You open the insurer's estimate after a fire, leak, windstorm, or break-in, and the pages feel written in another language. There are line items, abbreviations, category codes, and totals that look precise enough to seem unquestionable. But if you've ever looked at one of these reports and thought, “How did they get this number?” you're asking the right question.

The hard truth is that many property claims are decided long before anyone argues about fairness. They're decided when someone builds the estimate inside the software that insurers and adjusters rely on. If the scope is incomplete, the pricing logic is misunderstood, or key items are left out, the settlement starts low and stays low unless someone knows how to challenge it line by line.

That's where verisk xactimate training matters. Not as a resume badge. Not as a software hobby. As practical skill in the system that often controls what gets paid, what gets questioned, and what gets missed.

Your Insurance Claim's Hidden Language

A homeowner in Oregon might receive an estimate after a kitchen water loss and see charges for demolition, drying, insulation, drywall, paint, and flooring. On the surface, it looks thorough. Then the contractor walks through and says, “This doesn't include everything needed to put the room back correctly.”

That disconnect frustrates people because the estimate looks official. It has categories, quantities, and pricing. It feels final. But what you're really looking at is a translation of damage into software entries. If the person entering the damage speaks that language well, the estimate can be strong. If they don't, your claim can be reduced by omission.

That's why many policyholders get stuck. They know they have serious property damage, but they don't know how that damage gets converted into payment. The insurer's estimate isn't just math. It's interpretation. Even the meaning of “damage” can become a dispute, which is why understanding the broader legal definition of damage in property claims helps people see why scope disagreements happen so often.

Why the estimate feels so hard to challenge

Most homeowners and business owners don't work inside estimating platforms. They compare the insurer's number to what repair professionals say in the field, and the gap can feel impossible to explain.

Here's the plain-language version:

- The insurer speaks in estimate codes. You speak in real repairs.

- The contractor sees tasks. The estimate may separate, bundle, or exclude those tasks.

- Missing items often hide in details. They don't always look dramatic on the page.

Practical rule: If you can't tell how the estimate accounts for every repair step, you shouldn't assume it does.

The claim process gets less confusing when you stop treating the estimate like a verdict and start treating it like a draft written in a specialized language.

What Is Xactimate and Why Does It Control Your Settlement

A water loss hits your Portland kitchen or your Tacoma storefront. The contractor walks through and sees torn-out cabinets, wet insulation, damaged flooring, and finish work that all has to go back in the right order. The insurance carrier then turns that real-world repair into an estimate inside Xactimate. In practice, that estimate often becomes the number your settlement starts from.

Xactimate is a property estimating platform. It organizes room measurements, demolition, repair tasks, material categories, labor, and pricing into one report. For homeowners and business owners, that matters because the claim is usually not negotiated from a blank page. It is negotiated from what someone entered into this system.

A better way to understand it is to picture a rebuilding worksheet with rules. The person writing the estimate has to decide what was damaged, how far the damage extends, what work must happen first, and which line items match the actual repair. If those choices are too narrow, the estimate can look polished while still leaving out work your contractor knows is required.

A bathroom rebuild is a good example. Saying “replace the bathroom” is only the headline. Xactimate breaks that headline into smaller decisions:

- Measurements that control material quantities

- Line items that determine which repair tasks are included

- Labor and material categories that affect pricing

- Report details that shape how the carrier reviews the claim

Small entry errors can change the total in a big way. A missed detach and reset item, an incomplete room sketch, or the wrong repair line can remove work from the estimate without making the omission obvious to a policyholder reading the report.

The user matters more than the software alone. Xactimate gives structure, but it does not guarantee accuracy. The adjuster, estimator, or advocate still makes judgment calls about affected areas, repair sequence, code-related tasks, and whether the estimate returns the property to pre-loss condition. If you want a clearer sense of those responsibilities, it helps to understand what a claims adjuster does during estimate and settlement decisions.

For policyholders in Oregon and Washington, this issue is even more important. Moisture migration, layered repairs, drying-related tear-out, and regional building practices often mean the visible damage is only the front edge of the job. A clean-looking estimate can still miss insulation behind wet walls, trim removal needed to reach damaged materials, or finish work that cannot be restored in isolation.

That is the fundamental reason Xactimate controls settlement. It translates damage into payable line items, and the person who speaks that language best often has the strongest influence over the final number. For an Oregon or Washington policyholder, an advocate with strong Xactimate command is often the single biggest advantage in closing the gap between a low paper estimate and the full cost of proper repair.

How Expert Training Directly Increases Your Payout

There's a direct financial reason to care whether the person writing your estimate has strong Xactimate training. Errors in this software don't stay on a screen. They show up as unpaid work, delayed supplements, and pressure on you to prove what should have been included the first time.

The clearest example comes from Verisk's own training benchmarks. In Verisk's Xactimate User Certification materials, uncertified users can cause a 20-30% underestimation on supplemental claims by overlooking “click for detail” exclusions. The same source says certified users reduce estimate revision cycles by 40% and can increase payouts by 15-25% by correctly documenting non-included items like vapor barriers, which are especially important in the Pacific Northwest.

That sounds abstract until you understand what “click for detail” means.

The hidden trap inside line items

Many Xactimate line items look complete at first glance. A user may select a wall repair item and assume the software included all steps needed for proper restoration. But some line items contain exclusions or notes inside the detail view. Those exclusions can remove tasks a homeowner would reasonably assume are part of the repair.

For example, a repair line may not include prep work or a related material that the contractor must install to complete the job properly. If the estimator never checks the detail, the report can understate the actual cost of the repair.

That's not a minor paperwork issue. It changes what gets paid.

A Pacific Northwest example

In Oregon and Washington, vapor barriers matter. Moisture management matters. Assemblies that stand up to wet conditions matter. If a line item doesn't include a needed component and the estimator fails to add it manually, the estimate may still look professional while missing a real building requirement.

A trained user knows to ask:

- Is this item included?

- What does the detail view exclude?

- What related tasks must be added manually?

- Does the report reflect the repair sequence?

An untrained user may stop after step one.

Why this helps policyholders more than anyone else

When people hear “certification,” they often think of professional pride. In claims, certification should mean practical accuracy. Better sketching catches dimension mistakes. Better line-item judgment catches omitted work. Better reporting creates cleaner support for negotiation.

That's one reason many property owners learn about the benefits of hiring a public adjuster only after they've already accepted that the insurer's estimate feels too low. The value isn't only advocacy in the abstract. It's detailed estimate control.

If the estimate misses part of the repair, the negotiation starts from a weaker foundation. Training fixes the foundation.

What trained Xactimate users do differently

A strong estimate writer usually works with a discipline that homeowners can feel even if they don't know the software. They ask more exact questions. They verify dimensions. They compare field conditions to the estimate details. They don't assume a line item includes everything.

Look for these habits:

- They verify the sketch. A room's measurements drive quantities throughout the file.

- They inspect item detail. They don't trust line items at face value.

- They document omitted components. If the software doesn't automatically include something, they add and justify it.

- They build for negotiation. Their report is easier to defend because the entries match the repair logic.

That's why verisk xactimate training isn't just about passing a test. For policyholders, it's a safeguard against quiet underpayment.

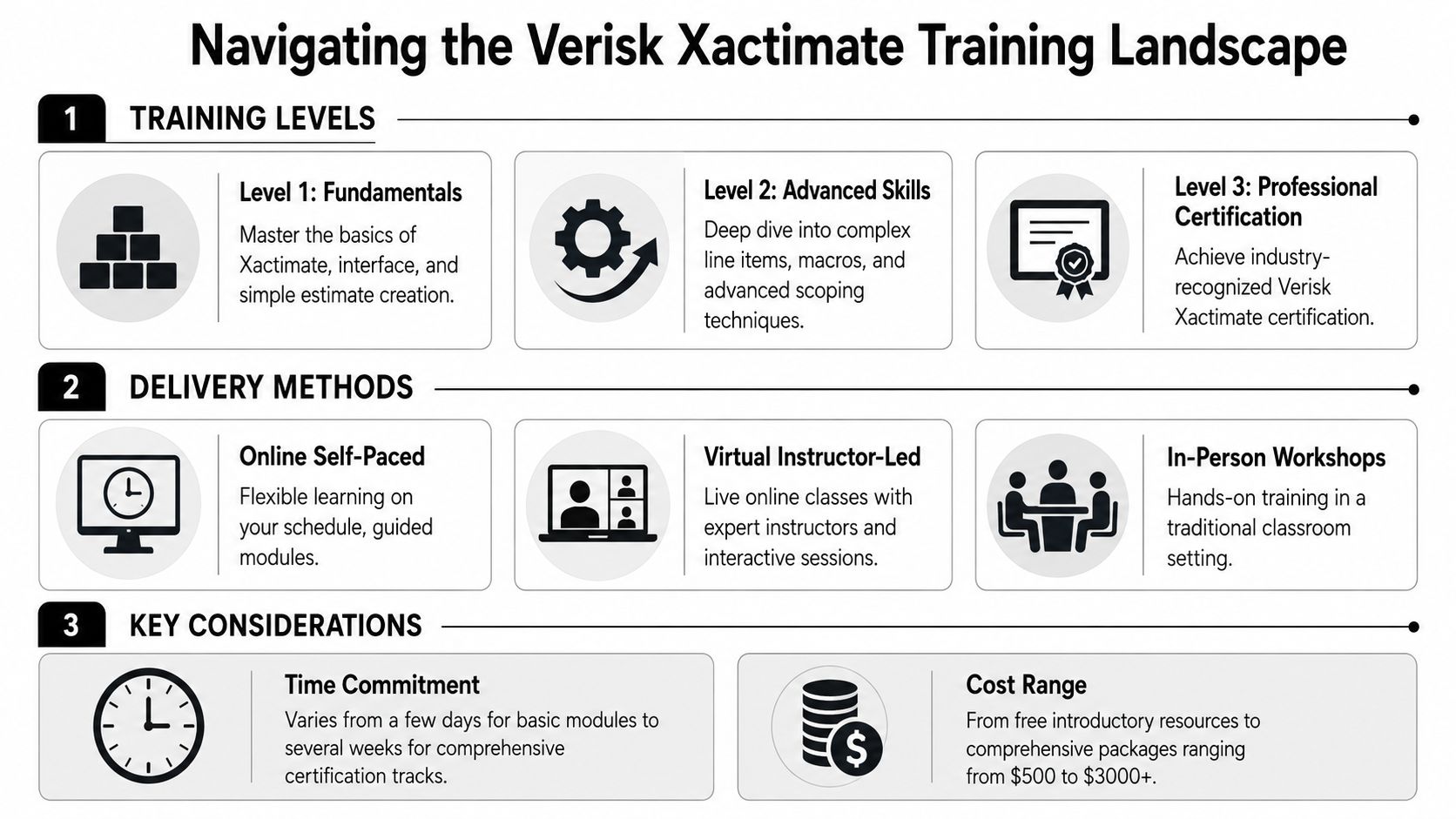

Navigating the Verisk Xactimate Training Landscape

The training world around Xactimate can feel crowded fast. You'll see official Verisk programs, independent trainers, self-paced videos, live virtual classes, and in-person workshops. For most people, the confusion comes from not knowing whether they need software familiarity, exam preparation, or real estimating fluency.

The official Verisk side is the best place to start if you want to understand the ecosystem itself. Verisk has built a wide support structure around Xactimate, not just a single class or exam.

According to Verisk's training support overview, the training ecosystem includes over 1,700 support documents and videos available 24/7, plus instructor-led options such as the three-day Xactimate 28 Training course. The same resource notes that learners can find trainers through Verisk's public Trainer Certification Directory.

The three main ways people learn

Not every learner needs the same format. The best path depends on what you're trying to do with the software.

Official Verisk training

This is the straight-from-the-source option. It tends to align closely with the software's intended workflow and the certification path.

It fits people who want consistency, formal structure, and direct alignment with Verisk's testing standards.

Third-party training providers

Independent educators often teach with more field context. Some focus on adjusters. Others are built for contractors or restoration teams.

These providers can be useful when you want practical examples and industry-specific application rather than software navigation alone.

Self-directed learning

Some people learn by working through support documents, videos, and practice files on their own. This works best for disciplined users who already have claim or construction experience and can connect the software to real repair logic.

Comparing Xactimate Training Options

| Training Type | Best For | Pros | Cons |

|---|---|---|---|

| Official Verisk training | Learners who want source-aligned instruction | Closely tied to certification structure, broad support ecosystem | Can feel technical if you need more field application |

| Third-party instructor-led training | Adjusters, contractors, and estimators who want practical workflow guidance | Often more scenario-based and easier for beginners to apply | Quality varies by provider |

| Self-paced online learning | Independent learners with schedule flexibility needs | Convenient, repeatable, useful for review | Easier to develop gaps if no expert corrects your mistakes |

| In-person workshops | Learners who benefit from live repetition and immediate feedback | Hands-on help, direct questions, structured pace | Requires fixed scheduling and travel in some cases |

What the certification levels actually mean

Verisk's certification path has three levels. Homeowners don't need to memorize them, but it helps to know what they signal.

Level 1

This verifies foundational ability to create an estimate from start to finish. It centers on core functions such as sketching, line item selection, price list use, and report output. For policyholders, this level suggests the user can at least build a basic estimate correctly.

Level 2

This moves beyond the basics into stronger proficiency. At this stage, users are expected to handle more involved estimating work with greater precision.

Level 3

This represents advanced capability within the certification track. For advocacy roles and complex claim environments, higher-level mastery matters because the disputes are rarely simple.

Field insight: A certificate tells you someone studied the platform. It doesn't automatically tell you how well they apply it to contested losses, supplements, or negotiation.

Which delivery method fits which kind of learner

People often choose the wrong format because they confuse convenience with learning fit.

- Self-paced online works when the learner can spot their own errors and revisit material patiently.

- Virtual instructor-led classes help when the learner needs interaction without travel.

- In-person training helps most when repetition, live correction, and hands-on support make the difference.

For homeowners and business owners, the takeaway isn't that you personally need to complete every training level. It's that the person advocating for your estimate should have gone far beyond casual familiarity.

Recommended Learning Paths for Different Roles

A homeowner doesn't need the same Xactimate knowledge as a contractor. A contractor doesn't need the same depth as a public adjuster. Problems start when people expect one level of training to serve every role.

The better question is simple. What do you need Xactimate knowledge for?

Homeowners and business owners

If you own the property, your goal is informed oversight. You don't need to become an estimator. You need enough understanding to ask sharp questions when an estimate feels incomplete.

That usually means learning how to read an estimate at a practical level:

- Recognize room-by-room scope. Can you see which areas are included and which aren't?

- Check whether quantities make sense. If the room is larger than the sketch suggests, the total may already be off.

- Look for missing repair steps. Removal alone isn't restoration.

- Ask for detail when language is vague. “Repair wall” is not the same as a complete explanation of the repair process.

Contractors and restoration teams

Contractors need operational proficiency. They're often comparing actual repair requirements to what the insurer's estimate allows. They don't just need software familiarity. They need enough command to communicate clearly, support supplements, and avoid talking past the adjuster.

For that audience, practical training should focus on the estimate as a job-cost communication tool. The strongest contractor users usually care less about certification language and more about whether they can scope work precisely, identify omissions, and explain why certain tasks must be added.

Public adjusters and claim advocates

Public adjusters need advocacy mastery. They aren't just producing a repair report. They're building a document that must survive scrutiny, support negotiation, and stand up in disputed situations.

For that role, deeper training and stronger certification levels make sense because the work requires:

- Accurate sketching and quantities

- Correct line-item judgment

- Clean file documentation

- Strong supplemental support

- Confidence under pushback

People exploring the profession often look at insurance trainee positions and claim career pathways before they understand how much estimate quality shapes the job. Xactimate fluency is one of the clearest lines between entry-level participation and serious claim advocacy.

You don't need everyone in the claim to be an expert user. You do need at least one person on your side who is.

The practical takeaway

If you're a policyholder, learn enough to spot red flags. If you're a contractor, learn enough to defend scope and support supplements. If you're a public adjuster, aim for mastery because your estimate may become the backbone of the entire negotiation.

Understanding the Investment Cost Time and Certification

Three practical questions arise about verisk xactimate training. How long does it take, what does it cost, and is certification worth it?

For a homeowner in Portland or a business owner in Seattle, those questions are not academic. They connect directly to settlement dollars. If your advocate can read and build an estimate with precision, missed line items are easier to catch, weak scopes are harder for the carrier to defend, and the claim starts to reflect the actual cost of putting the property back together.

The time investment depends on the goal. Someone who only wants basic familiarity may need enough study to read estimates, follow categories, and spot obvious omissions. A claim advocate or public adjuster needs far more. That person has to build accurate sketches, choose the right line items, document support, and defend the file under pressure. Software fluency takes repetition, the same way learning to read blueprints takes repetition. The screen may look simple. The judgment behind each entry is not.

Cost works the same way. There is the price of classes, practice, and testing. Then there is the hidden cost of weak estimating. That second cost is often larger, because errors inside the estimate can lower a claim before negotiations even begin.

For policyholders, that is the key point.

You usually do not need to become the trained user yourself. You need someone on your side who already put in the hours. If you want a clearer sense of what that professional development looks like, review this overview of claims adjuster training programs. It helps explain why stronger training often leads to stronger claim files.

What the investment actually buys

Training pays for more than software familiarity. It buys fewer avoidable mistakes and better judgment in the moments that matter.

| Investment area | What it buys |

|---|---|

| Formal training | A structured understanding of menus, categories, pricing logic, and estimate rules |

| Practice time | Speed, repetition, and the ability to catch errors before they affect the file |

| Certification | Proof that the user met a tested standard inside the platform |

| Field application | Construction judgment, documentation habits, and claim strategy under scrutiny |

Certification has value, but it should be viewed correctly. A certificate shows tested platform knowledge. It does not guarantee that the person can handle a disputed moisture claim in Eugene, a smoke loss in Tacoma, or a commercial interruption claim where scope gaps can cost thousands. Real claim strength comes from combining software skill with repair logic and disciplined file support.

That distinction matters because Xactimate works like a calculator loaded with construction assumptions. If the person using it enters the wrong measurements, skips a necessary task, or chooses a line item that does not match the repair sequence, the output still looks polished. It is just wrong. Training reduces that risk. Experience reduces it further.

Time matters because claims happen under stress

No one studies estimating software during a calm season of life. Training matters because claims arrive when people are tired, displaced, and trying to make fast decisions. Under that kind of pressure, an inexperienced user often accepts the first estimate that looks reasonable on the page.

A trained advocate is more likely to slow the file down and ask the right questions. Was demolition fully captured? Was drying or containment included? Does the repair sequence match how restoration happens in the field? For a practical picture of that real-world repair flow, Wheeler Painting's 2026 restoration guide is a useful reference.

For Oregon and Washington policyholders, this section comes down to one simple idea. The money spent on serious Xactimate training is often small compared with the money lost when your side lacks command of the estimating language that controls the claim.

Special Considerations for Oregon and Washington Claims

Property claims in Oregon and Washington aren't generic. Local weather, moisture exposure, building practices, and urban labor conditions affect how repairs should be scoped and valued. A user who understands Xactimate in the abstract is useful. A user who understands it in the Pacific Northwest is more valuable.

One place local context matters is repair sequencing. In the Pacific Northwest, moisture-related conditions often make it important to think carefully about what has to be opened, dried, cleaned, replaced, and protected. The estimate has to reflect that sequence, not just the visible finish damage.

For property owners trying to understand restoration steps before or during a claim, Wheeler Painting's 2026 restoration guide offers a useful overview of how restoration companies approach damaged properties. It's a practical companion when you're comparing on-the-ground repair needs with what appears in an insurance estimate.

Why local pricing and local logic both matter

Xactimate relies on price lists, but price alone doesn't solve claim accuracy. A perfectly priced line item still fails if it's the wrong line item or if the estimate leaves out part of the work.

In Oregon and Washington, strong estimate writers tend to focus on questions like these:

- Does the scope reflect moisture exposure realistically?

- Are the affected areas measured precisely, not roughly?

- Do the repair steps match how local contractors will perform the work?

- Have weather-related assemblies and materials been documented fully?

The local advocate's advantage

A capable public adjuster in the Northwest doesn't just know Xactimate screens. They know how local claim conditions show up inside the file. They understand that a roof issue in western Washington may require different documentation concerns than an interior water loss in Portland. They understand that moisture-related claims often create disputes about what is affected versus what is merely adjacent.

That blend of software skill and regional judgment is why many people look into claims adjuster training for Oregon and Washington claim professionals when they want to understand how serious advocates are developed.

In the Pacific Northwest, a clean estimate isn't enough. It has to reflect the way buildings here are repaired in real life.

What homeowners should listen for

When you speak with anyone reviewing your loss, listen for specificity. Do they talk in generic terms, or do they connect the estimate to actual repair conditions on your property?

The people who understand local claims well usually ask better questions. They want dimensions, assemblies, sequencing, and documentation. That's a good sign because those are the ingredients of a stronger Xactimate file.

Your Next Step Toward a Fair and Full Recovery

By the time many individuals start reading about Xactimate, they're already under stress. Their home is torn apart, their business is interrupted, or they're trying to make sense of a number that doesn't seem to match reality. At that point, the software can feel like the problem.

It isn't. The core issue is who's using it, how well they understand it, and whether they can turn that knowledge into a complete, defensible estimate.

That distinction matters because training conversations often stop too early. People ask whether someone is certified. They ask what class they took. They ask whether they know the platform. Those are fair questions, but they're not the final ones.

According to the gap analysis summarized in this research discussion on Xactimate training outcomes, there's a significant gap between exam-focused training and clear public data showing how certification translates into higher settlement values for public adjusters. The practical lesson is simple. You shouldn't evaluate an advocate by certificates alone. You should evaluate whether they know how to use Xactimate mastery to produce better claim outcomes.

What to look for in a real advocate

A strong advocate usually shows their value in the way they think, not just in the badges they hold.

Look for someone who can:

- Explain the estimate in plain English. If they can't translate it for you, they may not understand it thoroughly enough.

- Identify omissions with specificity. “It seems low” is weaker than “this report excludes required repair components.”

- Connect software entries to field reality. The best estimate writers understand what contractors really need to do.

- Document the file for negotiation. An argument is stronger when the estimate supports it line by line.

Why this is your biggest lever

Many parts of a claim feel outside your control. The carrier has its process. The policy has its wording. The damage has already happened. But the estimate itself remains one of the few places where skilled human judgment can materially change the outcome.

If the estimate is weak, everything downstream gets harder. If the estimate is disciplined, complete, and well-supported, your position improves before the negotiation even begins.

That's why verisk xactimate training matters so much to policyholders in Oregon and Washington. It gives your side a way to challenge missing scope, defend necessary repairs, and speak clearly inside the same system the insurer uses.

The simplest next move

If you are reviewing a confusing estimate right now, do not focus only on the bottom-line number. Ask who prepared it. Ask how they accounted for the full repair sequence. Ask whether the line items were checked in detail. Ask whether the estimate reflects the actual conditions at your property.

Those questions won't rebuild your home on their own. But they will point you toward the person who can.

If you need help translating a confusing estimate into a fair claim strategy, NW Claims Management helps Oregon and Washington policyholders evaluate property losses, document damage thoroughly, and negotiate for a fuller recovery. If your insurer's numbers don't seem to match the actual cost of repair, a professional review can show what's missing and what to do next.