Your roof is bruised by hail, water is finding its way where it shouldn't, and your insurer has already started asking for photos, dates, inventories, receipts, and recorded statements. You're exhausted before the actual argument has even begun.

That's normal. It's also dangerous.

Most Denver homeowners think the hard part is surviving the storm, the fire, or the pipe break. It isn't. The hard part is converting damage into a properly documented insurance claim that your carrier can't casually shrink, delay, or reclassify. If you're dealing with a major loss, especially a roof claim after hail, you're not stepping into a customer service process. You're stepping into a negotiation.

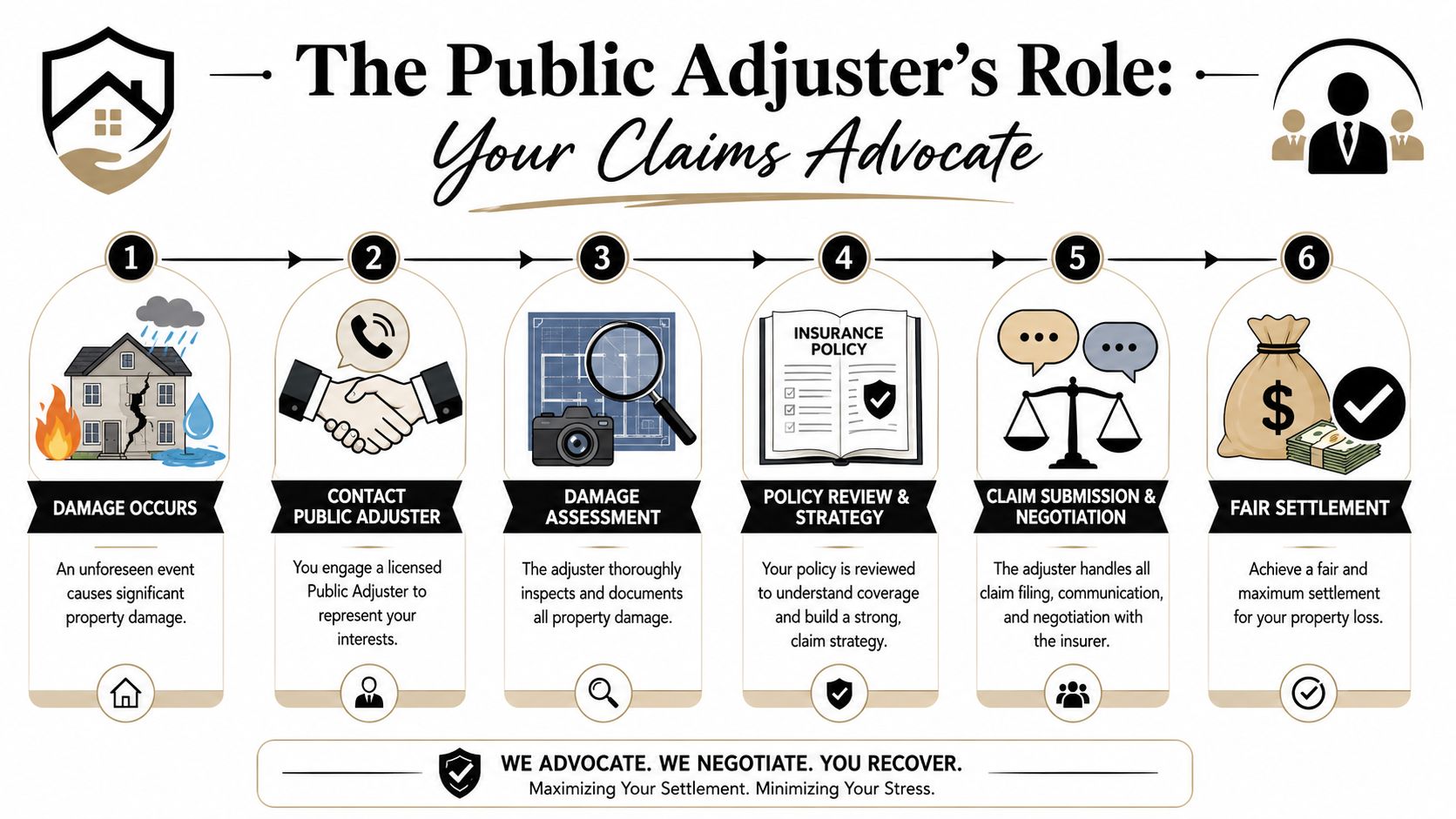

A public adjuster in Denver works for you, not for the insurance company. That distinction matters more than people realize. The company adjuster has a job. You need an advocate. If you're still sorting out emergency repairs, this practical 2026 restoration company guide can help you organize the mitigation side while you protect the claim side. And before you say the wrong thing or leave out something important, review this guide on how to file a property damage claim.

After a Disaster Your Insurance Claim Is Your Next Battle

The first day after a loss usually looks the same. You walk the property with your phone in your hand. You notice the obvious damage first. Missing shingles. Wet drywall. Smoke residue. Broken windows. Then the less obvious problems start showing up. Water behind trim. Soft spots in ceilings. HVAC contamination. Gutter and downspout impact. Detached flashing. Interior staining that wasn't there yesterday.

Then the calls begin.

The insurance company wants to open a claim. A contractor wants to inspect. Someone says don't worry, it'll all be covered. Someone else says don't file too fast. You're stuck between urgency and uncertainty, and that's exactly when bad decisions get made.

A lot of homeowners in Denver get blindsided on roof claims because they assume hail damage will speak for itself. It won't. Insurers often dispute whether the roof damage came from a covered storm event or from age, wear, prior deterioration, foot traffic, or installation defects. If your documentation is weak, your claim gets framed by the other side first.

Your policy is a contract. Your claim file is the evidence. If you don't control the evidence, you don't control the outcome.

That's why a public adjuster matters. Not as a luxury. As a counterweight. The insurer's adjuster represents the insurer. A public adjuster represents the policyholder. Those are not the same mission, and pretending they are is how people leave money, scope, and coverage on the table.

Your Advocate in the Claims Process

A public adjuster is to your property claim what a CPA is to your taxes. You can try to handle it alone. Sometimes that works. But when the file gets technical, the language gets dense, and the stakes get expensive, experience stops being optional.

What the job actually involves

A strong public adjuster doesn't just “help with paperwork.” That phrase undersells the work.

They review the policy line by line. They identify what coverage applies, what deadlines matter, what proof is required, and where the insurer may try to narrow the claim. They inspect the damage as a claim professional, not just as a contractor or homeowner. Then they build a defensible scope.

That technical edge comes from combining construction knowledge, policy interpretation, and estimate software proficiency such as Xactimate, which helps them separate cosmetic damage from functional damage, identify hidden or consequential loss, and produce a scope an insurer can test against its own estimate, as described in this industry explanation of what it takes to be a public adjuster.

If you want the clearest side-by-side breakdown of roles, read this comparison of public adjuster vs insurance adjuster.

Where Denver roof claims get technical fast

Hail claims are where inexperience gets expensive.

A roof can show visible impact marks and still trigger a fight over whether the damage affects function, reduces service life, or just counts as cosmetic marring. The adjuster you hire needs to understand roofing systems, slope-by-slope documentation, soft metals, collateral indicators, flashing, vents, underlayment implications, and what interior conditions support exterior causation.

A good public adjuster also knows that roofs are rarely the whole claim. When hail or wind compromises the building envelope, related damage can spread into other categories that require separate support.

That often includes:

- Debris removal: If the policy supports it, cleanup may need to be valued and included rather than absorbed into a rough contractor total.

- Code-related items: Some upgrades only belong in the claim when local requirements and policy terms support them.

- Contents exposure: Water, dust, smoke, or impact can affect personal property even when the structure gets most of the attention.

- Additional living expense: If the loss forces displacement, your receipts and timeline matter.

What you should expect from the right adjuster

You should expect a process, not promises.

A competent public adjuster should inspect thoroughly, photograph aggressively, measure carefully, organize the file, communicate in writing, and negotiate from evidence. They should be able to explain why an item belongs in the claim, where that support comes from, and what documentation still needs to be gathered.

The best adjusters don't sell confidence. They sell documentation.

If someone mainly talks about “maximizing” without talking about scope, policy language, causation, and proof, keep looking.

Ensuring Your Adjuster Is Legitimate and Licensed

When a neighborhood gets hit hard, good professionals show up and bad actors do too. Don't hire anyone until you verify they're legitimate.

Colorado regulates this profession for a reason

Public adjusting isn't a casual side hustle in Colorado. It's a regulated profession. Colorado requires licensing, and for non-resident public adjusters, the state requires a $20,000 surety bond, which creates a compliance and accountability layer for policyholders handling Denver-area claims, according to the Colorado licensing requirements listed through NIPR's Colorado non-resident adjuster licensing page.

That doesn't mean every licensed adjuster is excellent. It does mean anyone who isn't properly licensed is disqualified before the conversation starts.

You should also understand what licensing does and doesn't tell you. It tells you the person has met regulatory requirements. It does not tell you whether they know Denver hail claims, roofing systems, business interruption, smoke contamination, or complex water losses. That's where your vetting matters.

For a broader overview of credentials that matter in this field, review these claim adjuster certifications.

How to verify before you sign

Don't overcomplicate this. Use a short checklist and stick to it.

- Confirm the license is active: Ask for the full legal name and license details before discussing your claim in depth.

- Ask whether they're resident or non-resident: Either can be valid if they meet Colorado requirements, but you want a direct answer.

- Request proof of professional insurance and business identity: A real firm should have no issue providing documentation.

- Read the contract before you sign: If the fee language, cancellation terms, or scope of representation feel slippery, stop.

Practical rule: If a person asks for trust before they provide credentials, they're asking in the wrong order.

Storm chasers sound smooth

The people you want to avoid usually sound polished. They knock doors right after a storm. They say your insurer is definitely going to pay. They rush your signature. They make it sound like licensing and contract details are just technicalities.

They aren't.

A legitimate public adjuster should welcome scrutiny. If they get irritated when you ask for proof, that's your answer.

Is Hiring a Public Adjuster Worth It for Your Claim

For a small, clean, undisputed claim, maybe not. If the loss is minor, the scope is obvious, and the carrier is handling it promptly and fairly, you may not need outside representation.

That's not the typical scenario when someone searches for a public adjuster in Denver.

When the answer is yes

If your claim involves major hail damage, a disputed roof, fire, heavy water damage, a partial denial, or an offer that feels suspiciously thin, hiring a public adjuster is usually a smart move. Not because every insurer acts in bad faith. Because complexity favors the side with the better file.

One widely cited industry benchmark says using a public adjuster can raise insurance claim payouts by 747%, a figure often attributed to a government study and repeated in Denver-focused public adjusting content, including this Denver public adjuster page from Noble Public Adjusting Group. I treat that as an industry talking point, not a guarantee. But the reason the figure keeps resurfacing is simple. Representation changes how claims are documented, argued, and negotiated.

Here's my blunt advice. If your roof claim is being pushed into “wear and tear,” if parts of the loss are being ignored, or if the insurer's estimate doesn't match what the property needs, don't handle that like a routine errand.

When you might skip it

There are cases where hiring a public adjuster isn't worth it.

A few examples:

- Very small losses: If the claim is simple and the disputed amount is limited, the economics may not justify representation.

- Straightforward scope: If damage is obvious, accepted, and fully valued, adding another professional may not change much.

- You already have strong technical support: Some policyholders have unusually strong documentation and experienced professionals around them.

Still, most homeowners aren't equipped to challenge a weak roof determination on their own. If you're unsure where your claim falls, this breakdown of the benefits of hiring a public adjuster is a useful gut check.

If the claim is complex enough to keep you awake at night, it's complex enough to justify a serious review.

Your Checklist for Hiring a Denver Public Adjuster

Don't hire the first person who sounds confident. Hire the one who can prove they know how to build and defend your claim.

The Denver market attracts capable adjusters and opportunists. Your job is to separate them quickly.

Start with the non-negotiables

Ask for the basics first. Credentials. Contract. Experience with your exact type of loss. If they can't provide those without drama, move on.

The local labor market also gives useful context. ZipRecruiter's Denver data lists average annual pay for public adjusters at $66,844 as of June 5, 2026, which helps explain why experienced professionals price their time and expertise seriously on complex files, according to ZipRecruiter's Denver public adjuster salary page. Don't use that figure to compare fee proposals line by line. Do use it as a reminder that skilled claim representation is a real profession, not a side gig.

Public Adjuster Vetting Checklist

| Verification Item | What to Look For |

|---|---|

| License status | Active Colorado authority to act as a public adjuster |

| Contract clarity | Clear fee terms, cancellation language, and scope of representation |

| Claim type experience | Direct experience with hail, roof disputes, fire, water, or large-loss residential claims like yours |

| Documentation process | A real explanation of inspections, photos, measurements, and estimate preparation |

| Communication style | Direct answers, written follow-up, and no pressure to sign on the spot |

| Point of contact | One accountable person who will actually manage your file |

| Local familiarity | Understanding of Denver claim patterns, roofing issues, and insurer dispute themes |

| Professional references | Past clients or industry references who can speak to process and follow-through |

Questions worth asking in the interview

Don't ask soft questions. Ask questions that expose process.

- How do you evaluate a disputed roof claim? Listen for specifics such as slope documentation, collateral indicators, functional damage analysis, and policy support.

- Who writes the estimate? You want to know whether the person you meet does the technical work.

- How do you handle communication with the insurer? Good answer: organized, written, persistent.

- Can you show me a sample report or estimate format? You're not asking for another client's private file. You're asking how they present evidence.

- What happens if the insurer says the damage is old or unrelated? This answer tells you whether they know causation battles or just sales language.

What a good answer sounds like

A strong adjuster will sound measured, not theatrical. They'll explain their method. They'll identify what still needs investigation. They won't guarantee a payout number. They won't pretend every roof should be replaced. And they won't dodge contract questions.

A weak adjuster leans on slogans. “We maximize claims.” “We handle everything.” “Don't worry about it.” That's not competence. That's a script.

If you remember only one thing, remember this. Hire the person who can explain the file, not the person who flatters your expectations.

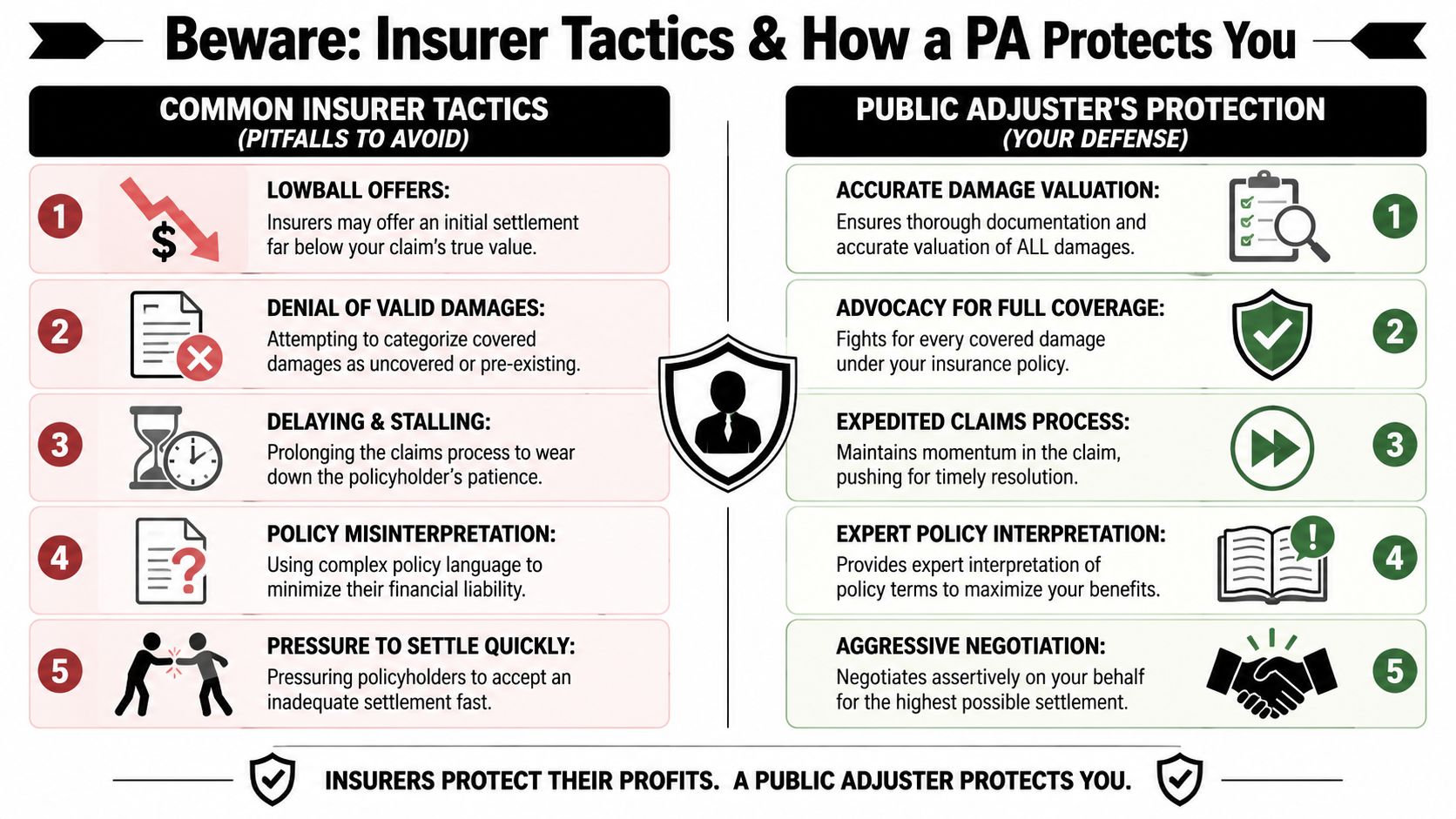

Protecting Yourself from Lowball Offers and Bad Actors

Denver roof claims have a pattern. The homeowner reports hail. The carrier inspects. Some items get acknowledged, some get minimized, and the most important debate often becomes causation. Was that damage from the storm, or was it old? Was it functional, or merely cosmetic? Was it hail, foot traffic, blistering, age, installation error, or “normal wear”?

That argument is where many valid claims lose traction.

The insurer tactic Denver homeowners miss

A key issue in Denver is hail-driven roof claims where insurers may attribute damage to wear and tear or pre-existing conditions instead of storm loss, a dispute point highlighted in this Denver-focused discussion of public adjuster support for Denver claims. That matters because roof claims aren't won by saying, “You can see the damage.” They're won by documenting why the observed condition ties back to covered loss.

Public adjusters earn their keep by forcing precision into the file. They detail which elevations show impact. Which soft metals support storm activity. Which interior symptoms align with exterior compromise. Which line items the insurer omitted. Which exclusions are being stretched too far.

If you suspect the insurer is playing games, review these common insurance adjuster tricks.

Red flags from insurers

Not every hard conversation is unfair. But these patterns should make you cautious:

- Fast pressure to close: If the company wants the claim wrapped before the scope is mature, slow down.

- Selective visibility: They discuss the roof surface but skip accessories, interior staining, or related components.

- Broad labels: “Wear and tear” gets used as a shortcut when the file lacks disciplined storm analysis.

- Thin estimates: The paperwork looks official, but key repairs are missing or undervalued.

When the explanation is vague and the estimate is thin, the burden shifts to you to prove what the carrier left out.

Red flags from bad public adjusters

Homeowners can get hit from both sides. A weak insurer response is one risk. A predatory representative is another.

Watch for these warning signs:

- Upfront pressure after a storm: Good professionals don't need panic to close business.

- Guaranteed settlement numbers: No honest adjuster can promise a specific outcome before the file is built.

- Messy contract language: If the agreement feels confusing now, it won't get clearer later.

- No real inspection method: If they don't talk about measurements, photos, scope, and policy support, they may not know how to do the work.

The right adjuster lowers your risk. The wrong one multiplies it.

Take Control of Your Property Claim Today

If you're dealing with a major property loss in Denver, stop thinking like a claimant and start thinking like the keeper of evidence. That mindset changes everything.

Your roof claim, fire claim, or water claim won't be decided by how frustrated you are. It will be decided by documentation, policy language, causation, scope, and persistence. That's why licensed public adjusting matters. It levels the field for homeowners who are otherwise expected to manage a technical dispute while also trying to stabilize their home and family.

Use the state's consumer resources. Contact the Colorado Division of Insurance to verify a license, raise concerns, or get help when the claim process goes sideways. If your home is unsafe or you're managing immediate damage control, lean on municipal and county emergency resources as needed. Separate the emergency response from the claim strategy. Both matter, but they aren't the same job.

If your Denver hail claim is already being narrowed into wear and tear, don't ignore that. That's usually the core dispute, not a side issue. Get the file reviewed before you accept the insurer's framing of the loss.

You don't need more reassurance. You need a disciplined claim strategy and the right professional on your side.

If you want a second set of eyes on your property loss, NW Claims Management offers a complimentary, no-obligation claim evaluation. The firm serves policyholders in Oregon and Washington directly, and if you need local representation in Denver, they can help you think through the claim issues and refer you to a vetted public adjuster who handles Colorado losses.