You come home to a soaked bedroom ceiling, a broken window, or a front door that no longer locks because someone forced it open. Your landlord is calling contractors. Your insurer wants a claim number started. You're staring at damaged clothes, electronics, and paperwork, trying to decide what to touch first.

That's where the renters insurance claim process usually goes wrong. Not because the loss isn't real, but because the first decisions are rushed, undocumented, or based on bad assumptions. A renter thinks, “I'll clean up first and deal with insurance later.” An adjuster then asks for proof that no longer exists.

As a public adjuster, I've seen the same pattern over and over. The people who recover best aren't always the most organized before the loss. They're the ones who get disciplined fast, document everything, and stop treating the claim like a casual customer service issue. It's a legal and financial file now. Handle it that way.

Your First 24 Hours After a Property Loss

The first day is about control. You do not need to solve the whole claim. You need to protect yourself, protect the property from further damage, and preserve evidence.

Start with safety and habitability

If there's fire residue, active leaking, structural instability, exposed wiring, or suspected mold growth, get out first and sort coverage second. If the unit isn't safe, don't stay there just because you're worried about reimbursement.

Then notify your landlord in writing. A text is fine if that's the fastest option, but follow it with email so there's a timestamped record. Keep it factual. State what happened, when you discovered it, whether emergency repairs are needed, and whether the unit is habitable.

If water is involved, move quickly to limit additional damage. Basic mitigation matters. Shut off water if you can do so safely, move salvageable items, and photograph every step before and after. For renters dealing with water intrusion or mold concerns, EZ Plumbing's LA remediation guide is a useful plain-language reference on what emergency remediation looks like.

Practical rule: Don't throw away damaged property in the first 24 hours unless it creates a health or safety hazard. If you must discard something, photograph it thoroughly first.

Report the loss without overexplaining it

Call your insurer as soon as you've stabilized the scene. Standard renters policies generally cover personal property, loss of use, and personal liability, and claims usually begin with fast notice followed by photos, receipts, inventories, and a detailed event description, as outlined in this renters claim overview from State Farm.

When you make that first report, say what you know. Don't guess about cause. Don't speculate about hidden damage. Don't volunteer opinions like “it was probably my fault” or “nothing major was ruined.”

Use language like this:

- Good first report: “I discovered water damage in the bedroom and closet this morning. I've notified the landlord, taken photos, and need to open a claim.”

- Bad first report: “I think the pipe may have been leaking for weeks and maybe some of my stuff is okay, but a lot is probably ruined.”

The difference is simple. The first version reports facts. The second creates avoidable issues.

Protect your living situation and your paper trail

If the unit can't be lived in, ask immediately about temporary housing or additional living expense handling. Don't wait until you've already spent money blindly. Keep every receipt tied to displacement. If you need a starting point for emergency accommodations and support planning, use this temporary housing directory.

The financial stakes are real. About 55% of U.S. renters have renters insurance, leaving 45% uninsured, and typical covered renters claims are summarized at about $3,000 to $5,000 for everyday losses and over $13,000 when major fire and water losses are included, according to RentRedi's renters insurance trend report. That's why the first day matters so much. A claim of this size shouldn't be handled from memory and hope.

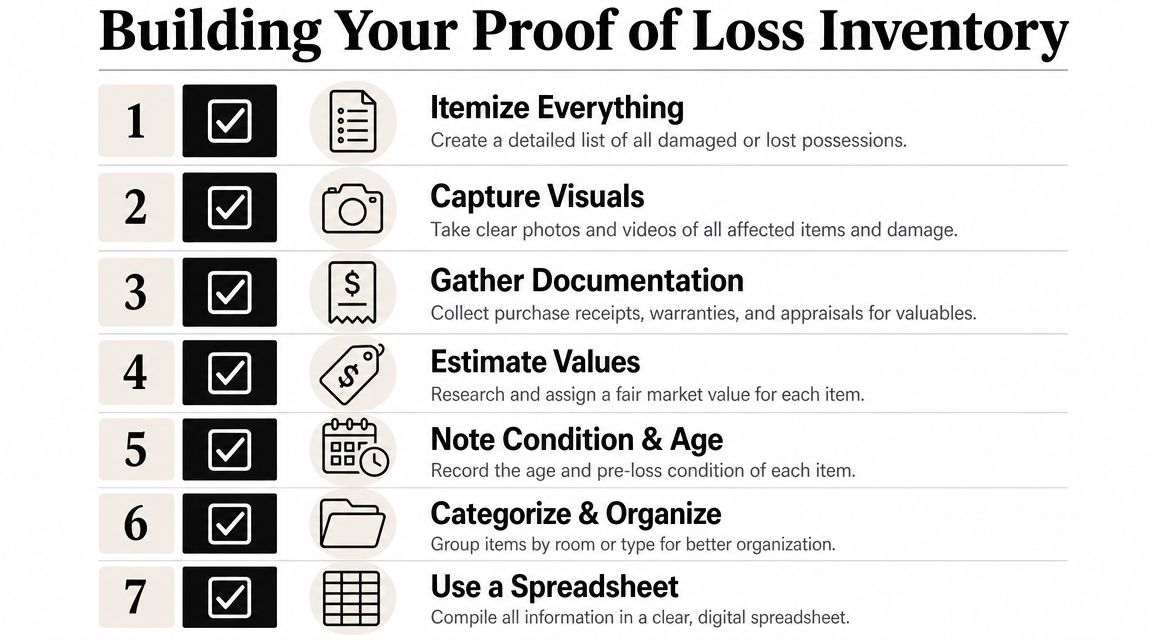

Building Your Proof of Loss Inventory

A renter after a fire or water loss usually remembers the big-ticket items first: the TV, the laptop, the couch. The money often slips away in the ordinary items that filled the unit every day. Carriers do not pay from memory. They pay from what you can identify, describe, and support.

Build the list room by room

Start with location, not price.

As a public adjuster, I tell renters to walk the unit in the same order every time and inventory by room: bedroom, hall closet, bathroom, kitchen, living room, entry, patio, storage area. That method does two things. It cuts down missed items, and it gives the adjuster a file that can be reviewed without guesswork.

Your spreadsheet should include these columns:

| Field | Why it matters |

|---|---|

| Room | Shows where the item was located |

| Item description | Identifies what was lost |

| Brand | Helps support quality and price range |

| Model number | Reduces disputes over replacement |

| Approximate age | Affects valuation |

| Purchase price | Supports claimed value |

| Place of purchase | Helps verify existence and quality |

| Condition before loss | Counters claims of pre-existing damage |

| Damage description | Ties item to the event |

| Replacement link or current equivalent | Supports current cost |

If you do not know every model number, do not stall the whole inventory. List what you know now, then add detail as you recover photos, receipts, order histories, and account records. In Oregon and Washington, that discipline matters. Carriers can ask for proof of ownership and value, but they still have to evaluate the claim in good faith and explain what information they need. A vague list invites a vague payment.

Don't forget the items people always miss

Large furniture gets attention first. Daily-use property usually does not.

Renters often lose money at this stage. Kitchen tools, pantry contents, socks, bedding, toiletries, cords, lamps, cosmetics, cleaning supplies, laundry items, school materials, and basic décor add up fast. After smoke, water, or sewage exposure, these smaller items are often unsalvageable even though they do not look dramatic in a photo.

Use this checklist as you go:

- Closets first: Clothing, shoes, luggage, hangers, bins, linens

- Then kitchen: Plates, glasses, cookware, utensils, small appliances, food

- Then electronics: Laptops, tablets, routers, headphones, chargers, speakers

- Then personal care: Hair tools, skin care, medications, razors, electric toothbrushes

- Then paper items: Books, notebooks, files, documents, specialty materials

If only the obvious items make it onto the list, only the obvious items get priced.

One practical warning. Do not write off soft goods too early, and do not assume the carrier gets to write them off either. Smoke odor, contaminated water, and microbial growth claims often turn on whether an item can be cleaned economically and safely. Ask for the basis of any salvage decision.

Use video and secondary proof

A slow phone video helps more than renters expect. Open drawers, closets, and cabinets. Show tags, labels, and damaged surfaces. Say the item name out loud while filming so the footage is useful later when you are matching property to your spreadsheet.

Receipts help, but plenty of valid claims are paid without them. Support ownership and value with whatever reliable proof you have:

- Bank or card statements showing the purchase

- Order confirmations from online or retail stores

- Old photos or videos where the item appears in the background

- Gift records or messages if someone else bought the item

- Product registration emails for electronics and appliances

- User manuals, boxes, or warranty records kept in a drawer or cloud folder

Valuation is where many renters get surprised. A covered item is not always paid at full new replacement cost on the first check. If you need a clear explanation before you submit your numbers, review how replacement cost works in renters insurance claims. That issue drives a lot of disputes, especially when the carrier pays actual cash value first and holds back the rest until replacement is completed.

Make the file easy to audit

Adjusters review large claim volumes. A disorganized inventory slows payment and gives the carrier room to question what should have been straightforward.

Create one master folder with subfolders by room. Name files so a stranger can understand them in five seconds, such as “Bedroom dresser photo 1,” “Kitchen blender receipt,” or “Living room TV model label.” Export the inventory to PDF before sending it, and keep the editable spreadsheet on your side so you can update it without losing the version you already submitted.

For larger losses, ask whether the carrier will accept staged submissions. That is often the better play. A clean first batch establishes credibility, starts the review process, and lets you keep building the remainder without turning the whole claim into a delayed pile of loose notes.

Filing the Claim and Managing Communications

A claim can be valid and still go sideways because communication wasn't controlled. The insurer's file becomes the official version of events unless you actively build your own.

Open the claim like you expect it to be reviewed later

You can file by phone, app, online portal, or email, depending on the carrier. The method matters less than the discipline. Before you file, gather the basics in one note:

- Policy information if you have it

- Date and time discovered

- Address of loss

- Short event description

- Emergency steps taken

- Police report information if theft or vandalism is involved

- Landlord contact information if repairs are underway

Then ask for three things immediately: the claim number, the assigned adjuster's name, and a full copy of the policy with endorsements. Policyholders should request a full copy of the policy and endorsements to verify what is payable and use a claim journal and written requests to reduce delays and preserve entitlement to additional living expenses, according to Boyd Insurance's claim guidance.

Keep a claim journal from day one

Most renters think they'll remember. They won't. Claims create too many calls, voicemails, portal messages, and conflicting instructions.

Your claim journal should track:

| Date | Person | Role | What was said | What you sent | Next step |

|---|---|---|---|---|---|

Keep it simple. A Notes app log, spreadsheet, or paper notebook is fine. What matters is consistency.

Write follow-up emails after phone calls. “Thank you for speaking with me today. My understanding is that you requested X, I provided Y, and the next step is Z.” That email can save you later if the file suddenly says something different.

Use firm, neutral language

Good claims communication is boring on purpose. You are not trying to persuade with emotion. You are creating a usable record.

A solid first email looks like this:

Following up on claim number [insert number]. The loss was discovered on [date]. I have attached initial photos and a preliminary inventory. Please confirm receipt and advise any additional documents required at this stage.

That tone works because it's factual and hard to distort.

If your claim includes displacement, continue documenting housing and support needs in writing. For renters dealing with the medical, logistical, or family impact of displacement, telephonic case management support can be one practical layer in the broader recovery process.

Navigating Your Meeting with the Insurance Adjuster

The adjuster is important, but don't confuse importance with alignment. The insurance company's adjuster works the insurer's file. Your job is to make that file harder to undervalue.

Know who's in front of you

There are usually three kinds of adjusters involved in property claims:

| Type | Who they work for | What to expect |

|---|---|---|

| Staff adjuster | Insurance company | Handles claims directly for the carrier |

| Independent adjuster | Contracted by insurer | Investigates on the carrier's behalf |

| Public adjuster | Policyholder | Documents and negotiates for the insured |

That distinction matters because renters often assume “the adjuster saw it, so it's covered.” Not necessarily. The broader claims environment involves standard adjuster scrutiny and loss verification. In homeowners data cited by the Insurance Information Institute, 97.3% of claims were for property damage, and renters enter a similar process focused on proving loss under policy rules, as summarized by the Insurance Information Institute.

Prepare the inspection like a file review

Don't wait for the adjuster to tell you how the meeting will go. Prepare the scene.

Before the visit:

- Group damaged items by category if possible

- Leave visible evidence in place unless safety requires removal

- Print or email your preliminary inventory

- Have receipts and photos accessible

- List questions in advance so you don't forget them

During the walkthrough, lead with facts. “These items were in the bedroom closet below the leak.” “This dresser was swollen after the water event.” “These clothes retained smoke odor after the fire.” Keep the conversation tied to observable damage and documented ownership.

Don't do these things:

- Don't guess about origin if you don't know

- Don't minimize damage because you feel awkward

- Don't exaggerate to make a point

- Don't let the adjuster rush past categories like textiles, pantry items, or storage bins

The adjuster's first pass is rarely the final word. It's an initial capture. If you miss items there, you'll spend the rest of the claim trying to put them back into the file.

Ask better questions

Weak question: “So, am I covered?”

Better questions:

- What additional documents do you need to evaluate personal property?

- Are you valuing this on actual cash value, replacement cost, or both under the policy?

- Do you need a revised inventory in a specific format?

- What is your timeline for issuing the first estimate or contents evaluation?

If you want a plain-language explanation of how insurer-side adjusters operate, this overview of claims adjuster duties is helpful. It clarifies why inspection notes, valuation decisions, and documentation requests carry so much weight.

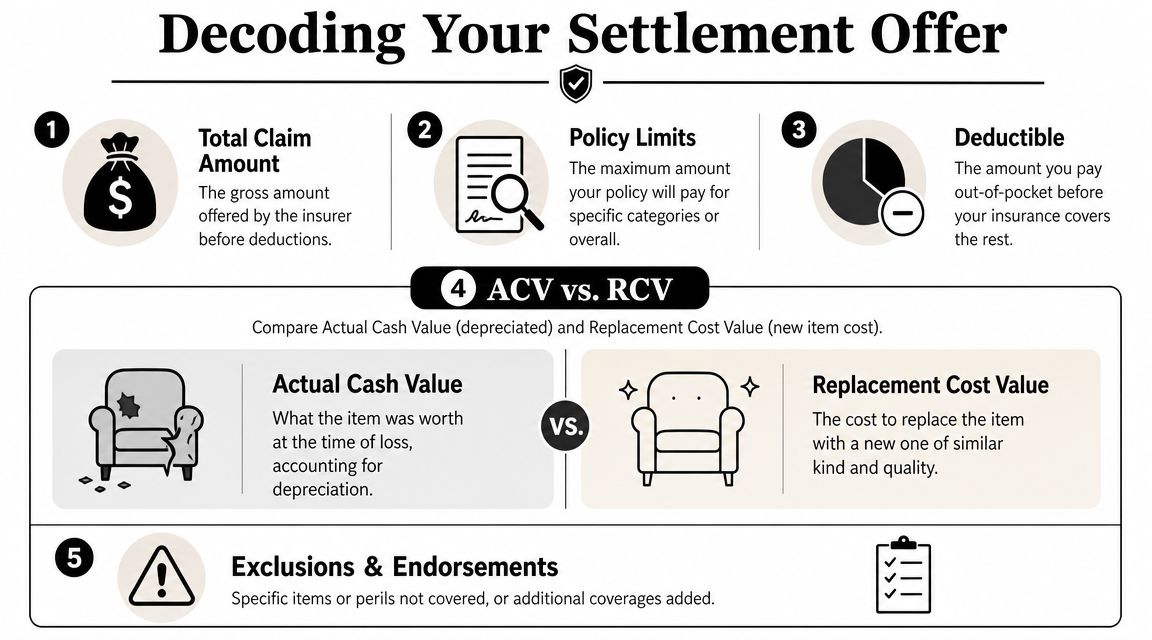

Decoding Your Settlement Offer and Payout

The settlement sheet is where many renters finally realize the claim isn't just about proving they owned something. It's also about how the insurer values it.

Read the settlement line by line

Don't look only at the total. Read every category.

A typical offer may include:

| Line item | What it usually means |

|---|---|

| Claimed item | What you reported |

| Quantity | How many units the insurer recognized |

| Replacement figure | What the carrier says a comparable item costs |

| Depreciation | Amount subtracted for age or condition |

| Actual cash value | Value after depreciation |

| Deductible | Your out-of-pocket share under the policy |

| Net payment | What's being paid now |

If something looks off, ask for the worksheet behind the worksheet. You're entitled to understand how the carrier reached the number.

ACV and RCV change the outcome

This is the most common surprise in the renters insurance claim process. Renters often discover after filing that payout depends heavily on the difference between actual cash value and replacement cost. Insurers may pay the lesser of the two, and incomplete documentation is a major reason payments get reduced, as explained in Lemonade's renters claim explainer.

Here's the practical version.

If you lost a five-year-old laptop, the insurer may agree you owned a laptop and still pay less than what a new one costs today. Why? Because under an ACV approach, the carrier applies depreciation for age and condition. Under replacement cost coverage, you may still need to prove what comparable new item replaces it, and some policies pay in stages.

That's why “I had a laptop” is weak evidence. “I had a Dell XPS with this configuration, bought from this retailer, and here's the old order email” is much stronger.

Proving value is just as important as proving ownership.

Watch the hidden pressure points

Low settlements often come from the same places:

- Generic item descriptions such as “TV” instead of a specific make and model

- Unchallenged depreciation where age or condition assumptions are too harsh

- Missed sub-limits for categories like jewelry or certain electronics

- Deductible confusion where the renter expected a higher net payment

- Incomplete loss of use documentation for hotel, meals, laundry, parking, or pet costs tied to displacement

If you need a side-by-side explanation before responding to an offer, this guide to actual cash value vs replacement cost is useful.

Additional living expenses need their own file

If your rental became uninhabitable, don't mix displacement costs into your general contents folder. Create a separate ALE folder with receipts, confirmations, and a simple ledger.

Track items such as:

- Temporary lodging

- Meal overages above your normal spending

- Laundry

- Transportation changes

- Pet boarding or related costs if tied to displacement

The insurer won't usually build this for you. You have to show what you spent, why you spent it, and how it connects to the covered loss.

How to Dispute a Denied or Lowball Claim

You open the carrier's letter expecting a check for the loss, and instead you see a denial, missing items, or a number that does not come close. That is the point where many renters hurt their own case by firing off an angry email or giving up too early. A better response is to slow down, isolate the dispute, and build a written record the carrier has to answer.

Start with the reason, not the frustration

Get the denial or low settlement explained in writing if it is not already. Then read the exact policy language the carrier is relying on. I tell clients to mark up both documents line by line. One side is what the insurer says happened. The other is what the policy says.

Your dispute letter should be tight and specific:

- State what is wrong. Denied coverage, omitted items, overstated depreciation, underpaid ALE, or unsupported pricing.

- Match each point to proof. Receipts, photos, videos, bank records, old order confirmations, landlord notices, or replacement pricing.

- Ask for a defined correction. Reopen coverage, revise item values, include named items, or issue supplemental payment.

That letter does not need drama. It needs a paper trail. If the company says your sofa was worth far less than claimed, ask what age, condition, and source they used. If they denied part of the claim for lack of proof, resend the proof with labels that are impossible to miss.

Escalate in an order that makes sense

Start with the assigned adjuster. If the response is vague or delayed, ask for a supervisor review in writing. If the file keeps stalling, ask for the claim notes, the valuation basis, and confirmation of what documents are still being requested.

Oregon and Washington renters have a practical advantage here. Insurers and public adjusters are regulated at the state level, and claim handling has to follow state insurance rules. That does not hand you a win, but it does give you a framework. Dates matter. Written requests matter. Unsupported conclusions matter. Keep your communication organized enough that a supervisor, regulator, or outside representative can understand the dispute in ten minutes.

One more point that gets overlooked. If your dispute involves property damaged during relocation after the loss, review any third-party transit or move-related protection separately. It helps to understand how to protect your belongings during a move so you do not mix one claim issue into another.

Know when to bring in outside help

Some disputes are manageable on your own. Others stop being worth your time. If the inventory is long, the apartment had major damage, the carrier is slicing values down item by item, or coverage questions are getting technical, outside help can change the result.

A public adjuster represents the policyholder, not the insurance company. The job is straightforward. Read the policy closely, rebuild the loss presentation, challenge bad valuation, and negotiate from documented facts. In Oregon and Washington, use someone licensed for that state and ask direct questions about fee structure, scope of work, and who will handle your file.

NW Claims Management is one firm that handles renter claims in Oregon and Washington. Whether you hire that office or another licensed public adjuster, the standard is the same. You want someone who can explain the denial in plain English, show where the numbers are wrong, and press the insurer for a corrected payment instead of accepting a thin offer as final.

Frequently Asked Questions on Renters Claims

How long does a renters claim take

There isn't one universal timeline. A straightforward theft claim with clean documentation can move much faster than a water loss involving habitability, cleanup, landlord repairs, and a long contents list. What controls speed is usually documentation quality, adjuster workload, and whether the insurer keeps asking for missing information. The fastest way to slow a claim down is to submit incomplete material in multiple inconsistent batches.

Can I file if the damage was partly my fault

Often, yes. If you overflowed a tub or left something running, that doesn't automatically end the claim. What matters is the policy language, the cause of loss, and whether the event fits within coverage rather than an exclusion. Report the facts exactly as they happened. Don't try to rewrite the story to sound better.

If my landlord caused the damage, whose insurance do I use

Usually start with your own renters policy for your personal property and displacement issues, then let the insurers sort out responsibility afterward if needed. Your landlord's policy generally addresses the building, not your belongings. You still need to protect your own claim promptly.

A related point gets missed during moves and temporary relocations. If you're packing up after a loss, it helps to understand how to protect your belongings during a move so you don't create a second documentation problem while the first claim is still open.

If you're in Oregon or Washington and the renters insurance claim process is turning into a fight over valuation, documentation, or delayed responses, NW Claims Management can review the file and help you understand your options. A strong claim starts with evidence, but a fair outcome usually depends on how that evidence is organized, presented, and defended.