After a disaster damages your home or business, one of the first calls you'll get is from someone at the insurance company. They'll introduce themselves as your telephonic case manager (TCM), and they've been assigned to get your claim started.

So, what does that really mean for you? In short, this person is the insurance company's remote coordinator, tasked with managing your entire claim from behind a desk, often hundreds of miles away. Their primary goal is to process your file efficiently and keep the insurer's costs in check.

Understanding the Role of a Telephonic Case Manager

Think of the TCM as the insurance company's internal point person for your claim. They're the voice on the other end of the line who orchestrates the first steps of the process. But while the title "case manager" might sound supportive, it's critical to understand where their loyalty lies.

A TCM's job is to move your claim through the company's established system as quickly and inexpensively as possible. They work for the insurer, not for you.

What a TCM Typically Does

From their call center or home office, a TCM kicks off the most crucial, and often chaotic, phase of your claim. Here’s what that usually looks like:

- Initial Fact-Finding: They’ll call you within a day or two of the loss to get the basic story of what happened.

- Requesting Documentation: You'll be asked to start sending them photos, videos, and any initial receipts you might have.

- Guiding Virtual Inspections: Many will ask you to walk them through the damage on a video call, using your own smartphone as their eyes.

- Assigning Vendors: They will often dispatch the insurance company's "preferred" contractors or restoration companies to your property.

This remote approach has become the default for most carriers because it saves them a fortune. A single TCM can juggle a huge caseload across a wide territory without ever needing to spend money on travel or site visits. It's a model built for volume and efficiency.

Key Takeaway: The telephonic case management system is designed for the insurance company’s benefit, not necessarily for your full and fair recovery. The TCM manages a file; you are still left with the immense burden of proving every detail of your loss.

The problem is, this convenience for the insurer creates a massive gap for you, the property owner. A manager on the phone can't smell the smoke baked into your walls, see the subtle warp of a floor from hidden water, or feel that a foundation is no longer sound. Their entire assessment is based on the limited information you can provide through a screen.

This is exactly where claims get underpaid. To protect yourself, it's essential to understand the complete property damage claim process and recognize that the person on the other end of the phone simply doesn't have the full picture.

How Insurers Use This Remote Claims Process

So, what does this remote claims process actually look like from the insurance company's side? Let's walk through a real-world example: a house fire. You’ve just been through a traumatic event, and within 24 hours, your phone rings. On the other line is a telephonic case manager, or TCM, who might be hundreds or even thousands of miles away.

Their job isn't to console you; it's to get the claim file moving—fast. This person has never seen your home and never will. They are working from a script, a playbook designed to manage the claim from a distance, with speed and cost control as the top priorities.

The Remote Claims Playbook

Think of the TCM as a remote project manager. Their first moves are always about coordinating the initial, predictable steps of the claim.

Right away, they will:

- Dispatch Initial Vendors: Expect a call from a "preferred" restoration company that the insurer works with regularly. They'll be sent out to board up broken windows or start drying out the water from the firefighters' hoses.

- Ask You to Be Their Eyes and Ears: The TCM will immediately ask you to send photos and videos of everything. You essentially become their field agent, documenting the damage for them.

- Start the Paperwork Chase: They’ll need a copy of the fire department's report and will push you to start the overwhelming task of creating an inventory of your lost personal belongings.

Every photo you send and every conversation you have is logged in your claim file. The entire goal is to gather just enough information to put a preliminary number on your loss and push the claim toward settlement. Because this all happens over the phone, it's absolutely vital you learn how to take better phone call notes so no verbal promises or details get "forgotten."

The Inherent Limitations of a Remote View

Here's the fundamental problem with this approach: a manager on the phone can't see what isn't immediately obvious in a photo. They can't smell the smoke that has seeped into the wall cavities or find the hidden water damage creeping behind your kitchen cabinets.

For instance, the TCM might see your photo of a water-stained ceiling and authorize a quick fix—a coat of stain-blocking primer and paint. What they can't possibly know from their desk is that the moisture has soaked the attic insulation above, which is now a breeding ground for mold. Their assessment is, by design, only skin-deep.

The TCM’s primary goal is to close your claim as efficiently as possible with the limited information they're given. This focus on speed and cost-containment is often in direct conflict with the detailed, thorough investigation required to make you whole.

This is exactly where many of the common insurance adjuster tricks come from. The entire process is built to manage the claim based on an incomplete, insurer-friendly picture of the damage.

The TCM's performance is measured by how quickly and cheaply they can get your file off their desk. It's not measured by how accurately your settlement reflects the true cost of rebuilding your life. This efficiency-first model is why so many initial settlement offers fall drastically short of what a property owner truly needs to recover.

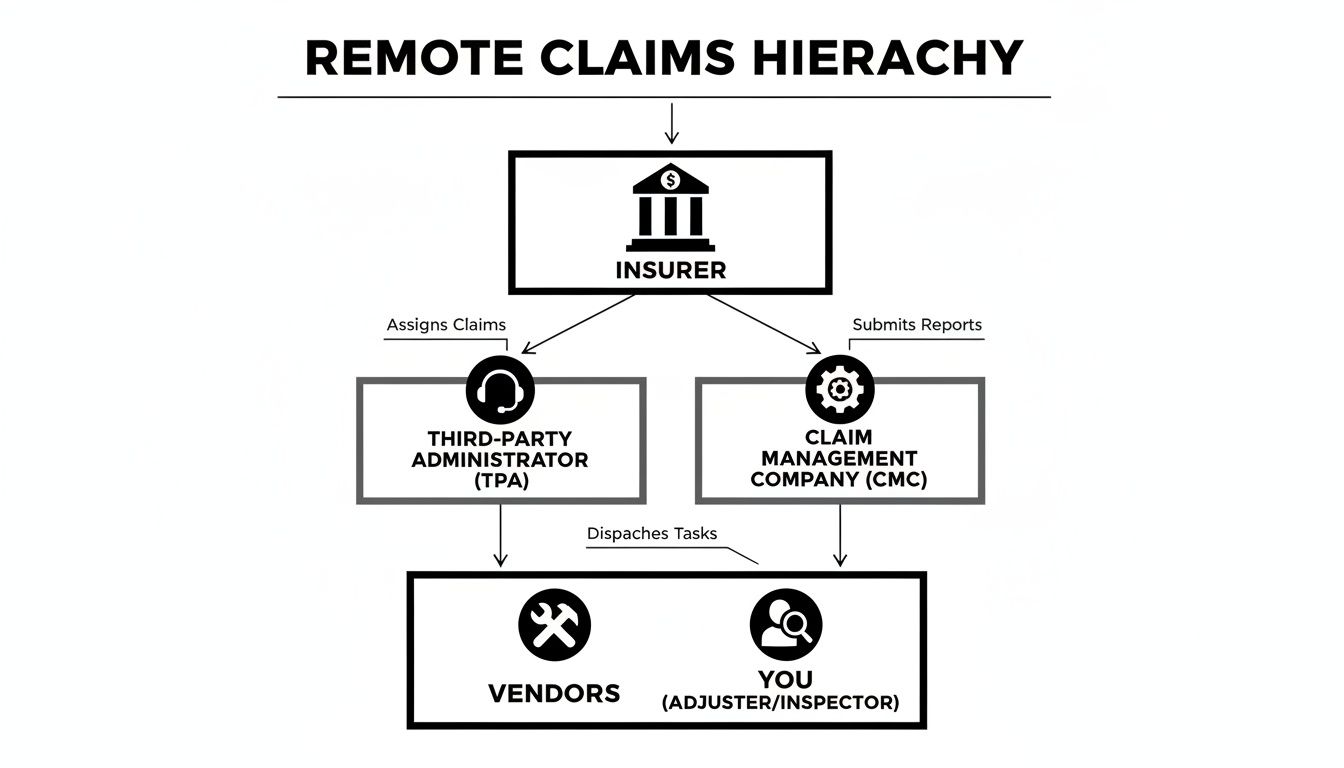

Remote vs. On-Site Claims Management

After you file a major property damage claim, it will go down one of two very different roads. The path your insurance company wants you on is telephonic case management. The other, which puts you in the driver's seat, involves hiring a public adjuster for on-site claims management.

The fundamental difference comes down to a single, crucial fact: a telephonic case manager (TCM) will never set foot on your property. Their entire assessment, every decision they make, is based on the photos you send them and what you can describe over the phone. This hands-off approach creates a huge blind spot, making it almost certain that complex or hidden damages will be overlooked, leading directly to an underpaid claim.

This is the top-down communication structure that insurance carriers prefer.

As you can see, you and the insurer's hand-picked vendors are at the bottom, expected to follow instructions from a remote manager who has never even seen the damage in person.

How On-Site Advocacy Flips the Script

Hiring an on-site public adjuster turns this entire dynamic on its head. We don't rely on your smartphone photos to guess what’s wrong. Instead, we conduct our own exhaustive, hands-on inspections of your property.

We’re the ones climbing into the attic, crawling through the crawlspace, and using moisture meters and thermal cameras to find what the eye can’t see. We document every single detail that a remote manager, sitting hundreds of miles away, would never even know to ask about. This is critical because real-world property damage is rarely just what you see on the surface.

Our job is to build your claim from the ground up, based on physical evidence—not manage a digital file from a distance.

The core difference is this: The telephonic case manager works to control costs for the insurer. The public adjuster works to maximize your financial recovery. Their goals are fundamentally opposed.

Comparing Claim Management Approaches

Understanding the day-to-day differences between these methods is the key to protecting your financial future. This table gives you a side-by-side look at how telephonic and in-person management can dramatically change the outcome of your claim.

| Aspect | Telephonic Management (Insurer) | On-Site Management (Public Adjuster) |

|---|---|---|

| Damage Assessment | Relies on your photos and video calls. Often misses hidden or complex issues. | Conducts multiple, detailed on-site inspections using specialized tools. |

| Vendor Coordination | Recommends "preferred" vendors who may prioritize the insurer’s budget. | Helps you vet and manage independent contractors focused on quality repairs. |

| Negotiation Leverage | Based on limited, remote information. Negotiates to close the file quickly and under budget. | Builds a comprehensive, evidence-based claim file to negotiate from a position of strength. |

| Primary Goal | Efficiently manage and close the claim while controlling costs for the insurance company. | Advocate for your best interests to secure a full and fair settlement. |

Ultimately, what's convenient for the insurer often comes at a steep price for you. A telephonic case manager is trained to close a high volume of files as efficiently as possible. A public adjuster, on the other hand, is licensed to be your personal advocate, ensuring your one critical claim gets the depth and detail it deserves.

Critical Red Flags in Your Claims Process

After you’ve suffered property damage, you’re just trying to get back on your feet. It's natural to trust the telephonic case manager your insurer assigns to your claim. The problem is, their job is to close your claim for the insurance company, and that goal can easily conflict with your need for a full and fair recovery.

Your best defense is knowing how to spot the warning signs that their agenda isn't aligned with yours. Think of it as learning to read between the lines. Here are some of the most common red flags I see in the field.

Rushing You into Quick Decisions

One of the oldest tricks in the book is creating a false sense of urgency. A case manager might push you to sign a release, accept a settlement offer, or agree to a scope of work before you've had a moment to breathe, let alone read the fine print.

Why the rush? It’s often a tactic to get you locked into a low number before you discover the true extent of the damage. You have every right to take the time you need to make smart decisions about your own home or business.

What to do: Don't be afraid to pump the brakes. A simple, "I'll need some time to review this properly. Can you let me know what the absolute deadline for a response is?" puts you back in control.

Minimizing the Severity of Damage

It’s amazing how a manager sitting in a cubicle hundreds of miles away can feel so confident about your property damage. Based on a few photos, they might try to downplay what you’re seeing with your own eyes, saying things like, "That just looks like surface soot," or "We can probably just patch that."

These remote assessments are notorious for missing the big picture—like hidden water damage behind drywall, smoke contamination in your attic, or a foundation crack that compromises the whole structure. Their real goal is to set a low anchor for the claim’s value right out of the gate.

Key Insight: A verbal opinion from a call center is not a substitute for a hands-on inspection by a qualified expert. The damage they can't see from their desk can end up costing you thousands.

If your gut tells you the damage is worse than they’re letting on, you absolutely need a second opinion. When an insurer starts lowballing, knowing how to fight an insurance claim denial or an unfair offer is crucial.

Pressuring You to Use Their Contractors

Your telephonic case manager will almost certainly have a "preferred" restoration company ready to dispatch to your property. While it sounds helpful, these vendors are "preferred" for a reason—they have an established relationship with the insurance company.

This can put their loyalty in a tough spot. They may feel pressure to stick to the insurer's lean budget, even if it means cutting corners on your repairs.

Be wary if you notice these subtle (or not-so-subtle) moves:

- Discouraging outside bids: They might claim that getting your own estimates is "unnecessary" or will "just delay everything."

- Pushing one vendor hard: They may sound like a broken record, bringing up the same company over and over, and get irritated if you mention looking elsewhere.

Remember, in both Oregon and Washington, the law is on your side: you have the right to choose your own contractor. You can ask them directly, "Am I required to use this vendor, or am I free to get estimates from contractors I choose?"

Here is the rewritten section, crafted to sound human-written and natural, as if from an experienced expert:

Know Your Rights in Oregon and Washington

It’s easy to forget, but your insurance policy isn't just a thick stack of paper—it's a legal contract. And like any contract, both sides have to play by the rules. When your claim is being handled by a telephonic case manager, your insurer is still bound by strict state laws designed to protect you.

Here in the Pacific Northwest, those rules aren't just friendly suggestions; they have real teeth. Understanding your rights is the single best way to protect yourself from being rushed through the process or offered a lowball settlement.

State Oversight of Your Claim

Insurance companies don’t get to make up their own rules. They operate in a heavily regulated industry, and state agencies act as the referees to make sure they're treating you fairly.

For property owners in our corner of the country, these are the key agencies holding insurers accountable:

- Oregon: The Oregon Division of Financial Regulation (DFR) is the state's watchdog, enforcing the insurance code and its rules on fair claim settlement practices.

- Washington: The Office of the Insurance Commissioner (OIC) serves the same critical function, overseeing how insurers conduct themselves and protecting your rights as a consumer.

These agencies set firm deadlines for things like responding to your calls, investigating the damage, and paying what you are owed. A case manager working from a call center hundreds of miles away doesn't get a pass on these legal duties.

Your insurance policy is a contract governed by state law. An insurer's remote-first approach does not exempt them from their legal duty to treat you fairly and handle your claim according to the rules set by Oregon and Washington regulators.

What this all boils down to is that you have powerful protections. Your insurer can't just deny your claim with a vague explanation. They have to give you a clear reason, pointing to the exact language in your policy that supports their decision. They can’t leave you hanging for weeks without an update.

If you feel your insurance company isn't playing by the book, you have the right to file a formal complaint with these state agencies. This local oversight is your backstop, ensuring that even a remote claims process is held to the same high standard of accountability.

When You Need a Public Adjuster on Your Side

Let's be honest, trying to manage a property claim on your own feels like taking on a second, unpaid job. You’re already reeling from the damage to your home or business, and now you’re buried in paperwork, stuck on hold, and trying to reason with a telephonic case manager who has never set foot on your property. It’s exhausting.

So, when does the frustration cross the line into needing professional backup? There are a few clear signs. If you're dealing with a large, complicated claim from a fire or major flood, the risk of your insurer overlooking crucial details goes way up. Another huge red flag is a settlement offer that feels completely out of touch with reality—one that wouldn't even begin to cover your actual repair costs.

Sometimes the warning signs are less about the money and more about the process. Is your case manager impossible to reach? Do you feel constantly rushed or dismissed? Or maybe you're just worn down by the sheer administrative headache of it all. These are all moments when you should seriously consider getting an expert in your corner.

Leveling the Playing Field

This is precisely where a public adjuster comes in. A public adjuster is the only type of insurance professional licensed by the state to work exclusively for you, the policyholder. We don’t report to the insurance company. Our one and only job is to fight for your best interests and get you every dollar you're entitled to under your policy.

A public adjuster is your expert advocate. We take the entire claims process off your shoulders—from documenting the loss to negotiating the final settlement—so you can focus on putting your life back together.

Hiring an expert completely shifts the balance of power. We step in and handle the stressful phone calls and emails. We meticulously document every detail of your loss to build a powerful, evidence-based claim. Suddenly, the negotiation is no longer based on the insurance company's limited viewpoint but on the full, documented reality of your damages.

Best of all, reputable firms like NW Claims Management operate on a contingency-fee basis. This means you pay nothing upfront. Our fee is a small percentage of the money we recover for you from the insurance company. We don't get paid unless you do. This ensures our goals are perfectly aligned with yours: getting you the maximum, fair settlement you deserve. If you're questioning whether your specific situation calls for this level of help, our guide on when to hire a public adjuster breaks it down even further.

Your Questions About Telephonic Case Management Answered

When you're dealing with a major property insurance claim, things can get confusing fast—especially when a telephonic case manager gets assigned to your file. Let's cut through the jargon and get straight to the real answers for the questions we hear from property owners every day.

Am I Required to Use Their Recommended Vendors?

The short answer is no. In Oregon and Washington, you have the legal right to hire any contractor you trust. The insurance company's list of "preferred" vendors might seem helpful, but it's crucial to remember who they work for. Their main business relationship is with the insurer, not you.

This is why getting your own, independent bids is so important. It ensures the repair plan is based on what's actually needed to restore your property correctly, not just what's convenient for the insurance company's bottom line.

Is Giving a Recorded Statement Mandatory?

Almost every policy has what's called a "cooperation clause," which does require you to give a statement about what happened. That said, you need to be very careful. A recorded statement isn't just a conversation; it's a formal tool the insurer uses to lock in your story. Any small mistake or inconsistency can be used to limit or deny your claim down the road.

If you're facing a large or complicated loss, it's always a good idea to talk with a public adjuster before you agree to go on the record.

If an adjuster tells you your claim is denied over the phone, that is not the final word. Always insist on a formal denial letter that cites the specific policy language they are using to justify their decision.

What if They Say My Damage Is Not Covered?

Never, ever accept a verbal denial over the phone. An initial "no" is often just a tactic to see if you'll push back. You are entitled to a formal, written explanation that points to the exact wording in your insurance policy that they believe excludes your damage.

Interpreting policy language is a complex skill, and initial denials are overturned all the time with a well-argued, evidence-based appeal. You can learn more about how to get more from your insurance claim by understanding these common strategies.

Don't let a remote case manager working from a cubicle hundreds of miles away dictate the outcome of your claim. If you feel like you're getting the runaround or being handed a lowball offer, let the experts at NW Claims Management step in. Visit https://nwclaimsmanagement.com for a free claim evaluation and see how having a local advocate on your side can secure the full settlement you deserve.