It really boils down to one simple question: does your business deal more with physical actions or professional advice?

Public liability insurance is your shield against claims of physical harm—think third-party injuries or property damage happening on your watch. On the other hand, professional indemnity insurance steps in to cover financial losses that a client suffers because of your advice or services. The right choice hinges on whether your biggest risks come from your physical operations or your professional expertise.

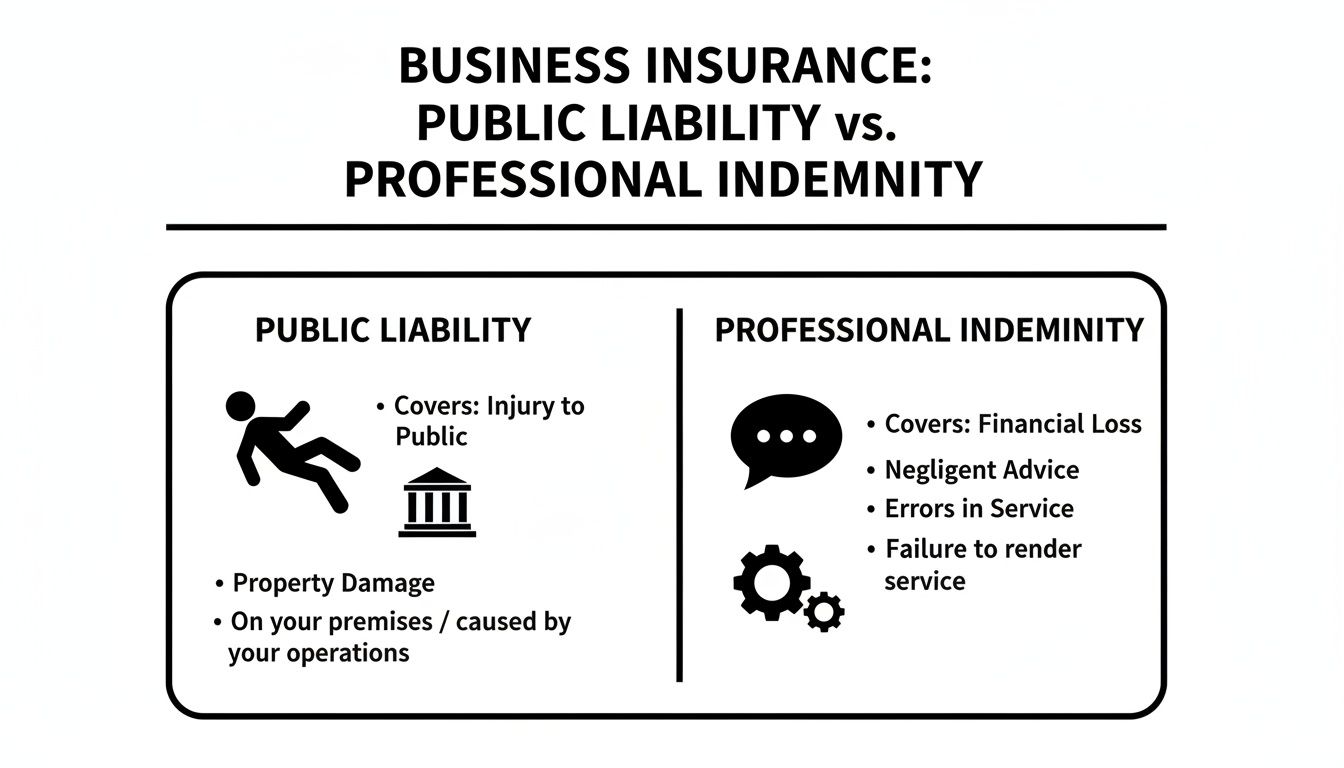

Understanding the Core Differences

Trying to sort out business insurance can feel like untangling a knotted rope, but getting a firm grasp on public liability versus professional indemnity is essential. These two policies cover completely different kinds of risks, and for many businesses in Oregon and Washington, having both is non-negotiable for operating with peace of mind.

I often tell clients to think of it this way: a general contractor’s world is filled with physical risk. A visitor could trip over a tool on a job site, or a crew could accidentally damage a neighboring building. That’s a classic scenario for public liability. Now, consider a financial advisor. Their greatest risk isn’t physical; it's giving advice that costs a client their savings. That's where professional indemnity is crucial.

Quick Comparison Public Liability vs Professional Indemnity

To make it even clearer, let's look at their core functions side-by-side. This table breaks down what each policy is designed for, who it protects, and what kind of event kicks off a claim.

| Coverage Aspect | Public Liability Insurance | Professional Indemnity Insurance |

|---|---|---|

| Primary Purpose | Covers claims for third-party bodily injury or property damage. | Covers claims for financial loss due to negligent services or advice. |

| Claim Trigger | A physical event (e.g., slip and fall, fire, water damage). | A professional error or omission (e.g., bad advice, design flaw, miscalculation). |

| Who is Protected | Your business from claims made by the general public (clients, vendors, visitors). | Your business from claims made by clients alleging a professional mistake. |

Ultimately, one policy covers what you do, and the other covers what you know.

Interestingly, we're in a market where increased competition among insurers has led to some premium drops for both policy types. While that’s welcome news for business owners, the underlying pressures driving claims haven't gone away. It's a reminder that getting the right settlement is just as important as having the right coverage. In fact, a recent insurance market report from Gallagher highlights that claims managed without professional representation historically settle for 40% less.

A Side-by-Side Comparison of Policy Coverage

To get a real handle on the difference between public liability and professional indemnity insurance, you have to look past the definitions. The true distinction becomes clear when a claim actually happens. Think of them as two completely different tools in your toolbox—grab the wrong one, and you could be facing a massive, uninsured loss.

At its core, the difference is all about the type of harm each policy covers.

Public liability is all about the physical world. It steps in when your business activities lead to bodily injury or property damage to someone else. This is your classic "slip and fall" coverage. It also covers things like one of your employees accidentally knocking over and breaking a client’s expensive server during a site visit.

Professional indemnity, on the other hand, deals with financial harm caused by your professional services. This policy protects you when a client claims your advice or work caused them to lose money. It's the coverage that kicks in when a client sues you because of a mistake in a report, a flaw in your design, or bad advice that led them down a costly path.

Claim Triggers: Physical Mishaps vs. Financial Errors

The clearest way to see the divide is by looking at what triggers a claim. One is for a tangible accident; the other is for an error in your professional judgment.

- Public Liability Trigger: A physical incident causing injury or damage. For example, a customer at your Portland coffee shop trips on an extension cord and breaks their wrist. Their claim for medical bills would trigger your public liability policy.

- Professional Indemnity Trigger: A professional mistake causing a client's financial loss. For example, a Seattle-based architect's blueprints have a calculation error. The mistake isn't caught until construction is underway, forcing the client to pay for expensive tear-down and rework. Their lawsuit to recover those costs would trigger your professional indemnity policy.

This infographic breaks down the primary focus of each coverage type.

As you can see, public liability is built to handle accidents that affect people and their property. Professional indemnity is all about the financial fallout from the work you produce.

Scope of Coverage: Bodily Injury vs. Errors and Omissions

What each policy actually pays for is also fundamentally different. A public liability policy is designed to cover concrete costs like medical bills, hospital stays, and the price to repair or replace damaged property.

A professional indemnity policy covers economic damages that are often much less straightforward. It covers the client's direct financial losses, but just as importantly, it also covers your own legal defense costs, which can become enormous even if you're eventually cleared of any wrongdoing.

It's no surprise that the need for this kind of protection is on the rise. In 2024, the global property and casualty insurance sector—which includes public liability—saw premiums jump by 7.7%, reaching a staggering EUR 2,424 billion. This isn't just a number; it reflects a real-world increase in physical and legal risks businesses are facing. For property owners and service professionals in Oregon and Washington, these stats show why solid coverage isn't just nice to have—it's essential.

Getting this right is especially important when you learn more about how to set your insurance policy limits. The potential financial damage from one professional error can easily dwarf the cost of a minor physical accident. If you're carrying the wrong type of insurance, your business is dangerously exposed to risks you could have easily covered.

Real-World Claim Scenarios for Each Policy

Insurance policies can feel a bit theoretical until you see them in action. Let’s walk through a few concrete examples for businesses here in the Pacific Northwest to really highlight the difference between public liability and professional indemnity. When you see how these policies respond to actual incidents, their separate but equally vital roles become much clearer.

What you'll notice in each case is how the source of the problem—a physical accident versus a professional mistake—determines which policy kicks in. For any business owner in Oregon or Washington, understanding this distinction is the key to building a truly solid financial safety net.

For the General Contractor

A Portland-based general contractor is a perfect case study. They're constantly exposed to both physical hazards on a job site and the risk of professional mistakes in their project management. They absolutely need both types of coverage.

Public Liability Claim: A prospective tenant is touring an active renovation site to check on the progress. They don't see a misplaced power cord, trip, and end up with a severe ankle fracture that requires surgery. They sue the contractor for medical expenses and time off work. This is a classic bodily injury claim on the contractor's property, so their public liability insurance would step in to cover it.

Professional Indemnity Claim: Several months into the same project, a massive error comes to light. The contractor’s team misread the architectural blueprints and built a primary structural wall five feet from where it was supposed to be. Fixing it means expensive demolition and reconstruction, throwing the project off schedule and over budget. The building owner sues the contractor for the rework costs and the financial losses from the delay. This claim originates from a professional error, making it a job for the contractor's professional indemnity insurance.

For the Marketing Agency

Now let’s look at a digital marketing agency in Seattle. Their day-to-day risks are less about physical accidents and far more about the advice, strategies, and creative work they deliver to clients.

Public liability Claim: A client arrives at the agency’s downtown office for a big strategy meeting. The lobby floor was just mopped, but no one put out a "wet floor" sign. The client slips, and their brand-new laptop goes flying, smashing on the tile floor. They file a claim for the damaged property. The agency's public liability policy is designed for exactly this and would cover the cost of a replacement laptop.

Professional Indemnity Claim: The agency rolls out a huge advertising campaign for a new client. The problem? A competitor alleges the campaign’s main slogan is defamatory and infringes on their registered trademark. That competitor sues the agency’s client, who then turns around and sues the agency for negligence and the massive financial loss they’re now facing. This is a textbook professional indemnity claim.

For the Nonprofit Organization

Even nonprofits aren’t immune to these dual risks. A community center in Eugene, for instance, has to manage potential liability from both the events it hosts on its premises and the services it provides to the public.

Public Liability Claim: The center is hosting its annual fundraising gala when a poorly secured stage light suddenly falls, striking and injuring a guest. The guest needs medical treatment and holds the nonprofit liable for failing to maintain a safe environment. This claim for bodily injury is a clear-cut case for the organization’s public liability insurance.

Professional Indemnity Claim: As part of its community outreach, the nonprofit runs free financial literacy workshops. One of the volunteer counselors gives a participant incorrect advice on debt consolidation, which leads them to a decision that severely harms their financial standing. The participant sues the nonprofit for the financial damages resulting from that bad advice. This triggers the professional indemnity policy.

Seeing how different situations play out is a crucial part of navigating the property damage claim process. Each one of these scenarios shows why having only one of these policies can leave your business dangerously exposed.

Navigating Insurance in Oregon and Washington

While the basics of public liability and professional indemnity insurance apply everywhere, running a business in the Pacific Northwest is a different ballgame. The legal environments in Oregon and Washington are unique, with state-specific rules that dictate everything from coverage minimums to how claims unfold. This isn't just theory; it's a practical reality that requires local knowledge to stay protected.

A Portland contractor or a Seattle tech consultant, for instance, operates under a completely different set of risks than their peers in other states. The legal climate, especially in major metro areas, can be tough, often resulting in complex and expensive settlements. Understanding the ins and outs of navigating insurance in Washington or Oregon is a must for any policyholder and can make all the difference when a claim is filed.

State-Specific Requirements for Professionals

In the PNW, carrying certain insurance policies isn't just a good idea—it's often the law. For many professions, it's a prerequisite for keeping your license active.

Construction Contractors (Oregon & Washington): If you're a licensed contractor, both states require you to have liability insurance. The Oregon Construction Contractors Board (CCB) and the Washington State Department of Labor & Industries (L&I) set the minimums, which are in place to protect your clients from property damage or unfinished projects.

Architects and Engineers: While a state board might not always mandate it, you'll find that client contracts in the region’s booming tech and construction sectors almost always demand strong professional indemnity (E&O) coverage. Just imagine the fallout from a design flaw in a new Bellevue high-rise—it could easily trigger a multi-million dollar lawsuit.

The Impact of Local Laws and Industries

The Pacific Northwest's distinct economy and legal landscape directly shape your insurance needs. Think about our famously wet weather. All that rain dramatically increases the risk of "slip and fall" accidents, making public liability a critical shield for any business with a physical storefront.

What many PNW business owners don't realize is that local court precedents and state laws can completely change the outcome of a claim. A premises liability case in Oregon, which follows specific comparative negligence rules, might play out very differently than the same incident in Washington. That kind of legal nuance can make or break your defense.

And you can't talk about business here without mentioning the tech sector. From Portland's "Silicon Forest" to Seattle's global tech giants, professional indemnity insurance has become absolutely essential. For thousands of consultants, software developers, and digital agencies, the risk of causing a client financial harm from a data breach, coding error, or bad IT advice is a daily reality. When a major loss does happen, knowing when to hire a public adjuster is often the most critical decision you can make.

Choosing Your Policy Limits and Endorsements

Alright, you’ve decided you need insurance. That’s the easy part. The real work begins when you have to figure out how much coverage you actually need. Simply having a policy in your back pocket isn't enough; the real protection is found in the details—the limits and the endorsements that shape your coverage.

Your policy limit is the absolute maximum your insurer will pay out on a claim. Don't just pick a number that feels right. This decision needs to be a calculated one, based on a clear-eyed look at the real-world risks your business faces every day. A solo graphic designer working from home is playing a completely different ballgame than a commercial construction firm, and their insurance should absolutely reflect that.

Assessing Your Risk Profile

So, how do you land on the right number for your public liability and professional indemnity limits? It starts with putting your own business under the microscope. You and your broker can use this analysis to zero in on a coverage amount that truly matches your potential liabilities.

Ask yourself these questions:

- What industry am I in? A construction company faces a high probability of causing expensive property damage or bodily injury, so a high public liability limit is a must—often $2 million or even more. On the other hand, an IT consultant’s biggest threat is causing a client financial harm from a system failure, which calls for a strong professional indemnity policy.

- How big is my operation? More revenue, more employees, and bigger projects all equal greater exposure. It’s just a numbers game—the more you do, the more chances there are for something to go wrong, and the higher the potential settlement could be.

- What do my clients demand? It's common for corporate and government contracts to spell out the exact minimum insurance limits you need to carry. Showing up without the required coverage is a surefire way to lose out on a great project.

- Where do I do business? A retail shop in a busy downtown Portland storefront has a massive public liability risk compared to a business that operates entirely remotely. Every person walking through your door represents another opportunity for a slip-and-fall claim.

Thinking through these factors is a lot like the due diligence that goes into learning how to choose a general contractor; you have to assess the complexity and potential risks of the job to ensure everyone is properly protected.

Understanding Key Endorsements

Once you have your limits figured out, it's time to look at endorsements. Think of these as custom upgrades for your insurance policy. They add back coverage for specific risks that a standard, off-the-shelf policy might exclude.

An endorsement tailors a generic policy to your specific operations. Without the right ones, you might believe you're covered for a risk that is actually excluded in the fine print.

Here are a few of the most common endorsements and why they matter:

- Products-Completed Operations Coverage: This is non-negotiable for contractors. It extends your public liability coverage to protect you from claims that pop up after you’ve packed up your tools and left the job site. Without it, you’re on the hook for any property damage or injury your finished work might cause down the road.

- Media Liability Endorsement: If you create content—as a marketer, consultant, or blogger—this is an essential add-on for your professional indemnity policy. It covers you for claims like libel, slander, copyright infringement, and invasion of privacy that can arise from the things you publish.

- Waiver of Subrogation: You'll see this requirement in a lot of client contracts. This endorsement essentially tells your insurance company that they can't go after your client to recoup their losses, even if the client was partly responsible for the incident that led to the claim.

How a Public Adjuster Maximizes Your Claim

When a major loss hits your business, you expect your insurance policy—whether it’s public liability insurance or professional indemnity—to come through for you. The reality, though, is that getting a fair settlement is rarely a simple process. This is precisely where a public adjuster becomes your most crucial ally.

You have to remember that the adjuster sent by your insurance carrier works for them. Their primary responsibility is to protect the insurer’s financial interests. A public adjuster, on the other hand, is a licensed professional who works exclusively for you, the policyholder.

Fighting for Your Best Interests

Think of it this way: your insurance company has a team of experts whose entire job is to interpret policy language to minimize payouts. A public adjuster’s role is to counter that by building an airtight case for the maximum recovery you're entitled to.

They accomplish this through a few key actions:

- Deep Policy Analysis: First, they comb through every line of your policy. They’re looking for all possible avenues of coverage, many of which are often overlooked by policyholders.

- Comprehensive Loss Documentation: They meticulously document the full extent of the damage. This goes beyond the obvious, including everything from hidden structural issues to lost business income.

- Expert Damage Valuation: A good public adjuster brings in their own network of trusted engineers, contractors, and forensic accountants. This team creates an independent and detailed estimate of what your claim is truly worth.

A public adjuster is your expert negotiator, fluent in the complex language of insurance claims. They manage the entire process, freeing you to focus on getting your business back on its feet while they fight to secure the settlement you deserve.

By handling all communications and presenting a claim backed by solid evidence, a public adjuster ensures your insurance company lives up to its end of the contract. You can find a more detailed breakdown of the benefits of hiring a public adjuster and see how they can champion your recovery.

For large or complex claims, having this expert representation is often the single most important factor in getting a fair and timely settlement.

Frequently Asked Questions

Even after a side-by-side comparison of public liability insurance and professional indemnity, a few questions always come up. Here are some of the most common things we hear from business owners across Oregon and Washington.

Can I Just Bundle These Two Policies Together?

Yes and no. Many insurance carriers offer something called a Business Owner's Policy (BOP), which is a great starting point. It conveniently bundles general liability (the most common type of public liability coverage) with commercial property insurance.

However, professional indemnity is almost always a separate, standalone policy. This is because it covers a completely different set of risks—financial loss from your advice or services, not physical injury or property damage. The good news is you can typically buy both policies from the same insurance provider, which helps keep your paperwork streamlined.

How Much Does This Insurance Cost for a Small Business in Oregon?

There's no one-size-fits-all answer for cost, as it really depends on your specific industry, annual revenue, and day-to-day risk exposure.

For example, a home-based marketing consultant might only pay a few hundred dollars a year for a basic professional indemnity policy. On the other hand, a small construction contractor in Portland could easily pay several thousand dollars for a solid public liability policy because the risk of someone getting hurt on-site is much higher. The best approach is always to get quotes tailored to your unique operations. Understanding how insurers calculate these prices can be tricky, and you can get a clearer picture by exploring what a public adjuster costs and the value they bring to the table.

Key takeaway: A crucial difference between these policies lies in when a claim is covered. "Occurrence" policies cover incidents that happen during the policy term, no matter when the claim is actually filed. "Claims-made" policies, which are standard for professional indemnity, only cover claims that are filed while the policy is active.

When you're facing a claim, trying to decipher your policy while managing a crisis is a battle you shouldn’t fight alone. The team at NW Claims Management works exclusively for you, the policyholder, to make sure you get the maximum settlement you're entitled to. Get your free claim evaluation today.