For property owners in Oregon and Washington, the threats of fire, floods, storms, and vandalism are not abstract concepts. They are tangible risks that can jeopardize financial stability overnight. While insurance is a crucial safety net, it's not a complete strategy. True resilience comes from proactive risk management, which involves more than just paying a premium. It means actively identifying and addressing potential problems before they escalate. For instance, understanding how to proactively address common issues, like learning the specifics of how to clean mold in shower stalls, is a simple yet vital part of preventing larger, more costly damage down the line.

Many owners believe they are prepared, only to discover devastating gaps in their documentation, policy understanding, and claims strategy when it's too late. This guide moves beyond generic advice to provide a robust framework. We will detail 5 risk management steps that empower residential, commercial, and nonprofit property owners to transition from a reactive stance to a position of control. By implementing these actionable steps, you can not only mitigate potential disasters but also ensure you are fully equipped to secure a fair and complete financial recovery if the worst happens.

1. Risk Identification and Assessment

The foundational step in any effective property risk management plan is systematically identifying and assessing potential hazards. You can't protect against a threat you don't know exists. This process involves a meticulous cataloging of every potential vulnerability affecting your residential, commercial, or nonprofit property, from structural weaknesses and aging systems to environmental exposures and even gaps in your insurance coverage. It's about moving from a reactive to a proactive mindset.

For property owners in Oregon and Washington, this means considering specific regional threats. The Pacific Northwest is prone to wildfires, earthquakes, winter storms, and flooding. A comprehensive assessment establishes a crucial baseline of your property's condition before a loss occurs, which is invaluable during an insurance claim.

Practical Examples of Risk Assessment

- Residential: A Portland homeowner, through a professional assessment, discovers their beautiful wood shake roof is a significant liability in a designated wildfire hazard zone. This early identification allows them to proactively replace it with a fire-resistant material, potentially preventing a total loss.

- Commercial: The owner of a business in a flood-prone Washington area documents recurrent water intrusion points in their building's foundation. This record enables them to implement targeted waterproofing measures and provides critical evidence for a future water damage claim.

- Nonprofit: A nonprofit organization in Eugene identifies severe structural deficiencies in their historic building during an annual review. This documentation becomes the basis for an insurance claim to fund necessary repairs, averting a catastrophic failure and ensuring the safety of its staff and visitors.

When considering the crucial stage of risk identification and assessment, understanding the practical application is key. For example, a thorough guide to the steps of fire risk assessment can provide a clear framework for one of the most common and devastating property threats. Although the guide is UK-based, its principles for systematically checking a property are universally applicable and highly useful.

Key Takeaway: A detailed risk assessment is more than a simple checklist. It's a living document that provides the evidence needed to validate claims, justify repairs, and negotiate fair settlements with insurance carriers.

Actionable Tips for Implementation

To make risk identification a routine part of your property management, consider these practical steps:

- Schedule Professional Inspections: Have your property inspected annually, especially if it's located in a high-risk area of Oregon or Washington. A professional, such as a public adjuster, can spot both obvious and hidden risks you might overlook.

- Maintain Detailed Records: Keep a comprehensive photographic and video log of all rooms, building systems (HVAC, plumbing, electrical), and structural elements.

- Document Major Systems: Note the age, installation date, and maintenance history of your roof, electrical panel, and plumbing. This documentation is critical when filing a claim for a system failure, like a fire. If you ever need to file a claim after a fire, having this prior documentation is a huge advantage; knowing what to do after a house fire with your insurance is much easier with good records.

- Organize Your Documentation: Create separate digital and physical folders for each area of your property to keep your risk assessment documents organized and easily accessible.

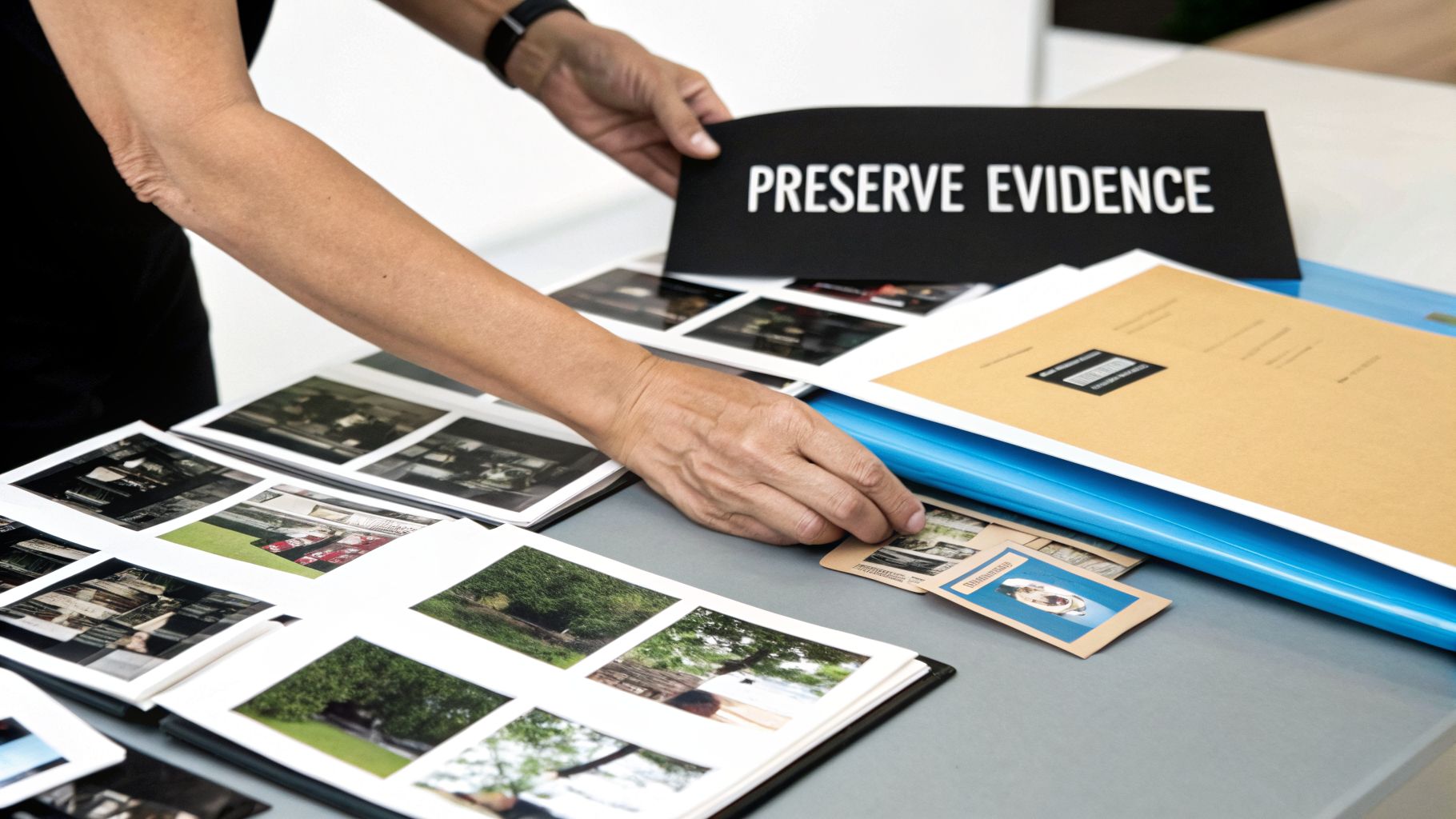

2. Documentation and Evidence Preservation

If risk assessment is the foundation, then thorough documentation and evidence preservation is the steel framework that supports your entire insurance claim. This critical step involves the systematic collection, organization, and maintenance of all records related to your property's condition, the damages it sustains, and the losses incurred. For property owners in Oregon and Washington, this process is not merely about taking a few photos; it is about building an irrefutable case to substantiate your loss and counter the common insurer tactic of undervaluation.

This step transforms abstract damage into quantifiable, provable figures. Following guidelines popularized by the National Association of Insurance Commissioners (NAIC) and FEMA, professional public adjusters specialize in this type of forensic documentation. They photograph damage patterns, catalog personal property, and preserve evidence in a format designed to withstand insurer scrutiny and potential legal challenges.

Practical Examples of Evidence Preservation

- Residential: A Salem homeowner, after a devastating fire, documents the damage room-by-room with photos showing specific burn patterns and smoke damage. This detailed evidence enables their public adjuster to calculate a total loss replacement cost, successfully challenging the insurance carrier's initial offer, which was 40% lower.

- Commercial: Immediately after a pipe bursts, a Portland business owner preserves evidence of water intrusion, including moisture meter readings and photos of the initial damage. This documentation supports a critical claim for business interruption losses and emergency mitigation costs that the insurer initially questioned.

- Nonprofit: A Tacoma nonprofit maintains a detailed inventory of donated equipment. When a flood damages their facility, this pre-existing list substantiates a $250,000 loss claim that their insurer had initially valued at only $75,000, ensuring the organization could replace essential community resources.

The goal is to create a complete and accurate record of the loss. A professional approach to property damage assessment moves beyond simple snapshots to build a comprehensive file that leaves no room for dispute, which is a key part of the 5 risk management steps.

Key Takeaway: Evidence is the currency of an insurance claim. Without meticulous documentation, you are negotiating from a position of weakness, relying on the insurance company's assessment of your loss, not your own.

Actionable Tips for Implementation

To ensure your documentation is robust and defensible, integrate these practices immediately following a loss:

- Photograph Extensively: Capture damage from multiple angles and distances (wide, medium, and close-up) to show both scope and specific detail.

- Create Detailed Captions: For every photo and video, note the date, time, specific location (e.g., "north wall of master bedroom"), and a brief description of the damage shown.

- Build a "Before and After": If you have "before" photos of your property, include them alongside the "after" shots of the damage to provide a clear comparison of the loss.

- Obtain Multiple Contractor Bids: Get written, itemized estimates from at least two licensed contractors. This establishes a credible, market-based cost for repairs.

- Maintain a Master Loss List: Create a spreadsheet of all damaged or destroyed personal property. Include descriptions, brand names, original purchase dates, costs, and estimated replacement values.

- Keep All Receipts: Save every receipt, invoice, and contract related to repairs, temporary living expenses, and replacement purchases. Organize them in a dedicated folder.

3. Policy Analysis and Coverage Optimization

A crucial, often-overlooked component in the list of 5 risk management steps is the deep analysis of your insurance policy. Having insurance isn't enough; understanding the intricacies of your coverage is what truly protects your assets. This step involves a detailed interpretation of complex insurance language, identifying all applicable coverages, and strategically presenting your claim to maximize the allowable payout. Most policies are filled with multiple coverage sections, exclusions, limits, and conditions that are unclear to the average property owner.

Professional public adjusters use their industry expertise to decode these provisions, finding coverage benefits that an insurer might initially overlook. This proactive analysis ensures you can structure your claim to access the full contractual benefits you are entitled to, rather than accepting an initial offer that may be an undervaluation. It turns your policy from a passive document into an active tool for recovery.

Practical Examples of Policy Optimization

- Residential: A Portland homeowner with a standard policy discovered, with expert help, that they had extended "loss of use" coverage providing 18 months of temporary housing. The insurer had not mentioned this benefit in their initial settlement offer, which would have left the family with a significant financial shortfall.

- Commercial: Following a fire, the owner of a commercial building in Eugene identified a business interruption clause that compensated them for six months of operating losses. This amounted to $350,000 beyond the basic structural damage coverage, proving critical to the business's survival.

- Nonprofit: A Seattle-based nonprofit found coverage for replacing their volunteer coordinator and preserving operational overhead within their commercial general liability policy. This discovery was essential for maintaining their community services without interruption after a covered event.

Understanding the nuances of your policy is a vital part of managing risk. For a clearer picture of how different parts of your policy work, learning how insurance policy limits are explained can give you a significant advantage before you ever have to file a claim.

Key Takeaway: Your insurance policy is a contract written in your favor. Expert analysis can uncover significant financial benefits and coverages that are not always obvious, ensuring you receive the full settlement you are owed.

Actionable Tips for Implementation

To properly analyze and optimize your insurance coverage, adopt these habits:

- Obtain Complete Policies: Always get complete copies of all your insurance policies and any attached riders. Do not rely on summary documents or declaration pages alone.

- Review Your Declarations Page: Carefully review the "dec pages" to understand your specific coverage limits and deductibles for each section of the policy.

- Document Insurer Communications: Keep a written record of all conversations with your insurer or agent regarding coverage questions. Their explanations can be important if a dispute arises later.

- Note Agent Recommendations: When you first purchase or renew a policy, keep detailed notes of your agent's explanations and recommendations about coverage. This can provide context and support your interpretation of the policy.

- Compare Loss Scenarios: Mentally walk through different loss scenarios, such as a fire, a burst pipe, or a windstorm, and try to trace how your policy would respond to each. This exercise helps identify potential gaps in coverage.

4. Damage Valuation and Loss Estimation

A critical stage in the risk management cycle, particularly after a loss has occurred, is the accurate valuation of damage and estimation of the total loss. This step involves a professional, detailed assessment of the repair or replacement costs for all affected property. An accurate monetary value is not just a number; it's the foundation of your insurance claim and the key to a fair settlement.

Insurance companies often use their own adjusters and proprietary software to generate initial estimates. However, these figures can sometimes serve the insurer's interest by minimizing payouts through lowball estimates, overlooked damages, or arbitrary depreciation. A precise, independent valuation is your most powerful tool to counter these tactics and ensure the proposed settlement truly reflects your actual loss.

Practical Examples of Damage Valuation

- Residential: After a fire in their Portland home, the owner received an initial insurer estimate of $75,000. A professional public adjuster conducted a forensic valuation, identifying $185,000 in structural damage, equipment replacement, and necessary mitigation costs, resulting in a settlement 2.5 times higher.

- Commercial: A Tacoma commercial building suffered significant water damage. The insurer applied an arbitrary 30% depreciation to the claim. An independent adjuster documented the correct depreciation methodology based on the materials' actual age and condition, showing only 8% was applicable and recovering an additional $95,000 for the business owner.

- Nonprofit: Following a storm, a nonprofit warehouse in Salem found its insurer classified donated equipment as "used goods," applying a steep 50% depreciation. An adjuster fought this classification by documenting fair market value and replacement cost, ensuring the organization could replace its essential equipment without a major financial shortfall.

Securing a fair valuation is the most direct way to ensure your financial recovery. Understanding the strategies involved is vital, as detailed in guides that explain how to maximize your insurance claim payout by challenging lowball offers and documenting your true costs.

Key Takeaway: An independent, meticulously documented damage valuation is your evidence-based argument for a fair settlement. It transforms the claim from the insurer's estimate into a factual negotiation based on real-world costs.

Actionable Tips for Implementation

To ensure you receive a fair valuation for your property damage claim, adopt these methodical practices:

- Obtain Multiple Contractor Estimates: Get detailed bids from at least two to three licensed, insured contractors to establish a clear market rate for repairs in your area.

- Demand Detailed Proposals: Do not accept summary figures. Ensure all estimates are itemized, breaking down the scope, materials, labor costs, and project timeline.

- Document Required Code Upgrades: If local building codes in Oregon or Washington require upgrades during repair (e.g., new electrical or plumbing standards), these are legitimate additions to your claim.

- Photograph Extensively: Before any cleanup or repairs begin, take photos of the damage from multiple angles and distances to show its severity and full extent.

- Record All Mitigation Costs: Keep every receipt for emergency services like water extraction, board-ups, or mold prevention. These are part of your overall claim.

5. Claim Negotiation and Settlement Strategy

The final and most critical of the 5 risk management steps is developing a claim negotiation and settlement strategy. This step transitions from preparation to active engagement, transforming all your prior documentation and policy analysis into a compelling case for a fair payout. It involves sophisticated communication, data-driven arguments, and strategic leverage to counter insurer tactics and maximize your settlement. Public adjusters, operating exclusively for policyholders, are central to this stage, fundamentally shifting the power dynamic in your favor.

After a loss, the insurance carrier’s goal is to minimize their financial exposure. A professional negotiation strategy, however, ensures your claim is paid based on the full extent of your policy and the true cost of your damages. This process requires an expert understanding of insurance regulations, legal precedents, and valuation methods, which is why bringing in a public adjuster is often essential for achieving an optimal outcome.

Practical Examples of Settlement Strategy

- Residential: After a fire, a Portland insurer offered a homeowner an initial settlement of $80,000. By presenting comprehensive valuation documentation and citing specific Oregon insurance regulations, a public adjuster from NW Claims Management successfully renegotiated the claim, resulting in a final settlement of $165,000.

- Commercial: An insurer denied a roof damage claim for a commercial property in Washington, citing a 'wear and tear' exclusion. The policyholder's public adjuster countered with a detailed report documenting that the damage was from a specific, sudden storm event, not gradual deterioration. This distinction, supported by Washington court precedents, forced the insurer to approve the claim.

- Nonprofit: A nonprofit organization's claim included valuable donated equipment. The insurer questioned the valuation. The organization's adjuster provided comparable sales data and official charitable organization guidelines for valuing donated goods, establishing a fair market value and recovering the full amount claimed.

Effective negotiation is a specialized skill. For those facing this challenging process, understanding the fundamentals of negotiating with your insurance company can provide the confidence and knowledge needed to advocate for a just settlement.

Key Takeaway: Never assume an initial insurance settlement offer is final or fair. Professional negotiation, backed by solid evidence and regulatory knowledge, is often the only way to secure the full compensation you are entitled to under your policy.

Actionable Tips for Implementation

To build a strong negotiation and settlement strategy, follow these expert-backed tips:

- Never Accept the First Offer: Initial offers from insurers average just 40-50% of a claim's actual value. Always treat it as a starting point for negotiation, not a final number.

- Demand Written Explanations: If your claim is denied or only partially covered, request a specific, written explanation from the insurer citing the exact policy language they are using to justify their decision.

- Document All Communications: Keep a detailed log of every phone call, email, and meeting with insurer representatives. Note the date, time, who you spoke with, and what was discussed. This creates an evidence trail for potential disputes.

- Cite State Regulations: If an insurer is causing unreasonable delays, cite Oregon Statute 746.097 or Washington RCW 48.30.020 regarding prompt payment obligations to hold them accountable.

- Consider Third-Party Mechanisms: If you reach a stalemate on valuation, your policy likely allows for third-party mediation or appraisal. These processes can break a deadlock and lead to a fair resolution.

5-Step Risk Management Comparison

| Item | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes ⭐📊 | Ideal Use Cases 💡 | Key Advantages ⭐ | Typical Speed ⚡ |

|---|---|---|---|---|---|---|

| Risk Identification and Assessment | Moderate — systematic inspections and expert analysis | Inspector/adjuster time, photo/video tools, periodic updates | Baseline risk inventory; fewer undocumented pre-existing conditions | Pre-loss planning, high wildfire/flood exposure, large properties | Prevents claim denials; enables targeted mitigation | Periodic (annual) — can be time-consuming for large sites |

| Documentation and Evidence Preservation | High — immediate, detailed forensic recording required | Photo/video equipment, forensic adjuster, contractor estimates, secure backups | Well-substantiated claims; stronger settlement and legal defensibility | Immediate post-loss, disputed valuations, business-interruption claims | Irrefutable evidence; speeds processing; supports litigation | Urgent — time-sensitive and requires prompt action |

| Policy Analysis and Coverage Optimization | High — clause-by-clause review and regulatory interpretation | Experienced public adjuster, full policy/rider copies, research time | Identification of overlooked coverages; maximized contractual recovery | Complex or multi-policy situations; ambiguous exclusions | Recovers higher payouts; prevents wrongful denials | Medium — detailed review may take days to weeks |

| Damage Valuation and Loss Estimation | High — forensic cost analysis and scope development | Licensed contractors, cost databases (RSMeans), adjuster expertise | Accurate replacement/ACV valuations; counters lowball estimates | Structural damage, catastrophic losses, depreciation disputes | Ensures full restoration funding; credible scope of work | Moderate — depends on contractor availability and market data |

| Claim Negotiation and Settlement Strategy | High — tactical negotiation and possible escalation | Senior adjuster/negotiator, complete documentation, legal support as needed | Larger settlements; regulatory leverage; documented dispute trail | Insurer denials, low offers, complex or high-value claims | Significantly improves outcomes; reduces policyholder burden | Variable — can be prolonged if insurer resists or escalation needed |

Your Strongest Advocate in the Claims Process

Mastering the framework we've detailed is the first step toward transforming your approach to property protection. These 5 risk management steps are not merely a checklist; they represent a fundamental shift from a reactive stance to a proactive strategy. By moving from simple risk awareness to deep, actionable preparation, you build a powerful defense against potential financial devastation.

This comprehensive process, from meticulous risk identification to strategic settlement negotiation, equips you with the knowledge and tools to face a property loss with a degree of control. You understand the importance of documenting everything, analyzing your policy with a critical eye, and accurately valuing your damages. This preparation alone places you miles ahead of the average property owner who often enters a claim situation unprepared and overwhelmed.

From Theory to Reality: The Aftermath of a Loss

While understanding these principles is crucial, executing them under the immense pressure of a real-world disaster is a different challenge entirely. The period following a fire, flood, or major storm is chaotic and emotionally draining. You are simultaneously trying to secure your property, care for your family or business, and begin the long road to recovery.

This is precisely when your insurance company, backed by a team of adjusters, lawyers, and experts, begins its own process. Their primary objective is to evaluate the claim based on their interpretation of the policy and their assessment of the damage, which often serves their financial interests by minimizing the payout.

Key Insight: The insurance claim process is inherently adversarial. Your insurer's team is trained to protect their company's bottom line. Without an expert of your own, you are at a significant disadvantage, no matter how well you've prepared.

This is where the theoretical knowledge of risk management meets the practical need for professional advocacy. Managing a complex claim requires a specific skill set: deep policy expertise, forensic documentation abilities, and tenacious negotiation tactics. Attempting to handle this alone while dealing with personal and professional upheaval can lead to critical errors, missed deadlines, and ultimately, a settlement that falls far short of what you are rightfully owed. A licensed public adjuster exists to level this unbalanced playing field. They work exclusively for you, the policyholder, to manage every facet of your claim and fight for your maximum possible recovery.

Firms specializing in this field, particularly those with deep roots in the Pacific Northwest, understand the specific challenges property owners in Oregon and Washington face. They act as your dedicated project manager, your policy interpreter, and your unwavering negotiator, lifting the administrative and emotional weight from your shoulders. They ensure every 'i' is dotted and every 't' is crossed, from the initial damage assessment to the final settlement check. Embracing the 5 risk management steps is your best defense, and partnering with a public adjuster is your strongest offense.

Don't navigate the complex claims process alone. The experts at NW Claims Management apply these risk management principles on your behalf, managing your entire claim to secure the full, fair settlement you deserve. Protect your investment and your future by contacting NW Claims Management for a consultation today.