The call usually comes after a brutal day. A pipe bursts in Portland. A kitchen fire shuts down a restaurant in Vancouver. A wind event tears into a retail strip, and by nightfall the owner is standing in a dark building wondering how payroll, rent, vendors, and customers will be handled if the doors stay closed.

That's where a business interruption claim stops being insurance jargon and starts being survival.

If you own a business in Oregon or Washington, you need a clear plan fast. Not a vague promise from the carrier that they'll “take a look.” Not a stack of forms with no explanation. You need to know what triggers coverage, how the loss is measured, what documents matter, and where insurers commonly shave the claim down. That's how you protect cash flow and push for a fair settlement.

Your Business Is Closed Now What

A business closure feels chaotic because every problem shows up at once. The property is damaged. Customers are asking questions. Employees want answers. Bills keep arriving even though revenue has stalled.

In the Northwest, I see the same pattern again and again. A business owner spends the first few days focused on cleanup and emergency decisions, then gets hit with the second crisis: the realization that rebuilding the space is only half the fight. Pressure often comes from the income that vanishes while the business can't operate normally.

That's why your business interruption claim matters. It's the part of the claim designed to address the financial fallout from the shutdown itself, not just the broken roof, soaked flooring, or smoke-damaged equipment. If you also need to spend money to keep operating in some temporary way, review how extra expense coverage works because that issue often runs alongside business income loss.

Your first job is stabilization

Do the practical things first.

- Protect the property: Stop further damage if you can do it safely.

- Notify the carrier: Open the property claim promptly.

- Start a claim file: Save emails, invoices, photos, notes from calls, and any timeline of closure and repairs.

- Track operational fallout: Write down when you stopped serving customers, which departments shut down, and what temporary workarounds you tried.

Practical rule: Treat the first week like evidence collection, not just disaster response.

Don't let confusion become a claim problem

Many owners wait too long to gather the financial records behind the loss because they assume the insurer will figure it out. They won't. The carrier will review what you submit, but the burden to present the loss sits with you.

A business interruption claim can absolutely help keep a damaged business afloat. But only if it's built carefully, documented early, and challenged when the insurer takes shortcuts.

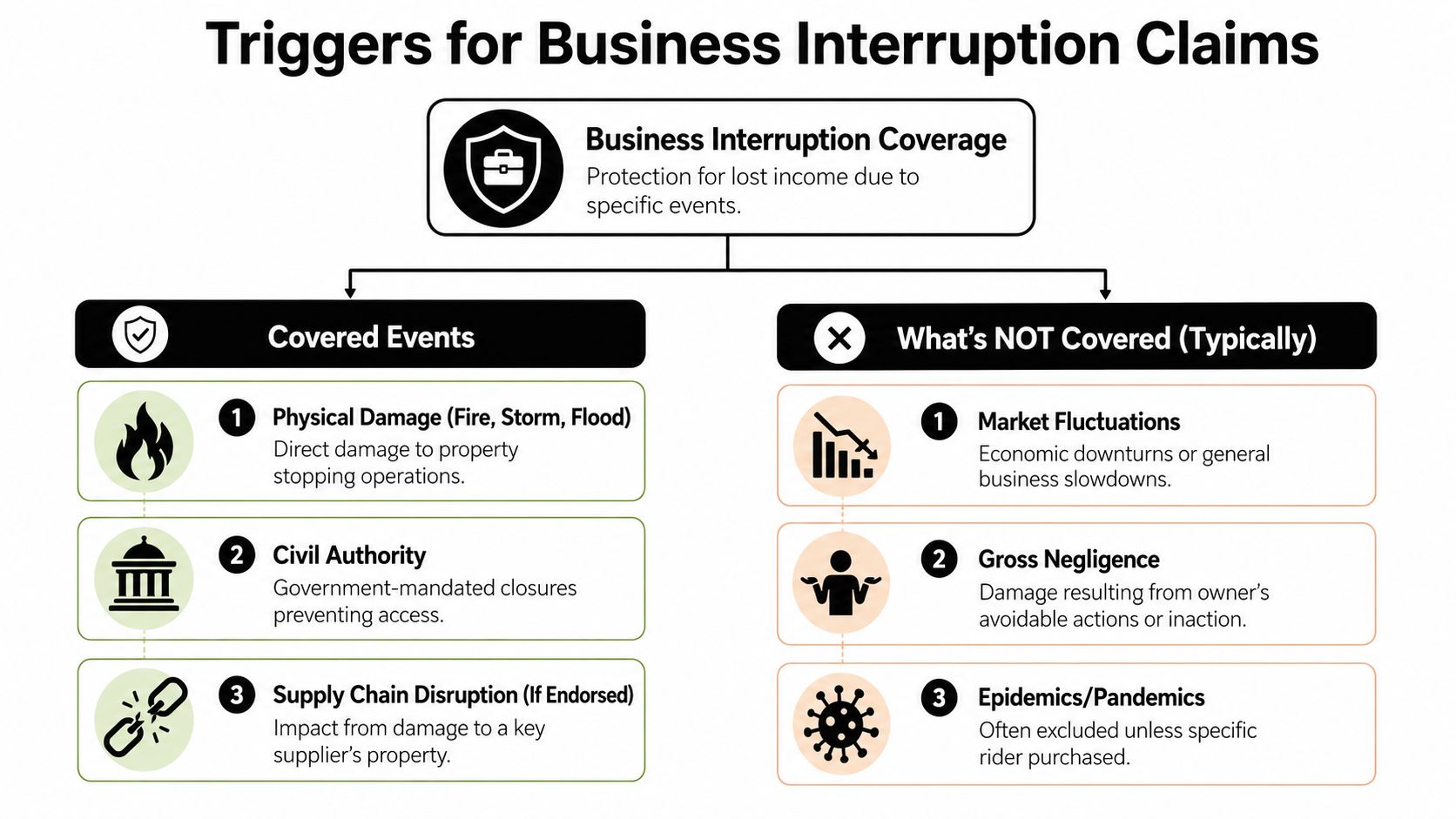

What Triggers a Business Interruption Claim

This part is simple, even if insurers and policy forms make it feel complicated. Business interruption coverage is usually triggered only when direct physical loss or damage hits the insured property from a covered peril, as explained in this business interruption coverage overview.

That requirement is the key. If you don't satisfy that requirement first, the income claim usually doesn't open.

The trigger is property damage first

If a fire burns part of your shop and you can't operate, that's the classic setup. If a storm damages the building envelope and forces closure, same idea. If vandals destroy key parts of the premises and business stops, you may have a path to coverage.

What usually doesn't work is a claim based only on business conditions around the property.

- Government order alone: Usually not enough without the required physical damage.

- Supply chain issues alone: Usually denied unless your policy has specific language that extends coverage.

- Fear of damage: Not enough.

- Virus or pandemic shutdowns: Commonly denied, especially where exclusions apply.

Document the physical damage immediately

If the income portion of the claim depends on the property damage claim, then prove the physical damage first and prove it well.

Use a tight evidence routine:

- Photograph every affected area before cleanup changes the scene.

- Get site access documented if parts of the building are unsafe or inaccessible.

- Preserve contractor findings that explain why operations can't continue normally.

- Tie the damage to the shutdown in writing. Don't assume the carrier will make that connection for you.

The strongest business interruption claims start with a clean, visual, undeniable record of the property loss.

Oregon and Washington owners need to think practically

In Oregon and Washington, weather losses, water damage, fire losses, and utility-related building impacts can all disrupt operations in ways that look obvious to the owner but still get challenged by the insurer. Adjusters often narrow the issue to one question: what exact physical damage prevented normal operations?

Answer that question early.

If the loss involved electrical failure tied to building damage, it can help to understand how commercial systems are maintained and assessed. A useful outside reference is this overview from Reno electrical maintenance contractors, especially when electrical infrastructure plays a role in why a commercial property couldn't function safely after a covered event.

Don't build your business interruption claim on frustration, lost momentum, or rough estimates. Build it on the damaged property that triggered the shutdown.

How Your Business Interruption Loss Is Calculated

Most disputes happen here. Business owners think the claim should equal lost sales. Insurers know it doesn't. The correct calculation sits in the middle, and if you don't understand the math, you'll either overstate the claim and lose credibility or accept an undervalued number.

A technically sound claim measures business income loss as revenue loss minus the expenses that would have been incurred to generate that revenue, and the claim should be supported with two years of historical financial statements, current budgets, and general ledgers during the period of restoration, as explained by the AFERM guidance on preparing a business interruption claim.

Lost revenue is not the same as claimable loss

A restaurant is the easiest example. If the dining room closes after a fire, revenue drops. But the restaurant also may not buy the same amount of food, packaging, or hourly labor while it's shut down. Those are saved variable costs. They matter.

So the core idea is this:

- Projected revenue you would have earned

- Minus expenses you didn't have to spend because the business was interrupted

- Equals the business income loss you're claiming

That distinction protects the integrity of the claim. It also stops the carrier from dismissing your numbers as inflated.

Three moving parts shape the claim

Net income loss

This is the heart of the business interruption claim. You are not asking the insurer to replace every dollar that would have come through the register. You are asking them to pay for the income the business would have generated after accounting for costs tied to producing that revenue.

If your books are messy, this gets ugly fast.

Continuing operating expenses

Some expenses keep going even when the business is partially or fully shut down. Rent may continue. Some payroll may continue. Certain service contracts may continue. These costs often become part of the financial pressure the claim is meant to address, but they still need to be shown clearly in the records.

Extra expenses

Sometimes the smartest move is to spend money to reduce the shutdown impact. Temporary space, short-term equipment, emergency outsourcing, or workarounds can matter. If you need help with the accounting side of that presentation, review forensic accounting services for insurance claims, because the numbers often need to be organized in a way an insurer can't easily dismiss.

The period of restoration matters more than owners expect

Your claim doesn't run forever. It tracks the period of restoration, meaning the time from the direct physical damage until operations resume, based on the policy language and actual recovery facts.

That period becomes a battleground when the insurer says you could have resumed sooner than was realistic.

Claim advice: Don't talk about reopening in broad terms. Tie the timeline to permits, contractor schedules, equipment availability, inspections, and actual operational readiness.

What to gather before the insurer asks

Strong calculation work starts with records, not opinions.

- Historical financial statements: These show how the business performed before the loss.

- Current budgets and forecasts: These help show what management reasonably expected absent the damage.

- General ledgers: These help separate continuing costs from saved costs.

- Department-level detail if available: Especially useful for multi-line businesses with uneven impacts.

- Payroll and purchasing records: These often reveal where variable costs dropped during the closure.

Watch for the insurer's shortcuts

Some adjusters use broad averages that flatten the full story of the business. Others push saved expenses too aggressively and strip out costs that weren't avoided. A careful claim doesn't just plug numbers into a spreadsheet. It matches the financial records to how the business operates.

That's why owners who understand their own margins, seasonality, labor model, and expense structure usually negotiate from a much stronger position.

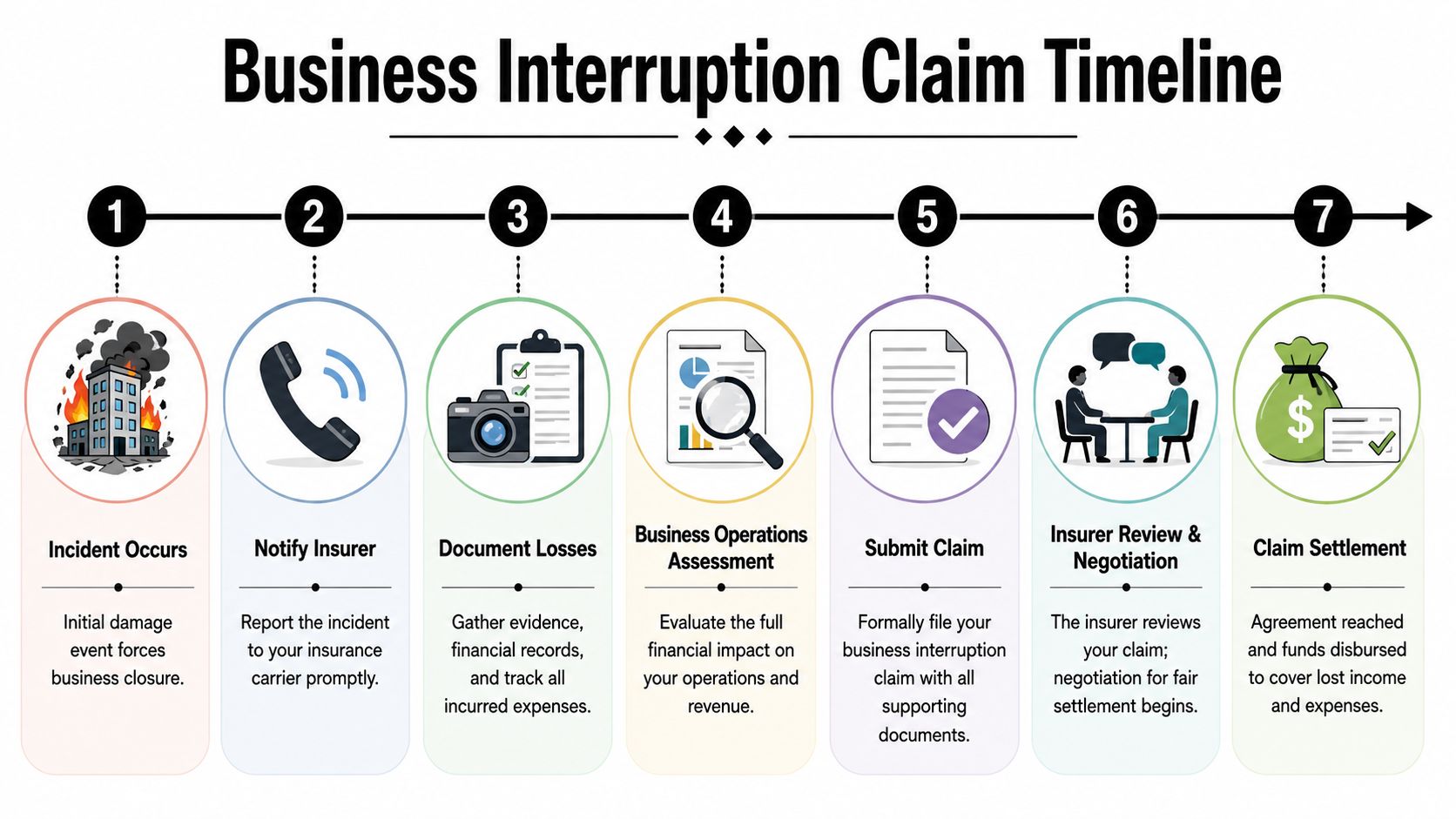

The Step-by-Step Claim Timeline

Once the damage happens, the claim process feels like ten problems at once. It's easier to handle when you break it into stages and treat each one as a task with a purpose.

Phase one starts on day one

The first phase is emergency action.

- Mitigate damage: Board up, dry out, secure, and protect inventory where possible.

- Report the loss: Open the property claim and make sure the carrier knows operations were interrupted.

- Create a timeline: Note when the damage occurred, when operations stopped, and what parts of the business were affected.

This stage shapes everything that follows. If the initial reporting is vague, insurers often use that vagueness later.

Phase two is evidence building

The claim gets stronger when the operational impact is documented as it unfolds, not reconstructed months later.

Keep a running record of:

- Closure dates and partial reopening dates

- Canceled jobs, bookings, or orders

- Staffing changes

- Temporary relocation efforts

- Repair milestones and access limitations

If you want a broader roadmap for the property side running alongside the income claim, review this guide to the property damage claim process. The two tracks are linked more than most owners realize.

Phase three is formal claim presentation

At some point, the insurer will ask for a proof of loss, financial support, or both. Don't rush this just to satisfy a deadline if your numbers aren't ready. Submit a claim package that's organized, backed by records, and clear enough that someone outside your business can follow the logic.

A good package usually includes a narrative, a timeline, financial support, and explanations for unusual items.

Don't hand over a pile of spreadsheets and hope the adjuster understands your business. Spell out how the damage interrupted revenue.

Phase four is review and negotiation

The insurer reviews the claim, asks questions, requests more records, and may present a lower number than expected. That isn't the end of the conversation. It's the start of claim negotiation.

Common pressure points include:

- Duration: The insurer argues you could have resumed sooner.

- Income projection: The insurer uses a weak baseline.

- Expense treatment: The insurer overstates what you supposedly saved.

- Scope linkage: The insurer disputes whether all operational losses tie back to the physical damage.

Phase five ends only when the numbers make sense

Settlement should follow evidence, not exhaustion. Too many owners accept a low figure because they're tired, cash-strapped, and trying to get back to running the business.

That's understandable. It's also expensive.

Stay disciplined. Every stage of the timeline should produce documentation that supports the next stage. When done right, the file tells the story for you.

Essential Documents for a Strong Claim

Documentation wins these claims. Not passion. Not frustration. Not a long explanation on a phone call with the adjuster.

If your records are thin, the insurer gets room to make assumptions. Those assumptions usually help the insurer, not you.

Build a claim file that proves the business before and after the loss

You need records that show how the business operated before the damage, what changed because of the interruption, and which costs continued or stopped.

Here's a practical checklist.

| Document Type | Why It's Important |

|---|---|

| Historical financial statements | Show pre-loss revenue patterns, margins, and operating structure |

| Current budgets and forecasts | Support what management reasonably expected absent the loss |

| General ledgers | Help separate fixed costs, variable costs, and unusual items |

| Tax returns | Provide a cross-check for reported financial performance |

| Payroll records | Show which labor costs continued and which were reduced |

| Bank statements | Help confirm cash movement and operating continuity |

| Sales reports by month | Useful when the business has seasonal swings or uneven demand |

| Vendor invoices and purchasing records | Help prove saved or continuing costs |

| Repair invoices and contractor updates | Tie operational delays to actual restoration issues |

| Lease, loan, and service contracts | Show obligations that continued during the shutdown |

The burden is on you

Insurers like records they can reconcile. If your submission includes summaries with no backup, expect delays. If your numbers don't match your tax reporting or internal books, expect pushback.

That doesn't mean the claim is lost. It means the file needs discipline.

- Keep original files: Don't rely only on exported summaries.

- Use monthly detail: Annual totals hide important patterns.

- Separate business lines: If one division stayed active and another didn't, prove it.

- Preserve inventory records: They often help explain gross profit changes.

Practical tools matter

A clean property inventory can support the broader claim file, especially when equipment, contents, or stock affect the shutdown. If you need a starting point, this personal property inventory template can help you organize damaged items and related records in a way that's easier to submit and review.

Records don't just support the claim amount. They also defend your credibility when the insurer starts testing the file for weaknesses.

Common Insurer Tactics and How to Respond

The insurer's first number is not sacred. It's a position. Sometimes it's reasonable. Sometimes it's built on assumptions that need to be challenged line by line.

For Oregon and Washington businesses, the biggest blind spot I see is seasonality. Ski-adjacent hospitality, coastal retail, agriculture-related operations, tourism businesses, contractors with weather-driven cycles, and specialty shops all face uneven revenue patterns. If the insurer uses the wrong pre-loss period, the claim can be underpaid from the start.

Tactic one uses the wrong baseline

A common insurer move is to default to the 12-month period ending on the loss date, even when that period doesn't reflect the business's true earning pattern. That issue is especially important where revenue rises and falls seasonally. Investopedia notes that lost profits are based on prior performance and highlights the importance of showing monthly revenue and profit fluctuations when selecting the right projection period in this overview of business interruption insurance and lost profit calculations.

If your business earns unevenly across the year, challenge the baseline directly.

- Bring multiple years of monthly sales data

- Show seasonal spikes and downturns

- Explain local business rhythms in Oregon or Washington

- Tie projections to documented patterns, not generic averaging

Tactic two shortens the restoration period

Insurers often push an aggressive reopening timeline. They may focus on when repairs could have been physically finished, not when the business could resume normal operations.

Push back with real-world proof:

- Permit timing

- Contractor availability

- Equipment lead times

- Inspection delays

- Operational testing before reopening

If the building was technically repaired but the business couldn't function, say so and prove why.

Tactic three inflates saved expenses

Saved expenses are legitimate. Inflated saved expenses are not. Some carriers treat almost any reduced spending as a basis to cut the claim, even when the expense wasn't directly tied to producing the lost revenue or the cost just shifted elsewhere.

Respond with a business-specific explanation. Show what costs stopped, what continued, and what reappeared in another form during mitigation.

If the insurer uses broad assumptions about your expenses, force the discussion back to your actual books.

Tactic four wears you down

Delay is a tactic, whether anyone says it out loud or not. Repetitive requests, vague questions, and partial analyses can drag the process out until the owner is tempted to settle cheap and move on.

The answer is organization and pressure.

- Answer in writing

- Attach supporting records

- Track every request and response date

- Ask the adjuster to identify disputed items specifically

- Reject vague denials and demand the policy basis

A fair settlement rarely comes from passive cooperation alone. It comes from presenting a disciplined claim and refusing to let weak assumptions stand unchallenged.

Why Oregon and Washington Businesses Hire a Public Adjuster

A public adjuster works for the policyholder, not the insurance company. That distinction matters more in a business interruption claim than almost anywhere else, because the fight is usually about interpretation, documentation, and financial presentation.

Owners in Oregon and Washington often bring in help when the claim is large, the operations are complicated, the insurer is delaying, or the carrier's math doesn't match how the business really earns money.

Local knowledge matters

A Northwest business isn't generic. Seasonal tourism on the coast, hospitality near recreation corridors, wildfire-related impacts, winter storm disruptions, and city-specific permitting realities all affect how a claim should be documented and negotiated.

That's where local representation can help. Firms such as NW Claims Management's public adjuster team handle property and business income claims by reviewing policy language, documenting damages, organizing financial support, and negotiating with the carrier on the policyholder's behalf.

When hiring help is the smart move

You should seriously consider professional representation if any of these are true:

- The insurer accepts coverage but disputes the amount

- Your business has strong seasonal swings

- The restoration timeline is being compressed unfairly

- You don't have time to build and defend the claim yourself

- The carrier keeps asking for more but gives no clear valuation

This isn't about making the claim aggressive. It's about making it accurate, complete, and hard to undervalue.

A damaged business needs cash flow, clarity, and advantage. A strong public adjuster brings all three.

If your property damage has shut down operations and you need help building or challenging a business interruption claim, NW Claims Management can evaluate the loss, review the policy, and help you pursue a fair settlement in Oregon or Washington.