Most homeowners put this off for the same reason they delay estate planning or emergency binders. They know it matters, but the work feels tedious, and nothing bad has happened yet.

Then a fire, burst pipe, or wind loss turns a normal evening into a negotiation over memory. The insurer asks for a list of what was in the home. Not just the television and sofa, but the small appliances, linens, coats, tools, storage bins, and everything inside every drawer and closet. That's when a personal property inventory template stops being busywork and becomes financial protection.

Why Your Memory Is Not Enough After a Disaster

The hardest inventories are the ones built after the loss.

A homeowner is standing in a damaged living room, trying to remember what was on the bookshelves, what was packed in the hall closet, and whether the upstairs guest room had one set of linens or three. The insurer wants specifics. Brand. Age. Quantity. Condition. Purchase details if available. That request usually arrives while the family is displaced, exhausted, and dealing with cleanup, temporary housing, and calls from contractors.

The California Department of Insurance says taking inventory of personal property before a loss is “very important” because it establishes a record of contents needed to recover insurance settlements after property damage. It also warns that without a pre-loss inventory, homeowners often struggle to prove the existence and value of lost items, which can reduce compensation, as explained in the California Department of Insurance home inventory guidance.

What people forget under pressure

People don't usually forget the obvious items. They forget the cumulative categories.

They leave out pantry goods, kitchen tools, extension cords, bath linens, seasonal clothing, hobby supplies, kids' items, backup electronics, and the contents of storage shelves. Those “small” categories can become a major part of the claim. Memory also compresses time. Owners mix up what they had before the loss with what they bought after it.

Most disputed personal property claims don't start with fraud. They start with incomplete recall.

That's why a claim-ready inventory has to exist before the loss, or at least before you ever need to defend a line item.

If you're building broader household preparedness systems, it also helps to prepare for emergencies with your key documents, insurance information, and access plan stored in one place. If you're already dealing with a serious loss, this guide on what to do after a house fire insurance claim can help you avoid early mistakes.

Building Your Claim-Ready Inventory Template

Most templates fail for one reason. They create a list, not evidence.

A basic spreadsheet with “item” and “value” columns might help you remember what you own, but it won't do much when an adjuster questions age, ownership, condition, or replacement quality. A claim-ready personal property inventory template needs to answer the questions an insurer is likely to ask before they ask them.

The fields that actually matter

A rigorous inventory should follow a room-by-room method and document each item with brand, model, serial number, purchase date, exact value, and proof of ownership, according to Rubin Adjusting's guide to preparing a personal property inventory. That same source notes that failure to include serial numbers or specific purchase details for high-value items is a leading cause of claim underpayment, and cites studies indicating that 30–40% of homeowners fail to document those identifiers.

That lines up with what works in practice. Specificity narrows the insurer's room to substitute a cheaper comparison item or apply broader depreciation assumptions.

| Field Name | Purpose & Example |

|---|---|

| Item description | Identifies the item clearly. Example: “Dining chair” is weak. “Pottery Barn upholstered dining chair, gray linen” is useful. |

| Room location | Shows where the item was kept. Example: “Primary bedroom dresser top” or “Garage wall rack.” |

| Category | Helps sort and total losses. Example: furniture, electronics, clothing, tools, decor. |

| Brand | Prevents generic replacement comparisons. Example: Sony, KitchenAid, Patagonia. |

| Model | Distinguishes between product tiers. Example: exact television or appliance model. |

| Serial number | Ties the item to ownership and can defeat disputes over existence. Best for electronics, tools, appliances, instruments, and collectibles. |

| Purchase date | Supports age and depreciation analysis. Even an approximate month and year is better than nothing if exact data isn't available. |

| Purchase price or exact value | Anchors valuation. Example: original cost from a receipt or invoice. |

| Condition before loss | Helps resist blanket assumptions that an item was old or worn out. Example: “excellent,” “good,” or a short note such as “reupholstered in 2022.” |

| Quantity | Critical for repeated items. Example: “6 bath towels,” “12 dinner plates,” “18 hardcover books on shelf 2.” |

| Proof of ownership | Links to receipts, appraisals, manuals, warranty confirmations, or product registration emails. |

| Photo or video file name | Connects the row to visual proof. Example: “KitchenMixer_Closeup_01.jpg.” |

| Notes | Holds appraisals, upgrades, sets, matching pieces, or custom details. Example: “custom drapery panels, lined, made to fit bay window.” |

What works and what doesn't

What works is a system that can survive scrutiny.

What doesn't work is a vague inventory built around categories like “clothes,” “kitchen stuff,” and “garage tools” with one round number beside each. That kind of list invites pushback because it doesn't give the insurer enough to verify quality, quantity, or ownership.

Use a spreadsheet if you're disciplined. Use an inventory app if it keeps you consistent. The best tool is the one you'll maintain, but the format has to support documentation. If you want ideas on how digital lists can streamline insurance claims with templates, review examples, then build yours around claim evidence instead of convenience alone.

Build for disputed items first

Start with the categories most likely to be challenged:

- Electronics with exact model and serial details

- Jewelry and watches with appraisals, close-up photos, and purchase records

- Appliances with manufacturer labels

- Collectibles and antiques with provenance or valuation notes

- Tools and equipment that often look generic without model identifiers

- Musical instruments with serial numbers and case photos

Practical rule: If two versions of the same item exist at very different prices, your template must show which version you owned.

Some belongings may also need separate insurance treatment. If you're unsure where your inventory intersects with endorsements and item-specific limits, it helps to understand scheduled personal property coverage.

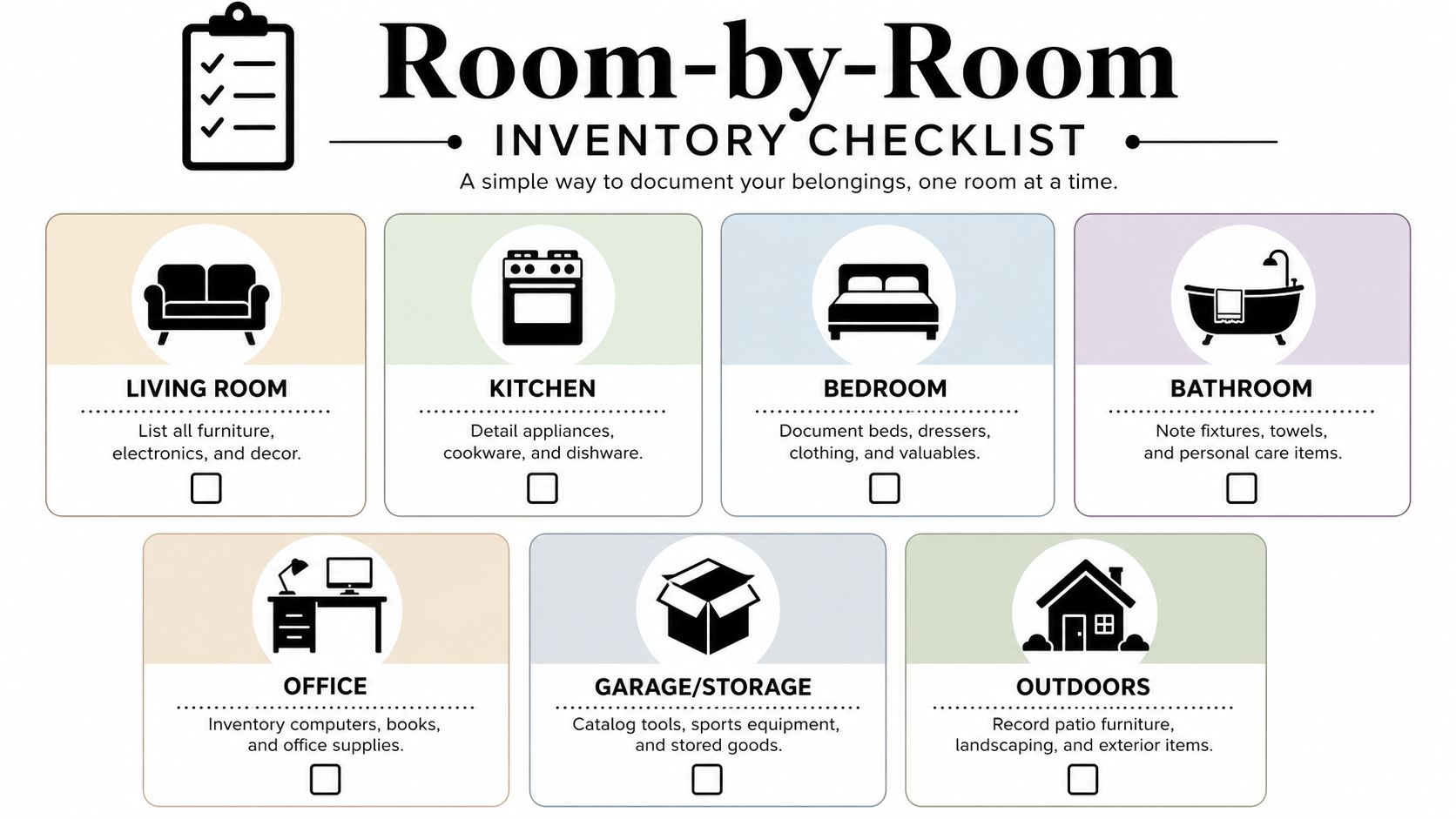

A Room-by-Room Guide to Documenting Everything

A full inventory feels overwhelming when you think about the whole house at once. It gets manageable when you work one room, one surface, one drawer at a time.

The mistake most homeowners make is starting with the expensive items and stopping there. That leaves entire categories undocumented, especially the daily-use property that doesn't feel important until it's gone.

The NAIC notes that low-cost, high-volume items like clothing and kitchenware can represent up to 60% of total household loss value in residential claims, and that denials for “insufficient inventory” disproportionately affect these everyday categories because homeowners don't itemize them in enough detail, as described in the NAIC home inventory consumer guidance.

Start with sight lines, then open storage

Walk each room twice.

The first pass captures what's visible. Furniture, electronics, decor, rugs, lamps, wall art, and major appliances. The second pass is where the real inventory gets built. Open cabinets, closets, dressers, bins, and shelves. Document contents, not just containers.

A practical order looks like this:

- Stand in the doorway and take a wide video sweep of the room.

- Move clockwise and stop at every major furniture piece or storage area.

- Open what closes. Closets, drawers, cabinet doors, trunks, and lidded bins.

- Count repeated items when they matter, especially dishes, linens, clothing, and books.

- Photograph labels on higher-value property before moving to the next room.

What to focus on in each area

Some rooms need detail. Others need discipline.

- Living room. Include sofas, side tables, media devices, gaming systems, speakers, lamps, artwork, blankets, and decor stored in consoles or baskets.

- Kitchen. Go beyond appliances. Document cookware, knife sets, dishware, glassware, pantry appliances, food storage systems, and specialty tools.

- Bedrooms. Beds and dressers are obvious. Don't skip shoes, handbags, folded clothing, jewelry boxes, bedding, and items under beds.

- Bathrooms. Hair tools, electric razors, linens, mirrors, organizers, and higher-end personal care devices often get missed.

- Office. Computers, monitors, printers, software media, books, cameras, microphones, and backup drives should each have their own record.

- Garage and storage. Tools, ladders, paint sprayers, sports gear, camping equipment, holiday items, and spare appliances deserve their own entries.

- Outdoor areas. Patio furniture, grills, garden tools, planters, and exterior storage contents often disappear from claims unless someone documents them deliberately.

If you want a practical framework for documenting spaces during or after a loss event, a property inspection checklist can help you stay systematic.

The insurer can only evaluate what you identify. Items left out of the inventory usually don't reappear later without a fight.

Use grouping carefully

Grouping saves time, but only when the group is specific enough.

“Kitchen contents” is too broad. “Twelve white ceramic dinner plates, Crate & Barrel, everyday use set” is workable. “Women's coats” is weak. “Five women's winter coats, including one wool dress coat and one insulated ski jacket” is much stronger.

For closets, bookcases, and kitchen cabinets, video is efficient. Narrate what you're seeing as you film. Then use your spreadsheet to turn the visual record into itemized rows or well-defined grouped entries.

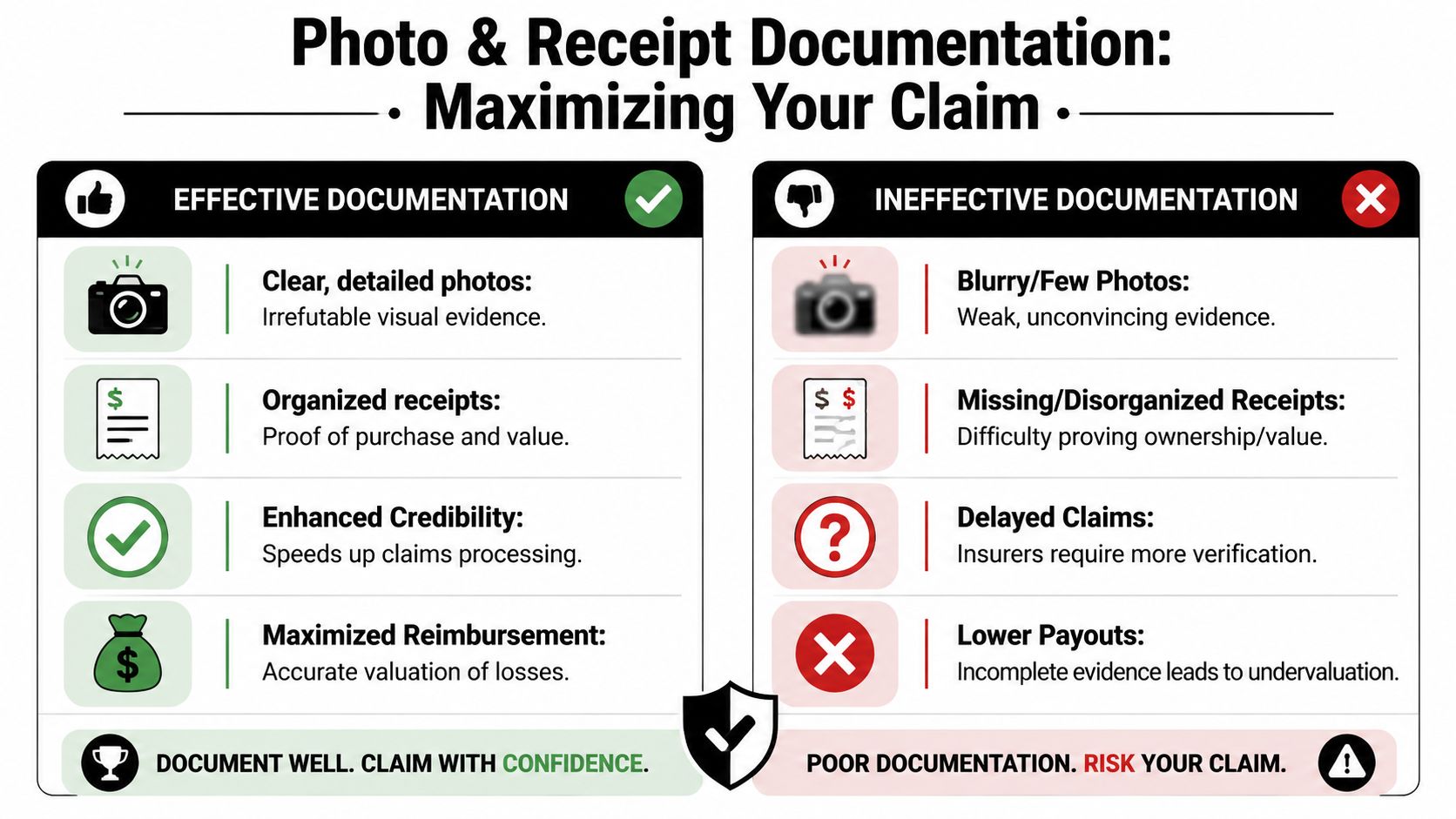

The Art of Proof Photographing and Managing Receipts

Casual photos help you remember. Proof photographs help you win arguments.

There's a difference between snapping a room from across the hall and creating a file set that shows the item, its brand, its condition, and its place in the home. The Wisconsin Office of the Commissioner of Insurance says a detailed inventory can save homeowners “time, money, and frustration” and recommends including video or photographs because detailed records support claim validation, as explained in the Wisconsin OCI personal inventory guide.

How to take photos that hold up

A usable documentation set usually has three layers.

First, take a wide room shot. This places the item in context and helps prove it was in the home before the loss. Second, take a mid-range shot of the specific item. Third, take a close-up of the model tag, serial number, maker's mark, brand label, or distinctive damage-free condition.

For certain categories, add one more detail shot:

- Furniture. Photograph brand tags, underside labels, and custom fabric details.

- Electronics. Capture rear labels with serial and model numbers.

- Jewelry. Use close-up images, appraisals, and box or receipt photos.

- Clothing. Photograph brand labels for higher-end pieces and take closet overview shots.

- Appliances and tools. Include manufacturer plates and any accessory kits stored with them.

A blurry photo proves there was “something” in the room. A sharp photo tied to a spreadsheet row proves what it was.

Receipts are only useful if you can find them

Paper receipts tossed in a drawer are almost as bad as no receipts at all. They fade, get lost, and won't help if the home is inaccessible.

The practical workflow is simple:

- Scan paper receipts with a phone scanning app as soon as possible.

- Rename files clearly so they match your inventory rows.

- Store by room or category in digital folders.

- Attach appraisals and invoices to the same folder as the item photos.

- Save retailer emails and order confirmations as PDFs for online purchases.

If you need a cleaner process for digitizing and sorting purchase records, Smart Receipts' guide on organizing receipts offers a practical starting point.

Match proof to valuation

A receipt proves purchase. It doesn't always prove current replacement quality.

That's why photos matter. A high-end sectional without proof of brand and materials may get compared to a basic sectional of similar size. A custom area rug without pattern photos may be valued like a machine-made standard rug. A camera body without its exact model record may be priced against an entry-level version.

For claim preparation, think in terms of evidence bundles. One bundle per item or item group. Inventory row, room photo, item photo, label photo, receipt or invoice, and any appraisal or product registration record. If you ever need a structured review of loss evidence, a property damage assessment process helps turn scattered documents into usable claim support.

Storing Your Inventory for Disaster-Proof Access

An inventory stored only inside your home isn't disaster-proof. It's disaster-adjacent.

Paper lists burn. Desktop files can be destroyed with the computer they're saved on. Even a well-organized binder becomes useless if it's soaked, buried, or inaccessible after evacuation. The California Department of Insurance guidance discussed earlier points homeowners toward secure online storage because the record has to remain accessible even if the structure is gone.

Use layered storage, not one storage method

The safest setup uses redundancy.

Keep the working version in a cloud folder such as Google Drive, Dropbox, OneDrive, or iCloud Drive. If you use a dedicated inventory app, make sure it syncs to cloud storage and lets you export your data. A system you can't export can create problems later if the app changes or you stop using it.

A practical storage stack looks like this:

- Primary copy in a cloud folder with subfolders by room

- Secondary copy exported as spreadsheet plus PDFs

- Photo library backup synced automatically from your phone

- Offline copy on an encrypted USB drive or external drive

- Off-site access shared with a spouse, trusted relative, or attorney if appropriate

Accessibility matters as much as security

After a major loss, you may be out of the house for days or weeks. You might be using a borrowed phone or logging in from a hotel business center. That's not the time to realize your inventory sits on a laptop that was inside the fire-damaged office.

Store passwords in a secure password manager. Test access from a second device. Make sure at least one trusted person knows where the records are and how to retrieve them if you can't.

The best inventory isn't the most detailed one. It's the most detailed one you can still open after the disaster.

Using Your Inventory to Maximize Your Insurance Claim

A strong inventory changes the tone of a claim.

Without it, the conversation often becomes speculative. The insurer asks for more detail, applies broad depreciation, substitutes lower-grade comparables, or delays decisions while requesting additional proof. With a claim-ready file, the discussion shifts toward verification and valuation, not whether the item existed at all.

United Policyholders reports that 42% of claim disputes stem from inadequate proof of ownership or value, and notes that many generic templates leave out purchase dates, condition notes, and appraisal attachments that are needed to push back on depreciation tactics, as outlined in its home inventory guidance for policyholders. That gap matters in Oregon and Washington, where policy wording can be technical and item valuation disputes can turn on documentation quality.

How insurers use weak inventories against you

Insurers rarely need to deny an entire contents claim to reduce it. They can narrow it line by line.

A vague entry such as “TV, $1,500” gives them room to ask what size it was, whether it was smart-enabled, how old it was, and what model you had. If you can't answer, they may value it using a lower-tier comparable. The same thing happens with rugs, furniture, cookware sets, power tools, and clothing.

Here's where strong documentation is powerful:

- Specific model details reduce substitution with cheaper alternatives.

- Condition notes and photos help counter aggressive depreciation.

- Receipts and appraisals anchor value for specialty items.

- Room-by-room structure makes omissions easier to catch before submission.

Use the inventory as a negotiation file

Your personal property inventory template shouldn't end as a spreadsheet. It should become a claim file.

That means each contested item can be supported quickly. If the insurer questions a watch, you produce the row, the photo, the appraisal, and the receipt. If they undervalue a set of dining chairs, you show the manufacturer, style line, quantity, and pre-loss condition. If they overlook garage contents, you already have the bin contents, tool labels, and overview photos tied together.

For homeowners trying to recover a fair settlement, that level of documentation can make a meaningful difference in bargaining power and speed. If you're already in the middle of a difficult claim and need help understanding where value is being lost, this guide on how to maximize insurance claim payout explains the broader strategy.

A detailed inventory doesn't guarantee a smooth claim. It gives you something far more useful. A defensible position.

The homeowners who recover best are usually the ones who can produce proof fast, organize it clearly, and keep pressure on each disputed line item until it's addressed properly.

If you're facing a fire, water, storm, or vandalism claim in Oregon or Washington and need expert help documenting losses and negotiating with the insurer, NW Claims Management can step in as your advocate. Their team works for policyholders, not insurance companies, and helps turn damaged property, missing documentation, and disputed values into a structured claim built for a fair settlement.