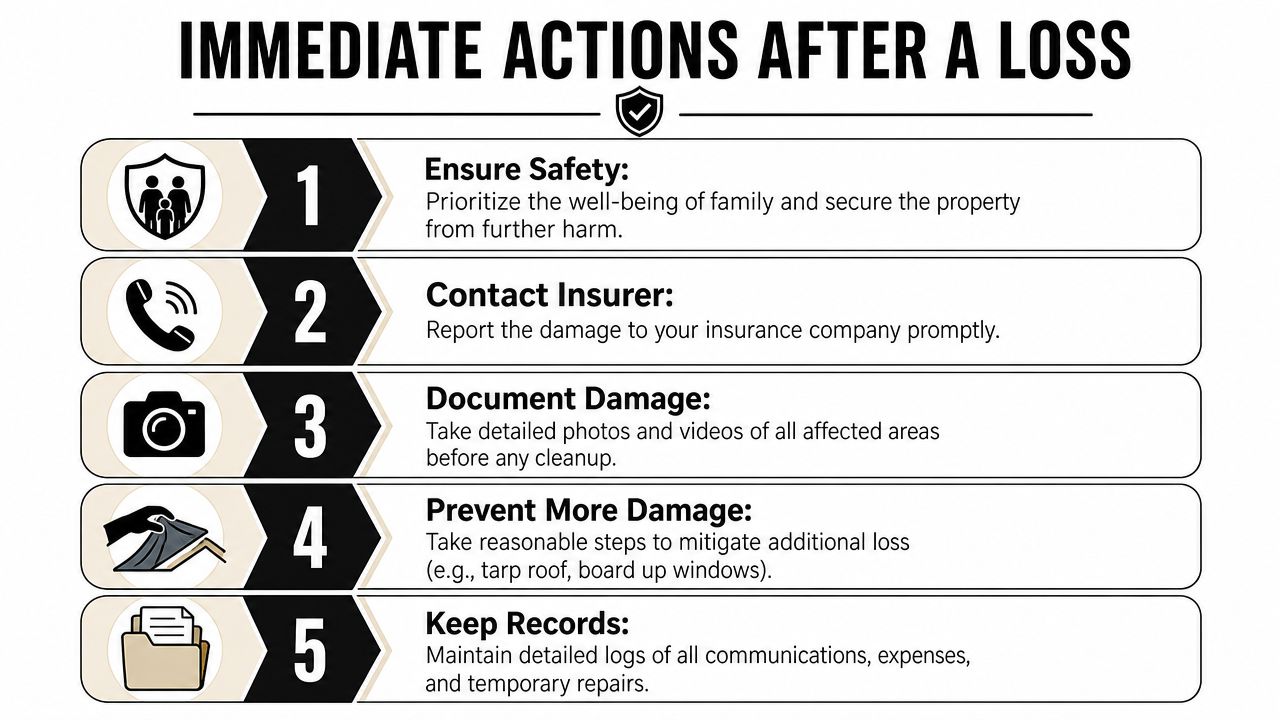

The first priority is safety. If there's active fire damage, electrical hazard, structural collapse risk, or standing water near live power, get people out and keep them out until the area is safe. Filing the claim comes after that.

In most losses, the first two days set the tone for everything that follows. You need to preserve evidence and prevent the damage from getting worse. That second part matters because policies generally require you to mitigate additional damage.

Start with the non-negotiables

Protect people first. Shut off water if a pipe burst. Cut power if it can be done safely. Leave any area that feels unstable or hazardous.

Stop ongoing damage. Board broken windows. Tarp roof openings. Move dry contents away from active leaks. These are temporary emergency measures, not full repairs.

Notify the insurer promptly. Many carriers expect immediate reporting, often within 24 to 48 hours of the incident according to homeowners insurance statistics and claim timing guidance. Waiting can invite arguments that later damage resulted from neglect.

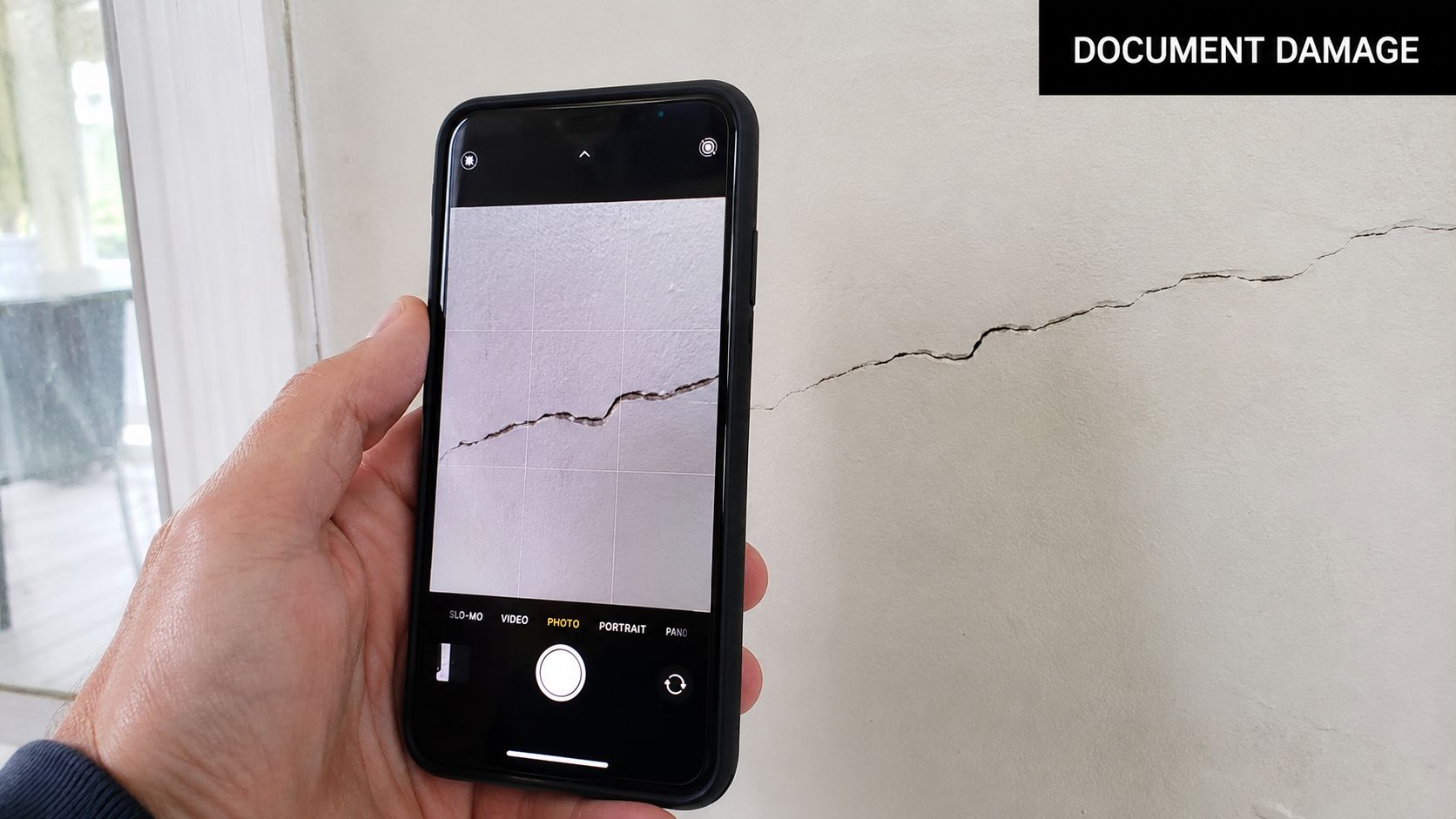

Photograph before cleanup. Don't start tossing wet drywall, flooring, insulation, or damaged personal property until you've documented what happened.

Temporary repairs versus permanent repairs

This distinction causes trouble for a lot of homeowners.

Temporary repairs are the emergency steps that keep the loss from expanding. Think tarp, board-up, plastic sheeting, fans, or shutting systems down. Permanent repairs are the fixes that change the damaged condition before inspection. Replacing roofing sections, rebuilding walls, removing all evidence of water intrusion, or fully restoring finishes too early can undercut the claim.

The Georgia Office of Commissioner of Insurance notes the importance of this distinction in its insurance claim tips for homeowners. If permanent repairs obscure the evidence, insurers may deny or reduce parts of the claim.

Save every receipt tied to emergency work. Materials, labor, equipment rental, and short-term protective measures are much easier to recover when you can show what was done and why.

What to say on the first claim call

Keep the first report factual and brief. You're opening a file, not giving a sworn narrative.

Use this basic structure:

- Policy information: Give your name, address, and policy number.

- Loss date: State the exact date of loss if known.

- Cause in plain terms: “A pipe burst under the sink,” “wind damaged the roof,” or “there was a kitchen fire.”

- Current condition: Explain whether the property is secure, partially uninhabitable, or actively taking on more damage.

- Immediate needs: Ask about inspection timing, emergency mitigation, and next steps.

Avoid guessing about cause, scope, or cost. If you don't know whether all the damage is visible yet, say so. If you're asked to speculate, don't. A rushed answer can show up later as if it were a final position.

For a practical field list you can use room by room and exterior by exterior, a property inspection checklist helps you capture damage while it's still visible.

Do not get pressured early

Some insurers move quickly. That can be helpful, but it can also create pressure. You may be asked for a recorded statement, urged to use a preferred contractor, or encouraged to move forward before you've gathered your own numbers. Slow down enough to understand what you're agreeing to.

The insurer's urgency isn't your deadline. Your job is to preserve the claim and protect your recovery.

Documenting Your Damage Like a Pro

A strong claim file doesn't happen by accident. It's built. The more serious the loss, the more you should think like a person assembling evidence, not a person “hoping the adjuster sees it.”

Progressive's guidance on how home insurance claims work makes this point clearly. A homeowners claim requires a complete inventory of damaged items, supported by high-resolution photos and original purchase receipts when available, before repairs are made.

Build the visual record first

Use your phone, but use it methodically.

Walk the entire property and capture:

- Wide shots: Each room from multiple corners. Exterior elevations from several angles.

- Mid-range shots: Damaged sections of ceiling, wall, flooring, cabinets, roofing, siding, or windows.

- Close-ups: Cracks, warping, staining, soot, blistering, broken seals, and damaged finishes.

- Item proof: Brand labels, model numbers, and serial numbers on electronics and appliances.

- Context photos: Show where each damaged item was located within the home.

Video helps too. Narrate carefully. State the room, what you're seeing, and the date. Don't editorialize. Just document.

Reconstruct your contents inventory

If you already had a home inventory, use it. Many do not. That doesn't mean you're stuck.

Start room by room. Open drawers, cabinets, closets, and storage areas. Make a spreadsheet or use a claim notebook. For each item, list what it was, where it was, its approximate age, and what it would cost to replace with something similar today.

A useful format looks like this:

| Area | Item | Details to note |

|---|---|---|

| Living room | Television | Brand, model, size, purchase date if known |

| Bedroom closet | Clothing | Type, quantity, labels, photos |

| Kitchen | Small appliances | Brand, model, condition before loss |

| Garage | Tools | Set contents, manufacturer, photos of cases |

If receipts are missing, look for confirmation emails, bank statements, product registration emails, old photos from holidays or real estate listings, and warranty documents. Those records often prove ownership and quality better than memory alone.

For homeowners rebuilding this list from scratch, a personal property inventory template can keep the process organized.

Keep a claim journal

This is one of the simplest habits and one of the most valuable.

Every time you speak with the insurer, mitigation company, contractor, police officer, or government office, log:

- Date and time

- Full name

- Job title or role

- Phone number or email

- What was discussed

- What they promised next

Travelers notes in its home insurance claim process overview that keeping a detailed contact log creates a verifiable audit trail. That matters when conversations start to blur together or when someone says, “We never received that.”

A claim journal turns a confusing process into a timeline. Timelines are persuasive because they're hard to argue with.

One habit that protects your leverage

Don't throw away damaged items too soon unless they create a safety issue. If disposal is necessary, photograph them thoroughly first and document why removal was required. Once the evidence is gone, you lose part of your ability to prove scope and condition.

That's the practical core of how to file homeowners insurance claim well. The homeowner who documents before changing the scene usually has the stronger file.

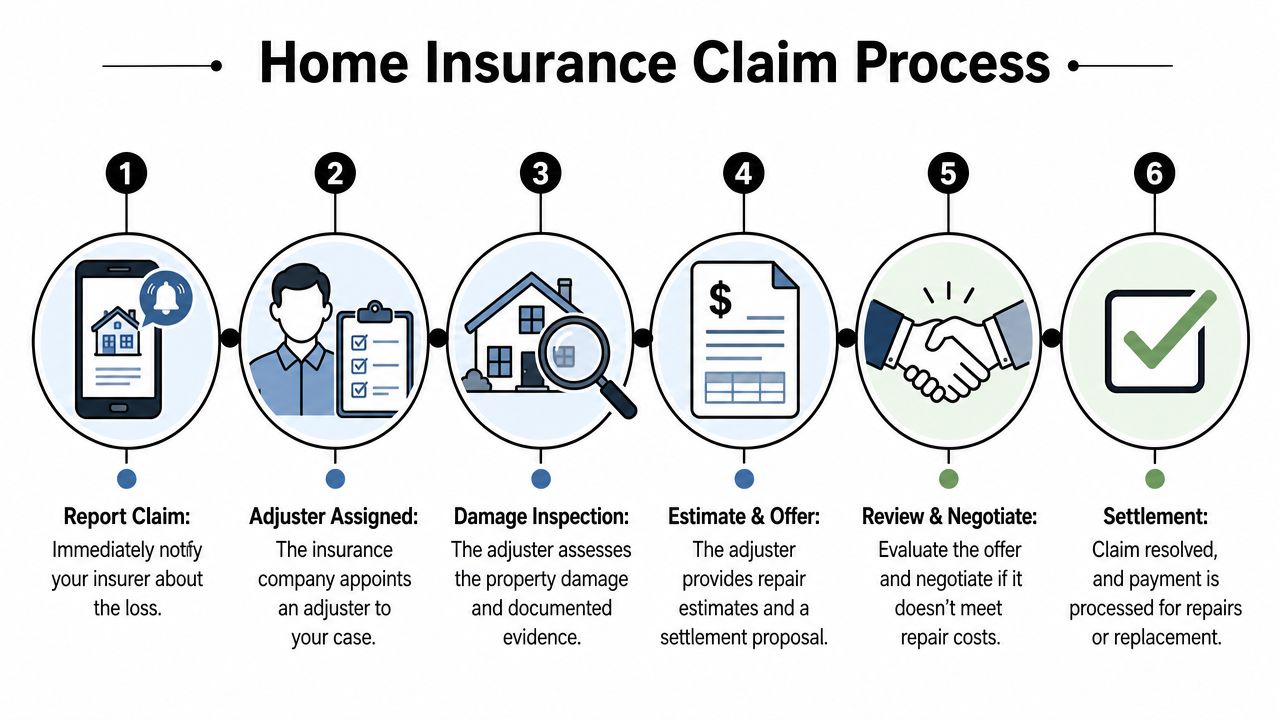

Managing the Claim Process and Your Adjuster

The first inspection often sets the tone for the whole claim.

A homeowner calls us after a fire or storm and says, “The adjuster was here for 20 minutes. He seemed nice. I guess now I wait.” That is the moment many claims start drifting off course. If the inspection misses rooms, materials, secondary damage, or code-related items, the estimate that follows is usually missing them too.

After you report the loss, the insurer assigns an adjuster. That may be a staff adjuster employed by the carrier or an independent adjuster hired by the carrier. Both work for the insurance company. Their task is to evaluate the claim under the carrier's procedures and policy interpretation. Your task is different. You need to make sure the scope is complete, the pricing reflects real repair conditions, and nothing covered gets left out because it was not obvious on day one.

What usually happens next

The basic sequence is familiar. The pressure points are not.

| Stage | What happens | What you should do |

|---|---|---|

| Claim opened | Carrier assigns a claim number and adjuster | Confirm who is handling the file and how they want documents submitted |

| Inspection scheduled | Adjuster sets a site visit | Reserve enough time, gather your repair concerns, and ask who will attend |

| Inspection completed | Adjuster reviews damage and cause | Walk with them, room by room, and make sure each damaged area is discussed |

| Estimate issued | Carrier sends its valuation | Review line by line for missing materials, quantities, labor, and code items |

| Payment or partial payment | Initial funds may be issued | Confirm whether depreciation is being withheld and what must be submitted to recover it |

Expect pauses between these steps. An inspection can happen quickly, then the file sits while photos are uploaded, notes are reviewed, or a supervisor signs off. Silence does not always mean trouble, but unreturned calls and vague answers should be documented and followed up in writing.

Prepare for the inspection like you are building the record

Be there if you can. If you cannot, send someone who knows the property and the damage.

Walk the adjuster through the loss in a logical order. Start where the damage began, then show where it spread. On water losses, that means tracing the path of moisture, not just pointing to the stained ceiling. On fire claims, that means discussing smoke, soot, odor, and cleaning needs, not just visible burn damage. On wind claims, that means checking elevations, gutters, windows, fencing, and detached structures, not just the main roof slope visible from the street.

Use a written list during the walk-through. A verbal comment is easy to forget. A written item is harder to ignore.

A regional example helps. For contractor-side context on how exterior losses are often organized and presented, this Kansas City storm damage claim guide shows the kind of jobsite coordination that can influence roofing and siding claims.

Understand the first estimate before you react to the first check

The insurer's estimate is not the claim. It is the carrier's current position based on the information in the file at that moment.

That distinction matters because many homeowners assume the first estimate reflects everything the adjuster saw. In practice, it may exclude items the adjuster considered unrelated, items hidden from view, overhead and profit, debris handling, permit costs, or work that becomes clear only after demolition. Review the estimate line by line. If a room was affected but not listed, raise it. If materials are wrong, raise it. If the pricing does not match what qualified local contractors are charging, get written support.

Payment structure also causes confusion. Many policies pay actual cash value first and hold back depreciation until repair or replacement is completed. Even on a replacement cost policy, the initial check may be lower than the total approved amount. That is not automatically improper, but it needs to be tracked carefully so recoverable depreciation does not get missed.

If the carrier asks for a signed, sworn accounting of your damages, stop and read before signing. That document can shape the rest of the claim. A plain-English explanation is here: what a proof of loss requires and why it matters.

How to deal with the adjuster without giving up ground

Professional, detailed communication works best. Hostility usually wastes time, but passivity costs money.

Use these habits:

- Confirm important conversations by email. If the adjuster says they will add an item, inspect again, or issue supplemental payment, send a same-day recap.

- Ask direct questions. If something was denied or omitted, ask whether the issue is causation, scope, pricing, depreciation, or policy language.

- Request the estimate promptly. Do not rely on a summary over the phone.

- Separate facts from assumptions. Describe what was damaged, when it was observed, and what qualified contractors found.

- Escalate carefully. If the file stalls, ask for a supervisor review before the delay becomes normal.

A few mistakes weaken a claim fast. Guessing at repair cost. Accepting “we can deal with that later” without written confirmation. Letting an inspection happen with no one present to identify less obvious damage. Signing broad releases before the scope is settled.

I tell clients this all the time. A polite homeowner with a disciplined paper trail usually has a stronger position than an angry homeowner with none.

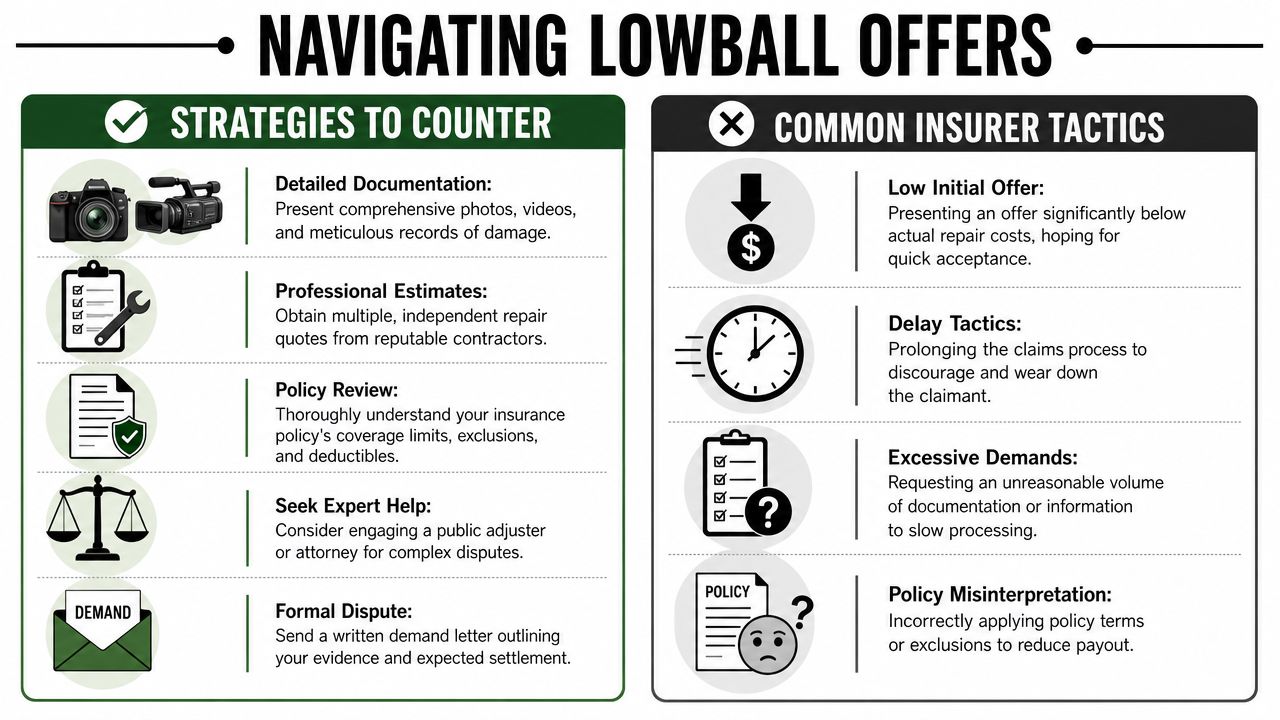

Countering Lowball Offers and Insurer Tactics

The first low offer often lands when you are tired, behind on repairs, and ready for someone to tell you the worst is over. Then the estimate arrives and leaves out half the drywall prep, prices labor like it is two years ago, or treats obvious damage like an optional add-on. I have seen that pattern many times. It does not always mean bad faith. It usually means the carrier is protecting its numbers until the policyholder proves the actual cost.

The offer is only the carrier's opening position

An insurance estimate can look polished and still be wrong. It may rely on incomplete measurements, generic pricing, or a scope written before all the damage was visible. That happens often on water losses, fire claims, and any job involving detach and reset, code items, specialty finishes, or moisture-related work.

Low offers usually come from a few recurring problems:

- Missing scope: insulation, cabinetry work, flooring transitions, overhead and profit, code upgrades, debris removal, or hidden damage

- Pricing gaps: carrier software pricing does not always match what local contractors in Oregon or Washington are charging

- ACV confusion: the first payment may reflect actual cash value, not the full replacement cost available under the policy

- Early closure pressure: some adjusters push for a quick sign-off before the full repair picture is documented

The fix is specific support. General frustration does not change a claim file.

Build a counterpackage the adjuster has to answer

The strongest response is organized, itemized, and tied to real repair work. I tell clients to answer the estimate like they are marking up a bid from a contractor. Line by line. Omission by omission.

Start here:

- Get detailed written estimates from qualified contractors. Verbal opinions do not carry much weight.

- Compare each estimate to the carrier's scope. Look for missing rooms, missing trades, and under-allowed quantities.

- Identify the exact dispute. Is it scope, unit cost, depreciation, code, or causation?

- Support each point with proof. Photos, moisture readings, measurements, invoices, and contractor notes all help.

- Send one clean written response. Make it easy for the adjuster or supervisor to follow.

A short example works better than a three-page rant: “Carrier estimate omits insulation replacement in the north wall. See contractor estimate page 4, thermal imaging photo 12, and demolition photos 18 through 24.” That kind of response creates negotiating power because it is hard to ignore and easy to escalate.

The same principle applies in other property valuation disputes. Owners who bring market support usually do better than owners who argue from frustration alone. If you want a parallel example, this guide on how to maximize your total loss payout shows why documented value beats opinion.

Common insurer tactics that weaken a claim

Some tactics are subtle. Others are obvious. Either way, the effect is the same if you are not ready for them.

A preferred contractor may be perfectly capable, but their scope and price are not automatically the standard your claim has to follow.

Watch for these pressure points:

- Recorded statements before the damage is fully known: answer truthfully, but keep to facts you know

- Preferred vendor steering: you usually have the right to choose your own contractor

- Partial payments framed as final resolution: read every letter and every release carefully

- Repeated document requests for items already sent: resend them in one indexed package and note the prior submission dates

- Scope disputes disguised as pricing disputes: if the carrier says the estimate is “priced correctly,” check whether entire tasks are missing

Policyholders frequently lose ground. They spend weeks arguing about rates, yet the underlying problem is omitted work.

If the carrier keeps narrowing the claim, ask for a revised estimate that addresses each disputed item in writing. If the file stalls or the disagreement turns into an appraisal fight, read this overview of contesting an appraisal before you invoke a process that may not fix a scope problem.

A low offer is often the point where the serious claim work begins. Stay calm, stay organized, and make the carrier respond to evidence instead of assumptions.

When to Hire a Public Adjuster in Oregon and Washington

Some claims stay manageable. Others turn into a second job you never asked for. That's when outside representation starts to make sense.

A public adjuster works for the policyholder, not the insurer. In Oregon and Washington, that role matters most when the claim is large, technical, disputed, or consuming more time and attention than you can realistically give it.

The clearest signs you need help

You should seriously consider bringing in a public adjuster when:

- The loss is complex. Fire, major water loss, structural movement, and multi-room damage usually create scope and valuation problems.

- The offer doesn't match reality. If contractor pricing and the insurer's estimate are far apart, someone needs to reconcile scope, not just argue numbers.

- The claim has been denied or partially denied. Denials need policy analysis and a disciplined response.

- You're getting overwhelmed. That's not a small thing. Claims involve paperwork, inspections, follow-up, pricing disputes, and deadlines.

The long-term impact also matters. According to Kin, homeowners insurance claims typically remain on your record for five to seven years, and filing multiple claims within that period can lead to premium increases of 20% to 30% or even policy non-renewal, as explained in this article on how long home insurance claims stay on your record. If a claim will affect your record for years, it makes sense to handle it carefully the first time.

What a good public adjuster actually does

A strong public adjuster doesn't just “argue with insurance.” They organize and present the claim properly. That includes documenting building damage, valuing personal property, reviewing policy language, preparing claim submissions, meeting adjusters, and negotiating from evidence.

In practice, they also reduce noise. Homeowners stop having to chase every email, decode every estimate, and wonder whether a missing item was accidental or strategic.

If you're evaluating whether representation is appropriate, start with a licensed professional. This resource on choosing a licensed public adjuster is a useful place to begin.

The right time to hire help is usually earlier than people think. Not because every claim needs a fight, but because complicated claims rarely become simpler after key evidence is missed.

If your property loss in Oregon or Washington has turned into delays, underpayment, or a scope dispute, NW Claims Management can step in as your advocate. The firm represents policyholders, not insurance companies, and handles residential, commercial, and nonprofit claims on a contingency basis. If you need a clear review of where your claim stands and what options you still have, request a free claim evaluation.