Industry benchmarks put the average insurance payout for hail damage car claims at about $4,300 to $5,000, and a widely cited benchmark puts it at about $5,000 per vehicle in 2021, up from $4,300 in 2020. That's a useful starting point, but it's only a starting point, because your actual settlement can land far below or far above that depending on your deductible, your vehicle's value, and how the damage is written up.

If you're reading this, there's a good chance you walked outside after a storm and saw the same ugly scene most drivers see. Dents across the hood, roof, and trunk. Maybe cracked glass. Maybe damage that looked minor at first, then got worse every time the light hit the panels from a different angle.

That's when the stress starts. You want one clean answer. What should the insurance company pay?

You should know the benchmark. You should also know that chasing the average alone is how people accept short settlements. A fair hail claim isn't based on some national number. It's based on the math of your policy, the repair method, and whether your car should be repaired or valued as a total loss.

For drivers in Oregon and Washington, that matters even more. Repair availability, shop backlog, and local labor conditions can affect how a claim moves and how hard you may need to push. The smart move is to treat the “average insurance payout for hail damage car” question as the entry point, not the final answer.

Your Car Was Hit by Hail What's a Fair Payout

You walk out after the storm, run your hand across the hood, and feel dent after dent. The first number the insurer offers can sound reasonable in that moment. That is when people get stuck with short money.

A fair payout is based on the actual cost to restore your vehicle under your policy, or the vehicle's actual cash value if the damage supports a total loss. Your job is to measure the loss correctly before you agree to anything.

That matters even more in Oregon and Washington. Shop schedules, local labor rates, parts availability, and how the carrier writes paintless dent repair versus conventional repair can all change the settlement. Two cars with similar-looking dents can produce very different outcomes on paper.

What a Fair Payout Includes

Start with the estimate. Read every line. Hail claims are often underpaid because the first write-up misses damaged trim, molding removal, glass, panel access, or the number of dents per panel.

Use this checklist to judge whether the offer is fair:

- Confirm the right coverage applies: Hail damage is usually paid under non-collision coverage for damage to your own vehicle. Liability-only coverage does not pay to fix your car.

- Match the repair method to the damage: Paintless dent repair works for some dents. It does not fit every panel, crease, or stretched-metal condition.

- Check for related damage: Windshields, side glass, moldings, roof rails, badges, and sensors can be part of the claim.

- Compare repair cost to vehicle value: If repair costs get too close to actual cash value, the carrier may shift from repair to total-loss valuation.

- Apply the deductible at the end: Many policyholders judge the claim by the gross estimate, then get surprised by the net payment.

One rule matters more than the rest. If you cannot explain how the estimate was built, you are not ready to accept the payout.

Do not let the insurance company be the only party documenting the loss. Take your own photos in angled light. Get a shop opinion. Keep every version of the estimate. If you need help reviewing valuation and damage documentation, this vehicle appraisal resource for auto claims is a solid starting point.

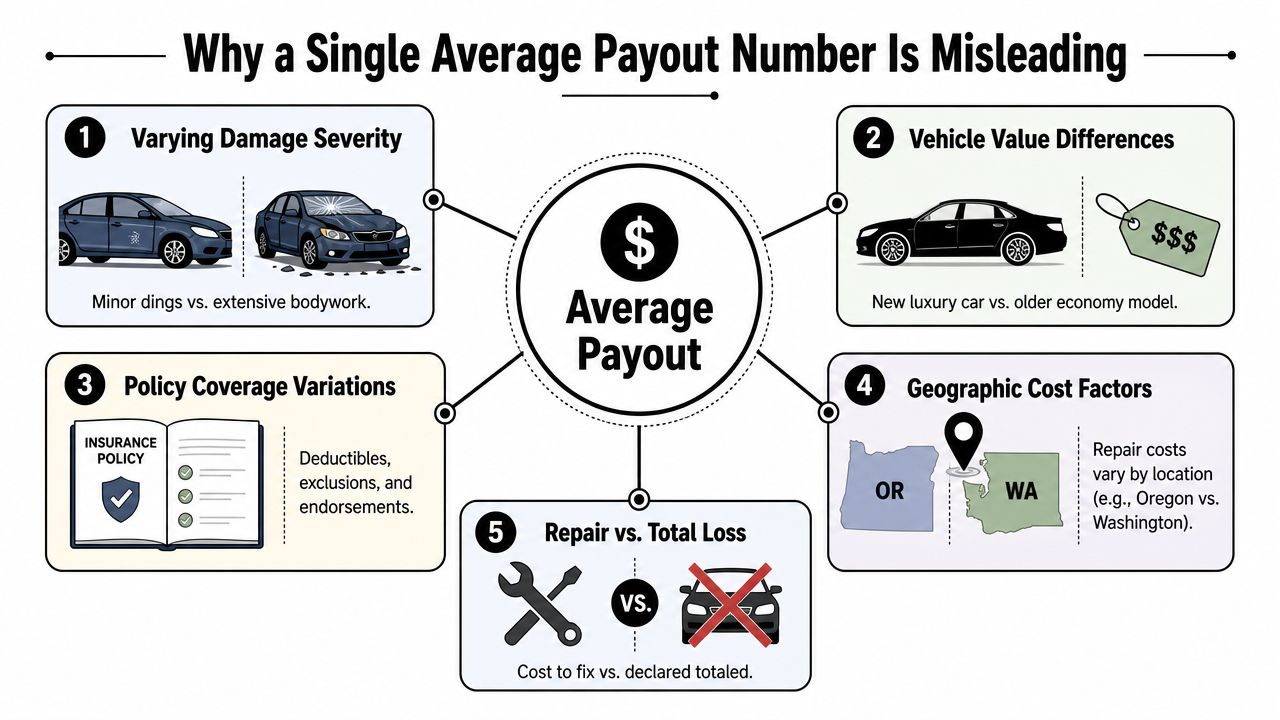

Why a Single Average Payout Number Is Misleading

Your insurer offers $2,100 for hail damage. Your neighbor says they got more than $5,000 on a similar claim. Both numbers can be real. Neither tells you what your car should be paid at.

A single average payout number creates false confidence. It pushes policyholders to judge the claim by a headline instead of by the actual damage, the repair method, local shop pricing, and the point where the carrier may stop calling it a repairable loss and start treating it as a total loss.

The average mixes claims that have nothing in common

A few shallow dents on a hood do not belong in the same mental bucket as a storm loss that hits the roof, hood, decklid, glass, trim, and sensors. Yet both end up inside the same average.

That creates two common mistakes:

- Policyholders anchor too high. They expect a large payment because they saw a national benchmark.

- Policyholders anchor too low. They accept a weak first estimate because it sounds plausible compared with a broad average.

Both mistakes cost money. Fair settlement value comes from your specific repair scope and policy terms.

Oregon and Washington make averages even less useful

This matters more in Oregon and Washington because hail claims do not move through one uniform market. Labor rates vary by metro area. Shop capacity changes after a storm. Parts access changes the repair plan. A vehicle in Portland, Salem, Vancouver, Spokane, or Yakima can produce a very different estimate even when the dents look similar in photos.

That is why I tell policyholders to stop asking, “What is the average payout?” Ask, “What should this car cost to restore in my market, under my policy, with this damage?”

The same problem shows up in property claims. If you want a parallel example, average hail roof payout ranges show how one broad number can hide major differences in scope, materials, and settlement approach.

The insurer's estimate is an opinion attached to a payment. Review it like one.

Use this framework instead

| Question | Weak way to judge the claim | Better way to judge the claim |

|---|---|---|

| What is my claim worth? | National average payout | Line-by-line repair scope for this vehicle |

| What will insurance pay? | A rough benchmark | Covered amount minus deductible |

| Could the car be totaled? | General payout chatter | Repair cost compared with actual cash value |

| Is the first offer fair? | It sounds close enough | It includes all necessary operations and damaged parts |

Keep the average in its place. It is a reference point, not a pricing tool, and definitely not a settlement promise.

Key Factors That Determine Your Hail Damage Settlement

Most hail settlements come down to four moving parts. Miss one of them, and you'll misread the entire claim.

The first is repair cost. The second is your deductible. The third is your vehicle's actual cash value, meaning what the car was worth just before the storm. The fourth is whether the insurer treats the loss as repairable or a total loss.

Repair scope drives the claim

Market guidance notes that moderate hail repairs commonly run around $2,500, while broader industry estimates put average payouts in the $4,300 to $5,000 range. Severe damage can push costs into the $10,000+ range and may total a vehicle, as explained in Liberty Mutual's hail-damage overview.

That spread tells you something important. A hail claim isn't one kind of repair. It can include:

- Paintless dent repair: Often the least invasive option when the metal can be worked without refinishing.

- Conventional body repair: Needed when dents are too sharp, too deep, or paint has been compromised.

- Glass and trim replacement: Windshield, side glass, moldings, lamps, and attached components may need separate line items.

- Panel replacement: Sometimes a hood or another panel costs less to replace than to chase dozens of dents.

Your deductible changes what you actually receive

Insurance doesn't pay the full estimate straight into your pocket just because damage exists. Your deductible comes off the covered amount. That means a lower-severity claim may be technically covered but still produce a small net payment, or none worth pursuing if the estimate sits near the deductible.

This is why people get confused. They hear average payout numbers, then see an insurer estimate that leaves them disappointed. The gross repair figure and the net insurance payment aren't the same thing.

Don't ask, “What's the estimate?” Ask, “What's the estimate after deductible, and does it include every damaged component?”

Actual cash value is where total-loss fights happen

If repairs become too expensive relative to the vehicle's value, the insurer may move toward a total-loss decision. Then the argument shifts. You're no longer debating dent count and labor operations alone. You're debating what the car was worth before the storm.

That's where people leave money on the table. They accept a low valuation because they don't challenge condition, options, comparable vehicles, recent maintenance, or prior market evidence.

If you need a clean explanation of how those valuation concepts differ, this guide to actual cash value versus replacement cost is worth reviewing.

The settlement formula is simple. The support behind it isn't

At a basic level, the math looks like this:

| Claim type | Basic formula |

|---|---|

| Repairable vehicle | Covered repair cost minus deductible |

| Total loss vehicle | Actual cash value minus deductible, subject to policy terms |

Simple formula. Messy execution.

The insurer can underestimate repair methods. A shop can find hidden damage later. The valuation can come in low. The adjuster can miss panel-specific work. That's why your best advantage isn't arguing emotionally. It's presenting better documentation than the insurer started with.

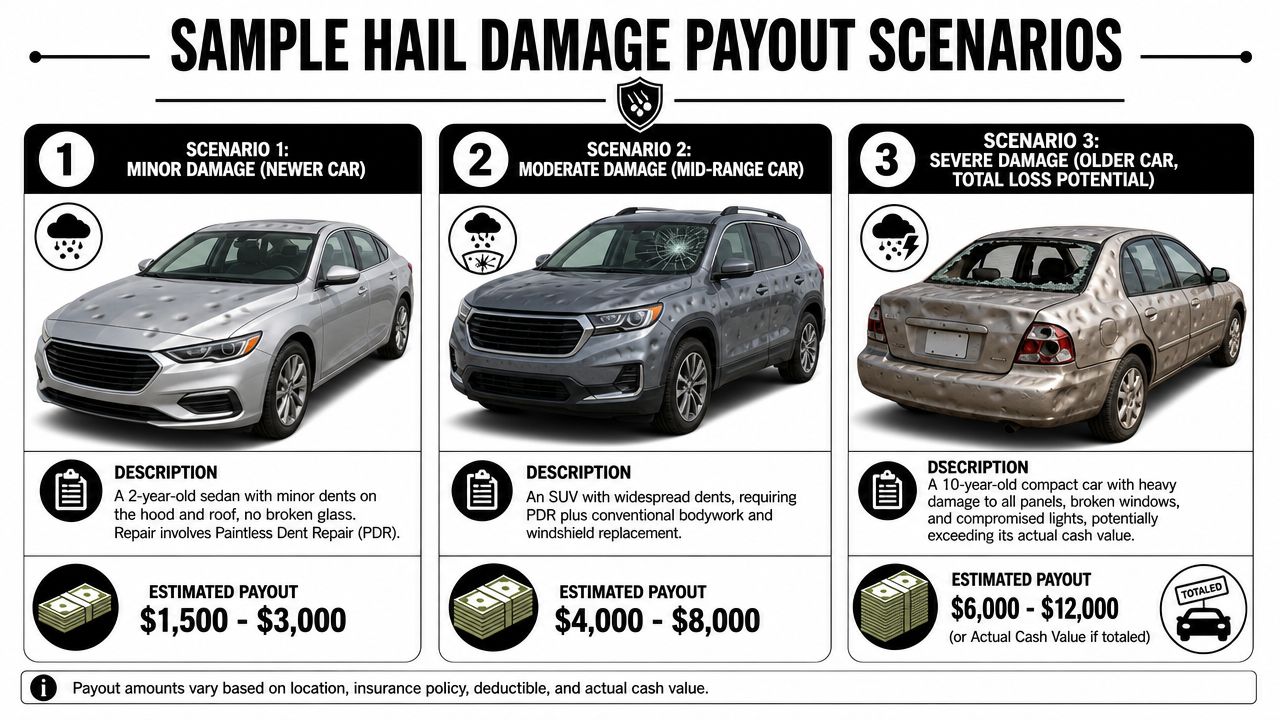

Sample Hail Damage Payout Scenarios

Examples make this easier. The core rule for hail damage claims is straightforward: insurers generally reimburse repair cost above the deductible and up to the vehicle's actual cash value, as explained in ValuePenguin's overview of hail coverage and claim limits.

Scenario one with lighter damage

You own a newer sedan. The hood and roof took visible dents, but the paint is intact and the glass survived. A qualified shop believes paintless dent repair can restore the panels.

The claim logic is simple. Start with the repair estimate. Subtract your deductible. The remainder is the likely covered payment, assuming the estimate is complete and accepted.

This is the kind of claim that often feels “small” until the estimate comes back. Even moderate-looking hail can produce a meaningful bill because dent counting across multiple panels adds up quickly.

Scenario two with broad moderate damage

You own an older SUV. Hail hit the hood, roof, liftgate, and one side of the vehicle. The windshield also cracked. The shop's first estimate is substantial, and a second estimate comes in differently because one shop leans heavily on paintless dent repair while the other includes more conventional work.

Policyholders often find themselves boxed in by the insurer's first number. The carrier may choose the leaner estimate. The shop may later submit a supplement once trim is removed and more damage is visible.

A supplement isn't a favor from the insurer. It's the mechanism for getting paid when the initial estimate missed damage.

For this type of claim, your payout can shift materially after teardown or deeper inspection. That's why one estimate rarely tells the whole story after a major hail event.

Scenario three with severe damage and total-loss potential

You own an older compact car. Hail damage is widespread. Multiple panels are heavily struck. Glass is broken. Lights and attached exterior components are involved. Repairs are so high that the insurer compares them to the car's actual cash value.

Now the file stops being a repair claim and starts behaving like a valuation dispute. The payment no longer turns mainly on repair operations. It turns on what the car was worth immediately before the storm and what the policy requires after deductible.

Here's the clean framework:

- If repair cost stays below the insurer's total-loss threshold, the car is repaired and the deductible is applied to covered repair cost.

- If repair cost exceeds what makes economic sense under the policy, the insurer may total the car.

- Once totaled, the key fight becomes vehicle value, not dent count.

How to use these examples on your own claim

Put your claim into one of these buckets:

- Mostly cosmetic and repairable

- Moderate but expandable once the shop starts work

- Severe enough to trigger a total-loss review

Then ask the right question for that bucket. Repairable claims need complete estimates. Borderline claims need shop-backed supplements. Total-loss claims need aggressive valuation review.

That's how you move from “What's the average insurance payout for hail damage car claims?” to “What's the fair number for my car?”

The Hail Damage Claim Process Step by Step

Claims go better when you move quickly and stay organized. State guidance recommends filing promptly, documenting all damage thoroughly, and getting more than one estimate because costs and timelines can vary widely after a major storm, as noted by the Texas Department of Insurance's post-storm claim guidance.

Start with proof before cleanup

Before you wash the car, photograph it from every angle. Take close shots of the hood, roof, trunk, glass, and trim. Take wide shots too, so nobody can later argue the photos were too tight to place the damage on the vehicle.

Then pull your policy and confirm that you carry coverage that includes hail damage. If you only have liability, this turns into a very different conversation.

If a storm also caused water intrusion, don't wait around while moisture sits inside the cabin. A practical companion resource is this emergency car water damage plan, which helps you limit secondary damage while the claim gets moving.

File fast and control the paper trail

Call the insurer early. Get a claim number. Write down the date, time, and the name of every representative you speak with. Email follow-up summaries when possible so there's a written record.

Then schedule the inspection. When the adjuster or appraiser sees the car, don't assume they'll catch everything. Hail damage can disappear under flat lighting and show up clearly only under the right angle or specialty shop lighting.

Here's the process I recommend:

- Photograph first: Exterior, glass, trim, and interior if water entered.

- Report the claim: Get the file opened immediately.

- Secure at least two estimates: One estimate isn't enough in a busy post-storm market.

- Review the insurer estimate line by line: Look for missing glass, trim, moldings, or panel-specific work.

- Choose the repair path carefully: Don't get pushed into the fastest option if it's not the right repair.

If you want a better sense of how carrier-side evaluations work, this explanation of the auto damage adjuster role can help you understand what to expect.

“The first inspection is the beginning of the claim, not the end of it.”

Expect delays after major storms

Oregon and Washington don't see the same hail patterns as the Plains, but when localized severe weather hits, repair calendars can still tighten fast. Shops get backed up. Adjusters get overloaded. Communication slows down.

That's not a reason to go passive. It's a reason to document harder, follow up consistently, and keep every version of every estimate.

How to Maximize Your Hail Damage Recovery

Insurers handle enormous hail exposure. In 2023, State Farm reported $6.1 billion in hail payouts, and that scale creates a clear incentive to control individual claim costs, as discussed in United Policyholders' review of rising hail losses. You don't need to be cynical to understand the implication. You need to be prepared.

Treat the first offer as a draft

The first estimate often reflects speed, not completeness. It may be enough for obvious visible damage, but hail claims frequently expand after shop review. If your repair shop finds additional dents, hidden panel issues, or line items the insurer left out, push for a supplement.

That is normal claims practice. You don't need permission to ask for the file to be updated with better evidence.

Push back on low valuation with actual support

If your car is headed toward total loss, the most important number in the file may become the insurer's actual cash value figure. Challenge it when it's weak.

Use concrete support:

- Vehicle condition records: Service records, tire replacement, recent mechanical work, and proof the vehicle was well-kept.

- Options and features: Trim package, safety features, premium audio, upgraded wheels, or other value-driving equipment.

- Comparable vehicles: Listings and market evidence that better reflect what it would cost to replace a similar car in your area.

Don't argue with general complaints. Argue with documents.

Don't ignore diminished value concerns

Even when a car is repaired well, policyholders often worry about resale stigma after a documented hail claim. Whether that becomes recoverable under your situation depends on policy language, facts, and how the claim is handled. What matters here is strategic awareness. If the repair path leaves lingering marketability concerns, raise the issue early and document your basis.

Be the organized party in the file

The organized side usually controls the outcome. Build a claim folder with:

| Keep in your file | Why it matters |

|---|---|

| Photos before repair | Confirms visible scope |

| Repair estimates | Shows pricing differences |

| Supplement requests | Captures added damage |

| Claim communications | Creates accountability |

| Valuation support | Helps challenge low total-loss offers |

If the insurer underestimates the loss, your advantage comes from better evidence and steady follow-up. Not anger. Not guesswork. Paper.

When to Hire a Public Adjuster in Oregon and Washington

Most straightforward hail claims don't need a fight. Some do. You should think seriously about outside help when the insurer undervalues a total loss, misses major repair items, delays the claim without clear explanation, or pressures you to accept a number that doesn't match the actual damage.

That's especially true if you're in Oregon or Washington and you're already juggling storm cleanup, work, family, and repair delays. The claim may be only one problem in your life. The insurer knows that. Fatigue leads people to accept weak outcomes.

Red flags that mean it's time

If any of these are happening, get help:

- The estimate feels stripped down: Missing glass, trim, molding, or panel work.

- The car may be totaled: You need someone to scrutinize actual cash value, not just repair numbers.

- The insurer keeps changing the story: Different representatives, different explanations, no stable path forward.

- Your documentation is stronger than their offer: That usually means the negotiation hasn't been pushed hard enough.

A public adjuster works for the policyholder, not the carrier. That matters. If you're dealing with a disputed claim in the Northwest, start by understanding what a licensed public adjuster in Oregon does and where that representation can change the outcome.

When the claim turns technical, representation stops being a luxury and starts being a practical decision.

If your hail damage claim in Oregon or Washington feels stalled, undervalued, or far more complicated than it should be, NW Claims Management can step in, review the file, document the loss, and advocate for a fair settlement so you don't have to fight the carrier alone.