Think of scheduled personal property coverage as a VIP pass for your most valuable belongings. It's a special add-on to your standard insurance that protects specific, high-value items for their full, appraised worth. This completely bypasses the frustratingly low limits built into a typical homeowners policy, making sure your prized possessions are actually covered when it counts.

Your Valuables Are Not as Safe as You Think

Can you imagine the feeling of discovering your treasured engagement ring or priceless art collection is only covered for a tiny fraction of its value after a theft or fire? It's a shocking and all-too-common reality for many homeowners. This is the costly blind spot hidden deep within standard homeowners and renters insurance policies. You might assume your policy protects everything you own, but it has a secret that leaves your most valuable items dangerously exposed.

Your basic policy does include personal property coverage, but it’s definitely not a blank check. Instead, it places strict internal caps, known as sub-limits, on specific categories of high-value goods.

The Hidden Risk of Policy Sub-Limits

These sub-limits are the absolute maximum an insurer will pay for a loss in a particular category, no matter what the items were actually worth. This creates a massive financial risk for anyone who owns anything of significant value.

Let’s say you’re a homeowner in Portland, Oregon, and a burst pipe floods your bedroom, ruining your $10,000 engagement ring. When you file a claim, you’re in for a rude awakening. Most standard policies cap jewelry coverage at just $2,000 to $2,500. That sub-limit means you’d only get a fraction of its true value back, leaving you with a huge financial loss. You can find more detail on how these standard limits work from insurance experts at Policygenius.

This is exactly why understanding scheduled personal property coverage is so critical. It’s an endorsement—an add-on to your policy—that completely changes the rules. By "scheduling" the ring, you list it individually with a professional appraisal, locking in coverage for its full $10,000 value.

Key Takeaway: A standard homeowners policy is built to cover general contents like furniture and clothes, not unique, high-value assets. Relying on it to protect your valuables is a recipe for major financial disappointment.

Standard Limits vs Scheduled Protection

To see just how different these coverages are, let's put them side-by-side. Think of standard coverage as a wide, but very shallow, safety net. Scheduled coverage, on the other hand, provides deep, focused security for the individual items that matter most to you. The first step to finding these gaps in your own policy is a thorough property damage assessment.

Here’s a quick comparison:

| Feature | Standard Homeowners Coverage | Scheduled Personal Property Coverage |

|---|---|---|

| Coverage Amount | Capped at a low category limit (e.g., $2,500 for all jewelry) | Covers the item's full, individually appraised value |

| Covered Risks (Perils) | Usually limited to "named perils" like fire and theft | Often "all-risk," including accidental loss & disappearance |

| Deductible | Your main policy deductible applies (often $1,000+) | Typically has a $0 deductible |

As you can see, this isn’t just about getting more money back after a disaster; it’s about getting the right kind of protection. Scheduling an item essentially gives it a personal, tailor-made insurance policy that accounts for its specific worth and risks. It is the only way to truly ensure your most cherished possessions are secure.

Scheduled vs. Unscheduled Coverage Explained

To really understand what scheduled personal property coverage is, you first have to know what it isn't. Every standard homeowner's policy comes with what’s called unscheduled personal property coverage. Think of it as the default, blanket protection for everything you own, from your couch and clothes to your kitchen gadgets.

This "blanket" coverage usually protects your belongings up to a set percentage of your home's insured value—typically 50% to 70%. So, if your home is insured for $500,000, you might have $250,000 in total coverage for your stuff. That sounds pretty good on the surface, but the devil is in the details.

The Problem With "Blanket" Protection

That big number is misleading because it’s riddled with sub-limits. These are frustratingly low caps on specific categories of valuable items. For instance, your policy might put a $2,500 total limit on all stolen jewelry, no matter if you lost one ring or ten, and regardless of their actual worth.

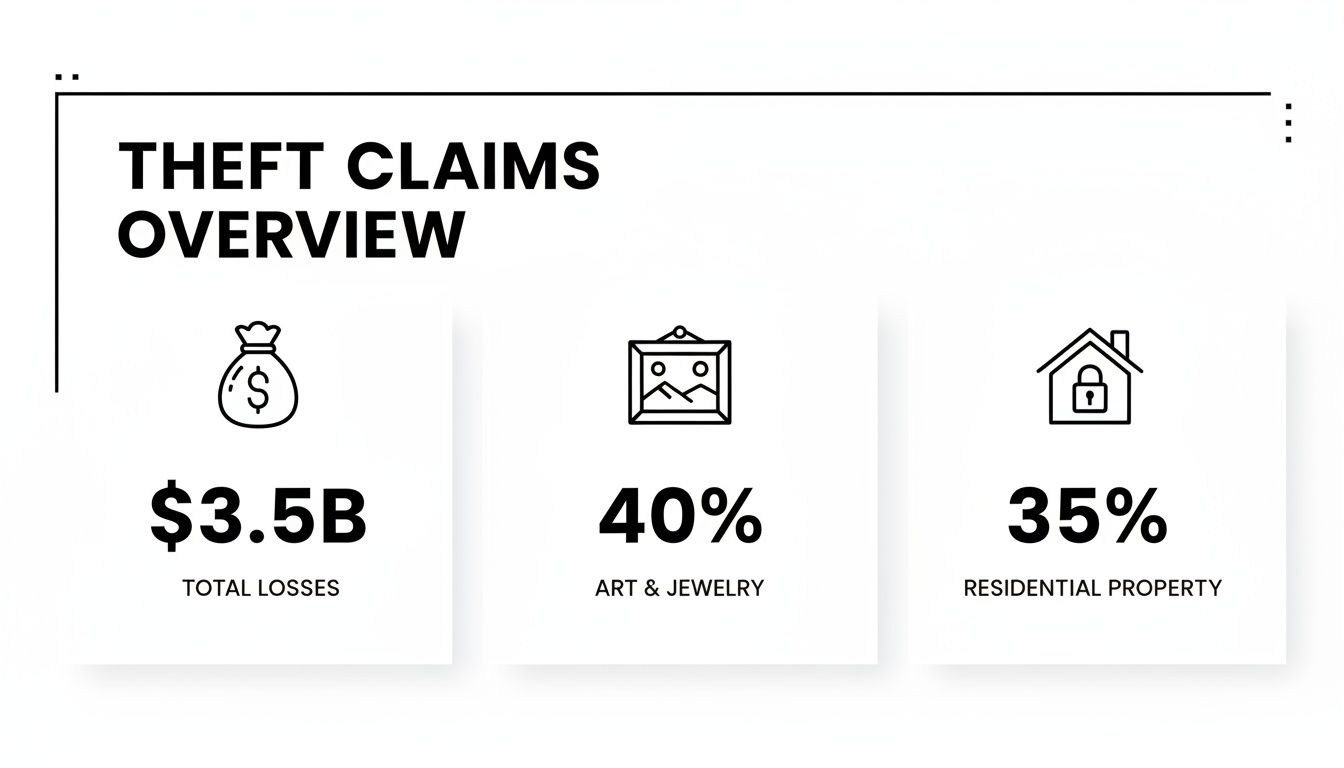

This is where homeowners get into serious trouble. Imagine a family in Washington whose house is broken into. The thieves take off with a $15,000 art collection they’ve spent years curating from local galleries. With only their standard, unscheduled coverage, they’d be lucky to get a couple of thousand dollars back because of a low sub-limit on fine art. It’s a shockingly common scenario. According to the Insurance Information Institute, theft claims hit over $3.5 billion in 2022, and a study highlighted on Bankrate.com found that nearly 40% of claims for high-value art and collectibles are underpaid because of these very caps.

This is exactly the problem that scheduled personal property coverage solves. Instead of a one-size-fits-all approach, it gives your most prized possessions their own dedicated protection.

How Scheduled Coverage Delivers Real Protection

When you "schedule" an item, you're essentially pulling it out from under that restrictive blanket coverage. You list it individually on your policy along with its specific, appraised value.

Doing this offers a few huge advantages that your standard policy just can't match:

- You Get What It's Worth: The item is insured for its full, agreed-upon value. If your $15,000 scheduled ring is stolen, you get $15,000. No arguments, no lowball sub-limits.

- You're Covered for More Scenarios: Scheduled items are typically covered on an "all-risk" basis. This means you’re protected from almost any cause of loss unless it's explicitly excluded. Crucially, this often includes mysterious disappearance—like an earring vanishing while you’re out for the evening—something a standard policy almost never covers.

- You Usually Skip the Deductible: Most scheduled property endorsements have a $0 deductible. With a normal claim, you'd have to pay your main policy deductible (often $1,000 or more) out-of-pocket before seeing a dime from the insurance company.

The Core Difference: Unscheduled coverage is for your general stuff, with broad but shallow limits. Scheduled coverage is for your specific treasures, with deep, itemized protection.

Knowing the difference between these two is absolutely critical. You need to know if you have one single limit for everything or separate, scheduled limits for your most valuable items. Our guide on understanding insurance policy limits dives deeper into reading your policy declarations page. Getting this right is the key to making sure you aren't blindsided by a devastating financial loss when you can least afford it.

Which Valuables Need Scheduled Coverage

So, how do you know which of your belongings actually need to be scheduled? The simple answer is this: if you own something valuable that would cost more to replace than your policy’s built-in limits, it’s a candidate for scheduling. It’s time to take a mental walk through your home and pinpoint those high-value items.

Most people are surprised by what they find. It's not just about dusty heirlooms locked away in a safe. We see clients with high-tech gear, extensive collections, and modern luxury goods that are dangerously underinsured.

Let’s dig into the specific items that almost always need this extra layer of protection.

Common Items That Need Scheduling

A standard homeowners policy might only give you $1,500 to $2,500 for an entire category of valuables, like jewelry. That’s not for one piece—that’s for everything. If you own any of the items below, it's time to talk to your agent about scheduling them.

- Jewelry: This is easily the most common category we see. An engagement ring, a luxury watch, or a family heirloom can be worth $5,000, $10,000, or much more. A standard policy's limit just won't cut it.

- Fine Art: That painting or sculpture you love? Your policy likely caps its coverage at around $2,500. For a single piece worth tens of thousands, that’s a massive financial risk.

- Firearms: Whether you have a collection for sport or for historical value, insurers put tight limits on firearms. A typical policy might only cover $2,500 for the entire collection, no matter how many you lose in a fire or theft.

- High-End Cameras and Electronics: Professional photographers and serious hobbyists can easily have a bag of gear worth well over $10,000. Scheduling ensures your specific lenses, camera bodies, and lighting are all covered for what they're actually worth.

Of course, this isn't an exhaustive list. We frequently work on claims involving valuable musical instruments, extensive stamp or coin collections, antique silverware, and even fine furs.

Your homeowners policy comes with built-in sub-limits for certain categories of personal property. These limits are often shockingly low compared to the actual value of the items. The table below illustrates just how wide that gap can be.

Typical Insurance Sub-Limits for High-Value Items

| Item Category | Typical Standard Policy Limit | Potential Uninsured Value (Example) |

|---|---|---|

| Jewelry & Watches | $1,500 per theft | $8,500 (for a $10,000 ring) |

| Firearms | $2,500 total | $12,500 (for a $15,000 collection) |

| Silverware | $2,500 total | $7,500 (for a $10,000 set) |

| Fine Art | $2,500 total | $17,500 (for a $20,000 painting) |

Without scheduling, the "Potential Uninsured Value" column represents the money you would lose out-of-pocket after a claim. It’s a powerful argument for getting these items properly insured.

Don't Forget Modern Collectibles

The definition of "valuable" is always changing. Your most prized possessions might not be the same things your grandparents cherished, but they absolutely need the same level of protection. Many modern collections carry immense value but are often completely overlooked when it comes to insurance.

Think about some of these less-obvious, but equally important, assets:

- Rare Sneakers: A curated collection of limited-edition sneakers can easily be worth thousands, if not tens of thousands, of dollars.

- Fine Wine or Spirits: That wine cellar you've spent years building is a significant investment. Your standard policy won't come close to covering its loss.

- Designer Handbags: Many luxury handbags are true investment pieces, often worth more than the entire jewelry sub-limit on a standard policy.

- Antiques and High-End Furniture: A single Biedermeier cabinet or Eames chair can be incredibly valuable and requires its own specific coverage.

For many, these items are more than just possessions; they are assets. People are actively investing in luxury watches and art, and protecting those investments with specialized coverage is just smart financial planning.

The Threat of Mysterious Disappearance

Here's one of the biggest—and most overlooked—perks of scheduling an item: you often get coverage for "mysterious disappearance." This is a huge deal for small, valuable things like jewelry.

Mysterious disappearance covers you when an item simply vanishes without any sign of a break-in or theft. Imagine your engagement ring slips off your finger while you're gardening and is gone for good. A standard policy won't cover that. But a scheduled policy almost always will.

Theft, of course, remains a primary threat, and the financial impact can be devastating.

As this data shows, theft leads to billions in losses each year, and a huge portion of that comes from residential property, especially valuables like art and jewelry. Knowing which items to schedule is the first step, but understanding what to do after a loss is just as crucial. If you ever find yourself in that unfortunate situation, our guide on how to file a property damage claim walks you through the entire process.

How to Schedule Your High-Value Items

Alright, so you've identified which of your prized possessions could use some extra protection. Now comes the important part: actually adding them to your policy. Scheduling an item is a surprisingly straightforward process, but it's one that delivers absolute peace of mind by making sure your valuables are covered for what they’re truly worth.

The entire process boils down to one simple idea: prove the item's value before a loss ever happens. When you do this upfront, you eliminate the guesswork and potential disputes later, which makes any future claim remarkably smooth.

Start with Solid Documentation

Before you can schedule anything, you need to prove what it is and what it's worth. Your insurance company isn't just going to take your word for it; they require official documentation. Think of this as building the unshakable foundation for your coverage.

Here’s what you'll need to gather:

- A Professional Appraisal: This is the cornerstone of your documentation. For things like jewelry, fine art, or rare antiques, you absolutely need a formal appraisal from a certified expert. Keep in mind, most insurers require these to be recent, typically from within the last 3 to 5 years.

- Detailed Receipts: Never underestimate the power of the original bill of sale. It’s concrete proof of both ownership and what you initially paid.

- High-Quality Photographs: Take clear, well-lit photos of your items from several angles. This visually documents their condition and captures any unique identifying marks.

A proper appraisal is much more than just a price tag; it's a detailed report. It will describe the item thoroughly—its materials, age, condition, and any special characteristics that make it valuable.

Contact Your Agent and Specify Coverage

With your documentation in hand, it's time to call your insurance agent. You'll need to tell them you want to add a scheduled personal property endorsement to your policy. You might hear them call it a "floater" or a "rider," but they all mean the same thing: specific, itemized coverage for your valuables.

During that conversation, you'll need to discuss the valuation method. This is a critical detail that determines how your insurer pays you after a loss, and getting it right is non-negotiable.

Crucial Insight: Don't assume your agent magically knows which items you want to schedule. You have to be proactive. It's your responsibility to start the conversation and provide the necessary proof of value to get the right protection in place.

There are two main ways insurers value your items, and the difference between them is huge.

- Replacement Cost Value (RCV): This is what you want. RCV pays you the full amount it would take to buy a brand-new, comparable item today. It completely ignores depreciation.

- Actual Cash Value (ACV): This method pays you what the item was worth the second it was destroyed. It calculates this by taking the replacement cost and then subtracting value for age, wear, and tear.

For your most treasured possessions, always insist on Replacement Cost Value. If you settle for ACV on a five-year-old camera or watch, you'll only get a fraction of what it costs to buy a new one. RCV gives you the funds to actually replace what you lost and make yourself whole again.

The Cost of Coverage and How Claims Work

So, we’ve covered the what and the why. Now, let's get down to the two questions that really matter: "What's this going to cost me?" and "What happens if I actually have to use it?"

Thinking about insurance costs can feel like a chore, but you'll be pleasantly surprised here. Scheduled property coverage is remarkably affordable. The price is typically a small annual percentage of an item's appraised value.

As a rule of thumb, you can expect to pay somewhere around $1 to $2 for every $100 of value you want to insure.

Breaking Down the Cost

Let's put that into perspective with some real-world numbers.

- A $15,000 watch? You're likely looking at an annual premium of $150 to $300.

- A $10,000 engagement ring? That might cost about $100 to $200 per year to protect.

- A $5,000 camera system? You could schedule it for as little as $50 to $100 a year.

When you stack those small annual payments against the risk of a sudden, five-figure loss, the value becomes crystal clear. It’s always smart to research the specific cost of insuring an engagement ring or other valuables to get a precise quote, but these estimates give you a solid starting point.

This kind of specific coverage is a huge deal, especially when you consider the alternative. Imagine a pipe bursts in your home office, destroying $20,000 worth of high-end electronics. Your standard policy likely has a sub-limit for electronics—often just $2,000 to $3,000. That leaves a massive gap you'd have to cover out of pocket. We see this all the time. Statistics from our region show that underinsurance is a major problem, with 28% of claims for valuable items in the Pacific Northwest being underinsured.

How a Claim Works: A Tale of Two Policies

The real magic of scheduling an item happens the moment you need to file a claim. The experience is night-and-day different from a standard claim.

Let's walk through a common scenario. Say you lose a beautiful $12,000 bracelet while traveling.

Claim Without Scheduling: You call your insurance company to file a claim on your homeowners policy. Right away, you’re on the hook for your $2,000 deductible. Then comes the bad news: your policy has a $2,500 sub-limit for jewelry. After your deductible, the insurance company pays you only $500 ($2,500 limit – $2,000 deductible). You just lost $11,500.

Claim With Scheduling: You file a claim against your scheduled property endorsement. You simply provide the paperwork showing the bracelet was scheduled for its full $12,000 value. And because most scheduled endorsements come with a $0 deductible, the insurance company cuts you a check for the full $12,000. It's that simple.

This stark contrast shows the incredible peace of mind that scheduling provides. The process is direct, the payout is fair, and you're made whole without the financial gut punch of deductibles and sub-limits. It makes that small annual investment feel like an absolute no-brainer.

Even with a scheduled item, claims aren't always straightforward. Insurance policies are complex contracts, and carriers can still find ways to underpay. Knowing the cost and value of hiring a public adjuster can be a game-changer, ensuring an expert is fighting on your side to get the full amount you're owed.

Why a Public Adjuster Is Your Best Ally

You did everything right. You identified your valuable items, got them appraised, and paid extra to have them scheduled on your policy. So when a loss happens, you expect a straightforward payout, right? Unfortunately, that’s often not the case.

Even with clear documentation, an insurance company might still push back. They may question the item's pre-loss condition, challenge the appraisal, or find some other reason to dispute the value. At the end of the day, their goal is to protect their bottom line, which means minimizing what they pay out in claims. This leaves you, the policyholder, in a stressful, uphill battle against a massive corporation with teams of experts working against you.

Leveling the Playing Field in Oregon and Washington

This is exactly where a public adjuster steps in. A licensed public adjuster, like our team at NW Claims Management, works only for you, the policyholder. We don’t work for the insurance company. Our entire job is to be your advocate, ensuring your insurer honors the promises made in your policy—especially for your specifically scheduled items.

In high-value claims across Oregon and Washington, having a professional on your side isn’t a luxury; it’s a necessity. We translate the dense policy jargon, build an airtight case for the full value you're owed, and fight back when the insurance company tries to undervalue your loss.

An insurance company's adjuster works to protect the company's interests. A public adjuster works to protect yours. It’s a fundamental difference that can be worth tens of thousands of dollars.

When your insurer argues over the condition of a lost heirloom or challenges a certified appraisal, we counter their arguments with facts, our own thorough documentation, and a deep understanding of state-specific insurance regulations. We take over the endless phone calls, emails, and paperwork, lifting that enormous burden off your shoulders so you can focus on getting back to normal.

From Documentation to Final Negotiation

Hiring a public adjuster means you have an expert managing every phase of the claim. We handle the entire process from start to finish. This includes:

- Digging into Your Policy: We comb through your policy and endorsements to find every bit of coverage you're entitled to.

- Documenting the Loss: We create a comprehensive proof-of-loss package, leaving no room for the insurer to question the details.

- Fighting for Full Value: We negotiate aggressively for the full, appraised value of your scheduled property, rejecting any lowball offers.

- Managing the Settlement: We navigate the complex final steps to make sure you get a fair and timely payment.

Our goal is simple: secure the absolute best possible settlement for you without the stress and frustration of a drawn-out fight. To see what this advocacy looks like in practice, you can learn more about the benefits of hiring a public adjuster and how we empower policyholders.

When your most valuable possessions are on the line, having a powerful ally makes all the difference.

Common Questions About Scheduled Coverage

Once you get the hang of what scheduled personal property coverage is, a few practical questions almost always come up. Let's walk through the most common ones to clear up the details and help you decide if it's the right move for your valuables.

Do I Still Have a Deductible for a Claim on a Scheduled Item?

This is where scheduling really shines. In most cases, the answer is no. Claims on a scheduled item often come with a $0 deductible.

Think about what that means for a moment. On a standard homeowners claim, you'd have to pay your policy deductible—often $1,000 or more—out of your own pocket before the insurance company pays a dime. With a scheduled item, you typically get a check for the full, agreed-upon value without that upfront hit. It’s always smart to confirm the exact deductible terms with your agent, but this is a major advantage.

How Often Should I Get My Scheduled Items Re-Appraised?

Keeping your values current is crucial. The rule of thumb is to get fresh appraisals for your scheduled items every 3 to 5 years.

This is especially true for things that can swing in value, like:

- Fine art and antiques

- High-end jewelry and vintage watches

- Rare collectibles

Markets shift. A piece you bought for $10,000 five years ago might be worth $15,000 today. If a disaster happens and your appraisal is out of date, you’ll only get paid based on that old, lower value. A simple calendar reminder can save you thousands by making sure your coverage keeps up with your item's actual worth.

Expert Tip: Don't rely on your insurance carrier to prompt you. Proactively managing your appraisals is your responsibility and the single best way to protect your investments.

Are My Items Covered When I Travel?

Yes, they are! This is another huge perk. Scheduled personal property coverage typically gives you what's called "all-risk" or "open peril" protection, which follows your items worldwide.

So, whether your watch is snatched on an overseas vacation or you lose an earring while running errands, your scheduled policy is designed to respond. This is a massive upgrade from a standard policy, which often has strict limits—or no coverage at all—for your belongings once they leave your property.

Can I Schedule an Entire Collection as One Item?

It really depends on the collection. For most high-value collections, you’ll need to itemize. This means listing each individual piece of jewelry, watch, or painting with its own specific appraised value.

But for some types of collections, you might be able to use a "blanket" limit. For instance, instead of listing every single stamp or coin, you might be able to insure the entire collection under a single, total value. This can be a much more practical and affordable way to handle things. The best approach is to talk it through with your insurance agent to see what makes the most sense for your specific collection.

Even with the best coverage, navigating a complex claim can be overwhelming. NW Claims Management acts as your exclusive advocate, managing the entire process to ensure you recover the full value you're owed. If you're facing a property loss in Oregon or Washington, contact us for a free claim evaluation.