You open the claim email, read the settlement figure, and your stomach drops. The insurer says your truck is a total loss, or says the repair is complete and your car is “back to pre-loss condition,” but the number doesn't match what you know that vehicle was worth in Portland, Seattle, Spokane, Bend, or anywhere else in the Pacific Northwest market.

When a vehicle's value is in question, a search for an auto appraisal company begins. This isn't driven by a desire for paperwork, but rather by the necessity for an advantage in negotiations.

Vehicle claims often turn on value, and value is where disputes start. If the carrier's number is too low, every next step gets harder. Your loan payoff, your replacement vehicle, your resale loss after repairs, even your willingness to sign the release all depend on whether the valuation is defensible.

What Is an Auto Appraisal Company and Why Do They Matter

A policyholder usually meets an auto appraisal company at the worst time. The car was just totaled. Repairs were sloppy. A diminished value claim got brushed aside. Or a classic or modified vehicle got valued like a plain commuter car.

An auto appraisal company is an independent valuation service that documents what a vehicle is worth and why. In claims work, that matters because the insurer controls the claim decision and also funds the payment. When the same side determines the value, a second set of eyes becomes more than helpful. It becomes a check on the process.

The real problem behind the dispute

Here's the pattern I see in disputed vehicle claims. The owner isn't always arguing that the insurer acted in bad faith. Often, the owner is saying something simpler: “You missed important facts about my vehicle, my market, or the quality of the repair.”

That's where a proper appraisal changes the conversation. A credible appraiser doesn't just throw out a higher number. They inspect the vehicle, review records, compare market data, and explain the reasoning in a format that can hold up in negotiation.

Practical rule: If the other side can't explain how they reached the number, you shouldn't trust the number.

This isn't some fringe corner of the market. One established firm, Auto Appraise, Inc., was founded in 1991 and advertises a nationwide network of over 250 appraisers, with an estimated annual revenue of about $26.5 million and an estimated valuation of $84.5 million, which shows how independent appraisal has grown into a significant specialty rather than a niche side service (Auto Appraise company profile).

What the appraiser does for you

A good appraiser serves a role similar to any other independent claims expert. They gather evidence, apply method, and produce a report that can support your position.

That's especially important when you need more than a casual opinion. If you're dealing with a total-loss dispute, diminished value issue, or post-repair disagreement, a service focused on auto insurance appraisals is built for that kind of conflict, not just private-party pricing.

If you want to understand the valuation side better before you hire anyone, AutoProv's guide on expert car valuation techniques is a useful primer on how serious vehicle pricing work is supposed to be approached.

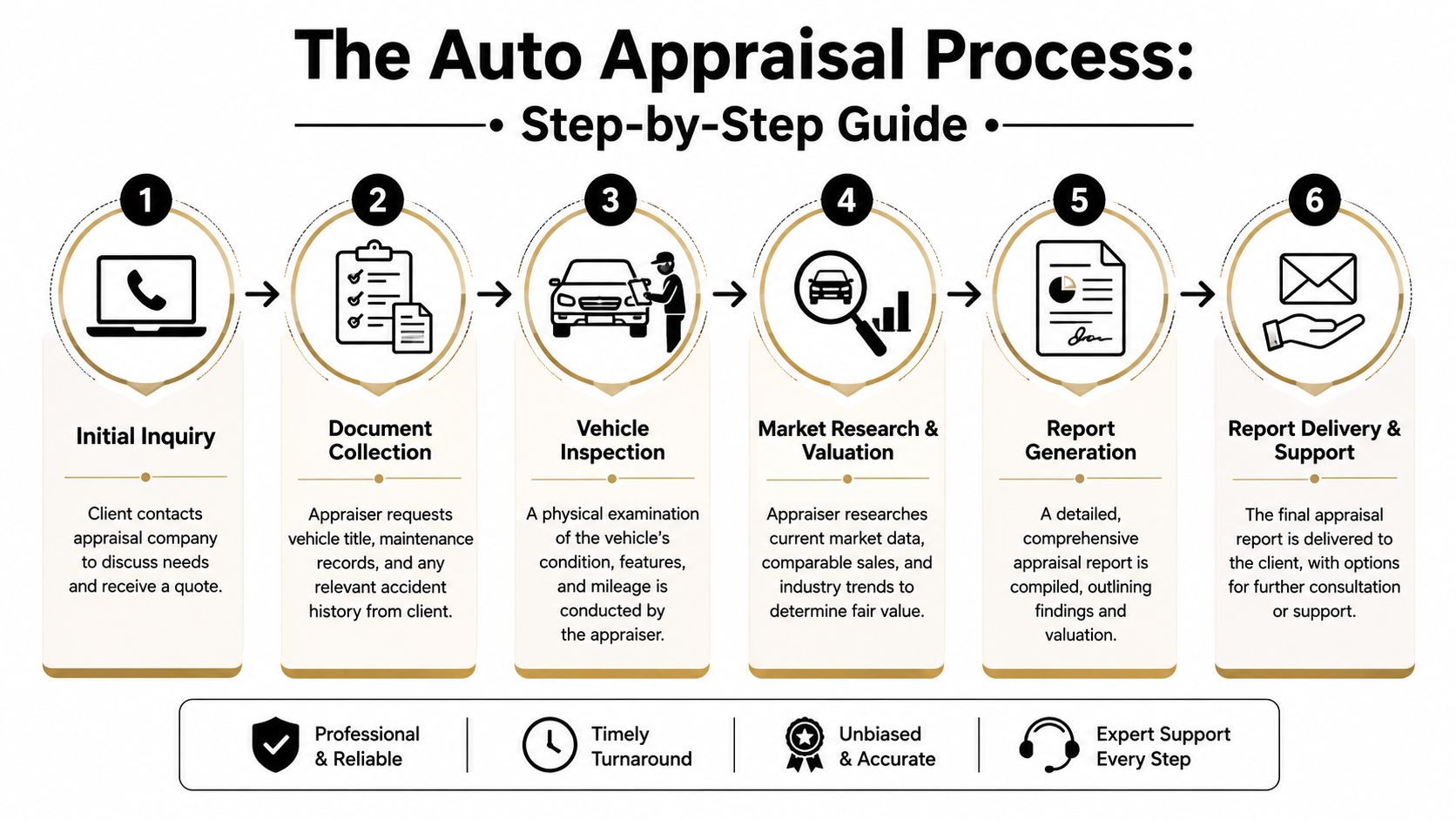

The Auto Appraisal Process from Start to Finish

Many drivers assume an appraisal is one quick look at the car and a number at the bottom of a page. That's not how a defensible report is built.

A solid appraisal follows a sequence. Each stage matters because weak inputs lead to weak conclusions. If the inspection is rushed, the market research won't fix it. If the records are incomplete, the final value may still be vulnerable.

Step one through three

Initial contact

You explain the dispute, the vehicle, and the purpose of the appraisal. A serious firm will ask whether this is for total loss, diminished value, repair quality, pre-purchase review, or another use. That matters because the scope changes the report.Document collection

The appraiser should ask for the title or registration, mileage, repair records, maintenance history, accident information, and photos if available. If the vehicle has upgrades, restoration work, or aftermarket parts, that documentation needs to be gathered early.Inspection method selection

Claims operations increasingly use both remote and in-person methods. Sedgwick and Travelers emphasize digital appraisal capabilities, and Travelers notes that virtual inspection can be the quickest resolution path when appropriate, while more complex losses still call for field inspections (digital auto appraisal practices).

What happens during the inspection

The inspection is where an auto appraisal company proves whether it knows what it's doing.

Industry guidance points to a dual-track workflow. The appraiser inspects the vehicle physically or virtually, then cross-checks those findings against market data. The inspection should cover body condition, engine performance, interior quality, mileage, modifications, and supporting records such as maintenance history, accident history, and restoration receipts. The report should also include the inspection date and location, valuation date, methods used, appraiser qualifications, and photo documentation so the result is defensible in a dispute (car appraisal workflow details).

A rushed walkaround misses what moves value. Prior paintwork. Incomplete repair. Non-OEM parts. A branded history issue. A documented maintenance file that supports a stronger number. Those details matter.

How valuation is built after inspection

Once the physical facts are pinned down, the appraiser works the market side. That means checking comparable vehicles and filtering out bad comps.

Not every listing is a real comparable. A clean-title Oregon vehicle with strong service records isn't the same as a similar model with weaker history in another market. A heavily modified truck in eastern Washington may appeal to a different buyer pool than a stock commuter sedan in downtown Portland.

A report is only as good as the comparables and assumptions behind it.

This is why policyholders often benefit from working with firms that handle broader auto claim solutions rather than generic valuation alone. In a dispute, the report has to answer the practical question: will this hold up when the insurer pushes back?

What you should receive at the end

Expect a written report, not a casual email estimate. It should show:

- Vehicle identity with VIN, year, make, model, mileage, and relevant options

- Condition findings with notes on damage, repair quality, wear, or upgrades

- Photo support that documents what the appraiser observed

- Methodology showing how the final value was reached

- Qualifications establishing who performed the work

If you don't see those pieces, you may have paid for an opinion that won't carry much weight.

Independent Appraiser vs The Insurer's Adjuster

These roles get mixed together all the time, and they shouldn't. An insurer's adjuster and an independent appraiser may both inspect vehicles and discuss value, but they do not serve the same client.

The insurer's adjuster works for the carrier. Even when the adjuster is professional and fair, their job sits inside the insurer's claim process. The independent appraiser works for the vehicle owner who hired them.

The difference at a glance

| Factor | Independent Appraiser | Insurance Adjuster |

|---|---|---|

| Who hires them | The vehicle owner or claimant | The insurance company |

| Primary duty | Support a defensible valuation | Administer the insurer's claim decision |

| Focus | Accuracy, supportable market value, condition-specific analysis | Claim handling, estimate review, settlement control |

| Use of report | Negotiation, appraisal clause disputes, arbitration, litigation support | Internal claim evaluation and settlement offer |

| View of unusual vehicles | More likely to isolate modifications, maintenance, or collector factors | More likely to use standardized valuation pathways |

| Post-report support | May explain or defend findings directly | Usually tied to the carrier's position |

Why this distinction matters

A lot of policyholders assume the insurer's adjuster is a neutral evaluator. In practice, the adjuster is part of the insurer's machinery. That doesn't automatically mean the value is wrong. It does mean you should be realistic about allegiance.

The same logic applies in property claims. A carrier adjuster handles the insurer's side of the file. A public adjuster handles the policyholder's side. On the vehicle side, an independent appraiser fills a similar advocacy gap by focusing on evidence that supports your valuation position.

If you want a clearer sense of how damage evaluation differs when the reviewer is working within the carrier structure, look at the role of an auto damage adjuster. That helps explain why these jobs are not interchangeable.

What works and what doesn't

What works is using each role for what it is. Let the insurer's adjuster present the carrier's number. Then test that number.

What doesn't work is assuming the first valuation is the final word, especially when the file involves repair disputes, limited comparables, aftermarket equipment, prior restoration, or a total-loss figure that feels detached from your actual replacement problem.

If a claim turns on value, the side with the better documentation usually controls the conversation.

When You Absolutely Need to Hire an Appraiser

Some claim situations are annoying but manageable. Others are expensive enough that you shouldn't go forward without an independent valuation.

The stakes are not small. Current market trend reporting notes that average collision claims now exceed $4,300, and it projects that three-year-old vehicles will retain around 58% of original MSRP in 2026, which is why even modest valuation disagreements can mean thousands of dollars in a total-loss or diminished value dispute (2026 auto market projections and appraisal impact).

Four situations where delay hurts you

Total-loss offers that feel low

This is the most common trigger. If the insurer totals the car and the offer doesn't line up with the actual replacement market, don't argue from memory alone. Get a report.

Owners often know their own vehicle history better than anyone else. They know the new tires were just installed. They know the service records are complete. They know the body and interior were above average. If the offer doesn't account for those facts, the appraisal can.

Diminished value after repairs

A repaired vehicle can still lose resale value. That's especially true when the damage history becomes part of the car's story, even if the body shop did respectable work.

People often make a costly mistake by focusing only on the repair bill and forgetting the market stigma attached to an accident history. An appraiser can isolate that loss in a way a body shop invoice cannot.

Classic, collectible, or modified vehicles

Standard valuation systems often struggle with non-standard vehicles. Lift kits, restoration work, specialty wheels, engine builds, or collector status can be undervalued or ignored if the valuation process treats everything like a stock commuter car.

For these vehicles, inspection depth matters more than speed. The person valuing the car needs to understand what adds value, what merely adds cost, and what narrows the buyer pool.

Pre-purchase and post-repair disputes

Not every appraisal is tied to an insurer. Buyers use appraisers to avoid overpaying. Owners use them after repairs when they suspect hidden issues, poor finish quality, or missed structural concerns.

If you need help locating outside inspection options for a transaction or dispute, this directory can help you find independent vehicle inspectors in a more structured way than random search results.

When it's probably worth the cost

Hire the appraiser when the value dispute is material to your finances, when the vehicle has unusual characteristics, or when the insurer's explanation is thin. Don't wait until you've already accepted the settlement and signed away your negotiating power.

A lot of people ask whether hiring an appraiser is “worth it.” The better question is whether relying only on the insurer's number exposes you to a larger loss.

How to Select a Reputable Auto Appraisal Company

Most appraisal websites say the same things. Fast turnaround. Insurance help. Nationwide service. Expert reports. That language doesn't tell you whether the company can produce a valuation that survives pushback.

The better question is the one many sites don't answer clearly: what makes the valuation persuasive? That's the core consumer issue in this field. A defensible auto appraisal company should be able to explain its methodology, credentials, and how its reports are structured to persuade insurers and courts in total-loss or diminished-value disputes (consumer guidance on persuasive auto valuations).

Ask for proof, not slogans

A reputable firm should be comfortable showing you a redacted sample report. You're looking for structure, not branding.

Check whether the report includes:

- Inspection specifics such as date, location, and condition findings

- Photographic support that clearly documents what was observed

- Valuation method that shows how comps were chosen and adjusted

- Appraiser identity with qualifications and signature

- Dispute readiness showing whether the report is built for negotiation, appraisal clause use, or testimony if needed

If the company won't show a sample, that's a warning sign.

Questions that separate strong firms from weak ones

Use a short list and listen closely to the answers.

Who performs the inspection

Is it a trained local appraiser, or is the company mostly a scheduling layer that outsources the hard part?How do you handle unusual vehicles

Modified trucks, collector cars, and prior repaired vehicles need more than template treatment.Will you explain your comparables

Good firms can discuss why a comp was used or rejected.Can you support the report after delivery

A report that no one will defend has limited value in a live dispute.

A persuasive appraisal is not the one with the highest number. It's the one with the strongest reasoning.

Look for dispute capability

Some companies are fine for private-sale pricing and weak in contested claims. That distinction matters.

An independent adjusting company may also understand the broader claims context, including documentation standards, insurer objections, and how a report gets used once the disagreement starts. That doesn't replace checking the actual appraisal product, but it does help you evaluate whether the company understands real-world claims pressure.

What doesn't inspire confidence

A few red flags show up repeatedly:

| Warning sign | Why it matters |

|---|---|

| Instant value with no real inspection | Fast isn't the same as defensible |

| No sample report available | You can't judge report quality |

| Vague talk about “industry standards” | They should name the method, not just gesture at one |

| No post-report support | Disputes rarely end at report delivery |

Oregon and Washington Specifics for PNW Drivers

Drivers in Oregon and Washington face the same basic valuation problems as everyone else, but the practical context is local. Market conditions vary between metro and rural areas. So do repair networks, comparable vehicle availability, and how quickly claims move when the file gets contested.

Why policy language matters here

The first thing to check is your policy. Some auto policies include an appraisal clause that can become important when you and the insurer disagree on value. The clause language, timing, and procedure matter. So does whether the dispute is about the amount of loss, repair quality, or a related issue the carrier says falls outside the clause.

That means Oregon and Washington drivers shouldn't treat appraisal as a generic service. It needs to fit the claim posture, the policy wording, and the likely route the dispute will take.

The useful comparison to property claims

The analogy to a public property adjuster helps clarify this.

In a property claim, a public adjuster works for the policyholder, not the insurer. They interpret policy language, document the loss, and advocate for a fair settlement. In an auto claim, an independent appraiser fills a similar role on the valuation side. They don't replace your lawyer, and they don't become the insurer's evaluator. They bring an owner-centered, evidence-based position into a process that otherwise tilts toward the carrier's valuation.

That comparison matters because many Oregon and Washington policyholders already understand why independent representation helps in a fire, water, or storm claim. Vehicle disputes are different in subject matter, but the logic is the same.

A local practical step

If you're in the Pacific Northwest and the claim is already becoming a fight, get local guidance early. That may mean an appraiser, a lawyer, or a policyholder-side claims professional depending on the issue. For broader claim advocacy in the region, a search for a claims adjuster near me should lead you toward policyholder-side help rather than only carrier-side contacts.

One Oregon and Washington option in this space is NW Claims Management, which also offers auto appraisal support connected to claims work through its Claim Complete Auto Appraisals service.

Common Questions About Auto Appraisals

Is an appraisal worth paying for

If the dispute is minor, maybe not. If the settlement number affects your replacement vehicle, loan balance, resale loss, or repair dispute, the appraisal often becomes a cost-control move rather than an extra expense. The point is to prevent a larger loss.

How long does it take

That depends on access to the vehicle, how quickly you provide records, whether the inspection is virtual or in person, and how complex the market research is. Straightforward files move faster than disputed, unusual, or poorly documented ones.

What if the insurer rejects the report

That happens. Rejection doesn't automatically mean the report is weak. It may mean the insurer disagrees with the comparables, the condition adjustments, or the scope of the dispute.

Your next move is usually to ask for a written response to the appraisal's reasoning, not just a blanket denial. From there, you may use the report in negotiation, invoke the appraisal clause if your policy allows it, or escalate with legal help if the case warrants it.

What should I do before I hire anyone

Gather your records first. Keep photos, repair invoices, maintenance history, and the insurer's valuation documents in one place. Ask for a sample report. Ask who will inspect the vehicle. Ask whether the company will stand behind the report if the file gets contested.

If you're dealing with a disputed claim in Oregon or Washington and need policyholder-side guidance, NW Claims Management helps insureds evaluate claim issues, document losses, and understand when independent valuation support makes sense. Start with a direct conversation about the dispute, the policy, and what evidence will move the claim forward.