The storm has moved on, but the house doesn't feel settled. You hear runoff in the gutters, you spot shingle grit near the downspout, and a neighbor is already saying their roofer found hail hits on the vents and ridge. Most homeowners in Oregon and Washington don't file a hail damage roof insurance claim often enough to feel confident doing it correctly. That's why the first few decisions matter so much.

The hardest part is that hail damage rarely looks dramatic from the driveway. A roof can take a hard impact, shed protective granules, bruise the shingle mat, and still look “mostly fine” from the ground. In the Pacific Northwest, that's a problem. Once rain returns, small impact damage can become a moisture problem faster than many homeowners expect.

The Aftermath of a Hailstorm and Your First Move

Right after a hailstorm, homeowners often make one of two mistakes. They either panic and call the insurer before they understand what was damaged, or they wait too long because the roof isn't actively leaking. Neither approach helps.

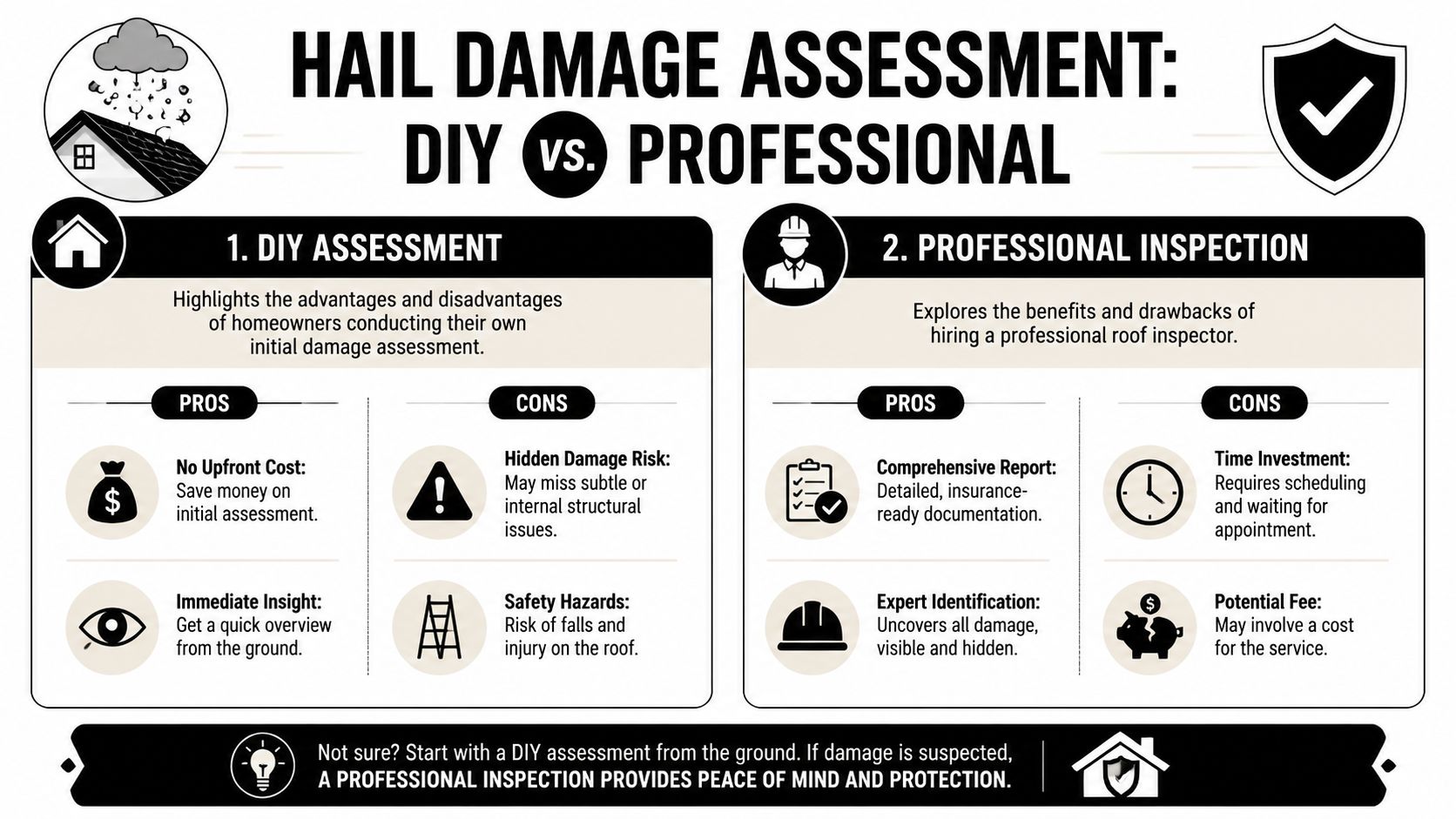

Start with control. Walk the property from the ground. Look at gutters, downspouts, window screens, deck furniture, metal flashing, and any soft metal roof components you can safely see. Take photos of everything that appears freshly dented or disturbed. Don't climb a wet roof, and don't let urgency push you into a bad inspection.

This is not a niche problem. Hail damage is the single leading cause of homeowners insurance claims nationwide, accounting for 45.5% of all such claims, and convective storm losses doubled from $30 billion in 2022 to $60 billion in 2023, according to Cape Analytics on hail risk for property insurers. That matters because insurers process a huge volume of these claims, and volume tends to produce shortcuts.

What your first move should be

Your first move is simple. Preserve evidence before the claim story gets muddy.

- Photograph conditions immediately: Capture the date, visible debris, gutter runoff, dented metals, broken accessories, and any interior signs of water entry.

- Write down the storm timing: Even an approximate window helps while you gather official weather confirmation later.

- Prevent further damage: If water is entering, take reasonable temporary steps to protect the property and save receipts.

- Avoid firm conclusions too early: Don't tell the carrier “it's probably minor” or “the whole roof is destroyed” before the roof is properly inspected.

A hail claim usually gets stronger or weaker in the first forty-eight hours, based on what the homeowner documents and what they say.

In Oregon and Washington, another issue shows up quickly. Homes here often go back into wet conditions soon after the storm. That means delayed action can blur storm damage with later moisture effects, and insurers may try to separate the two. The cleanest path is to establish the loss early, document carefully, and build the claim before anyone minimizes it.

Assessing Your Roof for Functional Hail Damage

A lot of claim trouble starts with one word: cosmetic.

Insurers may acknowledge marks on the roof but argue those marks don't affect performance. Homeowners hear that and assume the claim is weak. Sometimes it is. Often it isn't. Ultimately, the question is whether the hail caused functional damage, not whether the roof still looks presentable from the street.

Recent data shows 34% of denied hail claims were initially labeled “cosmetic,” yet 68% of those were later reversed after engineering reports confirmed functional damage, as explained in this review of cosmetic versus functional roof damage. That same source draws the line clearly: functional damage includes visible fractures or matting bruising, while cosmetic damage is limited to surface granule loss without structural compromise.

What to look for from the ground

You're not trying to perform a final expert inspection yourself. You're trying to notice indicators that justify closer review.

- Dented soft metals: Check vents, flashing, gutter screens, downspouts, and metal caps. If hail marked soft metal, the shingles deserve a closer look.

- Fresh granule accumulation: Heavy granule loss in gutters after the storm can support impact damage, though granule loss alone doesn't automatically prove functional failure.

- Collateral damage: Screens, patio covers, siding, and outdoor fixtures can help tell the storm story.

For safer initial review, many homeowners now start with a drone roof inspection to capture slope-by-slope conditions without walking a slick roof.

What functional damage actually looks like

Functional hail damage usually shows up as fractures, bruising, or asphalt loss that changes the roof's ability to shed water. On asphalt shingles, that can mean a soft bruise beneath the surface, a cracked shingle, or a broken area where the protective layer has been compromised.

In Oregon and Washington, that distinction matters more than generic hail guides admit. A roof that seems only “marked up” may still be vulnerable once repeated rain, wind-driven moisture, and normal seasonal dampness work into those impact points. What gets dismissed as minor can turn into a leak path.

Here's a practical approach:

| Condition | More likely cosmetic | More likely functional |

|---|---|---|

| Surface scuffing | Yes | Sometimes not |

| Simple granule loss with no fracture | Often | Depends on extent |

| Visible cracks in shingle surface | No | Yes |

| Bruised or softened matting | No | Yes |

| Asphalt loss exposing vulnerable material | No | Yes |

Practical rule: If the mark changes how the shingle protects the roof assembly, you're not dealing with a cosmetic issue anymore.

Don't argue this point from instinct alone. Look for visible markers, document what you can safely see, and expect that hidden damage may require a trained inspection to confirm.

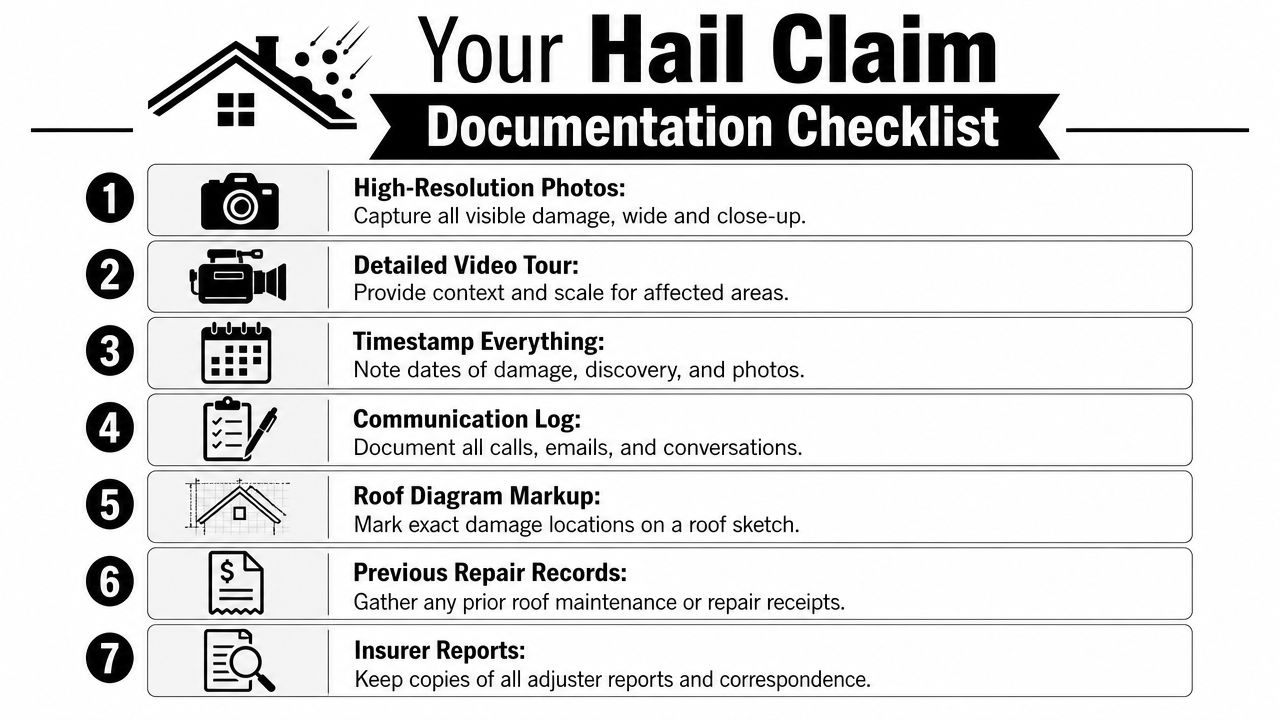

Building an Undeniable Claim with Professional Documentation

A hail damage roof insurance claim is won on proof, not suspicion. “The roof looks bad” isn't enough. “There was a storm in the area” isn't enough either. The file has to tie this roof, at this property, to this storm, with this pattern of damage.

The strongest claims are built like evidence packages. Each document should answer one of three questions: when did the loss happen, where did it hit, and how did it damage the roof system?

The three items insurers can't easily ignore

According to guidance on successful hail damage claim preparation, a successful submission needs a specific date of loss tied to official weather reports, an itemized software-generated scope identifying damage on multiple roof slopes and soft metals, and high-resolution photos with clear scale markings.

Those three points sound straightforward, but most homeowners fall short in the details.

Date of loss tied to weather records

Don't guess loosely. Use the specific storm date that matches official weather reporting for your area. If more than one storm passed through, identify the one that aligns with the observed damage.Itemized scope using estimating software

A proper scope should identify each affected slope, soft metal damage, flashing, vents, ridge components, and related items. Xactimate is the software many carriers and professionals use because it creates line-item estimates in a format insurers recognize.Scaled photo evidence

Close-ups should include a coin or ruler near the impact point so the image shows dimension, not just a dark spot. Wide shots matter too. They place the close-up in context and show which slope or component was hit.

The documents most homeowners forget

The claim file usually weakens because one category gets skipped, not because everything is missing. Use a checklist and keep it in one place. A printable property inspection checklist helps homeowners avoid gaps that later turn into disputes.

Focus on these supporting records:

- Communication log: Record calls, emails, names, and what was said.

- Roof sketch or diagram: Mark where damage appears by slope and component.

- Maintenance records: Prior invoices help separate old issues from new storm damage.

- Adjuster paperwork: Keep every estimate, reservation-of-rights letter, and scope revision.

If you want another practical example of how roof claim documentation is framed for homeowners in another hail market, this West Texas insurance roof guide is useful because it shows how local conditions and insurer review standards shape the inspection file.

What works and what doesn't

What works is layered proof. Weather confirmation, a disciplined scope, scaled images, and organized records all support each other.

What doesn't work is sending a handful of random phone photos and expecting the adjuster to build the claim for you. They won't. If soft metals weren't documented, if only one slope was photographed, or if normal wear can't be ruled out, the carrier has room to reduce or deny.

Filing Your Claim and Managing Insurer Deadlines

Once the evidence is organized, open the claim. Keep the first notice of loss simple and controlled. You're reporting a storm event and visible damage, not giving a full technical opinion before the inspection process begins.

Say what you know. Avoid guessing. A strong first report usually includes the storm date, property address, the fact that you observed hail-related damage indicators, and that a full inspection is being assembled.

What to say on the first call

A clean script sounds like this in practice: there was a hailstorm on a specific date, the property appears to have roof-related storm damage, and you want to open a claim for inspection and review. That's enough.

Avoid statements that box you in later.

- Don't minimize the loss: “It's probably nothing” can reappear in claim notes.

- Don't overstate certainty: “The whole roof needs replacement” is premature if the inspection file isn't complete.

- Don't speculate about cause if you're unsure: Stick to observed facts and the storm date.

Keep your language factual. The first call should open the file, not argue the entire case.

Deadlines and paperwork discipline

Every policy has notice and proof requirements. Read the loss conditions section carefully. If you can't locate it, request a certified copy of the policy and endorsements from the insurer.

Track everything in writing after the claim is opened. Confirm conversations by email. If the carrier asks for forms, inspection access, or repair documents, calendar those deadlines immediately. A missed deadline creates an avoidable side dispute.

For homeowners who want a more structured walkthrough before making the call, this guide on how to file a property damage claim is a useful starting point.

Claim administration principles also carry across different property-loss situations. This overview of Treecorp Solutions insurance claims assistance is worth a look for its emphasis on organizing records and keeping communication disciplined once the insurer gets involved.

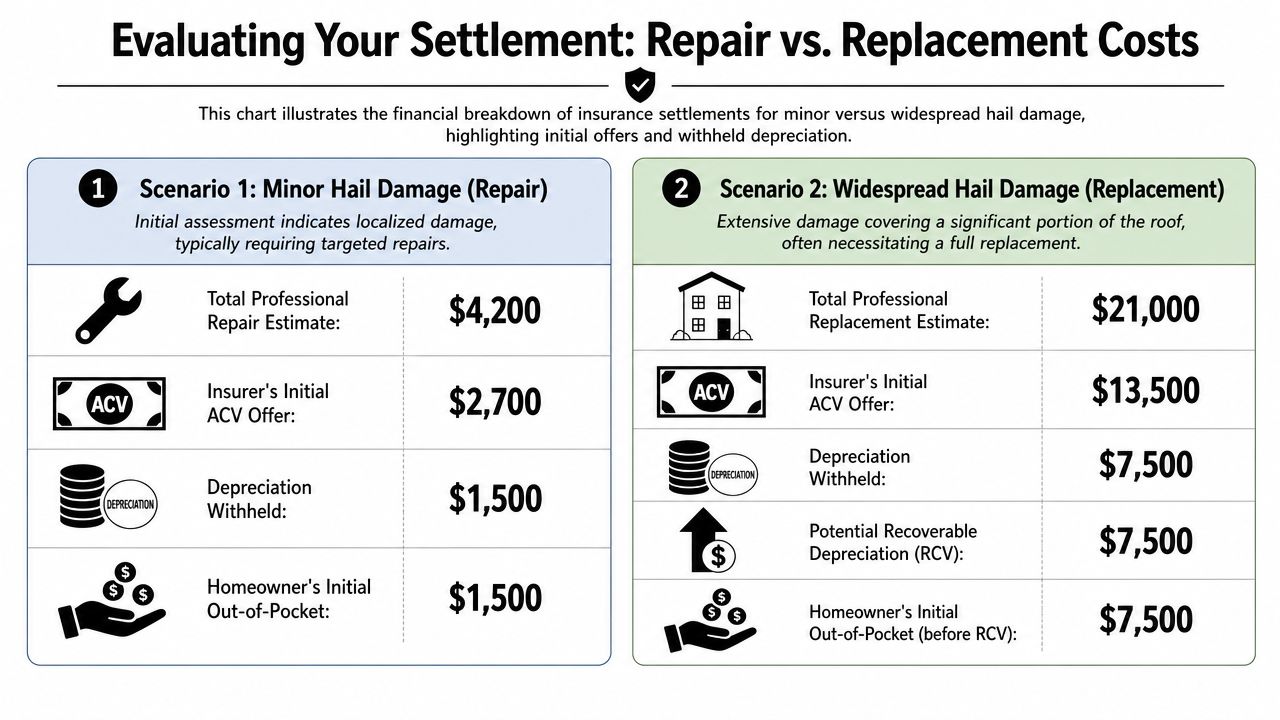

Evaluating the Settlement Offer Repair Versus Replacement

Many homeowners lose money at this point. The carrier issues an estimate, the numbers look official, and the temptation is to assume the hard part is over. It isn't. The first offer often reflects the insurer's preferred scope, not the roof's actual long-term needs.

One of the most common pressure points is the repair versus replacement debate. Insurers often offer repairs for hail damage affecting less than 15% of the roof, according to this discussion of roof claim disputes and partial repair outcomes. The same source cites a NAPIA report finding that 47% of homeowners who accepted partial repair offers later experienced roof failure within 2 years, leading to an additional $8K to $12K in out-of-pocket costs.

Why patchwork repairs often fail in Oregon and Washington

A limited repair can look reasonable on paper. Replace a few shingles. Swap a vent cap. Touch up what's obvious. But roofs in the Pacific Northwest deal with recurring wet exposure, and hidden hail bruising doesn't always stay hidden for long.

If matting is bruised or impact damage appears across multiple slopes, partial repair may leave the roof with mixed-age components and unresolved weak points. Water doesn't care that the estimate says “spot repair.” It follows the compromised area.

How to review the insurer estimate

Don't just compare the total. Compare the scope line by line.

Check for omissions such as:

- Soft metals left out: Vents, flashing, caps, and other dented components are frequently undercounted.

- Too few slopes included: If your photos show impacts across the roof, the estimate shouldn't isolate one small area without explanation.

- No allowance for hidden damage: Surface-only scopes often miss what becomes visible during tear-off.

- Improper repair assumptions: If the estimate assumes clean patching where brittle or impact-weakened shingles are present, challenge that assumption.

A helpful reference point for payout structure and deductible pressure is this overview of the average insurance payout for hail damage roof claims. It can help you read the offer with a more critical eye.

If the estimate repairs the visible marks but ignores the roof's ability to keep water out over time, the scope is incomplete.

A simple decision table

| If the offer does this | Treat it as a warning sign |

|---|---|

| Limits damage to one small area despite broader indicators | Ask for a reinspection with full slope review |

| Labels fractured or bruised areas as cosmetic | Request technical support for that conclusion |

| Ignores dented soft metals | Push for revised scope |

| Offers spot repair on a moisture-exposed roof with hidden damage concerns | Evaluate whether replacement is the only durable fix |

You don't have to accept the first offer because it arrived on company letterhead. Read it as a negotiable position.

When to Partner with a Public Adjuster for Your Claim

Some hail claims move cleanly. Many don't. The question isn't whether you can fill out forms yourself. The question is whether the dispute has become technical enough, or expensive enough, that you need someone who works only for you.

A public adjuster represents the policyholder. That's different from the carrier's adjuster, whose role is tied to the insurer's claim process and budget controls. When a roof claim turns into an argument about causation, scope, depreciation, code issues, or whether damage is “cosmetic,” representation starts to matter.

Situations where outside help makes sense

The need is usually clear when one of these shows up:

- The claim was denied or partly denied: Especially where the carrier says the roof has only cosmetic damage.

- The scope is obviously light: Missing slopes, soft metals, or related components usually signal a negotiation problem.

- The property owner doesn't have time to manage the file: Roof claims require follow-up, documentation review, and deadline control.

- The deductible is large enough that mistakes become expensive: In hail-prone states, special deductibles can be significant.

The financial stakes are real. Average roof hail payouts range from $12,000 to $17,000, and some policies in hail-prone states impose wind or hail deductibles ranging from 1% to 10% of the home's value, such as a $6,000 deductible on a $300,000 home, as outlined in this review of hail damage roof insurance payouts and deductibles.

What a good public adjuster actually does

A good public adjuster doesn't just “argue with insurance.” They read the policy, organize the damage presentation, compare scopes, challenge unsupported exclusions, and negotiate from documented facts. They also keep homeowners from making tired, expensive concessions just to get the claim over with.

If you're trying to decide whether your situation has crossed that line, this guide on when to hire a public adjuster lays out the usual trigger points.

For many Oregon and Washington homeowners, the deciding factor is simple. If the carrier and the roof evidence no longer match, handling it alone becomes a risk.

Frequently Asked Questions About Hail Damage Claims

How long do I have to file a hail claim in Oregon or Washington

Check your policy immediately. The notice and suit-limitation language can differ, and endorsements matter. Don't rely on a general deadline you heard from a neighbor or contractor.

Will a weather claim raise my premium

Rate impact depends on your insurer, claim history, underwriting decisions, and market conditions. No one should promise a universal answer. If you have legitimate storm damage, focus first on protecting the property and preserving your rights.

What if my roofer and the insurance adjuster disagree

That's common. Ask for both scopes in writing and compare them line by line. Look for disagreements about damaged slopes, soft metals, hidden damage, and whether the carrier called functional damage “cosmetic.”

Should I let the insurer inspect before I get my own inspection

You can open the claim quickly, but it's usually better to have your own damage documentation organized as early as possible. Going into the inspection blind often leaves the homeowner reacting instead of presenting evidence.

If the roof isn't leaking, should I still file

Possibly, yes. Hail damage doesn't need to produce an immediate interior leak to be claim-worthy. Impact damage can weaken the roof system before water shows up inside.

If you're dealing with a confusing hail damage roof insurance claim in Oregon or Washington, NW Claims Management can help you evaluate the damage, interpret the policy, and challenge an underpaid or denied claim. Their team represents policyholders, not insurers, and they handle the documentation and negotiation work that often decides whether a roof gets properly covered or shorted.