Think of your standard homeowners and auto insurance as a good, sturdy roof. It protects you and your assets from the everyday rain showers of small accidents and minor liability claims. But what happens when a "once-in-a-generation" financial storm hits? A catastrophic lawsuit from a serious car wreck or a major injury on your property can easily blow past the limits of your primary coverage.

That's where a Chubb insurance umbrella policy comes in. It’s not your first line of defense—it’s your financial storm shelter. This is a massive, secondary layer of liability protection that only kicks in after your primary home or auto policy has paid out its maximum amount. It's specifically designed to shield your life's savings, your home, and even your future earnings from being wiped out by a massive legal judgment.

Do You Need an Umbrella Policy? A Quick Assessment

While often associated with the ultra-wealthy, the reality is that many people have more at risk than they realize. If the total value of your assets—your house, savings, investments—is higher than the liability limits on your existing policies, you have a serious coverage gap. This simple table can help you gauge your own risk level.

| Risk Factor | Lower Risk (Standard Policies May Suffice) | Higher Risk (Consider an Umbrella Policy) |

|---|---|---|

| Assets | Savings and home equity are less than your current liability limits. | Savings, investments, and home equity exceed your current liability limits. |

| Lifestyle | You rarely host guests and have no high-risk features on your property. | You own a pool, trampoline, boat, or dog; frequently host parties. |

| Driving Habits | You have one or two drivers in the house with clean records. | You have teenage drivers, a long commute, or multiple vehicles. |

| Public Profile | You maintain a private life with little community recognition. | You're a well-known professional, business owner, or serve on a non-profit board. |

If you find yourself checking off more boxes in the "Higher Risk" column, an umbrella policy isn't a luxury—it's a critical part of a sound financial plan. You're simply a more attractive target for a lawsuit, and this extra coverage provides the peace of mind that one bad day won't derail your entire future. The first step is always understanding what you already have; you can get a clearer picture of how standard insurance policy limits explained here work before deciding if you need more.

Why Chubb Stands Out in Umbrella Coverage

Chubb has carved out a reputation as the go-to insurer for families with significant assets to protect. This isn't just marketing hype; it's backed by their dominant position in the market. As awareness about personal liability grows, the global umbrella insurance market is projected to expand from $3.034 billion in 2024 to over $5.05 billion by 2035.

For property owners in Oregon and Washington, where claims from everything from house fires to guest injuries are a constant reality, this extra protection is becoming essential. Chubb is consistently ranked as the #1 personal lines insurer for high-net-worth families in the U.S., giving them an unmatched presence in this space.

Imagine a Portland homeowner has a guest who suffers a severe slip-and-fall injury, resulting in a lawsuit that settles for $1.2 million. If their standard homeowners policy has a $500,000 liability limit, they would personally be on the hook for the remaining $700,000. With a Chubb umbrella policy (which often starts at $1 million in coverage), it would seamlessly step in to cover that excess amount, protecting their home and savings.

How Umbrella Coverage Works with Your Existing Policies

It helps to picture your insurance as a two-layer safety net. The first layer is your standard home and auto insurance—the policies that handle the more common, everyday claims. A Chubb insurance umbrella policy is the second, much larger layer of protection underneath. It’s there to catch you when a truly massive claim rips right through your primary coverage.

The whole system is designed to work together. Your umbrella policy doesn’t replace your car or home insurance; it adds a powerful layer of liability protection on top of them. It only kicks in after your primary policies have paid out their full limit. This way, you get a huge safety net for catastrophic events without paying for redundant coverage.

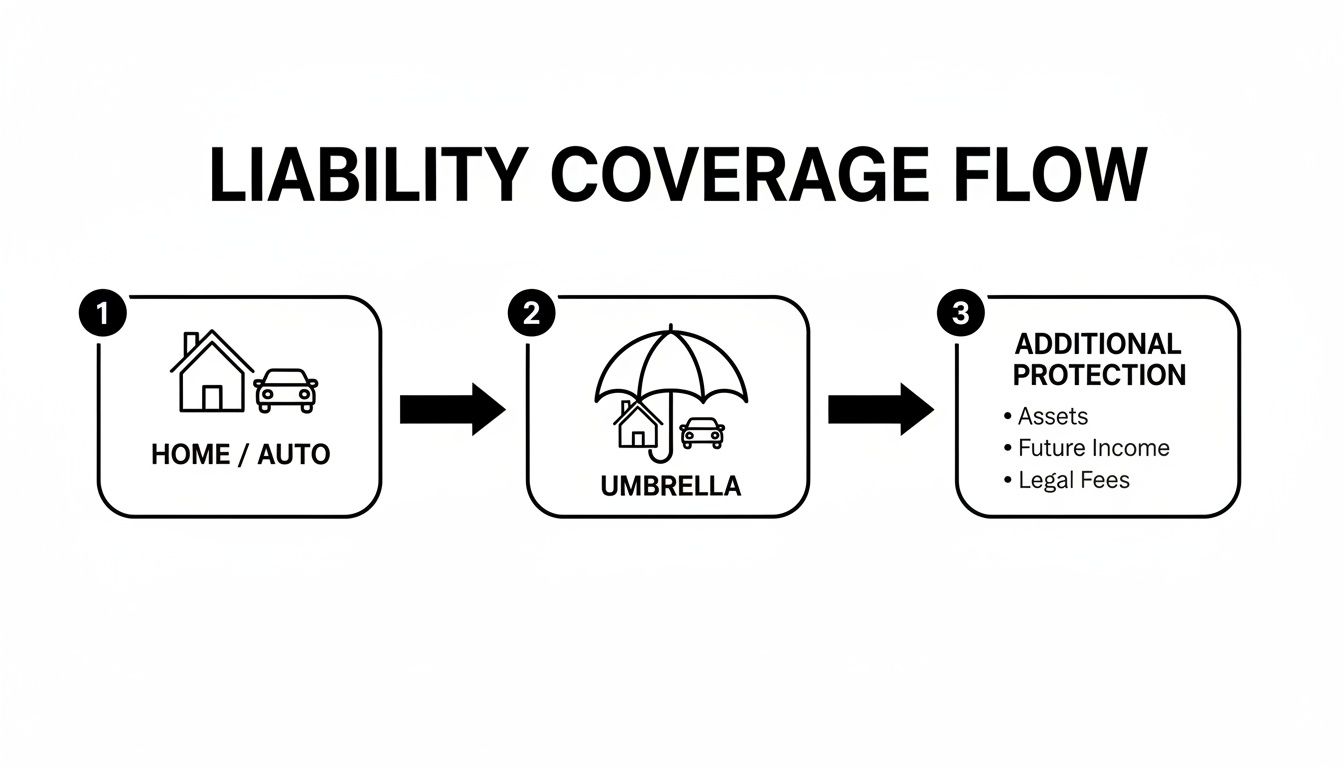

This flowchart gives you a great visual of how a claim flows from your standard policies up to your umbrella policy.

As you can see, the umbrella policy is the final, broad layer of defense, stepping in only after your home and auto policies have done their job.

The Role of Underlying Limits

For this to work smoothly, Chubb requires your primary policies to have a certain amount of coverage already in place. These minimums are called underlying limits or required underlying limits.

Think of it this way: the insurer wants to make sure your home and auto policies are strong enough to handle typical claims. This reserves the massive umbrella coverage for the truly devastating, once-in-a-lifetime events. It’s almost like a deductible for your umbrella policy, but instead of you paying it, your primary insurance carrier does.

As a baseline, Chubb will typically require underlying limits like these:

- Auto Liability: $250,000 per person / $500,000 per accident for bodily injury.

- Homeowners Liability: $300,000 or $500,000 per occurrence.

If your current policies don't meet these minimums, you’ll just need to increase their limits before you can add the umbrella protection.

The Claim Process in Action

Let’s walk through a real-world scenario. Say you’re found at fault for a pile-up on a wet Washington highway, and the court hands down a $1.5 million judgment against you. Here’s how your insurance would respond.

- Primary Policy Pays First: Your auto insurance has a $500,000 liability limit. It pays that full amount toward the judgment, completely exhausting its coverage.

- The Coverage Gap: Even after your auto policy pays out, you’re still on the hook for $1 million. Without an umbrella, your personal assets—your home, savings, and even future income—would be at risk.

- Umbrella Policy Activates: This is where your Chubb umbrella policy springs into action. It covers the remaining $1 million, picking up right where your auto policy left off.

The core function of a Chubb insurance umbrella policy is to bridge the gap between a primary policy’s limit and the final cost of a catastrophic liability claim, thereby protecting your personal assets from seizure.

This seamless coordination is what keeps your financial life intact. It prevents a single devastating accident from forcing you to sell your home, drain your retirement funds, or have your wages garnished for years.

Of course, having the coverage is one thing; getting the full value you're owed is another. When the stakes are this high, understanding the ins and outs of negotiating with an insurance company becomes absolutely critical.

What Your Chubb Umbrella Policy Actually Covers

It’s one thing to know how a Chubb insurance umbrella policy works in theory. It’s another thing entirely to understand what it protects you from in the real world. This isn't just an extra layer of insurance; it's a powerful shield designed to protect you from the kinds of liabilities that can come out of nowhere and threaten everything you've worked for.

Think of it this way: your standard policies are built to protect your property, but an umbrella policy is built to protect your entire net worth. A basic homeowner's policy might handle a minor slip-and-fall. A Chubb umbrella policy is for when that fall results in a permanent disability, sparking a multi-million-dollar lawsuit for a lifetime of medical care and lost wages.

Core Liability Protection

At its core, an umbrella policy gives your existing liability coverage a massive boost. When a claim is big enough to blow past the limits of your auto or home insurance, the umbrella policy steps in to cover the rest.

This is exactly what you need for scenarios like:

- Severe Auto Accidents: You cause a multi-car pileup that injures several people. The medical bills and vehicle damage quickly add up, soaring past your auto policy’s $500,000 limit.

- Major Injuries on Your Property: A delivery driver takes a hard fall on your icy steps in Portland. Or maybe a guest is seriously injured during a summer pool party at your Seattle-area home, leading to a huge lawsuit.

- Incidents Involving Your Family: Your teenager is at fault in a boating accident on the Columbia River, or your dog seriously bites someone at a local park.

In every one of these situations, once your primary insurance has paid its maximum, your Chubb umbrella policy takes over. It pays the rest of the settlement, all the way up to its own much higher limit.

Coverage Beyond the Basics

Where a Chubb policy really starts to show its value is in covering liabilities that most people don’t even realize they have. These "personal injury" risks are often specifically excluded from a standard homeowners policy, but they are a cornerstone of a high-quality umbrella plan.

This kind of protection is critical today and can cover claims for things like:

- Libel and Slander: You post a scathing online review of a local contractor. They sue you, claiming your review destroyed their business.

- False Arrest or Imprisonment: You're hosting a charity event and incorrectly accuse someone of stealing, leading to a claim for false arrest.

- Malicious Prosecution: You file a lawsuit against someone that is ultimately thrown out, and they turn around and sue you for damages.

Defending yourself against these claims can be incredibly expensive, even when they’re completely baseless. A huge benefit of a Chubb umbrella is that it typically covers the staggering legal defense costs, protecting you from financial ruin even if you're ultimately proven innocent.

The most powerful feature of a high-quality umbrella policy is often its duty to defend. It provides and pays for your legal defense against covered lawsuits, a benefit that can be worth hundreds of thousands of dollars on its own.

What Is Typically Excluded

Of course, knowing what isn't covered is just as important. An umbrella policy is a shield for your personal liability—it’s not a magic wand for every problem.

Common exclusions you'll find are:

- Business and Professional Liability: If you own a business or offer professional advice, you need a separate commercial liability policy. A personal umbrella won't cover lawsuits related to your business.

- Intentional or Criminal Acts: The policy won’t pay for damages you cause on purpose or while committing a crime.

- Your Own Injuries or Property: Remember, this is liability coverage, which means it pays for damages you cause to other people. It won't cover your own medical bills or damage to your own home.

Chubb has built its reputation on handling these kinds of specialized, high-stakes situations. In 2024, Chubb Ltd wrote an immense $33.327 billion in direct premiums in the U.S. property/casualty market. That 3.15% market share is especially concentrated in high-net-worth liability, where their deep expertise directly benefits homeowners in Oregon and Washington. This financial strength gives policyholders confidence that Chubb has the resources to pay when a catastrophic claim hits. You can see their market position for yourself in the NAIC's 2024 market share report.

Even with a top-tier carrier, legitimate claims can get complicated. If your insurer is undervaluing your claim or pushing back unfairly, it’s important to know your options. Our guide on how to fight an insurance claim denial can help you understand the next steps.

Real-World Scenarios Where Umbrella Insurance Is a Lifesaver

Policy documents and definitions are one thing, but seeing how insurance plays out in real life is another. To really understand the value of a Chubb insurance umbrella policy, you have to look at situations where it becomes the only thing standing between a family and financial ruin.

Let’s move away from the abstract and into some true-to-life examples that happen right here in Oregon and Washington. These stories show just how quickly an ordinary day can spiral into a multi-million-dollar liability.

This is where a solid umbrella policy proves it’s more than just a piece of paper—it’s a financial lifeline.

The Portland Backyard Party Lawsuit

Imagine you're hosting a summer barbecue in your Portland backyard. It's a perfect evening until a guest trips on a sprinkler head that didn’t quite retract into the lawn. It sounds minor, but the fall results in a severe spinal injury. The initial hospital bills are shocking, but the long-term costs are what create a financial nightmare: permanent mobility issues, years of physical therapy, and the inability to return to a physically demanding job.

The injured guest’s attorney files a lawsuit seeking $1.5 million to cover medical care, lost future earnings, and pain and suffering. Your standard homeowners policy carries a respectable $500,000 liability limit, which your insurer promptly pays. The problem? You're still on the hook for the remaining $1 million.

Without an umbrella policy, that Portland family would be looking at liquidating their retirement accounts, selling their home, and having their wages garnished for years to satisfy the court judgment. Instead, their Chubb umbrella policy kicks in. It covers the entire $1 million gap and pays for the costly legal defense, preventing a single accident from destroying their financial future.

The I-5 Chain Reaction Crash

Here’s another all-too-common scenario. A Vancouver resident is driving on I-5 during a classic Pacific Northwest downpour. Their car hydroplanes, triggering a chain-reaction crash that involves three other vehicles and injures five people.

The aftermath is a tangled mess of claims for hospital stays, vehicle replacements, and lost income. The combined lawsuits soar past their auto policy's $500,000 per-accident limit, and a judge hands down a total judgment of $2.2 million. After the auto insurance pays out, that driver is personally liable for $1.7 million. An amount like that means immediate bankruptcy.

Thankfully, they had a $2 million Chubb umbrella policy. It activates right when their auto policy is exhausted, covering the full $1.7 million shortfall. One terrible moment on a slick highway doesn't have to end in financial ruin. Catastrophic events, like a house fire, also show where extra coverage is vital; a guide like Fire Damage Restoration Tampa: Your Complete Recovery Guide can highlight the sheer scope of recovery costs.

The Online Comment That Sparked a Defamation Suit

It’s not just physical accidents, either. Think about this: a professional in Bend, Oregon, gets frustrated with a local contractor and vents in a public online review, accusing the business of fraud. The comment, posted in a moment of anger, goes viral.

The business owner sues for defamation, claiming the review destroyed their company’s reputation and cost them a massive number of clients. They demand $800,000 in damages. The professional’s homeowners policy offers zero coverage for libel or slander. They’re suddenly facing an $800,000 judgment and have to hire a defense lawyer out-of-pocket, with legal fees climbing by the day.

This is where a high-quality umbrella policy shines. Their Chubb policy includes broad personal injury coverage, which covers defamation. Chubb appoints and pays for a specialized legal team to defend them. In the end, the policy covers the final settlement and all legal fees, protecting their life savings from a single ill-advised comment. These examples show just how complicated claims can get, which is why understanding the entire property damage claim process is so crucial for policyholders.

Navigating a Complex Claim with Expert Help

Choosing a premium Chubb insurance umbrella policy is a smart move for protecting your assets. But here’s something many people in Oregon and Washington learn the hard way: having a great policy doesn't automatically mean you’ll get a great settlement. After a major loss, the claims process can suddenly feel like a fight, even with a top-tier company like Chubb.

At the end of the day, insurance companies are businesses. They have teams of adjusters, investigators, and lawyers working to protect their financial interests. That means any large claim—especially one that might tap into an umbrella policy—will be put under a microscope. This is where the power dynamic can tip, leaving you at a serious disadvantage.

Why You Need an Advocate in Your Corner

Your insurance company has a team of experts on their side. You should too. This is exactly why licensed public adjusters exist—they are insurance professionals who work exclusively for you, the policyholder, never for the insurance company.

For property owners in Oregon and Washington, a firm like NW Claims Management serves as your personal advocate. Their entire job is to level the playing field, managing every part of your claim to get you the best possible outcome. They turn a stressful, confusing process into a clear, strategic plan for recovery.

Here’s what an expert public adjuster brings to the table:

- Deep Policy Interpretation: They dig into the fine print of your Chubb policy, finding every bit of coverage you're entitled to by understanding the complex language, endorsements, and exclusions.

- Meticulous Loss Documentation: They professionally document the full extent of your damages, so nothing gets missed. A detailed home inventory for insurance claims is an invaluable tool in this process, helping to create a complete record of what was lost.

- Expert Negotiation: They take over all communication with the insurer’s representatives, pushing back against low offers and weak arguments to make sure you get paid what you're truly owed.

Leveraging Expertise for Maximum Recovery

Chubb's financial strength is a big reason its policies are so respected. With a P&C underwriting income that reached $5.9 billion in 2024 and payouts of $17 billion in claims each year, the company has the resources to pay. You can explore Chubb's 2024 annual report to see their financial standing for yourself.

A good public adjuster knows how to use this reliability to your advantage. With decades of experience, firms like NW Claims Management work on a contingency basis to secure the maximum settlement, giving you the funds you need to rebuild your life.

The single greatest benefit of hiring a public adjuster is that it places a seasoned professional on your side of the negotiating table, ensuring your interests are represented with the same level of expertise as the insurance company's.

By managing the entire claims process for you—from the first assessment to the final check—a public adjuster lifts a massive administrative burden off your shoulders. They handle the endless phone calls, paperwork, and meetings, freeing you to focus on what really matters. Knowing the signs of a complex claim is the first step, and learning when to hire a public adjuster can make all the difference in your financial recovery.

Frequently Asked Questions About Chubb Umbrella Policies

Even with a good grasp of how a Chubb insurance umbrella policy works, you're bound to have a few more questions. That’s perfectly normal. This is a major piece of your family’s financial security, so getting the details right is what matters. We've compiled the questions we hear most often from our clients in Oregon and Washington to give you clear, straight-to-the-point answers.

Think of this as the final walkthrough, helping you connect the dots on cost, qualifications, and some of those tricky "what if" scenarios.

How Much Does a Chubb Umbrella Policy Cost?

This is usually the first thing people want to know, and the short answer is: it really depends. The price of a Chubb umbrella policy is tailored to your specific risk profile, so there’s no single sticker price. That said, most people are pleasantly surprised by how affordable this level of protection actually is.

For the first $1 million in coverage, you can generally expect to pay somewhere between $200 and $500 per year. The good news is that each additional million dollars of coverage gets progressively cheaper. In other words, jumping from $1 million to $2 million will cost less than that first million did.

So, what moves the needle on your premium? Chubb looks at a handful of key factors:

- Your Footprint: The more homes and cars you insure, the more potential for a claim, which nudges the premium up.

- Household Risks: Having teenage drivers is a big one. Statistically, they represent a higher risk on the road.

- Attractive Nuisances: Things like a swimming pool, trampoline, boat, or even certain dog breeds can increase liability risk and your premium.

- Your Personal Record: Your driving history matters. A track record of accidents or tickets will signal higher risk to the underwriters.

Ultimately, your premium is a direct reflection of the risk the insurer is taking on. Chubb’s underwriting process is all about pricing that risk accurately based on your lifestyle.

How Do I Qualify for a Chubb Umbrella Policy?

Getting a Chubb umbrella policy isn’t about being wealthy; it’s about being responsible. Because an umbrella policy sits on top of your existing insurance, Chubb needs to see that you have a solid foundation in place first. This is where your "underlying limits" come into play.

To qualify, you’ll need your primary home and auto policies to meet certain minimum liability limits. It’s like building a house—you can’t put the roof on before the walls are up.

While the exact numbers can shift, here’s what Chubb typically requires:

- Auto Insurance: You’ll need at least $250,000 in bodily injury liability coverage per person and $500,000 per accident.

- Homeowners Insurance: Your personal liability coverage should be at least $300,000 to $500,000.

Think of these underlying limits as the deductible your primary auto or home insurer pays before your umbrella policy even sees the claim. If your current limits are below these minimums, don't worry. You'll just need to contact your agent and raise them before you can add the umbrella coverage.

Qualifying for a Chubb umbrella policy is less about your net worth and more about demonstrating that you are a responsible risk. Meeting the underlying limit requirements is the most critical step in the process.

Does Umbrella Insurance Cover Me When I Travel Abroad?

Yes, and this is one of the standout features of a policy from a global insurer like Chubb. For most policyholders, your liability protection has worldwide coverage.

This is a huge deal. It means if you cause a serious accident while driving a rental car in Italy, your Chubb umbrella can cover a massive judgment that far exceeds the local insurance you were required to get. It could also apply if a guest is seriously injured at a vacation home you've rented in another country.

But—and this is important—you should never just assume. Before you travel internationally, make it a habit to call your agent. A quick conversation to confirm your policy’s coverage territory can save you from a life-altering financial disaster thousands of miles from home.

Can I Have an Umbrella Policy Without Auto Insurance?

This question comes up a lot, especially from people living in cities like Portland or Seattle who've ditched their cars. In almost all cases, the answer is no. Most insurers, Chubb included, require you to carry both an auto and a home (or renters/condo) policy to be eligible for a personal umbrella.

The logic is simple: car accidents are the number one source of multi-million dollar liability claims. By requiring you to have a solid auto policy in place, the insurance company ensures the most common and expensive risk is already covered before they add that extra layer of umbrella protection.

If you don't own a car but still drive occasionally—using rentals or borrowing a friend's car—you're not out of options. Look into a "non-owner" auto insurance policy. It's designed for exactly this situation and can often satisfy the underlying auto insurance requirement, clearing the way for you to get the umbrella policy you need.

When you're facing the overwhelming stress of a major property damage claim, you don't have to go it alone. The expert team at NW Claims Management is here to advocate for you, ensuring you receive every dollar you're entitled to under your policy. Contact us today for a free claim evaluation and let us handle the fight for your fair settlement.