At 6:30 the next morning, the house is quiet for the first time since the fire. The flames are out, the trucks are gone, and the pressure shifts fast. A restoration company wants authorization. The carrier wants to open the claim. Family members want answers. You have to decide what gets touched, what gets documented, and what waits.

That is the point where a fire loss stops being only an emergency and becomes a claim.

PA fire recovery depends on sequence. Property owners often react on instinct and start cleaning, tossing damaged items, or signing the first work order put in front of them. I understand the urge. It feels like progress. But insurers evaluate documentation, cause, scope, mitigation, and consistency. Every early decision can either support your settlement or give the carrier room to question part of it.

The owners who protect their claim best are usually the ones who slow the process down just enough to separate urgent work from irreversible work. They preserve evidence before disposal. They authorize necessary mitigation without handing over control of the entire job. They keep records from day one. If you need a practical overview before making those calls, this guide on what to do after a house fire for insurance lays out the early claim priorities clearly.

There is also a real trade-off here. Waiting too long can make conditions worse, but moving too fast can erase proof of damage, confuse the scope, and weaken the file you will rely on later. The right approach is controlled action. Secure the property. Document everything. Approve only the work needed to prevent additional loss. Then build the claim in a way an adjuster, engineer, or reviewer can follow without guessing.

If you also want a contractor-side overview of cleanup and repair, these steps for fire damage restoration are a useful starting point.

The First 72 Hours After a Fire

The first full day after a fire is when expensive mistakes usually start.

The fire department is gone. Family members are asking what can be saved. A mitigation crew wants a signature. You want the house to feel less chaotic, so the natural impulse is to start clearing, cleaning, and making fast decisions. That instinct is understandable. It also creates problems fast if you act before the loss is documented.

The first 72 hours are not just about recovery. They are about setting the claim up correctly. Insurers look for cause, scope, condition, mitigation, and consistency from the start. If the file gets muddy in the first few days, it is much harder to clean up later. If you want a contractor-side overview while you sort out priorities, these steps for fire damage restoration are a useful starting point.

What your instincts tell you to do, and what protects the claim

Property owners often want to get the worst of it out of sight. They throw away charred contents, pull up wet flooring, wipe soot off surfaces, and let a vendor start demolition before anyone has created a clear record. Those choices feel productive because the property looks active instead of frozen.

Insurance does not reward activity by itself. Insurance rewards documented, supportable loss.

That distinction is important because people often say, “The adjuster will see it.” Sometimes they do. Sometimes they arrive after rooms have been cleared, damaged contents are stacked in a dumpster, and soot patterns that showed smoke spread are gone. At that point, parts of the claim depend on memory, and memory is weak evidence.

A more disciplined approach works better. Photograph first. Video first. List what was there before anyone removes it. Then approve only the work needed to stabilize the property and prevent additional damage. A practical checklist like what to do after a house fire insurance claim steps can help you keep the order straight when the day is pulling you in six directions.

The decisions that shape your settlement early

The first calls and authorizations matter more than many owners realize.

Open the claim promptly and get the claim number. Write down the date, the time, the name of every representative, and what was discussed. If coverage questions or scope disputes show up later, those notes become part of your working file.

Document the property before anything substantial changes. Start with wide shots of each room and exterior elevation. Then move to close photos of burned materials, smoke residue, water lines, damaged mechanicals, personal property, and any areas that look only lightly affected. Light smoke damage and hidden heat damage are often disputed later.

Keep every receipt tied to the loss. That includes board-up work, tarping, hotel stays, storage, emergency clothing, and other reasonable extra costs caused by displacement. Carriers usually want support for every dollar claimed, even when the expense was clearly necessary.

Be careful with work authorizations. Emergency mitigation is often appropriate. Full demolition, pack-out approvals, or open-ended restoration contracts signed on day one can create cost and control issues before the scope is even understood. I have seen owners lock themselves into a contractor relationship before they had a clear sense of what the insurer would accept, what could be cleaned instead of replaced, and what evidence needed to stay in place.

One practical rule holds up well here.

If the step cannot be reversed, document it first and understand why it is being done.

Many residential fires start in ordinary living areas such as kitchens, utility spaces, and garages. The point for claim strategy is simple. The room of origin is only part of the loss. Smoke, soot, odor, and firefighting water often affect areas that do not look dramatic at first glance. Owners who focus only on the visibly burned section often under-document the rest of the property, and that is where settlements start shrinking.

Securing Your Property and Preventing Further Loss

Once the scene is released, your job changes. You're no longer responding to a fire. You're preventing a second loss.

That second loss can come from rain through an open roof, theft through a broken entry, vandalism, frozen pipes after utilities are disrupted, or microbial growth from standing water left by firefighting. Policies generally expect property owners to take reasonable steps to prevent further damage. The mistake is confusing mitigation with cleanup.

Mitigation is necessary. Premature cleanup is dangerous

Mitigation protects the property from getting worse. Cleanup can erase evidence.

Use this distinction:

| Action | Usually the right move now | Why |

|---|---|---|

| Board up broken windows and doors | Yes | Prevents theft, weather intrusion, and trespass |

| Tarp exposed roof areas | Yes | Stops additional water entry |

| Extract standing water | Yes | Limits secondary damage from firefighting water |

| Set drying equipment | Yes, if documented | Preserves materials that can still be evaluated |

| Tear out finishes immediately | Not always | Can destroy proof of burn pattern, smoke spread, and water line evidence |

| Discard contents in bulk | No | Removes proof of condition, brand, model, and quantity |

The order that usually works

Handle the site in layers.

Secure openings first

Broken doors, windows, garage openings, and roof breaches need immediate attention. Ask for itemized invoices and keep photos before and after temporary protection goes in.Control water next

Firefighting water is a separate damage driver. Remove standing water, then dry the structure methodically. Don't let a contractor rush you into broad tear-out without documenting what was wet, how high the water reached, and which materials were affected.Protect salvageable contents

Move unaffected or lightly affected items to a clean, secure area only after they've been photographed in place. Label boxes. Keep packing lists. If contents go to storage, track exactly what left and where it went.Stabilize utilities and hazards

Electrical, gas, and HVAC systems need evaluation before reuse. For future prevention once you're through this loss, practical homeowner guidance on how to prevent electrical fires at home is worth reviewing.

Don't let anyone tell you that “we'll sort it out with insurance later” after they've already removed the evidence.

Risk management after the flames are out

The best site decisions are boring and well documented. The worst ones are fast, verbal, and undocumented.

A simple property-loss framework like these risk management steps for property owners is useful because it keeps you focused on exposure control, not panic spending. If a contractor can't explain what they're doing, why it's necessary now, and how they'll document it, slow the process down.

What works is temporary protection, moisture control, and careful logging.

What doesn't work is “clean as much as possible before the adjuster arrives.” That usually helps the insurer more than it helps you.

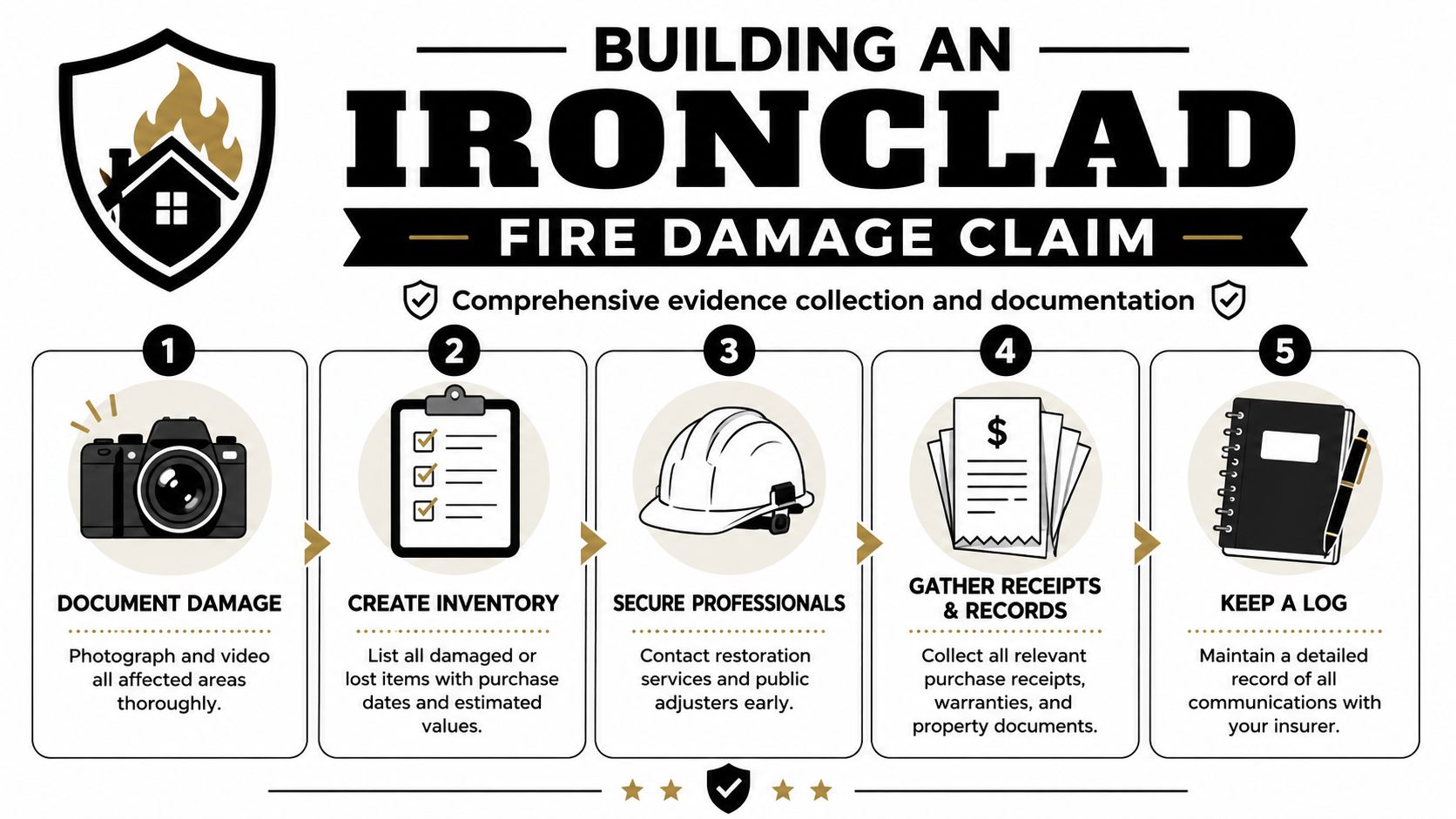

Building an Ironclad Fire Damage Claim

A strong fire claim isn't built from one stack of random photos. It's built from organized proof.

Pennsylvania recovery guidance is clear on the core principle. Document damage before beginning repairs, and include photos, serial numbers, model information, and supporting detail that helps establish replacement-cost value through the state's after-disaster guidance. In practice, the cleanest files separate evidence into four buckets: building damage, smoke and soot contamination, contents loss, and extra expenses.

Bucket one for building damage

Think like a surveyor, not a homeowner.

Go room by room with video first. Narrate what you're seeing. Then take still photos of ceilings, walls, trim, flooring, doors, windows, cabinets, insulation exposure, attic access points, basement conditions, and all exterior elevations. Include utility spaces, crawl access, detached structures, and fencing if affected.

Focus on details that often get missed:

- Heat impact: Warped metal, cracked glass, distorted fixtures, blistered finishes

- Water effects: Swelling at baseboards, saturated insulation, ceiling stains, pooled areas

- Hidden migration paths: Attic, wall cavities, chases, returns, and duct runs

- Code-triggered items: Safety systems, egress components, alarms, and related assemblies

Bucket two for smoke and soot contamination

Many claims are undercounted in this scenario.

People document the burned room and ignore the rest. Insurers look for a basis to limit scope. If the soot is visible only in the room of origin, they may treat the rest of the structure as light cleaning or no damage unless the file shows broader impact.

Document far from the flames. Open cabinets. Photograph soot on supply vents, tops of door casings, inside drawers, electronics, blinds, soft goods, attic framing, and light-colored surfaces. If the HVAC system moved particulates, note each affected register and return.

Smoke doesn't need heavy charring to create a real claim issue. Odor, residue, and particulate spread matter.

Bucket three for contents loss

This part overwhelms people because it's tedious. It's also where a lot of money gets lost.

Don't write “clothes damaged” or “kitchen items ruined.” Itemize. Brand if known. Model if known. Quantity. Age. Condition. Replacement equivalent. Serial number when available. If a receipt exists, save it. If it doesn't, use photos, manuals, warranty registrations, online order histories, and family pictures that show the item in the home.

A room-by-room approach works best:

- Primary bedroom: Mattress, frame, bedding, dresser contents, shoes, electronics

- Kitchen: Small appliances, cookware, utensils, pantry goods, dishes

- Garage: Tools, seasonal items, power equipment, storage bins

- Office: Monitors, printers, files, peripherals, desk furniture

If you've ever read a guide on winning your hail damage claim, the same principle applies here. Specificity wins disputes. Generalities lose them.

Bucket four for extra expenses

Track every cost tied to displacement or temporary operation.

That includes lodging, storage, extra travel, pet boarding when necessary, increased meal costs in situations where normal cooking isn't possible, laundry, emergency clothing purchases, and short-term business continuity expenses if the property is commercial. Keep the receipt and note why the expense happened.

A strong submission package often mirrors the discipline used in how to file a property damage claim properly. One folder for structure, one for smoke, one for contents, one for extra expense. Clean labels. Consistent dates. No guesswork.

The common mistakes are always the same. Throwing items away too early. Letting demolition outrun documentation. Forgetting the attic, basement, HVAC, and closed storage areas. Assuming the insurer will fill in missing facts on your behalf.

They won't.

Your Guide to the Insurance Claim Timeline

Most property owners think the claim process is a straight line. Report the fire, meet the adjuster, get a check, rebuild.

In real life, it's a negotiation process with moving parts, overlapping inspections, and a lot of paperwork. That complexity isn't accidental. Fire recovery has become a specialized financial process. PA Fire Recovery Service says 504 volunteer fire companies participated in its program, almost 50% of companies surveyed bill for some type of service, and 60% of those companies collect less than 20% of what they bill, according to PA fire recovery facts. The same source notes that Fire Recovery USA has operated since 2006 and serves departments in 42 states. That tells you something important. Cost recovery after a fire is formal, documented, and financially structured.

Policyholders are entering that same kind of system.

Who you'll deal with

Not every adjuster at your loss is there for the same purpose.

| Role | Who they work for | What to expect |

|---|---|---|

| Company adjuster | The insurance carrier | Reviews coverage, scope, and payment from the insurer's side |

| Independent adjuster | Hired by the carrier | Handles field work for the insurer but still represents carrier interests |

| Public adjuster | The policyholder | Documents, values, and negotiates for the insured |

That distinction matters because people often say, “The adjuster is helping me.” Maybe. But the company's adjuster is still evaluating the claim through the insurer's framework.

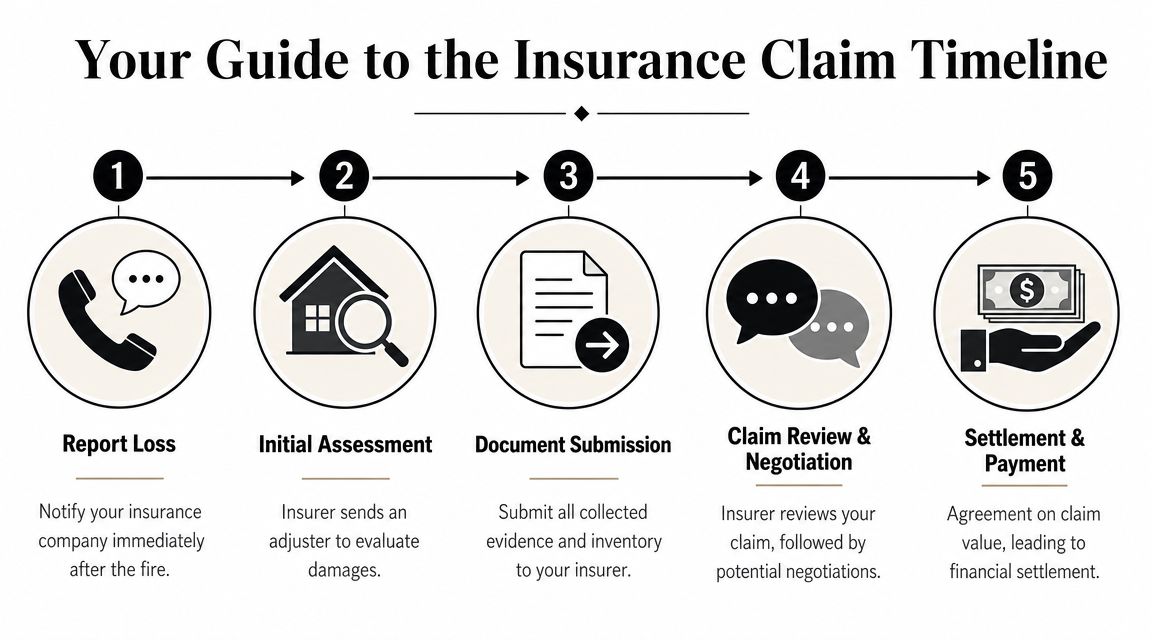

The normal sequence

The timeline usually unfolds like this:

- Notice of loss: You report the claim and receive a claim number.

- Emergency mitigation: Board-up, tarping, extraction, and stabilization begin.

- Initial inspection: The insurer's representative inspects the damage.

- Information requests: Inventories, receipts, photographs, contractor estimates, and forms start coming in and going out.

- Scope review: The insurer develops its view of what was damaged and what it will pay for.

- Negotiation: Differences over pricing, quantities, methods, code items, or contamination scope get addressed.

- Payment stages: Funds may come in portions rather than one final lump sum.

Where claims usually bog down

The friction points are predictable.

One is scope compression. The insurer may acknowledge the fire but narrow the repair footprint, especially for smoke migration, hidden water effects, or code-related items. Another is paper overload. Property owners get asked for records while trying to live out of a hotel or operate a disrupted business. A third is personnel change. Files get reassigned, and the new person may revisit earlier assumptions.

Keep one running claim log with dates, names, phone numbers, promises made, and documents sent. Memory is not a claim system.

A methodical communication approach is often more effective than emotional argument. Short emails. Attached support. Clear subject lines. Written follow-up after every call. If the insurer says something important by phone, confirm it in writing.

The people who struggle most are usually reacting one email at a time. The people who do better manage the file as a project.

Should You Hire a Public Adjuster for Fire Recovery?

Not every fire loss needs a public adjuster. Some do.

If the damage is limited, the scope is obvious, and the insurer is responsive, you may be able to handle it yourself. But many fire losses stop being simple once smoke spread, hidden moisture, code issues, contents inventory, or business interruption enter the picture.

When handling it alone gets risky

A public adjuster becomes a serious consideration when one or more of these conditions show up:

- The loss is large or near-total: Big files create more room for pricing disputes, missed line items, and staged payments that don't match actual rebuild needs.

- The contents claim is extensive: Inventorying a household or business after a fire is labor-heavy and detail-sensitive.

- Smoke spread is broader than the insurer admits: This is one of the most common pressure points in fire claims.

- You own a commercial, nonprofit, or mixed-use property: Operational losses add layers that most individual policyholders haven't handled before.

- You're too overwhelmed to manage the process well: That alone is a real factor. Fire losses happen while people are displaced, exhausted, and trying to keep life moving.

What a public adjuster actually does

A licensed public adjuster works for the policyholder, not the insurance company. The job is to interpret the policy, document the loss, assemble support, value the damages, and negotiate the claim.

That doesn't mean every public adjuster is the right fit. Ask how they document smoke claims, how they handle contents inventory, how often they communicate, whether they manage supplemental claims, and how fees work. If you need a plain-language overview of the benefits of hiring a public adjuster, start there and compare it against your situation.

A practical decision test

Ask yourself three questions.

First, do I know what my claim is worth. Not what the insurer says first. What the full documented loss is worth.

Second, do I have the time and concentration to build and manage this file properly.

Third, am I comfortable negotiating scope, valuation, and policy interpretation if the insurer pushes back.

If the answer to any of those is no, professional help may be a smart move.

A good public adjuster doesn't create damage. They make sure the documented damage is fully presented, properly valued, and hard to dismiss.

Managing Your Restoration and Rebuild

Getting the claim paid is not the finish line. It's the handoff to reconstruction.

Fire restoration works best as a staged process: safety assessment, cleanup and damage removal, water removal and drying where needed, then rebuild, as outlined in this fire restoration process guide. The owners who stay organized here are the ones who keep their settlement from leaking away through bad contracts, loose change orders, and poor recordkeeping.

Run the rebuild like a file, not a favor

Do not rely on verbal assurances.

Keep signed contracts, bid comparisons, change orders, invoices, materials lists, equipment charges, and payment records. FEMA-style discipline is useful here for a reason. Labor time records, equipment logs, receipts, invoices, purchase orders, and contract records make later disputes easier to solve. They also help if the insurer questions supplemental charges or if a mortgage company requires proof before releasing funds.

Use a simple review standard before approving work:

- Scope match: Does the contractor's scope match the settled claim and actual site conditions?

- Code review: Are alarm, exit, lighting, sprinkler, or other safety upgrades being addressed early?

- Cost support: Are allowances, unit costs, and markups understandable on paper?

- Payment timing: Are you paying against milestones or just writing large deposits without documentation?

Watch the valuation gap during rebuild

One issue shows up late and catches people off guard. The difference between what's already been paid and what's needed to complete replacement properly.

That's where understanding actual cash value vs replacement cost matters. If your policy pays in stages, you may need to document completed work and incurred costs before the recoverable portion is released. Don't assume money arrives automatically just because repairs are underway.

Keep control of the project

Choose contractors who answer questions clearly and document well. If they resist written change orders or can't show how they track labor and materials, expect problems later.

The strongest rebuilds are boring in the best way. Clean paperwork. Clear scope. Permits in place. Funds released in sequence. Final inspections completed before anyone declares the job done.

Fire recovery is exhausting, but it doesn't have to stay chaotic. Good decisions after the emergency are what turn a fire loss into a complete insurance recovery.

If you're dealing with a fire claim and need experienced policyholder representation, NW Claims Management helps homeowners, businesses, nonprofits, and public entities document losses, interpret policy language, and negotiate for fair settlements. The firm works on behalf of the insured, not the carrier, and offers direct guidance when the claim process has become too complex, too slow, or too expensive to manage alone.