So, you're looking for an Xactimate free trial. I get it. You've heard it’s the gold standard for estimating property damage claims, and you want to see if your insurance company's numbers add up.

Let's cut right to the chase: A true, do-it-yourself Xactimate free trial for your personal claim simply doesn't exist. Instead, what you'll find is a guided demo with a sales rep, and it's really aimed at industry professionals, not homeowners. This is a crucial distinction that saves you from a lot of wasted time and frustration.

The Truth About an Xactimate "Free Trial"

If you've searched for a free trial, you’ve probably hit a wall. There's a good reason for that. Xactimate is an incredibly powerful and complex piece of software. It’s built for daily use by professional contractors, adjusters, and restoration companies—not for a one-and-done estimate by a homeowner.

The real value of Xactimate isn't just the software itself; it's the massive, constantly updated database of local material and labor costs. This data is the "secret sauce," and giving away unrestricted access would be like a restaurant handing out its secret recipes for free.

What Verisk Offers Instead

Instead of a downloadable trial you can play with, Verisk (the company that makes Xactimate) offers a live, one-on-one demo. This is a scheduled video call where a sales expert walks you through the program and answers your questions.

Make no mistake, this is a sales call. It's designed for professionals who are seriously considering buying a subscription, which can easily run over $2,500 a year. The goal is to show potential buyers the software's immense capabilities to justify the investment, not to help a homeowner check a single estimate.

The Bottom Line: The "free trial" is actually a guided sales demo for professionals. It’s not a self-service tool for homeowners to write or double-check an estimate for their own property damage claim.

This is where homeowners often feel stuck. You know the insurance company is using this very tool to decide how much they'll pay you, yet you're locked out. This information gap gives the insurance carrier a major upper hand—it’s one of many common insurance adjuster tricks we see every day.

Knowing this is your first step toward leveling the playing field. For a single claim, the solution isn't trying to learn this complex tool overnight. It's about getting an expert who has already spent years mastering it on your side.

How to Schedule Your Free Xactimate Demo

So, you want to get your hands on Xactimate but can't find a "download trial" button. That's by design. Instead of a self-guided Xactimate free trial, what you'll get is a live, one-on-one demo with a representative from Verisk, the company behind the software.

Think of it less as a sales pitch and more as a guided tour. It's your best opportunity to see how the platform works for your specific trade.

To get the ball rolling, you’ll need to head over to the official Xactimate page on Verisk’s website. Find the "Request a Demo" button and fill out their form.

What to Put on the Demo Request Form

This form is your first impression, so it pays to be specific. They're trying to figure out who you are and what you need.

- Your Role: Don't just say "contractor." Are you a roofer, a restoration pro, or an aspiring public adjuster? The more detail, the better.

- Company Info: Be ready with your company name, size, and website. They want to see that you're a serious professional.

- Your Goal: What problem are you trying to solve? Tell them if you're aiming to write faster estimates, challenge insurance scopes, or just get more competitive with your bids.

After you submit the form, expect someone from their team to reach out within a few business days to get your demo on the calendar.

This is your shot to put the software through its paces. Don't go in cold. Prepare a list of questions and scenarios that you run into every day. A roofer might want to see how it handles a complex roof with tricky valleys and dormers. A water mitigation expert should ask how to input moisture readings and set up drying equipment.

Expert Tip: Don't be a passive observer. Ask the rep to build a mini-estimate for a job you've recently done. This forces them to move beyond a canned presentation and show you how Xactimate would actually work for your business. It transforms the demo into a valuable, personalized training session.

This guided demo approach is how most new users get their start. It's a proven method for Verisk, especially as they've grown. This strategy has been a key part of their expansion, a topic they’ve discussed at major industry events. You can watch a presentation that touches on Verisk's market growth strategy to get a feel for their perspective.

Practical Alternatives to a Full Xactimate License

If you're a homeowner dealing with a major insurance claim, paying for a full Xactimate license is usually a bad investment. Think of it like buying a full set of professional mechanic's tools just to change a flat tire—it’s expensive, complicated, and complete overkill for a one-time job.

Thankfully, you don't need to. There are much smarter ways to get the detailed estimate you need without the steep price tag and even steeper learning curve.

One option people often stumble upon is the Xactimate Training Version. It’s a great way for contractors or new adjusters to get a feel for the software, but it has a fatal flaw for your claim: you can't create a real, usable estimate with it. The reports it generates are basically watermarked samples, lacking the live, localized pricing data that carriers demand. An estimate from the training version is useless for actual negotiations.

Using Third-Party Services and Other Software

You could also look into hiring a third-party estimating service. You send them the details of your damage, and for a fee, they'll build an Xactimate report for you. This is certainly faster than trying to learn the program from scratch. The downside is that you’re still the one left to argue and negotiate the estimate with your insurance company, and the quality of that estimate is a gamble based on who you hire.

While you're researching, you might come across lists of the best estimating software for contractors. Some of these programs are quite good, but here's the reality: nearly every major insurance carrier in the U.S. uses Xactimate. Submitting your claim in a different format just gives the insurance company an easy excuse to question your numbers and slow things down.

The most powerful alternative for a policyholder isn't just about getting an estimate; it's about getting an expert who wields Xactimate as a tool for advocacy. This shifts the focus from just numbers to building an undeniable case for what you're owed.

The Ultimate Alternative: Hiring a Public Adjuster

This brings us to what is, in my experience, the most effective path for a homeowner: partnering with a licensed public adjuster.

When you hire a firm like NW Claims Management, you aren't just "accessing" Xactimate. You’re deploying a master of the software to fight on your behalf. A public adjuster uses the same tool the insurance company uses to build a meticulous, line-by-line argument that forces them to see and pay for the full scope of your loss.

There's a reason Xactimate has helped 90% of restoration professionals standardize their estimates—it's the industry language. We speak that language fluently. The key difference is that an expert public adjuster doesn't just list the obvious damage. We document the entire recovery process your policy entitles you to. We know exactly how to account for overhead and profit, local code upgrades, and dozens of other line items that are routinely "forgotten" by insurance adjusters. This is precisely how to get more from your insurance claim.

In our hands, the estimate is no longer just a document; it’s your single most powerful negotiation tool.

Why Your Insurer's Xactimate Estimate Might Be Low

It’s one of the biggest misconceptions we see. A homeowner gets an estimate from their insurance company, sees the Xactimate logo, and assumes the numbers must be right. But here’s the reality: the software is just a tool. The final estimate is only as good—and as complete—as the person who wrote it.

And who is that person? An adjuster who works for the insurance company. Their job is to manage the claim according to their employer's rules and financial targets. This often creates a conflict of interest, leading to an estimate that looks official but is missing huge chunks of what you're actually owed.

The Problem of Omissions and Scope

The most common way estimates come in low is through an incomplete scope of work. This is a classic move. The adjuster’s report will list the most obvious damage but conveniently leaves out all the related tasks required to actually restore your property to its pre-loss condition.

Think about a small kitchen fire. The adjuster’s Xactimate report might include line items for new cabinets and replacing a section of drywall. But what did they "forget"?

- The extensive smoke and soot cleaning needed in the dining room and living area.

- Mandatory electrical and plumbing upgrades that are triggered by the repair work, as required by local codes.

- The general contractor’s overhead and profit—a standard, legitimate industry cost for managing the project.

These aren't just little details; they represent thousands, sometimes tens of thousands, of dollars. Every single omission helps the insurance carrier’s bottom line, not yours. While you can read through Xactimate reviews that praise its granular detail, that very detail is what allows a biased user to pick and choose what to include.

A lowball estimate isn't always malicious. Often, it's a product of an overloaded adjuster trying to close files quickly. They write a bare-bones report to get it off their desk, leaving you with the nightmare of fighting for every single thing they missed.

The Public Adjuster's Approach

We use the exact same Xactimate software, but our goal is the complete opposite. Our mission is to build a comprehensive proof of loss that documents every single detail of your damage and everything you are owed under your policy.

We approach the estimate from your perspective. We start by asking, "What will it truly take to make this homeowner whole again?" This means accounting for everything from the initial demolition and debris haul-away to the final coat of paint and the necessary project supervision. It's this meticulous, detail-obsessed approach that ensures your settlement is enough to cover the entire repair, so you’re not left paying out-of-pocket. Knowing what your insurance policy limits is crucial, as this defines the total bucket of funds we have to work with.

When to Stop Searching and Hire a Public Adjuster

Let's be honest. For most homeowners, the hunt for an Xactimate free trial starts from a place of deep frustration. You're staring at your insurance company's estimate, and you have that sinking feeling in your gut that the numbers just don't add up.

This is the exact point where trying to DIY a solution can do more harm than good. Recognizing when to shift gears from "I can figure this out" to "I need an expert" is the single most important decision you can make for your claim's outcome.

If your claim involves major structural damage, a serious fire, or extensive water intrusion, you're already in over your head. The same goes if you're getting the runaround from your carrier—constant delays, confusing information requests, or a flat-out denial. These aren't just inconvenient hiccups; they're often deliberate tactics meant to exhaust you into accepting less.

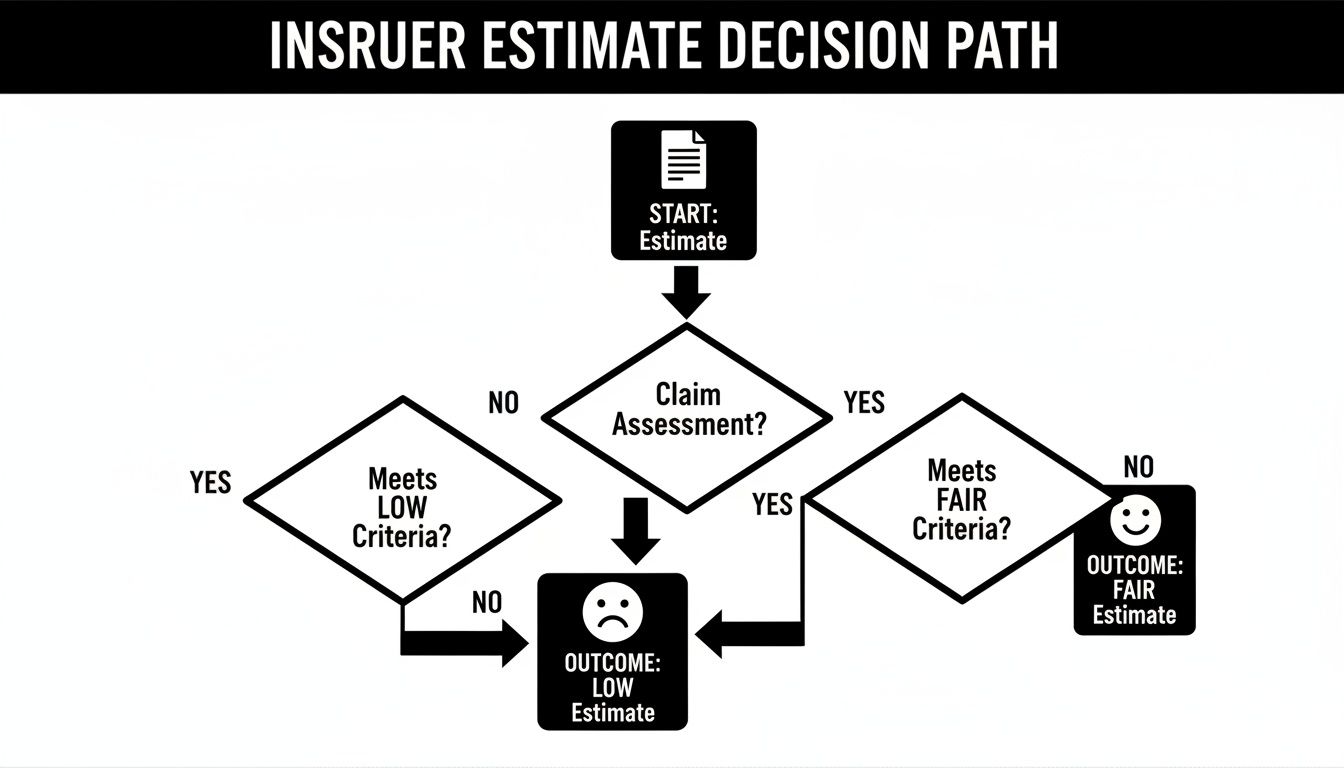

This flowchart shows the critical decision point you’re facing right now.

As you can see, a lowball estimate isn’t a signal to start a new software project. It's a clear signal that you need to change your entire strategy.

Leveling the Playing Field

Hiring a public adjuster isn’t giving up; it’s finally arming yourself with the right weapon for the fight. Think of it as bringing in a specialist who speaks the insurance company's language fluently.

We use the exact same software, but with one massive difference: our only goal is to document every single detail of your loss to get you what you're rightfully owed.

For a complex claim, the fight isn't about finding a magic software trial. It’s about deploying an expert who has already spent thousands of hours using that software to force carriers to pay what’s fair.

We take that burden completely off your shoulders. Our team builds a comprehensive, line-by-line valuation that leaves no room for the insurance company to argue. Instead of you battling over their lowball numbers, we hand them an undeniable case built on hard data, industry standards, and a deep understanding of your policy.

If you're wondering whether your situation warrants this kind of help, our guide on when to hire a public adjuster breaks down the specific scenarios where an expert is essential.

Frequently Asked Questions About Xactimate

When you're dealing with a property damage claim, you’ll hear the word "Xactimate" a lot. It’s the software your insurance company uses, so it's smart to understand what you're up against. Here are the straight answers to the questions we get asked all the time.

How Much Does a Full Xactimate Subscription Cost?

For a single user, a professional Xactimate license runs well over $2,500 per year. It’s a serious investment, which is why it’s a tool for full-time professionals like us, not homeowners who just need to file one claim. The steep price tag alone makes it completely impractical for a single-use situation.

Can I Use the Xactimate Training Version for My Claim?

Absolutely not. We see people ask this, and the answer is a hard no. The training version of the software is purely for learning the ropes and doesn't contain the live, localized pricing data that forms the backbone of a real estimate.

An estimate created with the training software is essentially a fake document. Any insurance carrier would reject it on the spot because it’s missing the real-world cost data needed to even begin a settlement negotiation.

My Contractor Uses Xactimate. Is That Good Enough?

It’s a great sign that your contractor is using professional-grade tools, but their job is fundamentally different from a public adjuster’s. A contractor’s estimate is all about their cost to perform their specific work, whether that's roofing, siding, or plumbing. It's an important piece of the puzzle, but it's not the whole picture.

A public adjuster’s Xactimate estimate, on the other hand, is a comprehensive claim document built to get you paid for everything you are owed under your policy. We’re looking far beyond a single trade's scope.

Our estimates often include items a contractor might miss, such as:

- Costs for other trades required to finish the job correctly.

- Additional living expenses if you're forced out of your home.

- The value of your damaged personal property and contents.

- Crucial code-required upgrades that your policy covers.

A public adjuster advocates for your entire claim, which almost always goes far beyond the contractor's initial bid. This becomes especially critical if the carrier starts pushing back, and you need to know how to fight an insurance claim denial.

At NW Claims Management, we live and breathe Xactimate. We use our mastery of the software to build an ironclad case for your financial recovery. If your insurer's estimate feels wrong, contact us for a free claim evaluation at https://nwclaimsmanagement.com.