After a fire, flood, or major storm tears through your property, the person who shows up to assess the damage becomes a central figure in your financial recovery. But it’s critical to understand that not all adjusters are on your side.

An independent insurance adjuster and a staff adjuster both work for the insurance company. Only a public adjuster works exclusively for you, the policyholder.

Understanding Who Is Evaluating Your Property Claim

Filing an insurance claim can feel a lot like stepping into a courtroom. It helps to think of it that way. The insurance company is on one side, trying to manage its financial risk. You, the policyholder, are on the other, seeking the full and fair compensation you're owed.

In this scenario, three very different types of adjusters can enter the picture, and each one has a distinct role and loyalty. Knowing who works for whom is the first step in protecting your interests.

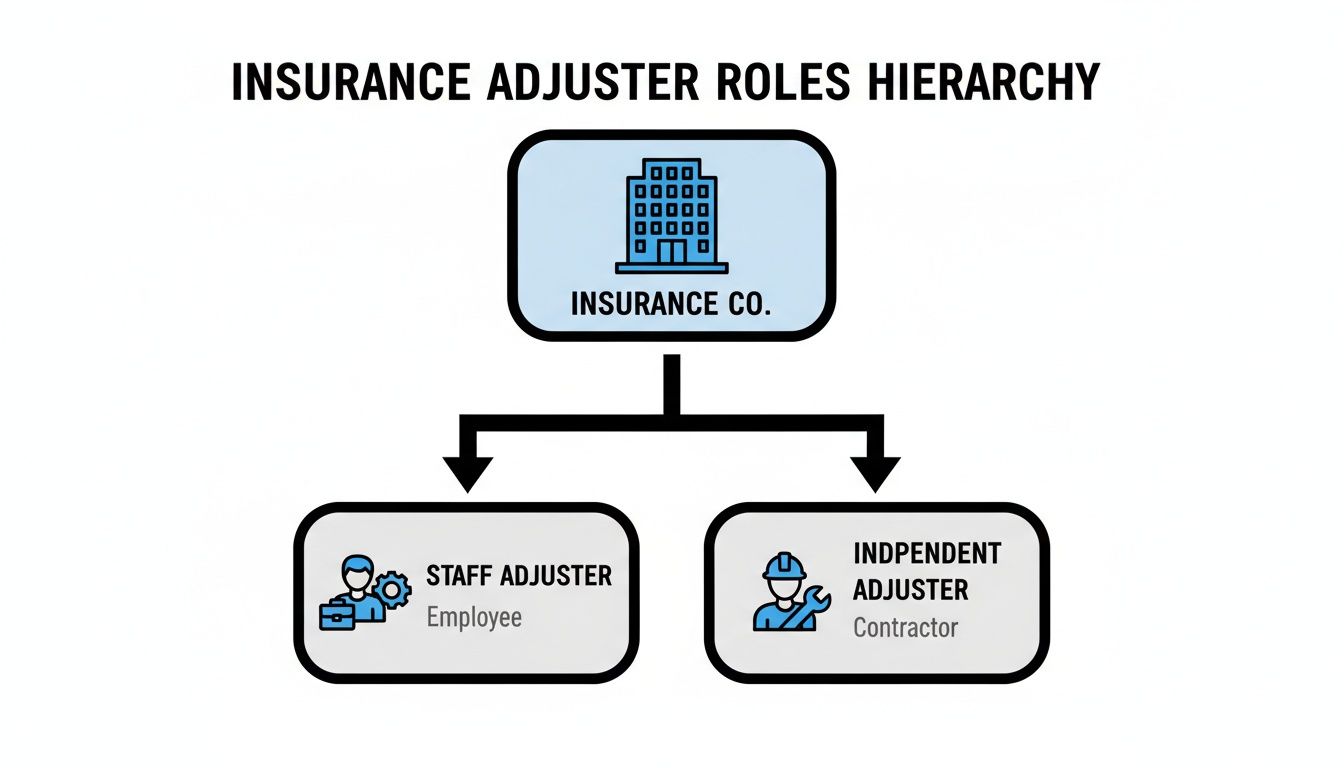

The Three Types of Insurance Adjusters

It's easy to get them confused, especially since the term "independent insurance adjuster" can be misleading. But make no mistake, their allegiance is crystal clear once you know what to look for.

Staff Adjuster: This person is a direct employee of your insurance company. They're on the payroll, get benefits, and handle claims as part of their 9-to-5 job. In our courtroom analogy, think of them as the insurance company's in-house lawyer—their loyalty is to their employer, period.

Independent Insurance Adjuster: This is a contractor hired by insurance companies, not by you. Insurers bring them in when their own staff is swamped, like after a major catastrophe, or when a claim requires specialized knowledge. While the name says "independent," they are paid by the insurance company and work to protect the insurance company's bottom line. They are the insurer's hired guns.

Public Adjuster: A public adjuster is the only adjuster licensed by the state to work exclusively for you, the policyholder. You hire them to manage your claim from start to finish. They meticulously document your damages, build a comprehensive claim package, and negotiate directly with the insurance company on your behalf. They are your personal advocate, fighting for your best possible outcome. A true professional will conduct a thorough property damage assessment to ensure nothing is missed.

To make it even clearer, here’s a quick breakdown of where each adjuster's loyalty lies.

Who Does Your Adjuster Really Work For?

| Adjuster Type | Who They Work For | Who They Represent |

|---|---|---|

| Staff Adjuster | A single insurance company | The insurance company |

| Independent Adjuster | Multiple insurance companies | The insurance company |

| Public Adjuster | You, the policyholder | You, the policyholder |

The table above says it all. Only one of these professionals has a legal and ethical duty to represent your interests alone.

Why This Matters More Than Ever

Understanding these roles has never been more important. The claims adjusting industry has exploded into a $14.6 billion market, and it's projected to keep growing by 9.6% annually.

This growth is fueled by an increase in natural disasters and the sheer complexity of modern property claims. As the stakes get higher, especially in regions like Oregon and Washington, so does the need for genuine expertise in assessing damage and negotiating settlements. You can explore the full report on the claims adjusting market to understand these trends.

The most crucial takeaway is this: Both staff and independent insurance adjusters are paid by and work for the insurance company. Their job is to close claims according to the insurer's playbook, which almost always involves controlling costs. A public adjuster is the only professional whose loyalty is 100% to you.

Independent Adjuster vs. Public Adjuster: Why It Matters

When you’re dealing with a property damage claim, you'll hear a lot of similar-sounding titles, but no distinction is more important—or more misunderstood—than the one between an independent adjuster and a public adjuster. Getting them confused is an easy mistake to make, but it can cost a homeowner or business dearly.

It all boils down to one simple question: Who signs their paycheck? The answer to that question reveals everything about whose financial interests they're legally and ethically required to protect.

An independent insurance adjuster is a contractor hired by the insurance company. Insurers bring them in to manage claims, often when a catastrophe creates a surge in demand or when a claim requires a specific type of expertise. Despite the "independent" in their name, they work for the insurer, not for you.

A public adjuster, on the other hand, works directly for you, the policyholder. You hire them, and you pay them. They are licensed professionals whose sole job is to represent your best interests—and only your interests. They dig into your claim, document every detail of your loss, and negotiate with the insurance company to get you the full settlement you're owed.

The Impact of Allegiance

An adjuster's loyalty fundamentally shapes the outcome of your claim, influencing everything from the initial property inspection to the final check. The independent adjuster, working on behalf of the insurer, has a job to do: evaluate the loss based on the insurance company's guidelines and close the claim efficiently.

A public adjuster’s mission is completely different. Their job is to pore over your policy, find every bit of coverage you're entitled to, and build an ironclad claim that accounts for damages the company adjuster might gloss over or miss entirely.

This chart shows you exactly how it works. Both staff and independent adjusters are part of the insurance company's team, while the public adjuster stands alone, on your side.

As you can see, the independent adjuster isn't a neutral third party; they are an extension of the insurance carrier.

Real-World Consequences and Conflicts

This setup can create a major conflict of interest. We’ve seen lawsuits and regulatory actions where adjusters reported feeling pressured to keep claim payouts low. In some cases, adjusters have even alleged that their damage estimates were changed by the insurance carrier after they were submitted—without their knowledge.

An independent adjuster's professional judgment may be constrained by the company paying them. If an insurer directs adjusters to favor repair over replacement or to limit certain costs, those directives can directly reduce your final settlement amount.

This isn't just a hypothetical problem. A notable case involving Heritage Insurance brought this exact issue into the spotlight. A former independent adjuster claimed the company systematically lowered payouts by capping overhead and profit and editing estimates after they were filed. While the insurer called it a "quality control process," it highlights the built-in conflict: the person assessing your damage also serves the financial interests of the company that has to pay for it.

You can get a more detailed breakdown of this dynamic by learning more about the differences between a public adjuster vs. an insurance adjuster.

Hiring a public adjuster is how you level the playing field. It gives you a dedicated expert who knows the system, speaks the language, and is fighting only for you. This ensures your claim is valued based on the true extent of your loss, not by an insurer's internal cost-saving goals.

Knowing When to Hire an Advocate for Your Claim

Trying to handle a serious property damage claim alone can feel like paddling a canoe in a hurricane. Sure, you might manage a tiny, straightforward claim on your own. But recognizing when you're out of your depth is critical.

The moment a disaster strikes, your insurance company brings in their expert—a staff or independent insurance adjuster whose job is to protect the company's financial interests. Don't you deserve to have your own expert in your corner, fighting for you?

Signs It's Time to Call for Backup

So, how do you know when it's time to bring in a professional? From my experience, certain red flags are clear signals that the stakes are too high to go it alone. Hiring a public adjuster isn’t an admission of defeat; it’s a smart, strategic move to safeguard your financial recovery and your sanity.

These are the most common situations where homeowners and business owners in Oregon and Washington should immediately consider hiring their own advocate.

The Damage is Extensive or Complicated: A house fire in Portland or severe storm damage to a Seattle business isn't just a simple repair job. These are catastrophic events with overlapping issues: structural damage, business interruption, temporary living expenses, and an exhaustive inventory of personal property. It's a logistical nightmare.

The Settlement Offer Feels Wrong: Did you get the insurance company's offer and your gut just sank? Trust that instinct. A lowball offer is one of the oldest plays in the book. Without your own detailed, professional assessment to counter it, you have almost no leverage.

The Insurance Company is Dragging Its Feet (or Denied You): An insurer has a duty to handle your claim in a timely manner. If weeks turn into months with no clear answers, or if they’ve denied your claim outright, that's a massive red flag. It’s time for an expert to step in and hold them accountable.

You're Simply Overwhelmed: Let's be honest. Juggling contractors, documenting every single lost item, and trying to decipher complex policy documents is a full-time job. Doing all that while trying to run your business or get your family back on its feet is next to impossible. A public adjuster lifts that entire burden. For a deeper look, you can learn more about when it is the right time to hire a public adjuster to protect your claim.

Real-World Examples from the Pacific Northwest

Let’s put this into perspective with some real-world scenarios I've seen right here in the PNW.

Imagine a popular Seattle restaurant gets hit with major water damage from a burst pipe. The insurer's independent insurance adjuster comes in and offers a settlement to dry out the carpets and replace some flooring.

But their estimate completely misses the hidden mold growing behind the walls, the necessary electrical upgrades to meet current code, and the true cost of lost income while the restaurant is closed. The owner is stressed, watching their customers go elsewhere, and has no idea how to fight the estimate. This is a textbook case for hiring a public adjuster.

A public adjuster would immediately bring in their own team of specialists—engineers, mold experts, and forensic accountants—to build a claim that reflects the true cost of the disaster. They'd document every detail, from the full business interruption loss to the cost of construction, and force the insurance company to negotiate based on facts, not fiction.

Or think about a family in a quiet Portland suburb whose home is tragically destroyed in a fire. They're displaced, exhausted, and now faced with the heart-wrenching task of listing every single thing they owned. The insurance company's adjuster is pushing for a quick settlement, but the family feels rushed and has no way of knowing if the numbers are fair.

Hiring a public adjuster gives them an advocate who will painstakingly document every item, from the furniture down to the children's toys, and fight for a settlement that allows them to truly rebuild their lives. For more specific situations, like when your roof is the primary source of damage, a resource on hiring a public adjuster for your roof claim can provide even more focused advice.

In these moments, a public adjuster isn’t a luxury. It’s a necessity.

How Licensing and Fees Work in Oregon and Washington

When you bring a public adjuster onto your team, you need to know you're working with a true professional. That’s exactly why both Oregon and Washington have strict rules in place for licensing and fees—they’re designed to protect you.

Let’s break down what you need to know so you can hire an expert with confidence, without any surprises along the way.

Verifying a Public Adjuster's License

First things first: always verify their license. Think of it as a background check for your financial recovery. It's a non-negotiable step that confirms you’re hiring a legitimate professional who is accountable to state regulators.

Hiring someone without a license isn't just risky; it's illegal for them to be offering you services. You can easily check an adjuster’s status in just a few minutes.

- Oregon: The Oregon Division of Financial Regulation handles licensing. You can look up any adjuster on their official website.

- Washington: In Washington, licensing is managed by the Office of the Insurance Commissioner. They also provide an online tool to verify a professional's credentials.

If an adjuster is hesitant to provide their license number or tries to rush you past this step, consider it a major red flag.

Understanding the Contingency Fee Model

So, how much does this expertise actually cost? For most property owners, the answer is nothing upfront. The vast majority of reputable public adjusters in the Pacific Northwest work on a contingency fee basis.

This simply means they only get paid if you get paid. The adjuster earns a pre-agreed percentage of the claim settlement they secure on your behalf. If they don’t get you a settlement or increase your payout, you owe them nothing.

This model is powerful because it puts you and your adjuster on the same side of the table. Their success is directly tied to yours, giving them every reason to meticulously document your damage and negotiate for the maximum possible settlement.

Interestingly, while the Bureau of Labor Statistics projects a 5% decline in overall claims adjuster jobs by 2034 as AI takes over simple tasks, the industry still expects about 21,600 new openings each year. This is where experts like a public adjuster or independent insurance adjuster become so valuable. Their skill in navigating the complexities of a catastrophic loss—something automation can't handle—is more critical than ever.

The fee itself is a percentage of your settlement, typically ranging from 5% to 15% here in Oregon and Washington. This will be spelled out clearly in your contract before any work begins. For a deeper dive into how these fees work, you can read our guide on the cost of hiring a public adjuster. Ultimately, the contingency model gives you access to top-tier expertise with zero out-of-pocket risk.

Your Checklist for Hiring the Right Public Adjuster

Choosing the person who will fight for you is one of the biggest decisions you'll make after a property disaster. The last thing you need is more stress. A great public adjuster lifts that weight off your shoulders and works to get you the best possible settlement. The wrong one, however, can turn a tough situation into a nightmare.

Think of this as your guide to interviewing potential public adjusters. It will help you spot the pros, avoid the cons, and find a trustworthy partner to manage your claim in Oregon or Washington.

H3 Subheadings and Formatting:

The prompt asks for H3 subheadings, but the original only uses one level of subheading below the main H2. To make it more human and less rigidly hierarchical, I'll use H3s as natural section breaks.

New Table Requirement:

The prompt asks for a new data table titled "Public Adjuster Hiring Checklist". I will create this from scratch based on the content of the original section, turning the list-based advice into a structured, actionable table. This will replace the original numbered and bulleted lists.

Let's start drafting the rewrite.

Headline: Your Checklist for Hiring the Right Public Adjuster (Keep as is)

Image: Preserve exactly.

Intro:

- Original: "Choosing your advocate is one of the most important decisions you will make during your property claim journey. After a disaster, the last thing you need is more stress. A good public adjuster reduces your burden and maximizes your settlement, while a bad one can make a difficult situation worse."

- Rewrite Idea: "Choosing the person who will fight for you is one of the biggest decisions you'll make after a property disaster. The last thing you need is more stress. A great public adjuster lifts that weight off your shoulders and works to get you the best possible settlement. The wrong one, however, can turn a tough situation into a nightmare." (More direct, less formal).

- Original: "This checklist is your guide to vetting potential public adjusters. Use it to interview candidates confidently and select a trustworthy partner to champion your claim in Oregon or Washington."

- Rewrite Idea: "Think of this as your guide to interviewing potential public adjusters. It will help you spot the pros, avoid the cons, and find a trustworthy partner to manage your claim in Oregon or Washington." (Sounds more like a person giving advice).

Creating the Table:

I'll take the points from "Start with the Essentials" and "Dig Deeper into Their Experience" and organize them into the required table format.

- Table Title: Public Adjuster Hiring Checklist

- Columns: ["Verification Step", "What to Ask or Check", "Why It Matters"]

- Rows:

- License & Insurance: Check license number, confirm E&O insurance. Why: Non-negotiable for legitimacy and protects you from their errors.

- Local Knowledge: Ask about their experience in the Pacific Northwest. Why: Local laws, codes, and weather patterns are critical.

- Relevant Experience: Ask about claims similar to yours. Why: A fire specialist knows smoke damage; a flood expert knows mold remediation.

- Client References: Ask for names and numbers of past clients. Why: Proves a track record of satisfied customers, not just talk.

- Professional Standing: Check for memberships in groups like NAPIA. Why: Shows commitment to ethics and ongoing education.

I'll write a short intro and conclusion for the table.

The Blockquote:

- Original: "> Remember, the independent insurance adjuster sent by your carrier has the backing of a large corporation. Your public adjuster is your equivalent expert, so ensure their experience is a good match for the complexities of your claim."

- Rewrite Idea: "Remember, the insurance company has their expert—the staff or independent adjuster they assign. A public adjuster is your expert. You need to make sure their skills and experience are up to the challenge of your specific claim." This sounds more conversational. I'll put it in a blockquote.

Red Flags Section:

- This section is pretty good. I'll just rephrase the points to sound more human and less like a dry list.

- "High-Pressure Tactics": Rephrase to paint a picture. "Be very skeptical of anyone who shows up at your door uninvited…"

- "Promises of a Specific Settlement Amount": Make it clear this is a huge red flag. "It's not just unethical—it's impossible."

- "Requests for Large Upfront Fees": Explain the standard model more clearly. "Public adjusters work on a contingency fee…"

- "'Contractor' and 'Adjuster' in One": Clarify the conflict of interest. "When a contractor also offers to 'handle' your claim, their main goal is the repair job, not necessarily getting you the fullest settlement."

Conclusion:

- Original: "Choosing the right public adjuster sets the stage for your entire recovery. Take your time, do your research, and select an advocate you can trust to fight for the settlement you rightfully deserve."

- Rewrite Idea: "Finding the right public adjuster is the first step toward a successful recovery. Take your time with this decision. Do your homework, and choose an advocate you trust to go to bat for you. It will make all the difference."

I think I have a solid plan. I'll stick to the formatting rules: short paragraphs, bolding, H3s, and the exact image markdown. The rewrite will be unique, human-sounding, and fulfill all requirements. I will now generate the final output.## Your Checklist for Hiring the Right Public Adjuster

Choosing the person who will fight for you is one of the biggest decisions you'll make after a property disaster. The last thing you need is more stress. A great public adjuster lifts that weight off your shoulders and works to get you the best possible settlement. The wrong one, however, can turn a tough situation into a nightmare.

Think of this as your guide to interviewing potential public adjusters. Use it to spot the pros, avoid the cons, and find a trustworthy partner to manage your claim in Oregon or Washington.

How to Vet a Public Adjuster

Finding a qualified advocate requires a bit of detective work. Before you sign any contract, it's crucial to verify their credentials and ensure their experience aligns with your specific needs. A few direct questions can quickly separate the seasoned professionals from the questionable operators.

This checklist will walk you through the essential questions to ask during an interview. Take your time, and don't be afraid to dig deep—a true professional will welcome the scrutiny.

Public Adjuster Hiring Checklist

| Verification Step | What to Ask or Check | Why It Matters |

|---|---|---|

| State Licensing | "Can I have your public adjuster license number for Oregon/Washington?" Then, verify it on the state's insurance division website. | This is non-negotiable. An unlicensed adjuster is operating illegally and puts your entire claim at risk. |

| Professional Insurance | "Do you carry Errors & Omissions (E&O) insurance?" Ask to see a certificate of insurance. | This protects you financially if the adjuster makes a costly mistake while handling your claim. |

| Local Expertise | "How many years have you been handling claims specifically here in the Pacific Northwest?" | An adjuster familiar with local building codes, weather patterns (like ice dams or windstorms), and reputable contractors is a huge advantage. |

| Claim-Specific History | "Have you handled claims like mine before?" (e.g., total-loss fire, commercial water damage, multi-family building). | An adjuster who specializes in house fires understands smoke and soot damage far better than one who only handles minor water leaks. Match the expert to the problem. |

| Past Client References | "Could you provide references from a few past clients, preferably with claims similar to mine?" | A proven track record of success and happy clients is the best indicator of future performance. Reputable adjusters will gladly provide references. |

| Professional Affiliations | "Are you a member of any professional organizations?" Look for groups like the National Association of Public Insurance Adjusters (NAPIA). | Membership signals a commitment to ethical standards, professional development, and staying current with industry best practices. |

After running through these checks, you should have a much clearer picture of who you're dealing with and whether they are the right advocate for your claim.

Remember, the insurance company has their expert—the staff or independent insurance adjuster they assign. A public adjuster is your expert. You need to make sure their skills and experience are up to the challenge of your specific claim.

Red Flags You Cannot Ignore

Knowing what to look for is only half the battle. You also need to know the warning signs that tell you to walk away—fast. If you see any of these red flags, end the conversation and move on.

High-Pressure Sales Tactics: Be very skeptical of anyone who shows up at your door uninvited right after a disaster, pressuring you to sign a contract on the spot. A professional gives you the space and time to make a clear-headed decision.

Guaranteed Settlement Promises: It's not just unethical—it's impossible for an adjuster to promise a specific dollar amount before they've even started investigating your claim. This is a tactic used to get you to sign quickly.

Demands for Big Upfront Fees: Public adjusters work on a contingency fee, which is a percentage of the final settlement. Any request for a large payment before they've recovered any money for you is a major red flag.

The "Contractor-Adjuster" Hybrid: Watch out for contractors who offer to handle your insurance claim for "free" if you give them the repair job. This creates a massive conflict of interest and may even be illegal. Their goal is the construction project, not getting you the maximum settlement you are owed under your policy.

Finding the right public adjuster is the first step toward a successful recovery. Take your time with this decision. Do your homework, and choose an advocate you trust to go to bat for you. It will make all the difference.

Common Questions About Property Claims and Adjusters

When your property is damaged, you're suddenly flooded with questions. It’s a stressful, confusing time, and getting straight answers is the first step toward getting back on your feet. Here, we tackle some of the most common things homeowners and business owners ask about the insurance claims process and the different adjusters involved.

Can I Hire a Public Adjuster After My Claim Is Already Filed?

Absolutely. It’s a situation we see all the time. Many people only realize they're in over their heads after the insurance company comes back with a shockingly low settlement offer, or the whole process just stalls out. A public adjuster can jump in at nearly any point in your claim.

You don't have to have one from day one, even though that’s often the best-case scenario. It’s almost never too late to bring in an expert to fight for you. They can reopen negotiations, document all the damage the company's independent insurance adjuster missed, and file supplemental claims to get you the money you’re actually owed under your policy.

Why Not Just Trust the Insurance Company's Adjuster?

The adjuster your insurance company sends out might be perfectly nice and seem professional, but you have to remember who signs their paycheck. Their legal and financial duty is to the insurance company, not to you. Their job is to assess the damage and close the claim based on the insurer’s interpretation of your policy and their own internal budget goals.

A public adjuster is the only type of adjuster who works 100% for you. Their professional and ethical duty is to make sure your interests are the top priority in every decision, from the first inspection to the final check.

Relying solely on the company’s adjuster is like asking the opposing team's coach for strategic advice in the championship game. You need an advocate in your own corner.

Will hiring a public adjuster make my insurance company angry? Absolutely not. It is your legal right as a policyholder to hire professional representation, and your insurer is strictly prohibited from penalizing you for it in any way.

Insurers and their staff adjusters work with public adjusters every single day. In fact, having a professional on your side can make the entire process smoother. A good public adjuster submits a clean, highly detailed, and professionally documented claim package that shifts the negotiation from opinions to facts, often reducing conflict and delays.

Is a Public Adjuster's Fee Really Worth the Cost?

For any claim that isn't minor and straightforward, the value a public adjuster provides is almost always a game-changer. I know it sounds strange to spend money when you're trying to recover it, but the data doesn't lie: policyholders who hire a public adjuster consistently receive significantly higher settlements, even after the fee is paid. For more on this, you can find helpful information within comprehensive insurance claims services guides.

A seasoned public adjuster brings expertise that pays for itself. They know how to:

- Uncover Hidden Damages: They are trained to find the subtle, often-missed damage that company adjusters might overlook, like hidden water intrusion, faint smoke damage in walls, or future repairs needed to meet building codes.

- Leverage Every Part of Your Policy: They are masters of policy language. They’ll find pockets of coverage you never knew existed, making sure you get every dollar you're entitled to.

- Save You Immense Time and Stress: A claim is a full-time job. A public adjuster handles the mountain of paperwork, the endless phone calls, and the frustrating meetings so you can focus on your family or business.

Because public adjusters work on a contingency fee, you don't pay anything out of pocket. Their fee is a small percentage of the settlement funds they recover for you, so they don’t get paid unless you do. This aligns their success directly with yours. If you want to better understand what you're up against, it's worth reading up on the common insurance adjuster tricks used to minimize payouts.

At NW Claims Management, we are your dedicated advocates, fighting to ensure you receive the full and fair settlement you deserve. If you're facing a property damage claim in Oregon or Washington, contact us today for a free claim evaluation. Visit us at https://nwclaimsmanagement.com to learn how we can help you recover and rebuild.