The fire is out. The engine lights are gone. You are standing in a wet driveway in socks, staring at broken windows, smoke stains, and a kitchen that no longer looks like your home.

Then the insurance process begins.

Many believe the hard part is the disaster itself. In my experience, the second hard part is the claim. You are tired, worried about where you will sleep, and suddenly expected to make careful decisions about damage, coverage, inventory, estimates, and deadlines. If you say too little, you risk leaving money on the table. If you say the wrong thing, you can create problems you did not mean to create.

That is why people start looking at firms like allied public adjusters. They are trying to answer a practical question: who can stand beside me, speak the insurance company’s language, and help me recover what my policy owes?

For homeowners and business owners in Oregon and Washington, there is one more layer to that question. A national firm may have a strong reputation, but you still need to know whether that firm understands Pacific Northwest claims, local rules, wet-weather damage patterns, smoke migration, contractor pricing, and the licensing standards that protect you here.

After the Disaster Why You Need an Advocate

At two in the morning, after a house fire, the questions come fast. Where will we sleep tonight? Is the roof safe? What do I tell the insurance company in the morning? By breakfast, you are being asked about square footage, personal property, cleanup, and whether the damage is from fire, smoke, water, or all three.

That last part trips people up in Oregon and Washington all the time. A single loss often has layers. Fire leads to water damage from suppression. Wind opens the roof, then steady rain works into insulation and drywall. Smoke travels farther than people expect, especially in our tighter homes and damp conditions, where odor can cling to framing, textiles, and HVAC systems.

Insurance companies move quickly to open a claim, and that can feel reassuring. It should. A claim needs attention right away.

But quick contact is not the same as personal advocacy.

The carrier’s adjuster is there to inspect the loss and evaluate it for the insurer. Your interests may overlap in some areas, but they are not the same in every conversation, estimate, or coverage decision. If the loss is large, the scope is changing, or the numbers do not line up with what your contractor sees on site, it helps to have someone who is reading the same policy and file from your side.

A public adjuster fills that role. They work like a skilled bookkeeper during a messy rebuild. They gather the details, organize the record, catch what is missing, and present the claim in a way the insurer can evaluate. For a family living out of a hotel or with relatives, that support is not about making the claim dramatic. It is about making it accurate.

That need becomes even clearer here in the Pacific Northwest. National firms such as Allied Public Adjusters may be part of your search, but homeowners here should ask a local question first. Is the adjuster properly licensed for Oregon or Washington, and do they understand how claims play out here, with regional contractor pricing, wet-weather damage, smoke migration, and state rules that govern public adjusters? A national name can be fine. Local knowledge still matters, because claims are settled on the ground, not in a brochure.

I hear the same sentence from clients after major losses: “I thought this would be simpler.”

That reaction makes sense. A serious property claim is part documentation project, part policy review, and part negotiation. If you want a clearer sense of the moments where outside help starts to make sense, this plain-English guide on spotting the turning points in a claim is a useful place to start.

After a major loss, control feels scarce. An advocate helps you rebuild some of it by turning a pile of damage, photos, receipts, and questions into a claim that is organized, supported, and ready to stand up under scrutiny.

What a Public Adjuster Is and Who They Work For

After a fire, a lot of homeowners hear three different people described as “the adjuster” and assume they all serve the same role. That is where confusion starts.

A public adjuster is a state-licensed insurance claim representative for the policyholder. In plain terms, this is the person you hire to stand with you, document the loss, present the claim, and negotiate from your side.

That distinction matters a great deal in Oregon and Washington, where licensing rules, contract requirements, and claim handling expectations are set at the state level. A national firm may be well known, but the person handling your claim should be properly licensed where your property sits and familiar with how losses are evaluated here in the Pacific Northwest. Local contractor pricing, moisture exposure, smoke spread in tightly built homes, and regional rebuilding conditions all affect how a claim should be documented.

The three adjusters people confuse

Homeowners usually run into three categories of adjusters during a claim:

| Type of adjuster | Who they work for | What that means for you |

|---|---|---|

| Staff adjuster | Insurance company | Employee of the carrier reviewing the claim for the insurer |

| Independent adjuster | Insurance company | Outside contractor hired by the carrier, still representing the insurer |

| Public adjuster | Policyholder | Licensed representative hired to prepare and negotiate the claim for you |

A simple comparison helps. A public adjuster works like the accountant you hire during a difficult tax dispute. The insurance company may have its own people reviewing the file, but your professional is there to protect your interests, not the carrier’s.

If you want a clear, plain-English overview, this page helps explain the role of a public adjuster.

What they do

Public adjusting is not one phone call and a few photos. It is a methodical claim-preparation job that blends construction knowledge, policy reading, documentation, and negotiation.

That usually includes:

- Inspecting the property in detail: fire, smoke, water, soot, and secondary damage

- Reviewing the policy: covered categories, limits, deadlines, duties after loss, and exclusions

- Preparing the claim file: estimates, inventories, measurements, photos, and supporting records

- Handling insurer communication: keeping the file organized and responses timely

- Negotiating scope and value: correcting omissions, low pricing, and incomplete evaluations

For a Pacific Northwest homeowner, one of the practical benefits of the right adjuster is context. A person who works claims here should understand issues such as persistent moisture after firefighting efforts, smoke movement through crawlspaces and attics, and why local labor and material costs can differ sharply from national estimating assumptions.

Where Allied Public Adjusters fits

Allied Public Adjusters is one example of the kind of firm homeowners may find while researching representation after a major loss. The important question is not just the company name. It is whether the adjuster assigned to your file is licensed in your state, knows the rules that apply in Oregon or Washington, and can handle a claim in a way that matches local conditions.

That is the key point to keep in mind. A public adjuster works for you. If you are comparing a national firm like Allied Public Adjusters with a local Pacific Northwest expert, start with allegiance, then confirm licensing, state law compliance, and on-the-ground knowledge of how claims are resolved here.

A Deep Dive into Public Adjuster Services

When people ask what they are paying for, I tell them this: you are not hiring someone to “make a few phone calls.” You are hiring someone to build a claim the insurer has to take seriously.

With a firm like allied public adjusters, the value is in the process. Good public adjusting is technical, detailed, and relentless in the right way.

Policy review that finds what often gets overlooked

Insurance policies are contracts. They are also full of language that many homeowners only read after something terrible happens.

A seasoned public adjuster reviews the policy with one question in mind: what does this loss trigger? That may include dwelling coverage, debris removal, code-related items, business interruption, or Additional Living Expense if you cannot stay in the home.

A common mistake after a fire is focusing only on the visible rebuild. But the policy may also address smoke contamination, temporary housing, contents cleaning, and related soft costs. If those items are not raised properly, they can be minimized or omitted.

Damage assessment that goes past the obvious

After a fire, the obvious damage gets attention first. The hidden damage is where many claims go sideways.

A strong public adjuster documents not just what burned, but also what smoke affected, what water reached, what materials now need replacement, and what secondary conditions could worsen if ignored. Firms like Allied Public Adjusters say they use a proprietary claims process with engineering and forensic expertise to achieve 633% higher average settlements than competitors by documenting damage often missed in insurer assessments, according to Allied’s public adjuster resource page.

That does not mean every claim turns into a dramatic dispute. It means the file is built with technical depth from the start.

Inventory and loss presentation

Contents claims are where many families feel overwhelmed.

You are asked to remember what was in dresser drawers, hallway closets, kitchen cabinets, storage bins, and the garage. Then you are expected to describe, price, and support those items while displaced and stressed.

A public adjuster helps turn that chaos into a usable inventory.

They often help with:

- Room-by-room reconstruction: Identifying what was in each area before the loss.

- Categorizing damaged property: Separating salvageable items from replacement items.

- Supporting values: Matching items to fair replacement descriptions so the claim is harder to discount.

- Packaging the claim: Presenting the loss in an organized format the insurer must address.

Key takeaway: The better the documentation, the less room there is for an insurer to say, “We did not see that,” or “That item was not supported.”

Negotiation backed by evidence

Negotiation is not just arguing for more money. It is showing why a line item belongs, why a quantity is correct, why a finish level matters, and why a repair method is incomplete.

That usually involves combining several kinds of evidence:

| Service | Why it matters in a claim |

|---|---|

| Policy interpretation | Connects damage to the right coverage sections |

| Forensic documentation | Supports hidden or disputed damage |

| Detailed estimating | Prevents broad, vague underpricing |

| Claim presentation | Forces a response to specifics, not generalities |

When this is done well, the claim becomes less emotional and more defensible. That shift matters. Insurance companies respond best to organized proof.

Your Insurance Claim Journey with a Public Adjuster

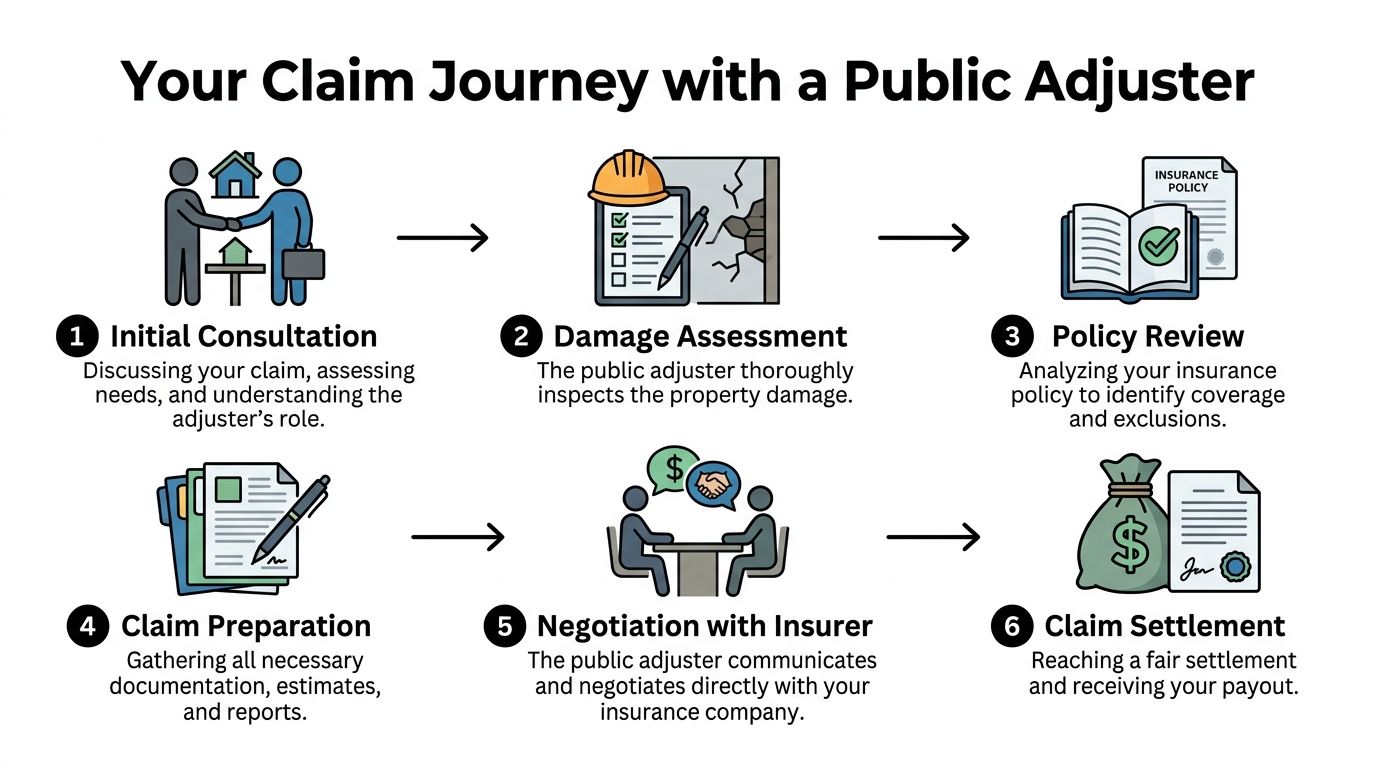

Policyholders often calm down once they can see the path ahead.

The claim journey is still work, but it feels less overwhelming when you know what happens first, what comes next, and where a public adjuster takes weight off your shoulders.

Step one is the first conversation

The relationship usually begins with a consultation. You explain what happened, what the insurer has done so far, and where things feel unclear.

During this conversation, a good adjuster listens for trouble spots. Was the claim reported properly? Has emergency mitigation been done? Did the carrier inspect yet? Are you already being asked for a recorded statement, estimates, or a contents list you are not ready to complete?

The point is not to pressure you into signing anything. The point is to understand the loss and decide whether professional representation is useful.

For a broader view of the sequence, this overview of the property damage claim process gives a solid framework.

Step two is the site inspection

Then comes the fieldwork.

A public adjuster inspects the property in a much more deliberate way than most homeowners expect. In fire losses, that may mean tracing smoke spread, checking insulation, examining cabinetry interiors, documenting soot deposition, and noting where water from firefighting moved through floors or wall cavities. In water losses, it means following moisture migration, not just photographing the stain on the ceiling.

Advanced public adjusters use diagnostic tools like FLIR thermal imaging cameras to detect hidden moisture and structural weaknesses, identifying latent issues that can increase repair costs by 20% to 50% if not caught during the initial assessment, according to Allied’s team and process material.

That matters in the Pacific Northwest. Our claims often involve prolonged damp conditions, layered water intrusion, and hidden moisture that lingers behind finished surfaces.

Step three is policy review and claim strategy

After inspection, the work shifts to the contract itself.

The adjuster reads the policy and compares it to the loss. They identify what parts of the damage belong under which coverage. They also watch for practical issues that homeowners miss when they are under stress, such as deadlines, documentation requirements, or the difference between repair cost and replacement language.

Here, strategy takes shape. Not gamesmanship. Strategy.

For example, a water loss may involve drying, demolition, reconstruction, temporary housing, damaged contents, and code-related repair questions. Each needs to be framed properly or it may be undervalued.

If you are dealing specifically with moisture-related loss, this guide on filing an insurance claim for water damage is a helpful companion because it explains the kinds of documentation and early decisions that often affect the rest of the claim.

Step four is assembling the claim package

This is the part homeowners rarely see coming.

The public adjuster gathers photographs, measurements, estimates, notes, inventories, contractor input, and other supporting material into a formal submission. If the claim is large, this can take real time. But speed is less important than accuracy.

A strong package does several things at once:

- It defines the loss clearly

- It ties the damage to the policy

- It supports pricing with detail

- It reduces room for broad denials or omissions

Tip: If you hand the insurer a rough list and a few photos, you often get a rough response. If you hand them a documented claim file, the conversation changes.

Step five is negotiation and follow-up

Once the insurer reviews the submission, there is usually back-and-forth.

Sometimes the carrier agrees with much of the claim. Sometimes it does not. A public adjuster then pushes on specific disagreements. They may challenge incomplete scope, pricing, depreciation, causation assumptions, or missed categories of damage.

At this stage, your stress level often drops. You are no longer answering every technical question alone. You have someone managing the file, pressing for responses, and keeping the claim moving.

Step six is settlement and payout review

When the numbers finally come together, the last task is not just cashing a check.

A good adjuster reviews the settlement to see what it covers, what remains open, and whether supplemental issues still need to be raised. They help the policyholder understand what has been paid and what steps come next for repairs, contents replacement, or additional claim activity.

The best part of the process is simple. You stop carrying the whole burden by yourself.

Decoding Public Adjuster Fees Contracts and State Laws

The morning after a house fire, fee questions can feel almost rude. You are trying to find socks, medication, a place to sleep, and a path back to normal. Then someone hands you a contract full of percentages, cancellation language, and state-specific rules.

That is exactly why this part deserves a calm read.

How contingency fees work

A contingency fee means the public adjuster is paid according to the contract, usually as a percentage of the insurance recovery. They are not billing you like an attorney tracking hours or a contractor sending weekly invoices.

For many homeowners, that arrangement feels easier to manage after a loss because there is usually no large upfront retainer. The tradeoff is simple. You need to understand exactly how the percentage is calculated, when it applies, and whether it is charged on the full settlement or only on added money the adjuster helps recover.

That last point causes a lot of confusion.

If two firms both say "10 percent," those numbers may not mean the same thing in practice. One contract may apply the fee more broadly than another. That is why the contract matters more than the sales pitch. If you want a plain-English explanation before signing, this guide on the pricing model gives a helpful breakdown.

What to read in the contract

Read the agreement when you are tired anyway. Then read it once more when your head is clearer.

A good contract should spell out the parts that affect your claim and your wallet:

- Who you are hiring: The legal business name and the licensed individual who will work on the file

- What the firm will do: Inspection, documentation, estimating, contents inventory, negotiation, supplements, or other claim tasks

- How the fee works: The percentage, what money it applies to, and when it is earned

- How you can cancel: Any rescission period or cancellation steps required by state law

- Who your contact is: The person responsible for returning calls and updating you

Ask one direct question before signing: “Who will personally handle my Oregon or Washington claim, and are they licensed here?”

That answer tells you a lot.

Oregon and Washington require local verification

Pacific Northwest homeowners need to slow down and check the details here. A national firm may market heavily across the country, but your claim is governed by the law of the state where the loss happened.

In Oregon or Washington, confirm both the company and the individual adjuster are properly licensed for that state before you sign. Do not rely on a website footer, a business card, or a statement that the firm works nationwide. Ask for license information and verify it with the state regulator.

Why does that matter? Because state rules shape the contract language, consumer protections, complaint process, and the standards the adjuster must follow. A firm with hurricane experience in Florida or wildfire experience in California may still be unfamiliar with how a Northwest claim should be handled on paper and in practice.

Local presence matters too. In the Pacific Northwest, claims often involve wet weather, hidden moisture, smoke movement through tight building envelopes, regional contractor delays, and permit timelines that out-of-state firms may underestimate. A local adjuster usually understands those conditions firsthand. A national firm can still be a good fit, but only if its local licensing and local claim handling are clear.

A practical checklist before you sign

Use this like a flashlight, not a formality:

- Verify the license for the firm and the person assigned to your claim

- Read the fee section out loud until you can explain it in your own words

- Confirm the scope of work so you know what is included and what is not

- Check cancellation rights and any deadlines tied to them

- Get one point of contact by name, phone, and email

A clean contract will not settle the claim for you. But a confusing contract is often the first sign that confusion will continue after you sign.

Evaluating Allied Public Adjusters vs Local Experts

At 6 a.m., your house still smells like smoke, the tarp is snapping in the rain, and a firm from out of state says they can take over the claim right away. That can sound like relief. It can also blur the question that matters most for an Oregon or Washington owner. Who is equipped to handle this claim here?

That is the lens I would use for Allied Public Adjusters, or any national firm. Start with fit, not brand recognition. A company can be well known and still be the wrong choice for a Pacific Northwest loss if the local licensing, file handling, and regional claim experience are not clear.

What a national firm can offer

A larger firm often brings a polished intake process, organized paperwork, and experience with high-value or complex losses across several states. That can help if your claim is large, technical, or already turning into a dispute.

Allied has been in business for many years and has built a recognizable name in the policyholder-advocacy space, as noted earlier in the article. That history may give some homeowners confidence.

Still, a house fire in Seattle or a water loss in Eugene is not handled in a vacuum. The work happens on the ground. The estimate has to match local labor and material conditions. The damage has to be documented the way your carrier and your state rules require. So the next question is the practical one. Who is the adjuster assigned to your file, and how familiar are they with claims in your part of the Northwest?

Where a local Pacific Northwest expert often has an edge

This region has its own habits, and claims reflect them.

Moisture is the obvious example. After a fire or water loss, damage here often keeps evolving because rain, damp air, and slower dry-out conditions can affect insulation, framing, subfloors, and crawlspaces. Smoke claims can be tricky too. In tighter homes common across the Northwest, odor and residue can travel farther than owners expect, especially through attics, ductwork, and wall cavities.

Then there is the rebuild side. Local permit timelines, contractor backlogs, steep-site access, and code updates can all affect the true cost of repair. A local adjuster usually reads those issues almost the way a local carpenter does. They know where estimates tend to come in light and where delays are likely to show up.

That does not mean a national firm cannot do good work here. It means you should verify that the person handling your file has real Oregon or Washington claim experience, not just general catastrophe experience from another state.

The Pacific Northwest questions that matter most

If you are comparing Allied with a local firm, ask questions that expose how the claim will be handled.

- Who is licensed for my state, the company, the individual adjuster, or both?

- Who will inspect the property in person?

- Who writes or reviews the scope for hidden moisture, smoke spread, and code-related repairs?

- How often do you handle Oregon or Washington claims like mine?

- Will my file stay with one adjuster, or move between intake, inspection, and negotiation staff?

- How do you account for local contractor pricing and permit delays?

Those questions get past marketing language. They show whether you are hiring a real advocate for your claim, or just signing up with a recognizable logo.

A side-by-side way to evaluate the choice

| Evaluation point | National firm such as Allied | Local PNW firm |

|---|---|---|

| Brand recognition | Easier to find online and may feel more established | Often known through referrals, local reputation, and regional search |

| Systems and staffing | May have more standardized intake and admin support | Often smaller, but communication can feel more direct |

| Local licensing clarity | Needs careful verification for Oregon or Washington | Often easier to confirm because the firm works mainly in the region |

| Regional claim judgment | May know large-loss handling across many states | Often stronger on rain exposure, moisture tracking, smoke migration, and local rebuild conditions |

| Day-to-day contact | Ask whether the assigned adjuster is local and accessible | Often simpler to identify who will inspect and negotiate the claim |

| Repair context | May rely on broader pricing habits and remote coordination | Often better grounded in local trade availability, code issues, and permit timing |

How I would read Allied from a Northwest homeowner's perspective

I would not rule Allied in or out based on size alone.

I would treat them the same way I would treat any national firm. Ask for Oregon or Washington licensing information. Confirm the name of the person who will handle the claim. Ask how many claims they have handled in your state and with your loss type. Then listen to how they explain the process. If the answers are clear, specific, and grounded in local reality, that is a good sign. If the answers stay broad, that is a warning sign.

A local firm has to earn trust too. Being nearby does not automatically mean being better. But in the Pacific Northwest, local presence often helps because the claim issues here are not generic. Wet weather, hidden moisture, smoke behavior, and rebuild bottlenecks can change the value of the claim if the adjuster misses them.

If you want a clearer sense of who represents whom in the claim process, read this comparison of the roles. It helps you ask sharper questions before you sign anything.

A practical standard for deciding

Choose the firm that can show you three things without hedging.

They are properly licensed for your state. They understand your kind of loss in Oregon or Washington. You know exactly who will carry the file from inspection through negotiation.

That is the true comparison. Not national versus local as a slogan. Competent, local-fit claim handling versus uncertainty.

Making the Right Choice for Your Property Recovery

After a serious loss, the claim can feel like one more disaster layered on top of the first one.

The paperwork is technical. The deadlines matter. The pricing can be disputed. Hidden damage can change the scope. And while all of that is happening, you are still trying to live your life.

That is why public adjusters matter. They bring structure to confusion, evidence to disagreement, and advocacy to a process that often feels one-sided. Firms like allied public adjusters have earned attention because they position themselves as strong representatives for policyholders in complex claims.

For Oregon and Washington property owners, though, the smartest decision is not based on branding alone. It is based on fit.

You want a firm that can show you, clearly and without hedging, that it is licensed for your state, comfortable with your type of loss, able to document the full scope of damage, and prepared to negotiate in a way that protects your interests. If the firm is national, verify the local details. If the firm is local, verify the technical depth.

The right adjuster should leave you feeling more informed, not more pressured.

Use the checklist. Ask direct questions. Read the contract. Confirm licensing. Find out who will touch your claim once the papers are signed. Those steps may feel small, but they often separate a smooth recovery from a long, frustrating fight.

If your Oregon or Washington property claim feels bigger than you can handle alone, NW Claims Management offers licensed public adjuster support for homeowners, businesses, nonprofits, and public entities across the Pacific Northwest. Reach out for a free claim evaluation and get clear guidance on your options before you commit to the insurer’s version of the loss.