The call usually comes early.

A pipe bursts overnight in a Portland restaurant. A wind-driven leak soaks a nonprofit office in Vancouver. A small retail shop in Salem takes smoke damage, and the inventory is still there, but the space isn't usable the way it was yesterday. You're not just dealing with repairs. You're trying to stay open, keep staff working, serve customers, and stop a bad week from turning into a business-ending loss.

That's where extra expense coverage matters. Property coverage repairs the damage. Extra expense coverage pays for the temporary, above-normal costs that help you keep operating during the repair period. If you don't understand that difference, you'll leave money on the table. If you don't document it correctly, the insurer will often challenge it line by line.

For policyholders in Oregon and Washington, the problem isn't usually the idea of the coverage. It's the execution. Most small businesses, nonprofits, and homeowners don't have a controller, a forensic accountant, or a claims team sitting in the back office. They have receipts, texts, a debit card statement, and a lot of stress. That's still workable, but only if you build your claim the right way from day one.

When Disaster Strikes Your Business Stays Open

A water loss doesn't always shut a business down completely. Sometimes it shuts down the profitable half, the functional half, or the public-facing half. That's enough to create chaos.

Take a common Pacific Northwest scenario. A neighborhood café has a soaked kitchen floor, damaged wiring, and equipment that can't be used safely. The owner can't run the full menu, but the front counter still works. They move to coffee, bottled drinks, and packaged goods while repairs happen. They rent a temporary refrigeration unit, pay for emergency cleanup, and bring in extra labor to reorganize the layout.

Those added costs aren't part of ordinary operations. They exist because the damage happened and because the owner is trying to stay in business.

The practical purpose of Extra Expense Coverage

That's the primary function of extra expense coverage. It supports the workaround. It pays for the temporary fixes, rushed solutions, and stopgap operating costs that help you avoid a full suspension.

Property owners often focus only on demolition, rebuild cost, and replacement items. That's too narrow. The immediate question after a loss is often, “What do I need to spend right now so this place can still function at some level?”

Examples can include:

- Temporary space: Renting a short-term office, storage unit, or alternate service location.

- Emergency equipment: Bringing in portable heaters, fans, refrigeration, fencing, or security equipment.

- Short-term labor changes: Paying overtime or bringing in temporary help so normal work can continue.

- Faster logistics: Using expedited delivery or rush services to avoid longer downtime.

If your damage also involves repairs by mitigation crews or specialty trades, it helps to understand how restoration contractors structure their own insurance and operations. That's why a guide on coverage for Ohio restoration contractors can still be useful as background, even for owners here in the Northwest. It gives you a clearer picture of the vendors who often show up first after a loss.

For local recovery planning, policyholders also need to think about cleanup and rebuild timing. A commercial owner dealing with active damage should understand the restoration side of the process, not just the claim side. This overview of commercial property restoration services is a good starting point.

Extra expense coverage doesn't reward convenience. It reimburses reasonable action that helps keep operations moving after covered damage.

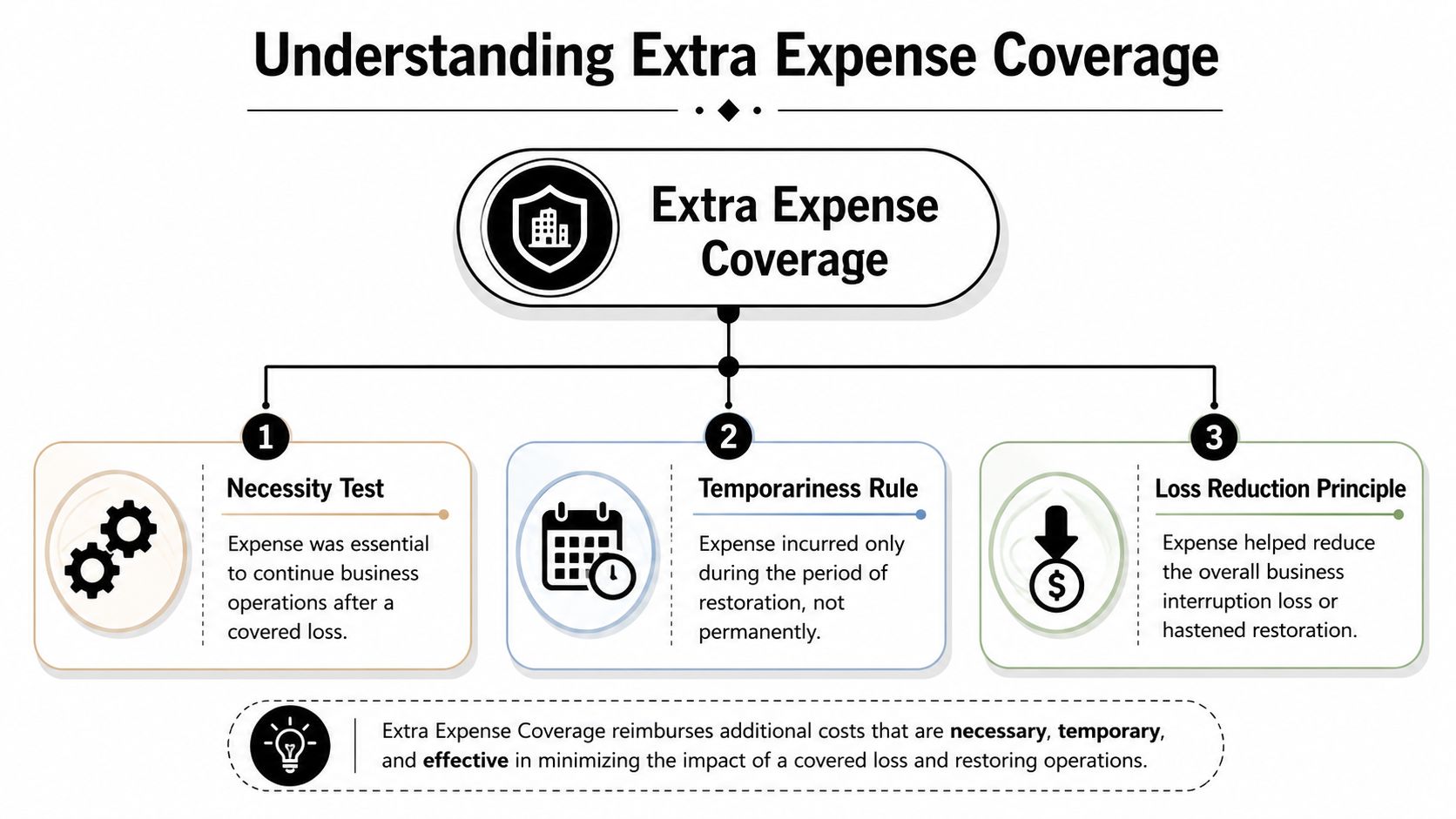

What Extra Expense Coverage Actually Is

The insurance industry likes technical wording. Policyholders need a usable rule.

Under the Insurance Services Office form, extra expense coverage means necessary expenses that wouldn't have been incurred without the loss and that exceed normal spending, as explained in IRMI's definition of extra expense coverage. Courts and insurers commonly apply a three-part test: the expense must be necessary to continue operations, incurred during the period of restoration, and absent but for the physical damage caused by a covered peril.

The three-part test you should use

When you're deciding whether to track a cost as extra expense, run it through this filter:

Was it necessary?

Not helpful. Not nice to have. Necessary to continue operations, reduce suspension, or support temporary continuity.Did it happen during the restoration period?

This coverage is temporary by design. It applies while the damaged property is being restored, not forever.Would you have spent this money anyway?

If the answer is yes, it's probably a normal operating expense. If the answer is no, and the loss forced it, it belongs in the extra expense discussion.

A simple way to separate it from other claim categories

Think of business interruption coverage as income replacement. It addresses money you would have earned.

Think of extra expense coverage as the money you had to spend to avoid losing even more.

That distinction matters because insurers review these categories differently. They will usually ask whether a cost is incremental. A normal payroll line, normal utility bill, or regular monthly software subscription usually won't become extra expense just because a loss occurred. But an added generator rental, temporary office internet setup, or emergency security patrol might.

What the restoration period means in real life

The phrase period of restoration sounds abstract, but the working idea is simple. It's the repair-and-recovery window tied to the covered physical damage. That's the time frame in which these extra costs have to arise.

Practical rule: If you can't explain the direct link between the damage, the temporary measure, and the timing, the insurer has an opening to deny the line item.

This is why sloppy bookkeeping hurts claims. If you mix normal expenses with loss-related extras, you force the insurer to do sorting work. They won't do it in your favor.

Extra Expense Versus Business Interruption Insurance

A lot of policyholders use these terms as if they mean the same thing. They don't.

Business interruption coverage and extra expense coverage are separate tools. You need both concepts straight before you can present the claim correctly. Extra expense coverage developed because standard property insurance left a gap, and by the mid-1980s it had become a regular part of business income forms, as outlined in Investopedia's history of extra expense insurance.

Extra Expense vs. Business Interruption at a Glance

| Feature | Extra Expense Coverage | Business Interruption Coverage |

|---|---|---|

| Primary purpose | Pays added costs to keep operating or reduce downtime | Replaces lost income and certain continuing expenses during shutdown or slowdown |

| What it focuses on | Temporary, above-normal spending caused by the loss | Income the business would have earned if the loss hadn't happened |

| Typical question | “What did you have to spend to stay functional?” | “What revenue or income did you lose because operations were disrupted?” |

| Common example | Renting temporary equipment or space | Claiming lost earnings while part or all of the business can't operate |

| How insurers analyze it | Necessity, timing, and whether the expense was truly extra | Financial records, trends, and ongoing operating costs |

Why the difference matters in a live claim

If you shut down completely, business interruption becomes central. If you stay partially open by spending money on temporary solutions, extra expense becomes central. Many claims involve both.

A damaged dental office is a good example. If treatment rooms are unusable, the practice may lose revenue. That leans into business interruption. If the office also rents portable equipment and shifts certain services into a temporary suite to keep seeing patients, those added costs point to extra expense coverage.

The mistake I see most often is this: policyholders track only the lost revenue and ignore the costs they spent to limit the damage to the business. That's backwards. Insurers expect mitigation. If you took reasonable steps to keep operating, those steps need to be documented and claimed.

One more distinction policyholders miss

Business interruption is often backward-looking. It asks what the business would have earned.

Extra expense is more operational. It asks what you did, what it cost, and whether it helped preserve continuity.

If your policy also includes timing extensions after the physical repair work is done, that's a separate issue and needs its own review. Policyholders dealing with that question should understand how an extended period of indemnity works, because it affects recovery after the property itself is repaired.

The cleanest claims are the ones where each cost is assigned to the right bucket before the insurer starts asking questions.

What Triggers Coverage and What Are the Limits

Extra expense coverage doesn't activate because life got harder. It activates because covered property suffered direct physical loss from a covered cause, and that loss created necessary temporary costs.

If your building had a fire, a burst pipe, storm damage, or another covered event, you may have a valid trigger. If the problem falls outside the property coverage grant, extra expense usually won't stand on its own. This is where policy language matters. A policyholder can have a real-world problem and still face a coverage fight if the underlying cause of loss isn't covered.

Why limits deserve your attention immediately

Don't treat extra expense as a side item. In large business interruption events, extra expense claims often represent 10 to 25% of total indemnity paid, and average extra expense payouts can range from $40,000 to $120,000 per claim, according to the discussion of extra expense claims and limits at Merlin Law Group.

That should change how you read your declarations page.

The limit questions to ask right away

Pull the policy and answer these:

- Is there a separate dollar limit? Some policies state extra expense as its own limit.

- Is it bundled with business income? If so, both coverages may be drawing from the same pool.

- Is there a time boundary tied to restoration? Most forms don't allow these expenses to run indefinitely.

- Are you claiming temporary measures or permanent improvements? Permanent betterments are frequent dispute points.

Costs that commonly create friction

Insurers often push back when a policyholder tries to include items that look more like upgrades than temporary continuity measures. Examples include:

- Permanent improvements: New systems or buildouts that go beyond what was needed to operate temporarily.

- Code-driven upgrades: These may require separate coverage analysis.

- Unrelated overhead: Costs you were already going to incur before the loss.

- Poorly timed expenses: Charges that show up long after the restoration window without a strong explanation.

The practical lesson is simple. Don't wait until the end of the claim to understand the cap and scope of coverage. If you spend first and read later, you may create unrecoverable costs.

How to Document Your Extra Expense Claim

Here, most smaller claims go sideways.

A lot of policyholders in Oregon and Washington don't have polished accounting systems. They've got QuickBooks that's half up to date, handwritten notes, vendor emails, Venmo records, and a stack of receipts in the truck. That's normal. It's also dangerous. Unclear documentation is a leading cause of disputed or delayed extra expense claims, especially when the proof consists of self-made spreadsheets without enough justification, as discussed in this analysis of documentation problems in extra expense claims.

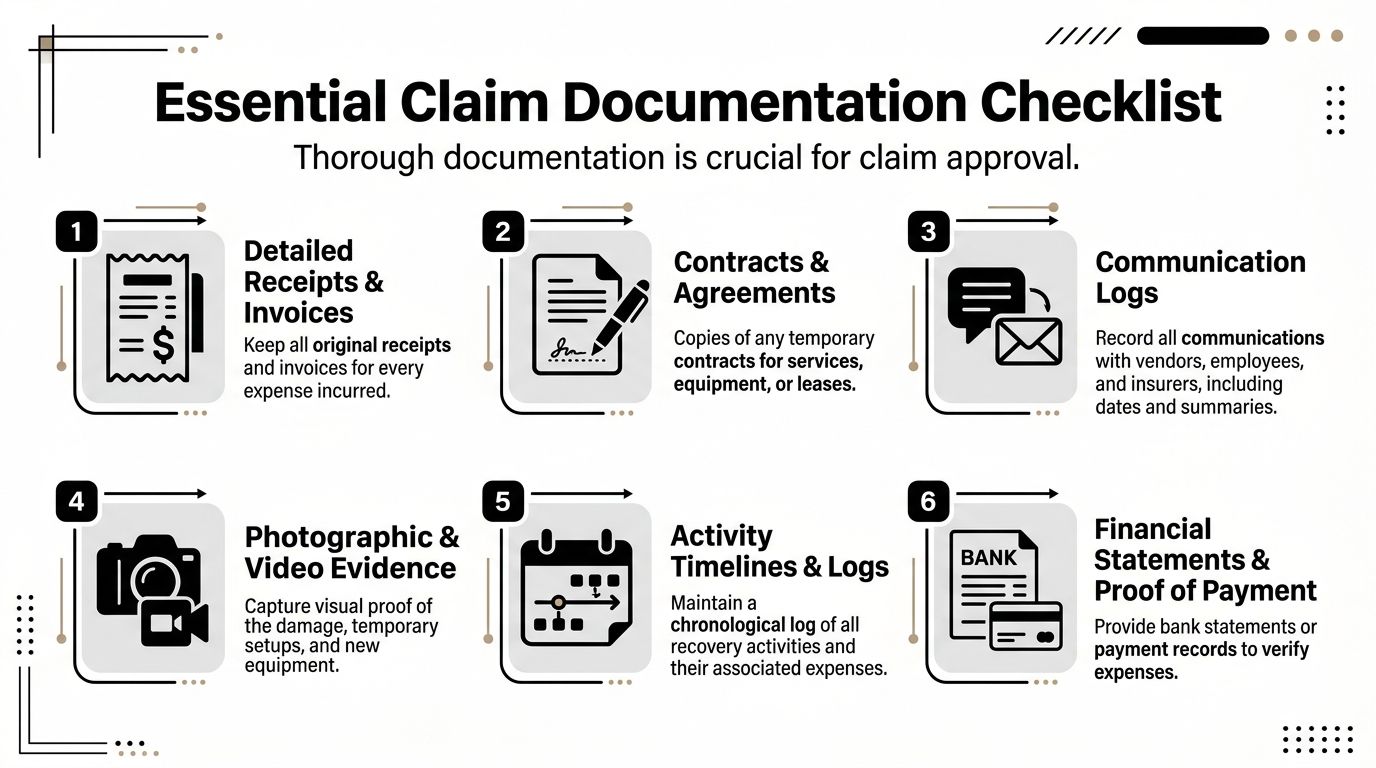

Your claim file needs five basic parts

Build one folder, digital or paper, and separate it into these sections:

Receipts and invoices

Keep every original receipt. If you paid cash, write the reason on the receipt immediately.Proof of payment

Match each charge with a bank record, card statement, canceled check, or payment confirmation.Reason for the expense

A common error occurs here. Don't just keep the invoice. Explain why the expense was necessary because of the loss.Date and timeline support

Every item should fit into the restoration timeline.Photos and communications

Save pictures, vendor emails, and texts that show the problem and the temporary response.

How to label expenses so the insurer can't play dumb

A receipt by itself doesn't prove coverage. Add a short note to every item.

Good examples:

- Generator rental: “Temporary power needed after covered fire damage interrupted normal electrical service.”

- Portable fencing: “Installed after storm damage to secure unsafe area and keep property usable.”

- Hotel stay for homeowner: “Temporary lodging required while covered interior damage made home partially unusable.”

- Extra labor hours: “Cleanup and relocation time above normal staffing caused by water loss.”

That note can be typed into a spreadsheet, written on a scanned receipt, or saved in a claim log. What matters is the connection.

“If the receipt doesn't answer why this was necessary because of the loss, the insurer will ask. Sometimes they'll ask months later.”

A simple spreadsheet that works

You do not need fancy accounting software. You need consistency.

Use columns like these:

| Date | Vendor | Amount | Normal Expense or Extra | Why It Was Needed | Proof Attached |

|---|---|---|---|---|---|

| [date] | [vendor] | [amount] | Extra | [loss-related reason] | Receipt, card statement, photo |

Then add a second tab if needed for comparison items, such as normal utility bills versus increased utility use during drying or temporary occupancy.

Documentation checklist for small businesses and nonprofits

- Create a daily log: Record what happened, who authorized a purchase, and what business function the expense supported.

- Photograph temporary setups: Show the rented equipment in use, the alternate workspace, or the temporary safety measure on site.

- Save every vendor communication: Estimates, revised invoices, and approval emails all matter.

- Track labor separately: If employees worked extra hours on cleanup, relocation, or temporary operations, isolate those hours from normal payroll.

- Keep baseline records: Prior bills, rent statements, and regular operating costs help prove what was “extra.”

Homeowners dealing with water losses can also benefit from practical guidance on filing water damage claims, especially when they're trying to track temporary housing, emergency drying, and immediate mitigation costs.

Before you submit anything, use a property-specific review tool. A solid property inspection checklist helps you connect the physical damage to the expenses you're claiming.

The rule that wins arguments

Don't hand the insurer a stack of receipts and expect them to build your case for you.

Build the argument yourself. Show the expense, the timing, the reason, and the payment proof. If you do that consistently, the claim gets harder to chip away at.

Insurer Tactics That Minimize Your Payout

Insurers don't usually deny extra expense claims with dramatic language. They trim them subtly.

They question one invoice, then another. They recast a temporary measure as a business improvement. They decide a cost was helpful but not necessary. They argue that repairs should have finished sooner, so the restoration period ended earlier than you claim. Each move cuts the number without sounding unreasonable.

The most common pressure points

Here's where carriers usually push:

“This wasn't necessary.”

They say the expense was optional, excessive, or mainly for convenience.“This is a betterment.”

They argue you upgraded the property or operation instead of using a temporary solution.“You would have spent this anyway.”

They reclassify the charge as normal overhead.“The restoration period should have ended sooner.”

This is a favorite. Shorten the time window, and a whole category of expenses disappears.

Why policyholders lose these arguments

Individuals often respond with frustration instead of evidence.

That doesn't work. Insurance claims are documentation contests wrapped in contract language. If the insurer narrows “necessary,” you need records showing why the expense preserved operations. If they call something a betterment, you need proof that it was temporary, limited, and loss-driven. If they cut off the timeline, you need a day-by-day restoration record tied to actual repair conditions.

What you should do when the pushback starts

First, stop talking in generalities. Replace “we had to do this” with records, dates, invoices, photos, and explanation.

Second, force line-item review. Don't accept a broad statement that “several charges appear excessive.” Ask which charges, on what basis, under what policy language.

Third, keep your own claim management record. A centralized insurance claim management system overview can help policyholders understand how to organize communications, status updates, and support materials so the file stays controlled.

What to say back: “Please identify each disputed line item, the factual basis for the dispute, and the policy language you contend limits or excludes that charge.”

That one sentence changes the tone of the conversation. It forces specificity.

The hard truth about extra expense negotiations

These claims look small compared to a full rebuild, so policyholders often treat them casually. That's a mistake. Carriers know many owners are too overwhelmed to fight over a rented trailer, security service, temporary internet setup, or labor overage. But those costs add up fast.

If you're not organized, the insurer has an advantage. If you are organized, the discussion gets narrower, cleaner, and much harder for them to manipulate.

Securing Your Full and Fair Recovery

Extra expense coverage is one of the most useful parts of a property claim, and one of the easiest to underclaim.

It exists for a practical reason. When covered damage disrupts your property, you may need to spend money you never planned to spend just to keep functioning. That can mean temporary space, emergency equipment, added labor, security, storage, or other short-term operating costs. If those expenses were necessary, temporary, and caused by the loss, they deserve serious attention.

The two things that matter most are simple.

First, document everything while it's happening. Not later. Not from memory. Build a file that shows what you spent, why you spent it, when you spent it, and how it connects to the physical damage.

Second, treat insurer scrutiny as predictable. Don't act surprised when they challenge necessity, timing, or whether a cost was really extra. Prepare for that review from the start.

If your claim also involves complicated accounting, blended categories of loss, or a dispute over what belongs where, it helps to understand the role of forensic accounting in insurance claims. That's often where the difference between a rough estimate and a defensible claim becomes obvious.

You don't need to be an accountant to present a strong claim. But you do need discipline. And if the carrier starts minimizing valid costs, you need someone who knows how to push back effectively.

If you're dealing with property damage in Oregon or Washington and you're not sure whether your temporary costs qualify, talk to NW Claims Management. Their team represents policyholders, not insurers, and they offer a free claim evaluation to help you understand what your policy may owe for extra expense, business interruption, and related losses.