The tow truck is gone. Your car is in a lot somewhere. Your phone is full of photos, claim numbers, and voicemails. You've already told the story three times, and now the insurance process starts asking for the same details again in slightly different ways.

That's the moment many drivers start looking for auto claim solutions. Not because they want a fancy system, but because they want the mess to stop. They want the car fixed, the value paid correctly, and the claim closed without getting pushed into a bad decision.

I'll be direct. A claim is never just paperwork. It's a negotiation about money, scope, timing, and proof. In auto claims, the stakes feel immediate because you need transportation. In property claims, the same issues get bigger fast. The damage is harder to measure, the policy language gets denser, and the insurer's financial incentive doesn't disappear just because your loss is serious.

Navigating the Aftermath of an Accident

Right after a crash, the smartest move is to slow down and get organized. Adrenaline makes people forget simple things. They miss photos, accept vague instructions, or assume the insurer will automatically handle everything fairly.

Start with the basics. Confirm safety, document the scene, gather names, insurance details, vehicle information, and witness contacts. Then preserve every document that follows. Estimates, emails, towing invoices, rental receipts, medical notes, and adjuster communications all matter because claims get decided by what you can show, not by what you remember.

If you need a practical checklist, this guide on what to do after car accidents is useful because it walks through the early decisions that often affect the claim later. Those first hours matter more than people think.

What auto claim solutions really mean

Many hear “auto claim solutions” and think of an app, a repair shop, or a claims hotline. That's too narrow. The solution is the path you choose once the claim begins.

You can:

- Handle it yourself and manage the paperwork directly

- Rely on the insurer's process and accept their adjuster's direction

- Bring in outside help when valuation, liability, or repair scope starts to drift against you

That choice matters because the dollars involved are not small. According to Verisk's claim severity analysis, auto insurance claim severity is increasing at rates that substantially exceed the decline in claims frequency, and the average total cost for repairable claims reached $4,774 in the first half of 2025.

Practical rule: The earlier you document thoroughly, the harder it is for anyone to shrink the claim later.

Why the process feels harder than it should

Insurers want consistency. Policyholders want fairness. Those goals overlap sometimes, but not always.

An adjuster may focus on approved procedures, preferred vendors, and internal timelines. You're focused on whether the estimate reflects the loss, whether the damage was fully identified, and whether the settlement gets you back where you were before the accident. Those are not the same thing.

If you want a better sense of how vehicle damage gets evaluated, a resource on auto damage adjuster services can help you understand what adjusters look for and where disagreements usually begin.

Understanding Your Options After a Claim

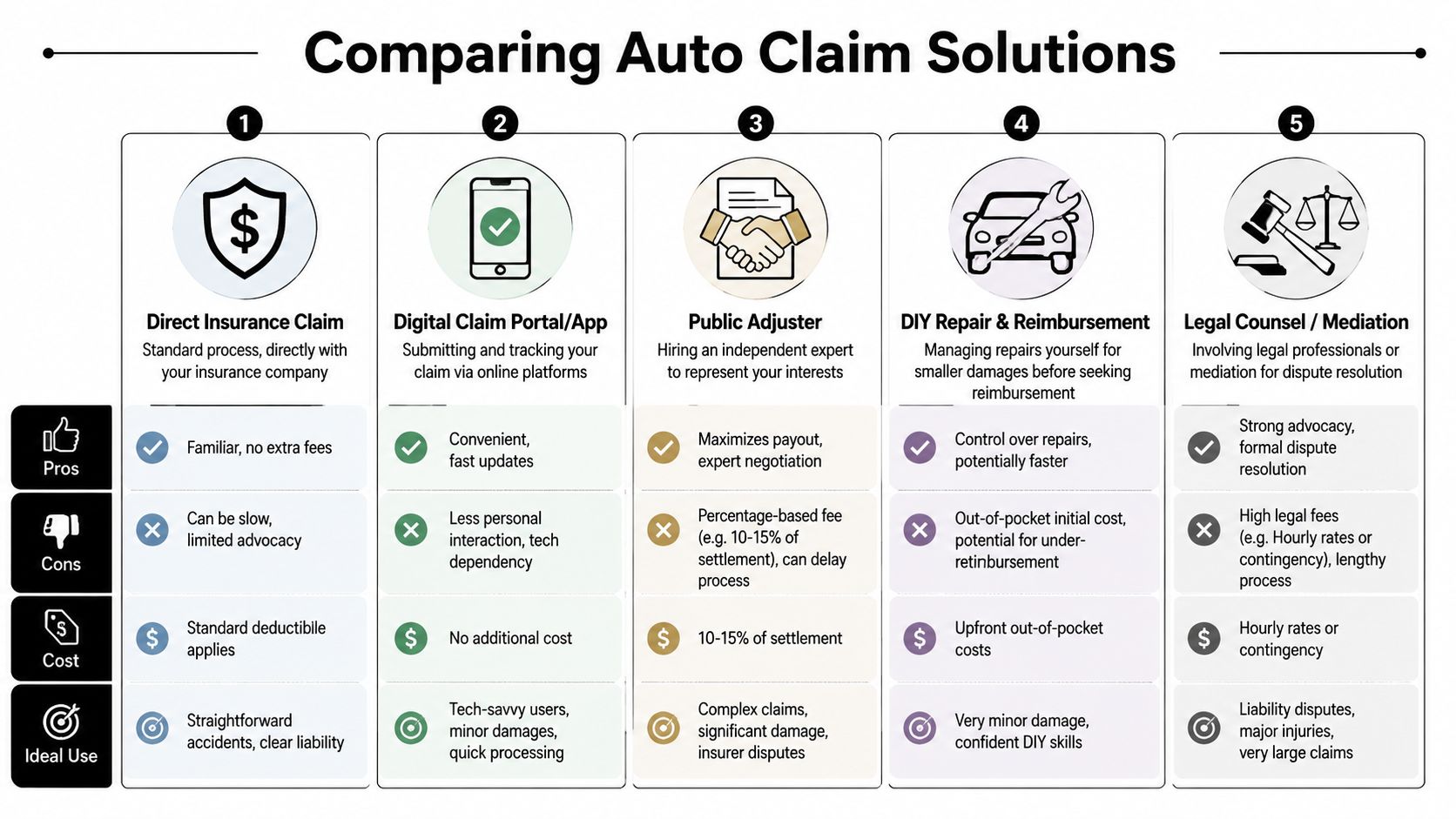

An auto claim doesn't give you one route. It gives you several. That's why auto claim solutions is the right phrase. You're not buying a product. You're choosing a guide.

Some people take the solo route. Some accept the guide provided by the other side. Some hire their own. The right choice depends on the claim, not on what feels easiest in the first phone call.

Three broad paths

Think of it this way:

| Path | Who leads | Best fit |

|---|---|---|

| Going alone | You | Small, clear, low-conflict claims |

| Using the insurer's process | Insurance company adjuster | Straightforward claims where scope and value are obvious |

| Hiring your own expert | Your advocate | Disputed, high-value, or technically messy claims |

The reason this matters is simple. The market is seeing fewer claims in some categories, but each serious claim carries more weight. According to Autobody News reporting on industry claim trends, total auto claims counts were down 8.5% year-over-year through August 2025, while total loss claims as a percentage of all claims excluding broader physical damage scenarios rose to over 23%.

That means the average consumer can't afford to treat a claim casually. If your car is close to a total loss, if the repair methodology is disputed, or if value is being compressed, the “easy” route can become expensive.

The question to ask first

Don't start with “Who can open the claim fastest?”

Start with this instead: Who is responsible for protecting my outcome?

That question changes everything. A digital claims portal might be convenient. An insurer adjuster might sound helpful. A shop might want to move repairs along. But convenience isn't the same as advocacy.

If valuation is already becoming an issue, it helps to understand how auto insurance appraisals work, because disputes often turn on documentation, comparable values, and the method used to measure the loss.

Comparing Your Claim Solution Paths

Most claim advice is too polite. It pretends all paths are roughly equal and you just need to “communicate well.” That's not true. Different paths produce different outcomes because the people involved answer to different incentives.

Path one, DIY filing

This is the cleanest route on paper. You report the loss, collect estimates, submit documents, and push the file forward yourself.

DIY works when liability is obvious, damage is limited, and you have time to stay on top of every detail. It fails when the insurer starts narrowing the scope or pushing a valuation you don't know how to challenge.

Pros

- No outside fee: You keep direct control

- Fast start: No need to onboard another professional

- Useful for simple matters: Good for minor damage and short claims cycles

Cons

- You carry the burden: Every missing receipt, photo, and follow-up lands on you

- You may not spot underpayment: Many people don't know what was omitted until it's too late

- Emotional fatigue: A claim becomes a second job fast

Path two, insurer staff adjuster

This is the default route. Many assume it's neutral. It isn't. The insurer's adjuster works inside the insurer's system, under the insurer's standards, and with the insurer's cost controls.

That doesn't make every adjuster dishonest. Many are professional and courteous. But courtesy doesn't erase alignment.

The most important question in any claim is not who sounds helpful. It's who they work for.

A useful breakdown of that difference appears in this guide on public adjuster vs insurance adjuster. The distinction sounds technical until money is on the line. Then it becomes the whole game.

Path three, independent adjuster

People often confuse independent adjusters with public adjusters. They are not the same. An independent adjuster is usually hired by the insurance company on a contract basis. They may be outside the carrier's office, but they are still handling the claim for the insurer.

This path can help the insurer move volume or address catastrophe claims. For the policyholder, the practical issue remains the same. The adjuster is not your advocate.

Use this path with caution when:

- The loss has multiple layers of damage

- You're getting mixed messages from different claim handlers

- The estimate changes without a clear explanation

Path four, public adjuster or attorney

This is the route people usually wait too long to consider. A public adjuster represents the policyholder. An attorney addresses legal disputes. They are not interchangeable, but both change the power dynamic because they answer to you, not the carrier.

The conflict-of-interest issue gets ignored in most mainstream claims advice. Yet one source discussing that gap states that insurer adjusters have incentives to minimize payouts, while public adjusters work on a contingency basis aligned with the client's recovery, and that this distinction can lead to settlements 20% to 40% higher for policyholders who hire their own advocate, as discussed in this review of insurance billing and claim challenges.

That doesn't mean every claim needs outside representation. It means serious claims deserve a serious look at representation before you lock in a bad number.

Path five, repair shop-led claim handling

Some repair shops are excellent at helping move a claim. They know supplements, labor lines, teardown issues, and parts disputes. That can be valuable. But a shop's expertise is centered on repair, not necessarily on your broader financial position.

This becomes obvious when parts quality becomes an issue. If you're weighing replacement options, understanding the quality of aftermarket vs OEM parts can help you ask better questions about fit, safety, warranty concerns, and long-term value.

A plain comparison

| Claim path | Main strength | Main weakness | Best for |

|---|---|---|---|

| DIY | Control | High burden on you | Minor, clean claims |

| Insurer staff adjuster | Familiar process | Built-in loyalty to carrier | Basic claims with little dispute |

| Independent adjuster | More field capacity | Still not your advocate | Carrier-managed overflow or catastrophe work |

| Public adjuster or attorney | Stronger advocacy | Added fee or legal cost | Complex, disputed, high-value claims |

| Repair shop-led help | Technical repair input | Narrow scope of advocacy | Repair-focused disputes |

Bottom line: If the claim is simple, keep it simple. If the claim is expensive, disputed, or getting narrowed, stop treating it like a customer service issue. It's a representation issue.

How to Choose the Right Path for Your Claim

Picking the right path doesn't require industry jargon. It requires honesty about three things: the value of the claim, the complexity of the damage, and your own capacity to manage conflict.

Start with claim size and complexity

A scraped bumper is one thing. A multi-panel impact, frame concern, airbag deployment, diminished value issue, or total loss dispute is another.

Use this simple filter:

- If the damage is minor and visible, DIY may be enough.

- If the damage is technical or hidden, get outside opinions before accepting the first scope.

- If the car may be totaled or the value feels off, don't rely on convenience. Review the numbers carefully.

- If the insurer changes adjusters, delays decisions, or keeps asking for the same file again, assume the process is drifting and tighten your documentation.

Measure your own bandwidth honestly

A lot of people could manage their own claim if they had spare time, energy, and patience. Most don't. They're working, arranging transportation, dealing with family logistics, or trying to recover physically.

That matters. A claim handled poorly because you were exhausted is still a poorly handled claim.

Ask yourself:

- Do I have time to chase updates and challenge mistakes?

- Can I read estimates closely enough to spot omissions?

- Am I comfortable pushing back when the insurer says no?

If the answer is no, that's not a personal failure. It's a sign to get help.

Red flags that should change your path

You don't need to hire someone the moment a claim opens. But you should escalate when the facts justify it.

Watch for:

- A quick offer before the full damage is documented

- Pressure to use a specific process without a clear explanation

- Repair methods or parts you're not comfortable accepting

- Conflicting statements from adjusters, shops, or appraisers

- Long periods of silence followed by rushed deadlines

Don't choose the cheapest path first. Choose the path most likely to protect the full value of the claim.

The best auto claim solutions are matched to the claim in front of you, not to the insurer's preferred workflow. That same decision logic becomes even more important once the loss involves a building instead of a vehicle.

Decoding Insurer Tactics and Protecting Your Rights

Insurers don't have to shout to control a claim. They can do it through process. A low estimate, a narrow scope, a repeated request for documents, or a software-driven flag can have the same effect as an outright denial. They slow you down, wear you out, and make a reduced settlement look reasonable.

Fast doesn't always mean fair

Carriers now use automation aggressively in claims handling. According to this explanation of automated claims processing, modern claims automation systems use AI and machine learning to improve settlement speed by 50% and reduce handling costs by 20% through automated data extraction and severity-based triage.

That sounds efficient, and sometimes it is. But speed for the carrier doesn't guarantee accuracy for you. The same source notes that automation can also become algorithmic gatekeeping that unfairly delays or undervalues legitimate claims without human oversight.

Common tactics and the right response

Here's what I see most often:

Quick low offers: The insurer wants closure before the full picture develops.

Your response: Ask for the full basis of valuation in writing. Don't accept a number you can't trace back to evidence.Scope narrowing: Damage gets framed as smaller, unrelated, pre-existing, or not covered.

Your response: Build a clean record with photos, repair opinions, invoices, and timeline evidence.Delay by repetition: You submit what was requested, then someone else asks again.

Your response: Keep a claim log with dates, names, and attachments sent. Resend from that log, not from memory.Preferred-vendor pressure: You're nudged toward a process that may be easier for the carrier, not better for your outcome.

Your response: Ask whether you have a choice, what standards apply, and what happens if hidden damage appears later.Fraud-style suspicion without clear accusation: Something in the file gets flagged as unusual.

Your response: Push for specifics. Vague doubt should never go unanswered.

A practical consumer-facing overview of these patterns appears in this guide to insurance adjuster tricks. It's worth reading because many tactics look harmless until they stack up.

Protect yourself with a paper trail

You don't win claims by sounding upset. You win them by becoming hard to dismiss.

Build a file that includes:

- Chronology: Dates of loss, inspection, estimate, supplement, and follow-up

- Visual proof: Photos before repair, during teardown, and after any additional damage is discovered

- Written confirmations: Email beats phone calls when the issue is disputed

- Independent opinions: When valuation or repair method is contested, third-party documentation matters

If a claim decision can't be explained clearly in writing, challenge it. Ambiguity usually benefits the carrier, not the policyholder.

Beyond Auto Claims A Look at Property Damage

Auto claims teach people one useful lesson fast. Insurance is not just about reporting a loss. It's about proving scope, value, and cause to a company that controls the money. That lesson becomes much more important when the damaged asset is your house, apartment building, storefront, church, school, or nonprofit facility.

A vehicle claim is usually confined. The damage is visible, the repair ecosystem is established, and the timeline is shorter. Property losses are different. Water travels. Smoke residue spreads. Structural issues hide behind walls and ceilings. Business interruption can turn a building loss into an operating crisis.

Why advocacy matters more in property claims

In Oregon and Washington, weather-driven losses, water intrusion, fire damage, and complex restoration questions can make a property claim far more technical than an auto file. Small mistakes early in the process often lead to major underpayment later.

This gets worse when insurers use data tools to flag claims that don't fit expected patterns. According to this overview of insurance analytics and anomaly detection, insurers use predictive analytics and behavioral anomaly detection to identify potential fraud, but those systems can also misclassify unusual yet legitimate claims. For complex property losses, where the damage pattern may be unique, challenging that kind of decision takes real expertise.

The house version of the same problem

Think about what happens when you spot staining, swelling, or softness in a wall. Those surface clues might point to a much larger issue. A practical maintenance guide on signs of water damage in walls is helpful because it shows how easily visible symptoms can understate the actual problem.

Property claims work the same way. What the insurer sees at first inspection may be incomplete. What the policy covers may depend on language the average owner doesn't read until after the loss. What the building needs to return to pre-loss condition may exceed the initial estimate by a wide margin, even when the first inspection seemed straightforward.

If you want a clearer picture of how these files unfold, reviewing the property damage claim process helps connect the dots between inspection, documentation, valuation, and negotiation.

When to Call NW Claims Management for Your Property Claim

If your property loss is large, technical, or already turning into a fight, call early. Waiting rarely improves your advantage.

Call when the damage involves fire, water, storm impact, vandalism, or hidden structural issues. Call when the building is commercial, nonprofit, municipal, or otherwise hard to value with a simple estimate. Call when the insurer's offer feels low, when communication has stalled, or when you're being asked to accept conclusions that don't match what you're seeing on site.

You should also call when you're overwhelmed. That's not a soft reason. It's a practical one. Serious property claims require documentation, policy interpretation, damage scoping, contractor coordination, and negotiation. Most owners don't have the time or technical background to do all of that while trying to stabilize their home, business, or organization.

For property owners in Oregon and Washington, the right advocate can level the field. The goal isn't drama. It's accuracy, advantage, and a settlement that reflects the loss.

If you're dealing with a property claim in Oregon or Washington and you need experienced advocacy, contact NW Claims Management. They represent policyholders, not insurers, and help homeowners, businesses, nonprofits, and public entities document damage, interpret policy language, and negotiate for a fair payout.