Standard homeowners insurance typically does cover wildfire damage because wildfire is generally treated as a fire peril, and that usually includes the house itself, detached structures, personal property, and sometimes temporary living expenses if you can't live there. The hard part is that being covered doesn't mean the check will be enough, or that the claim will move smoothly without a fight over limits, depreciation, documentation, and what the insurer decides the damage is really worth.

If you're reading this while smoke is in the air, evacuation notices are popping up, or you've just come home to ash, soot, and a house that no longer feels safe, the question isn't academic. You want to know whether your policy will protect you, and whether you're about to get trapped in a claim that sounds covered on paper but falls apart in practice.

That gap is where homeowners get blindsided. I've seen people feel relieved when they hear “yes, wildfire is covered,” then run straight into a second shock when they learn their insurer is valuing contents low, limiting certain outdoor items, scrutinizing smoke damage, or paying part of the loss now and making the rest harder to recover later. A wildfire claim is rarely just about visible flames. It's about rebuilding costs, proof, timing, and whether your policy language works the way you think it does.

The Simple Answer to a Terrifying Question

An evacuation notice hits your phone at 2:13 a.m. You grab medication, a few clothes, the dog leash, and the policy folder you have not looked at in years. On the drive out, the question is simple and urgent. If the fire reaches your property, will insurance come through?

Usually, yes. Wildfire is generally treated as a covered fire loss under a standard homeowners policy.

That answer helps for about five minutes. After that, the true challenge begins. Homeowners do not just need a claim opened. They need enough money to repair the house properly, replace what was lost, and get through the months that follow without funding part of the loss out of pocket.

That is the gap people miss. Covered is not the same as made whole.

In wildfire claims, the fight is often not about whether the policy responds at all. The fight is about scope, pricing, documentation, and timing. I have seen carriers accept coverage quickly, then dispute smoke contamination, apply depreciation aggressively, or pay actual cash value first and leave the homeowner to chase the rest later. If you are not clear on how actual cash value and replacement cost change what you recover, the first payment can create a false sense of relief.

What people miss in the first phone call

A worried homeowner asks, “Am I covered?” That is understandable, but it is only the first question. The practical questions are the ones that shape the final payout:

- How much insurance is available: Coverage only pays up to the limits and sublimits in the policy.

- What part of the loss the insurer will challenge: Smoke, ash, odor, corrosion, electronics, and hidden contamination often draw more scrutiny than visible burn damage.

- What valuation method applies at each stage: Some insurers issue an initial payment on a lower basis, then require more proof before releasing the full replacement amount.

- What deadlines control the claim: Proof of loss, inventory support, and receipts for temporary living costs can all affect payment if they are late or incomplete.

Practical rule: Claim acceptance marks the start of the valuation process.

Wildfire losses turn into documentation battles fast. The homeowners who recover best are usually not the ones with the cleanest yes-or-no coverage answer. They are the ones who document early, track every expense, and catch underpayment issues before those numbers harden into the claim file.

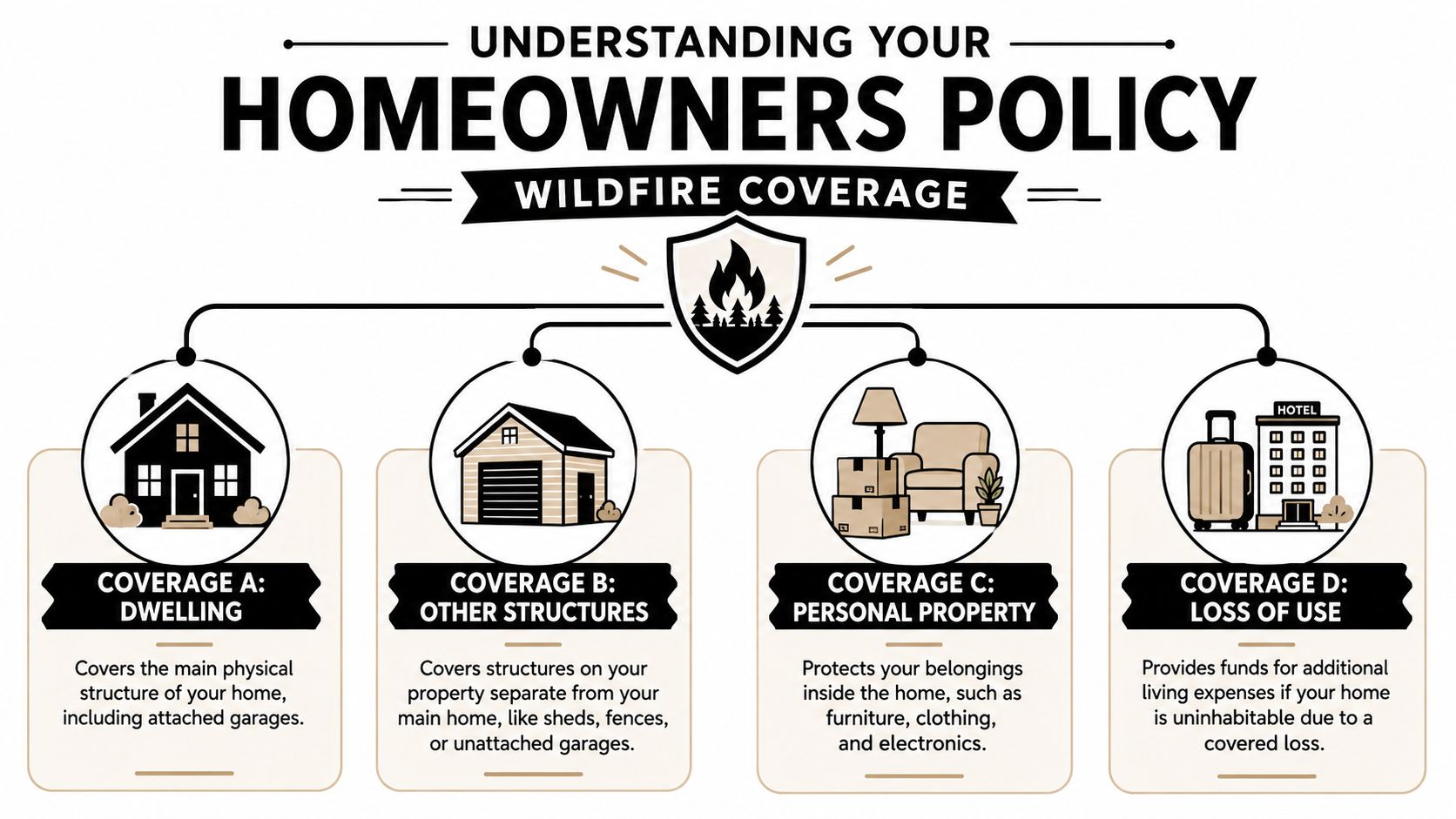

Anatomy of Your Homeowners Policy Wildfire Coverage

A wildfire claim gets divided long before the insurer talks about payment. The policy separates the house, detached structures, personal property, and temporary living costs into different buckets, each with its own limit, rules, and pressure points. That distinction matters because a homeowner can hear “the loss is covered” and still come up short if one category is underinsured or poorly documented.

Wildfire is usually treated as a covered fire loss under a standard homeowners policy, so many homeowners do not carry a separate wildfire policy. The essential work starts after that basic answer. You need to know which part of the policy applies to each piece of damage, how the insurer values it, and where sublimits or depreciation can reduce what gets paid.

Coverage A for the house itself

Dwelling coverage pays for damage to the main structure of the home, including attached features such as an attached garage, built-ins, and major structural components.

If the house burned, this is usually the largest part of the claim. If the structure is still standing but has serious smoke, heat, or firefighting damage, this coverage is still often the battleground because the dispute shifts to scope. Insurers may write for cleaning, sealing, and spot repair where a contractor recommends deeper tear-out and replacement.

Valuation adds another layer. Many homeowners expect one full check and quickly learn the policy may release money in stages depending on whether it pays on an actual cash value basis first or on a replacement cost basis after repairs are incurred. That gap explains a lot of the frustration in early estimates. For a practical explanation, review how actual cash value and replacement cost affect wildfire claim payments.

Coverage B for structures that aren't attached

A detached garage, shop, shed, fence, pergola, or guest structure usually falls under other structures coverage.

This category gets missed constantly. After a wildfire, homeowners focus on the house and carrier adjusters often do the same unless the outbuildings are clearly listed, photographed, and priced. I have seen real losses get trimmed because the detached structure was mentioned late or described too vaguely in the claim file.

The limit here is often a percentage of Coverage A, not a separate number chosen with the outbuildings in mind. That can create a hard cap even when the property includes expensive fencing, a workshop, retaining walls, or custom exterior features. Homeowners who invest in exterior protection should also understand strategies for fire-safe landscaping, because resilient design can help reduce future loss even though it does not change what this coverage limit will pay.

Coverage C for what you owned inside

Personal property coverage applies to furniture, clothing, electronics, tools, kitchen items, décor, and other belongings that are not part of the structure.

Wildfire claims often become labor-heavy. A burned couch is simple. A smoke-affected computer, mattress, rug, photo album, or set of kitchen goods is harder because the damage may not read clearly in a single photo. The insurer may ask for age, condition, brand, model, purchase date, and replacement price room by room. Families are usually dealing with displacement at the same time.

The insurer's inventory form helps them process the claim. It does not protect your valuation unless you fill it out with enough detail to support replacement.

Build your own inventory record as you go. Use photos, videos, receipts, serial numbers, online order history, and notes by room. If you wait until memory fades, the contents claim usually shrinks.

Coverage D for living somewhere else while the house is unusable

If a covered wildfire loss makes the home unlivable, loss of use or additional living expense coverage can pay the extra cost of living elsewhere during repairs or rebuilding.

This coverage can save a family financially, but only if they track it carefully. The policy usually pays the increase above your normal living costs, not every dollar you spend while displaced. Hotel bills, short-term rent, storage, pet boarding, laundry, parking, and added commute costs may all come into play, but support matters. Delays in claim handling can also create pressure if the insurer questions whether the home still needs to be vacant.

Here is the practical breakdown:

- Coverage A: Repair or rebuild the main house

- Coverage B: Pay for detached structures on the property

- Coverage C: Cover damaged or destroyed belongings

- Coverage D: Reimburse extra living costs while the home cannot be occupied

That is how the policy is organized on paper. The harder question is whether each category is valued fully enough to make you whole.

Beyond the Flames Smoke Ash Debris and Landscaping

A wildfire claim isn't limited to a blackened frame and a collapsed roof. Some of the most contested losses happen when the house is still standing.

Smoke can travel through vents, attic spaces, insulation, soft goods, and HVAC systems. Ash can settle in places you don't notice until corrosion, staining, odor, or mechanical issues show up later. Debris can create safety hazards and cleanup costs before repairs even begin. Landscaping losses often surprise homeowners because they assume everything on the lot is protected the same way the house is. It isn't.

Where claims get narrowed

Insurers usually recognize direct fire damage more readily than secondary effects. The disputes tend to start when the damage is harder to see or easier to discount.

Here's a practical snapshot.

| Damage Type | Typical Coverage Status | Common Pitfall or Limit |

|---|---|---|

| Structural fire damage | Usually covered under the dwelling portion if caused by a covered wildfire loss | The repair scope may be narrower than needed |

| Smoke damage inside the home | Often claimed as part of the covered fire loss | Insurer may argue cleaning is enough when replacement is needed |

| Ash contamination | May be part of the loss if it physically affects the property | Homeowners often fail to document where ash traveled and what it affected |

| Debris removal | Often available, but how it's handled depends on policy wording and claim setup | People assume it's always unlimited or separate |

| Trees, shrubs, fences, and similar exterior items | Coverage may exist, but often with tighter limits or restrictions | Outdoor property is frequently underpaid or subject to sublimits |

Landscaping is where expectations crash

A lot of people learn too late that policies may limit payment for trees, shrubs, fences, and detached exterior features. That doesn't mean you shouldn't claim them. It means you should read the policy language carefully and document each damaged item instead of presenting the yard as one broad loss.

If you're trying to reduce future risk while rebuilding, it's worth reviewing strategies for fire-safe landscaping. Not as a design trend, but as claim prevention. The closer vegetation, fencing, mulch choices, and outbuildings are to the structure, the more they affect both fire behavior and insurer scrutiny.

Smoke claims need a paper trail

A nearby wildfire can leave a house standing but contaminated. That's where homeowners often under-document the claim. They take a few exterior photos and assume the odor speaks for itself.

It doesn't.

Use a room-by-room process. Photograph residue, vents, windowsills, attic spaces, HVAC returns, furniture surfaces, closet contents, and any visible staining. If contractors or remediation vendors inspect the property, keep every written finding. A detailed property inspection checklist for insurance claims can help you organize what to capture before cleaning or disposal starts.

If you throw away damaged items before you've photographed and listed them, you make your own claim harder to prove.

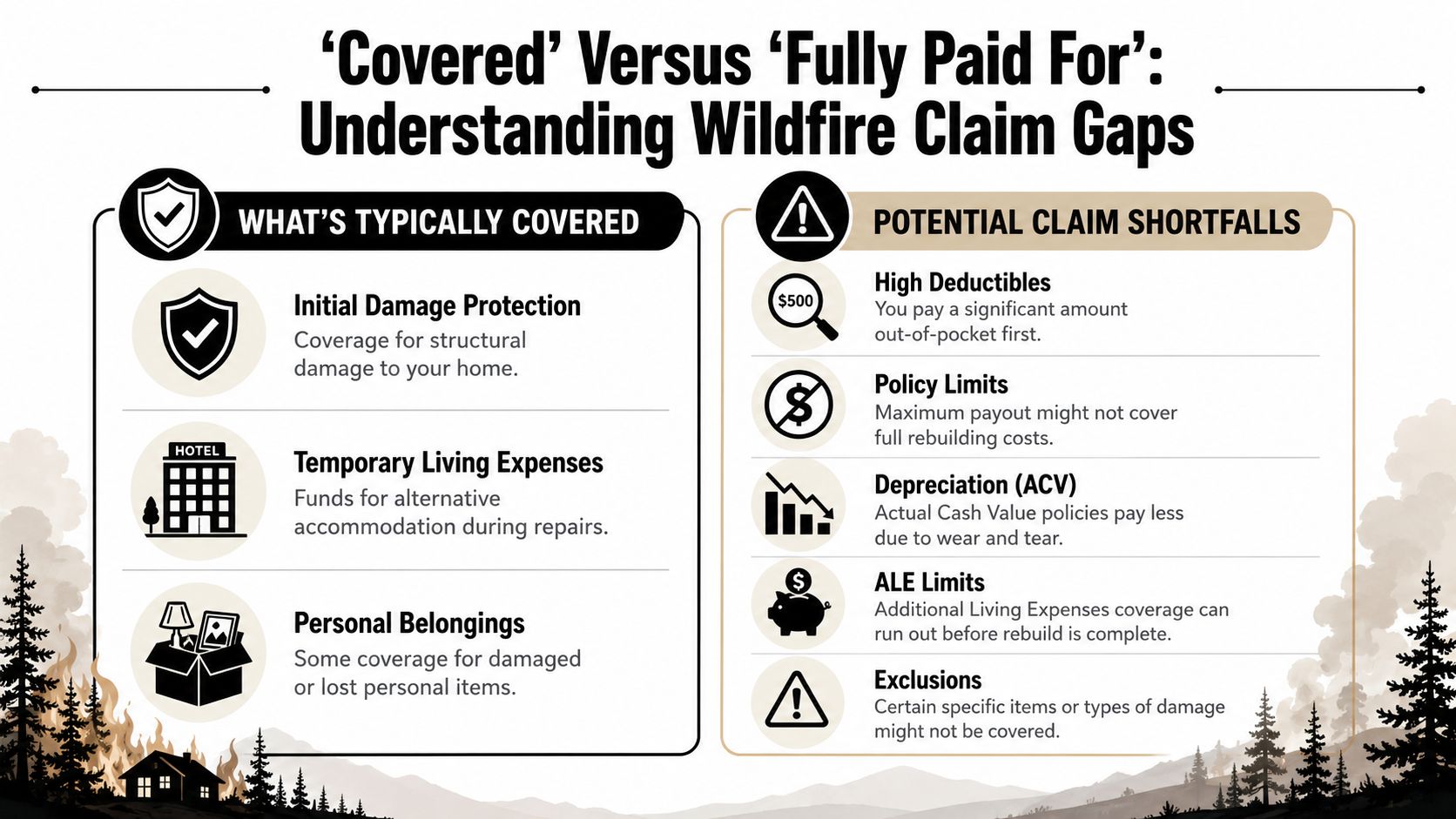

Why Covered Does Not Mean Fully Paid For

A wildfire claim often turns into a money fight after the carrier accepts coverage. The dispute then centers on scope, pricing, timing, and proof. Homeowners hear “covered” and expect the insurer to fund the full recovery. Those are not the same thing.

I see this problem constantly. The policy opens the door to payment, but the claim file decides how much comes through it.

The market pressure behind tougher claims handling

Insurers are dealing with rising wildfire exposure, higher rebuilding costs, and more pressure on pricing. In California, analysts at the Berkeley Terner Center found premium increases above 10% in the prior year, along with reduced availability from some carriers. The same analysis reported dwelling-fire premiums rose from $150 to $230 per $100,000 of covered value between 2018 and 2021, while fire-loss-to-premium ratios were higher for dwelling-fire policies than for standard homeowners policies over that period, according to the Terner Center's insurance market analysis.

That pressure reaches the claim desk. Carriers scrutinize estimates harder, question repair scope more aggressively, and look for policy provisions that limit what they owe.

Where homeowners get paid less than they expected

Underpayment rarely arrives as a dramatic denial letter. It usually shows up in pieces.

- Policy limits stop the claim at a fixed ceiling: If local rebuild costs have climbed faster than your coverage, the house may be insured for wildfire and still be short on funds. Reviewing how homeowners policy limits work after a major loss helps before a fire and matters even more after one.

- Deductibles cut into recovery immediately: In higher-risk areas, the deductible can be large enough to change what the claim puts back in your pocket.

- Contents payments may come in stages: Carriers often pay actual cash value first, then hold back the rest until replacement is completed and documented.

- Additional living expense coverage has a clock on it: Rebuild delays, permit issues, and contractor shortages can outlast the benefit period.

- Scope disputes trim the claim: Smoke cleaning, demolition, code upgrades, debris removal, and detached structures are frequent pressure points.

That is the gap homeowners need to understand. Covered means the peril is insured. Made whole depends on limits, valuation rules, documentation, and whether the insurer's estimate matches what the loss really costs.

Insurability affects claims too

Wildfire risk now affects both who can get coverage and how closely a property is examined after a loss. Insurers and regulators increasingly use wildfire risk scoring and mitigation inspections in underwriting. Carriers may require a Class A roof, ember-resistant vents, and defensible space because those features reduce structural ignitability and the odds of a total loss, according to the National Association of Realtors consumer guide on fire damage and policy coverage.

After a fire, that history can matter. If the carrier had prior inspection notes, mitigation requirements, or underwriting conditions in the file, expect those details to get attention during the claim.

A wildfire claim can be fully covered on paper and still leave the homeowner short on repair money, temporary housing, or personal property recovery.

What Oregon and Washington Homeowners Must Know

Oregon and Washington homeowners don't live in the same insurance environment as someone reading a national article from a coastal metro with very different fire patterns. In the Pacific Northwest, the questions are increasingly local. Foothill communities, timber-adjacent neighborhoods, canyon properties, and homes along the wildland-urban interface face a different underwriting reality than urban infill homes.

In practice, that means carriers may look harder at roof type, venting, access, surrounding vegetation, slope, and whether prior inspections flagged mitigation issues. Even when a standard homeowners policy still covers wildfire as a peril, the harder question can be whether the carrier wants to write or renew the policy at all.

Local homeowners should review more than the declarations page

A declarations page tells you the broad numbers. It doesn't tell you enough about the weak points in a wildfire claim. Oregon and Washington homeowners should also review endorsements, loss settlement wording, detached structure treatment, ALE language, and post-loss duties.

If you've been non-renewed, moved to a less favorable form, or told to complete mitigation before renewal, take that seriously. Waiting until smoke season to read the policy is late. Waiting until after a fire is later.

State-specific help may matter if the standard market tightens

Some homeowners who can't get traditional coverage end up exploring FAIR Plan or other residual-market options where available. Those plans can keep insurance in place, but the form and scope of coverage may not match what the homeowner had before. That's why policy comparison matters more than getting any policy bound.

For people dealing with a live loss in the region, local claim handling knowledge matters too. Building costs, debris issues, code compliance, contractor availability, and insurer response can all play out differently in Oregon and Washington than they do in national guidance pieces. Homeowners who need claim representation often look for someone licensed in-state, such as an Oregon public adjuster familiar with regional property claims.

The main point is simple. Pacific Northwest homeowners shouldn't assume that because wildfire coverage exists in general, their own policy, carrier appetite, and claim outcome will line up cleanly.

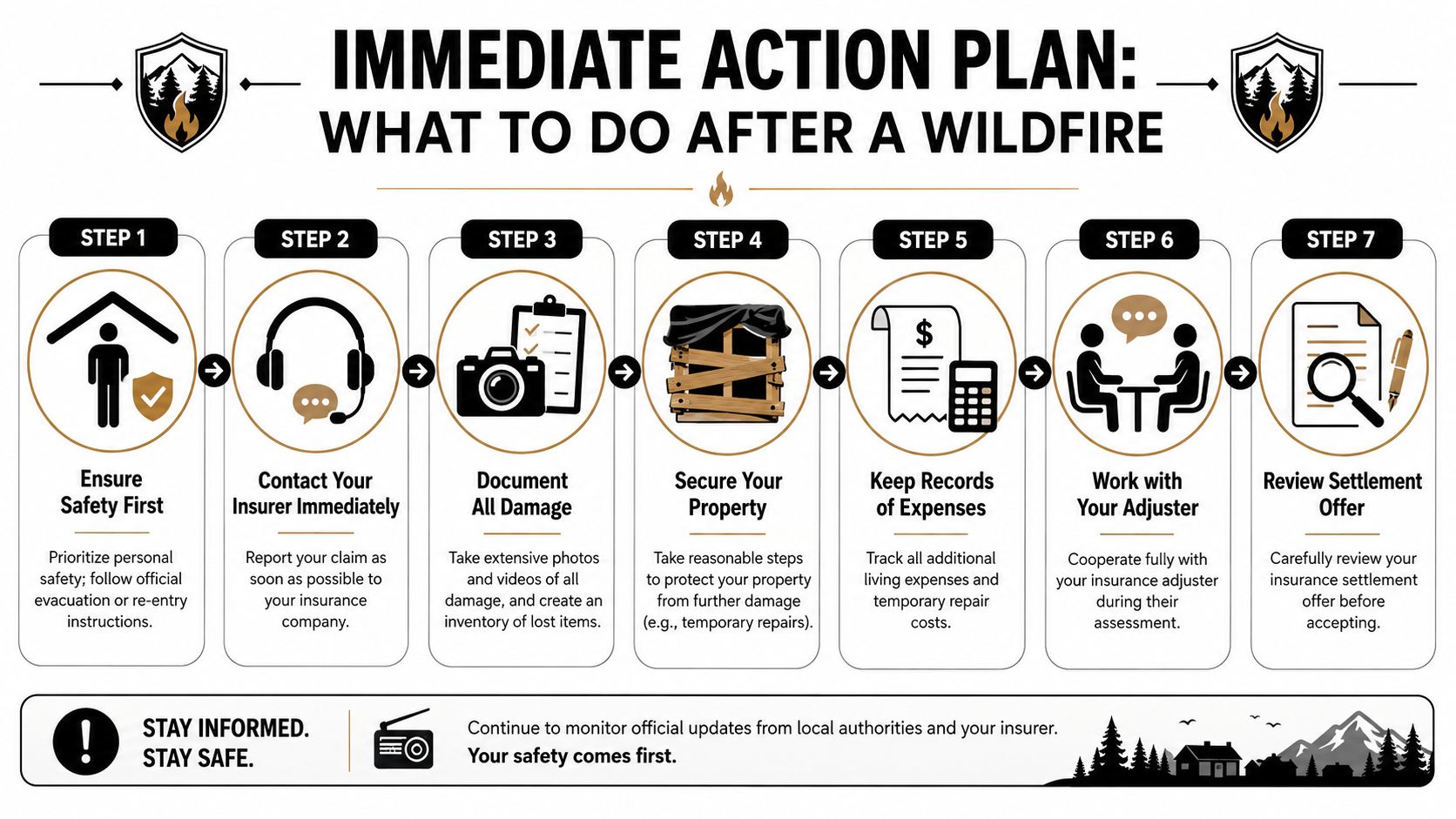

Your Action Plan After a Wildfire

The first days after a wildfire are messy. You may be displaced, dealing with authorities, trying to locate records, and making decisions while exhausted. The right sequence helps protect both your safety and your claim.

The first moves that protect your rights

- Follow safety and re-entry instructions first. Don't enter a property before officials say it's safe.

- Report the claim promptly. The Insurance Information Institute, as summarized by Progressive, notes that insureds should check deadlines and submit proof of loss promptly after a fire.

- Stop further damage if you can do it safely. Temporary board-up, tarping, or securing openings may be necessary.

- Start a dedicated claim file. Keep emails, claim numbers, receipts, inspection notes, hotel invoices, and contractor communication in one place.

Documentation wins the argument later

Once you can access the property, document before cleanup changes the scene.

- Photograph broadly first: Start outside, then move room by room.

- Video the condition in one continuous pass: Narrate what you're seeing if helpful.

- List damaged contents in plain language: Brand, model, age, where it was located, and condition before loss.

- Save every extra expense receipt: Hotels, rentals, meals if applicable under the policy, laundry, storage, pet boarding, and temporary supplies.

If your roof took ember damage or you're dealing with overlapping fire and roofing issues, homeowners sometimes find it helpful to review practical guidance on managing your roof claim effectively so they don't miss a major component of the property loss.

Don't wait for the insurer's adjuster to “discover” everything. Your record should exist before their estimate does.

Treat the insurer's estimate as a starting position

The carrier's adjuster is part of the process, but their scope and pricing aren't automatically final. Read the estimate line by line. Look for omitted rooms, short contents lists, incomplete smoke remediation, missing code items, and low allowances for detached structures or cleanup.

If the claim becomes too large or technical to manage alone, homeowners sometimes hire a public adjuster to document the loss, interpret policy language, assemble estimates, and negotiate with the insurer on the policyholder's behalf. One example in Oregon and Washington is NW Claims Management's wildfire and fire claim support, which focuses on representing insured property owners rather than insurers.

Before you sign a proof of loss, accept a final settlement, or dispose of major damaged items, make sure the numbers reflect the full claim. A wildfire loss feels urgent, and it is. But rushed acceptance can lock in a shortfall that follows you through the entire rebuild.

When a wildfire claim is turning into a valuation fight, NW Claims Management helps Oregon and Washington property owners document damage, interpret policy language, and negotiate with insurers for a fair settlement. If you're unsure whether your wildfire loss has been fully scoped or properly valued, a direct review of the claim can clarify what's covered, what's missing, and what to do next.