A lot of Oregon and Washington property owners land in the same place. The storm has passed, the fire is out, the emergency cleanup has started, and then the insurance estimate arrives. You read it once, then again, because the number doesn't look like it matches what contractors are telling you. It feels low, incomplete, or built on assumptions that don't fit your building.

That moment is where many claims go sideways. People think their only choices are to accept the offer or hire a lawyer. In many property policies, there is a third path: the appraisal clause. It can be one of the most effective tools for resolving a disagreement about how much the loss is worth without turning every claim into a lawsuit.

For policyholders in Portland, Seattle, and throughout the Pacific Northwest, that distinction matters. If the fight is about repair scope, pricing, depreciation, or replacement cost, appraisal may be the right tool. If the fight is about whether the policy covers the damage at all, appraisal usually won't solve it. That difference is where people often lose time, advantage, and peace of mind.

If you're comparing your options after a weather event, it can also help to see how claim support works in other regions. This guide on support after Colorado hail storm damage gives a useful outside example of how homeowners start organizing evidence and pushing back when insurer estimates don't match real repair needs. If your dispute has already moved from underpayment into denial territory, this overview on how to fight an insurance claim denial is the better starting point.

Your Guide to Insurance Claim Disputes

When a carrier's number feels detached from the true cost to repair your home or business, the stress isn't just financial. It affects where you'll live, how quickly work can begin, and whether you can successfully restore the property to its pre-loss condition. In Oregon and Washington, I've seen policyholders get stuck because they were arguing the right facts in the wrong forum.

Insurance appraisal services are useful when both sides agree there is covered damage, but they disagree on value. That could mean the cost to replace roofing, the proper scope for smoke cleaning, the pricing for interior finishes, or the actual cash value of damaged property. In plain terms, appraisal is for pricing the loss, not proving coverage exists.

Why this matters in the Pacific Northwest

Regional claims often involve messy fact patterns. A wind event may damage part of a roof, but water enters later. A wildfire claim may involve obvious fire damage plus smoke contamination and cleaning questions. A pipe break may trigger disputes over tear-out, drying, and finish restoration. These losses create two different kinds of arguments:

- Value disputes involve numbers. How much drywall? What labor rate? What quality of flooring? What depreciation is proper?

- Coverage disputes involve policy interpretation. Was the cause excluded? Was there late notice? Did the carrier deny the entire category of damage?

If you use appraisal for a value dispute, it can narrow the case fast. If you try to use it for a coverage fight, you may burn time while the actual issue stays unresolved.

Practical rule: If the insurer says, "we agree there is damage, but not that much," appraisal may fit. If the insurer says, "this damage isn't covered," appraisal usually isn't the tool.

What worried clients need to know first

You don't have to accept a low estimate just because it came on insurer letterhead. You also don't have to treat every disagreement as a courtroom battle. The smart move is to identify the dispute correctly before you spend money, invoke a clause, or hand control to the wrong professional.

What Are Insurance Appraisal Services

Think of appraisal like a dispute between two mechanics after a car crash. One says the repair will require major parts replacement. The other says most of it can be repaired for less. If they can't agree, each side brings in a qualified professional, and if necessary, a neutral tie-breaker helps settle the number. The process isn't about whether the accident happened. It's about what the repair is worth.

That's what insurance appraisal services do in property claims. They help turn disagreement into a structured valuation process.

According to the Bureau of Labor Statistics, insurance appraisers are formally classified as professionals who determine repair costs for claim settlements, which confirms that appraisal is a standardized claim function rather than an informal estimate or guesswork (BLS occupational classification for insurance appraisers).

The clause versus the service

People often use the same word for two related but different things.

| Term | What it means |

|---|---|

| Appraisal clause | The part of the insurance policy that gives the parties a method to resolve a value dispute |

| Insurance appraisal services | The professional work performed by appraisers who inspect, analyze, price, and support the valuation |

The clause is your contractual right. The service is the expert work needed to use that right effectively.

A clause alone doesn't win anything. Someone still has to inspect the damage, understand construction or contents valuation, assemble support, and defend the number.

What appraisal is for

Appraisal is built for disputes such as:

- Repair scope disagreements where both sides accept some damage exists but disagree on what must be repaired or replaced

- Pricing differences where contractor bids, insurer estimates, and market conditions don't line up

- Depreciation disputes where actual cash value calculations look too aggressive

- Replacement cost disputes involving materials, finishes, code-related work, or specialized property

If your claim is in the auto context, the same general logic applies, and this page on auto insurance appraisals gives a parallel example of how valuation disputes are handled in another common insurance setting.

What appraisal is not for

Appraisal is not a magic key for every bad claim outcome.

It usually doesn't decide whether a policy covers a cause of loss. It usually doesn't resolve bad faith allegations. It usually doesn't force payment where the insurer says there is no coverage in the first place.

That distinction matters because policyholders are often told, or assume, that appraisal can fix any underpayment or denial. It can't. It is a strong tool, but it is a specialized one.

If you use a screwdriver like a hammer, the problem isn't the tool. It's that the job required something else.

Why good appraisal work changes outcomes

A weak estimate invites argument. A strong appraisal file narrows it. The difference is documentation, method, and credibility. The best insurance appraisal services don't just produce a number. They show how the number was built and why it fits the actual property, the actual damage, and the actual market.

The Insurance Appraisal Process Step by Step

Appraisal is often imagined as one meeting where experts argue over price. In reality, it's a staged process. Each stage matters, and shortcuts early in the process usually create bigger fights later.

Invoking the clause

The process usually starts with a written demand for appraisal under the policy. The wording matters less than the clarity. You want the carrier to understand that you are invoking the appraisal provision for a dispute over the amount of loss.

Before anyone sends that demand, review the policy language closely. Some policies describe how each party selects an appraiser and how an umpire is chosen if the appraisers can't agree. Dates, deadlines, and notice language can also matter.

Choosing the appraiser

Many policyholders often make a costly mistake. They choose someone who can estimate repairs but can't hold up under a real dispute.

The appraiser's job is larger than writing numbers in Xactimate or copying a contractor quote. The appraiser needs to inspect the property, understand the loss, identify valuation issues, and defend methodology. If the loss is complex, they also need to work comfortably with engineers, contractors, contents specialists, or accountants depending on the claim.

If you're trying to understand the estimating side of claim preparation, Verisk Xactimate training is relevant because many property disputes turn on estimate structure, line-item logic, and how replacement costs are documented.

Building the valuation file

This stage is the backbone of the case. A thorough insurance appraisal report is a replacement cost analysis that includes site inspection photos, detailed measurements, analysis of materials and finishes, and building valuation worksheets. That level of detail turns an estimate into proof-of-loss documentation that parties can use to settle a dispute (replacement cost analysis and documentation details).

A solid file often includes:

- Site documentation such as photographs, room-by-room observations, measurements, and condition notes

- Material analysis covering roofing type, wall finishes, flooring, trim, cabinetry, HVAC, and other building components

- Scope support including contractor input, code-related concerns, and access or sequencing issues

- Valuation worksheets that separate covered repair items from exclusions or non-insurable components

This is the point where a claim stops being "my contractor says" versus "their adjuster says" and becomes an evidence file.

A strong appraisal report should read less like a bid and more like a record.

Appraiser negotiation

Once both appraisers complete their work, they compare valuations and try to narrow the differences. Sometimes the gap is smaller than it looked at the beginning. One side may accept revised measurements. The other may revise pricing or depreciation. Good appraisers don't posture. They isolate the core disagreements.

These discussions can be technical. They may involve unit pricing, repairability, matching issues, overhead and profit questions, or whether certain line items belong in the covered scope.

The umpire phase

If the two appraisers can't resolve all differences, they submit disputed items to an umpire. The umpire doesn't replace the appraisers. The umpire acts as the tie-breaker on unresolved valuation points.

In many claims, the final award is signed when any two of the three agree. That structure matters because it keeps the process moving even when one side refuses to meet in the middle. It is one reason appraisal can work well for amount-of-loss disputes that would otherwise drag on for months.

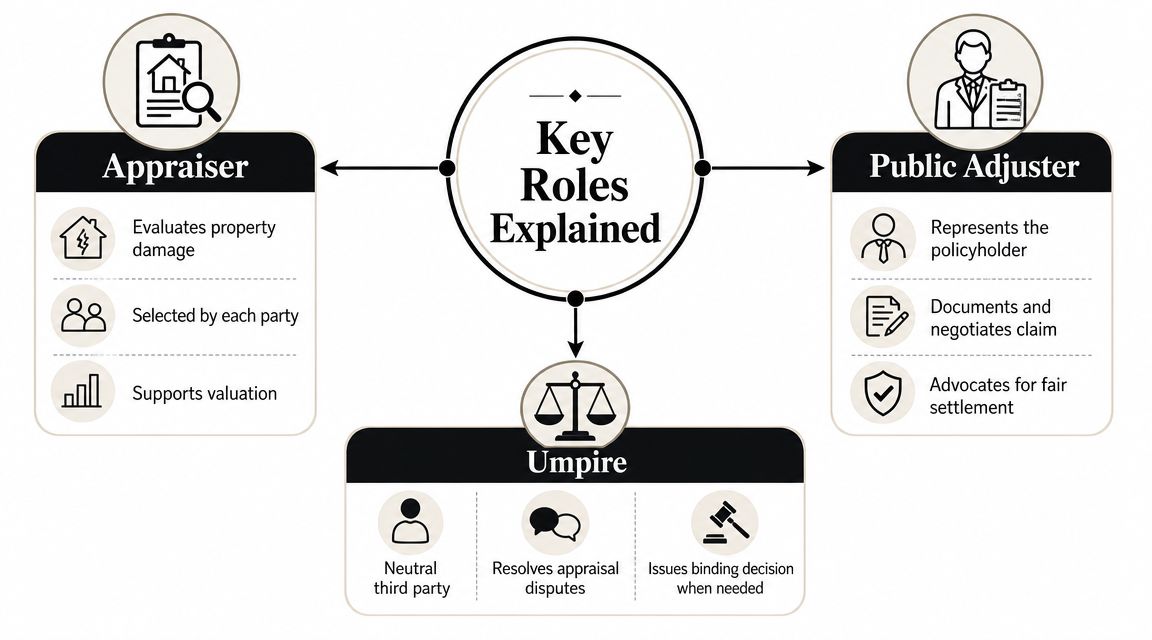

Key Roles Explained Appraiser Umpire and Public Adjuster

A lot of claim problems come from hiring the right person for the wrong job. In Oregon and Washington, that mistake can cost time, money, and position. Appraisal is a tool for deciding value. It is not a substitute for a coverage analysis, and it does not fix a badly prepared claim file.

The appraiser

The appraiser handles valuation. That job is narrower than many policyholders expect and more technical than many insurers admit. A capable appraiser inspects the damage, measures the loss, prices the work, and explains how they reached their numbers in a way an umpire can follow and trust. For a broader industry overview, see this guide to appraiser valuation work.

What separates a weak estimate from a strong appraisal file is documentation, method, and credibility. The appraiser should be able to show how the property was inspected, what information was used, how repair versus replacement decisions were made, and how depreciation or condition affected the valuation.

An appraiser should also stay in their lane. If the carrier says a category of damage is excluded, that is usually a coverage dispute, not an appraisal issue. In practice, that distinction matters a great deal in Oregon and Washington claims, because policyholders are often pushed toward appraisal before anyone clearly addresses whether the policy covers the item in dispute.

The umpire

The umpire is the neutral decision-maker for unresolved value disagreements. The umpire does not advocate for either side. The umpire also should not expand the process into a legal fight about policy interpretation.

Good umpires are disciplined. They review the competing positions, test the support behind each number, and decide the valuation points the appraisers could not resolve themselves. If one side submits a thin file and the other submits photos, measurements, pricing support, and code-related reasoning, the difference usually shows up quickly.

The public adjuster

The public adjuster represents the policyholder. That role starts earlier and reaches wider than the appraiser's role. A public adjuster helps build the claim, review the policy, organize evidence, deal with carrier communications, and decide whether the disagreement belongs in negotiation, appraisal, or something more formal.

If you want a plain-language explanation of that role, this page explains how to define public adjuster. The confusion is common. Homeowners often mix up the insurer's adjuster, the policyholder's public adjuster, and the appraiser. They are not interchangeable.

Here is the practical breakdown:

| Role | Main duty | Whose interests they serve |

|---|---|---|

| Appraiser | Determine the amount of loss | The valuation process |

| Umpire | Resolve valuation deadlock | Neutral role |

| Public adjuster | Advocate for claim presentation and settlement | The policyholder |

Clients usually ask one question first. Who is protecting my side of the claim?

The answer is the public adjuster. The appraiser's job is to produce a supportable value opinion. The umpire's job is to decide unresolved valuation points fairly. If the carrier is denying part of the claim on coverage grounds, a public adjuster helps identify that problem early so you do not spend time and money forcing an appraisal process to answer the wrong question.

NW Claims Management is one example of a licensed public adjusting firm serving Oregon and Washington policyholders with policy review, damage documentation, and settlement advocacy.

The right professional at the right stage can change the outcome. The wrong one can leave you arguing about price when the real dispute is coverage.

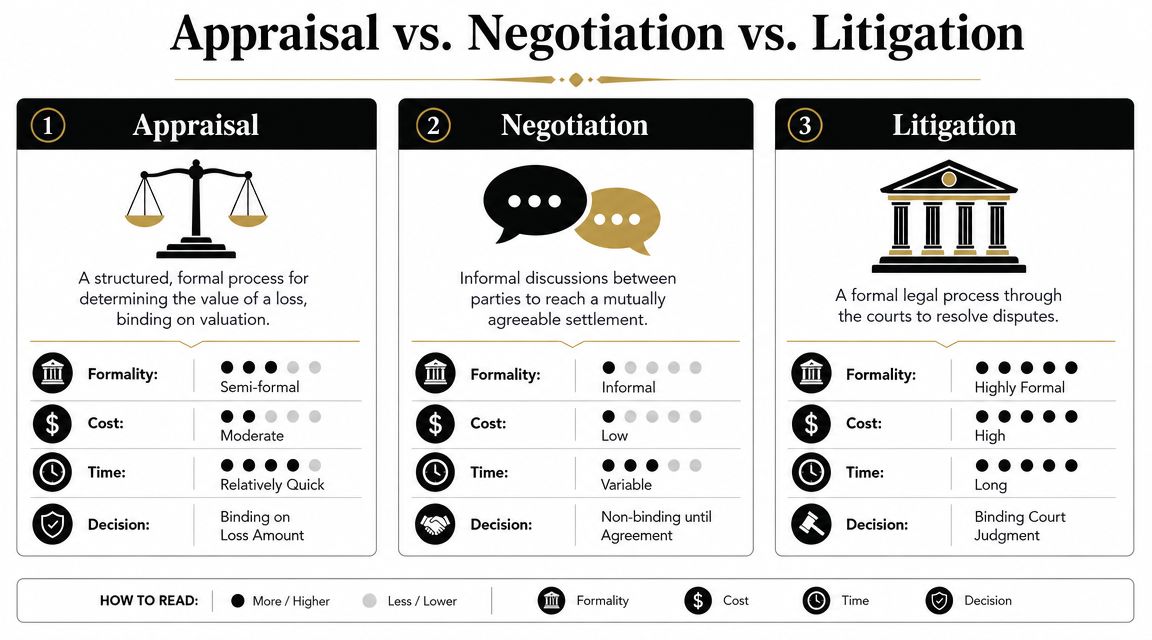

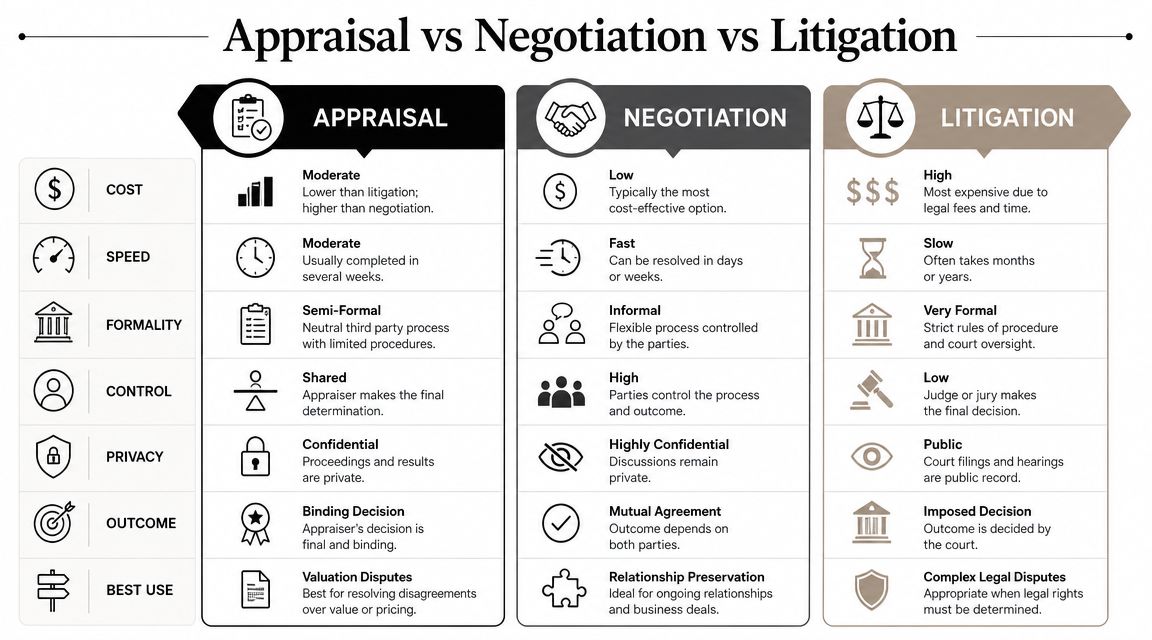

Appraisal vs Negotiation vs Litigation

Most disputes don't begin with appraisal. They begin with negotiation. Some later move to appraisal. A smaller set go all the way into litigation. The right path depends on the kind of disagreement, how entrenched the positions are, and whether coverage is part of the fight.

| Path | Best use | Strength | Limitation |

|---|---|---|---|

| Negotiation | Early disputes where facts are still developing | Flexible and informal | No final answer unless both sides agree |

| Appraisal | Amount-of-loss disputes | Structured and usually faster than court | Narrow scope focused on value |

| Litigation | Coverage disputes, legal violations, complex deadlocks | Can address broader legal issues | Slower, more formal, and more expensive |

When negotiation still makes sense

Negotiation is often the first and cheapest tool. If the disagreement comes from missing documents, an incomplete contractor bid, or a field adjuster who overlooked rooms or line items, direct negotiation may solve it. A revised estimate, better photos, or a more complete scope can move the carrier.

The downside is simple. Negotiation only works if the insurer is willing to move.

When appraisal is the middle ground

Appraisal makes sense when everyone is talking past each other on price. It introduces structure without requiring a full lawsuit. In many claims, that's enough to break the stalemate because the discussion shifts from broad complaint to itemized valuation.

This is why appraisal often feels like the practical middle path. More formal than ordinary back-and-forth. Less burdensome than court. Focused on one question: what is the covered loss worth?

When litigation becomes necessary

Litigation enters when the problem isn't just valuation. If the insurer denies the claim on policy grounds, invokes exclusions, or the dispute includes legal conduct beyond the amount of loss, appraisal may leave the key issue untouched.

Some disputes need a calculator. Others need a judge. The first job is figuring out which one you're dealing with.

Finding the Right Appraiser in Oregon and Washington

The best appraiser for your claim is not just someone with a title. It's someone who understands your type of loss, your type of property, and your local market. In Oregon and Washington, local knowledge isn't a bonus. It changes the valuation.

What local experience looks like

A Portland-area claim and a Seattle-area claim can involve different contractor availability, municipal requirements, material sourcing, and pricing realities. An appraiser who knows the region will usually ask better questions about moisture intrusion, smoke migration, roofing assemblies, access challenges, steep-slope work, and repair sequencing in wet conditions.

Look for someone who can speak concretely about:

- Regional damage patterns such as wind, water intrusion, wildfire, smoke, and tree impact losses

- Local repair conditions including permit habits, labor availability, and contractor workflow in your area

- Property type familiarity from single-family homes to mixed-use buildings, schools, churches, and nonprofit facilities

If you're comparing firms with local claim experience, this page on a claims adjuster near me is a practical place to start.

Red flags that should make you pause

Not every appraiser is a good fit for every claim. Be careful with anyone who relies on generic templates, doesn't inspect thoroughly, or can't explain how they separate valuation issues from policy issues.

A few warning signs:

- No regional footing if they don't understand Pacific Northwest construction realities, expect disconnects in pricing and scope

- Thin documentation if their process is mostly a quick walk-through and a bottom-line number, the file may not hold up

- Overpromising if they suggest appraisal can solve denial, coverage interpretation, and every legal issue at once, they're overselling the process

Special note for commercial and nonprofit properties

Commercial, industrial, and nonprofit properties need a higher level of valuation discipline. Kroll notes that periodic appraisals are important for these organizations because inflation and labor shortages can make valuations outdated quickly, which raises underinsurance risk when a major loss happens (insurance valuation services for complex properties).

That matters in real claims. A school, nonprofit campus, apartment building, or industrial property may involve specialized systems, phased repair work, and replacement-cost assumptions that age badly in volatile markets. The right appraiser needs to account for those moving parts.

In a complex property loss, the appraiser isn't just pricing a building. They're pricing the reality of rebuilding it.

Common Questions About Insurance Appraisal

These are the questions people usually ask once they understand what appraisal is and what it isn't.

Who pays for the appraisal process

Most policies require each side to pay for its own appraiser, while the parties share the umpire cost. The exact wording depends on the policy, so don't assume. Read the clause carefully before invoking it.

The practical point is that appraisal has a cost, but it can still be more efficient than letting a value dispute sit unresolved or forcing every disagreement into formal litigation.

How long does appraisal take

There isn't a universal timeline. The speed depends on the policy language, the complexity of the loss, how quickly inspections happen, how organized the documentation is, and whether the appraisers narrow the issues efficiently.

Simple losses move faster. Large fire losses, complex commercial claims, and disputes involving many line items take longer. Delay usually comes from incomplete records, poor appraiser selection, or fights over issues that don't belong in appraisal.

Is the award binding

In many policies, the appraisal award is binding as to the amount of loss if the process is completed according to the policy terms. That doesn't always mean every issue in the claim disappears. Payment can still involve other policy conditions.

The safe way to think about it is this: appraisal can settle the valuation number, but it doesn't necessarily erase every separate legal or coverage issue surrounding the claim.

Can I use appraisal if my whole claim was denied

Usually, no. A key limitation of appraisal is that it resolves disputes over the amount of loss, not disputes over coverage. If the insurer denies the claim on the ground that the damage isn't covered by the policy, appraisal cannot force payment because that is a coverage issue handled separately (coverage versus amount-of-loss limitation).

This is the distinction most guides gloss over, and it's the one Oregon and Washington policyholders need to get right early.

Should I invoke appraisal right away

Not always. If the dispute comes from a sloppy first estimate, missing rooms, or poor documentation, negotiation may still fix it. Appraisal makes more sense once the disagreement is clearly about value and both sides have enough information to frame the issue properly.

If you're unsure, slow down and identify the dispute before you choose the process.

If you're in Oregon or Washington and you're staring at an estimate or denial that doesn't make sense, NW Claims Management can review the claim, help determine whether the dispute is about value or coverage, and guide the next step so you don't waste time using the wrong tool.